Before I introduce this company, it is important that we understand some of the common operation metrics used to evaluate hospitals:

- Occupancy Rate - % of hospital beds occupied by patients. Higher the better.

- ARPOB – Average revenue per occupied bed. Higher the better.

- ALOS – Average length of stay (days between admission and discharge). Generally, lower the better.

Why? Because, lower ALOS means higher bed turn-around to accommodate more patients. Also because most of the hospital earnings comes from the initial few days of admission during initial tests and procedures compared to the later part of stay for monitoring and recovery.

The Indian Healthcare sector

-

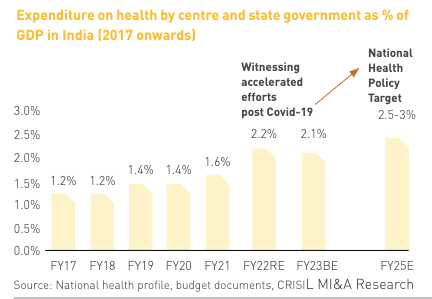

Increasing public, state and government expenditure on healthcare:

-

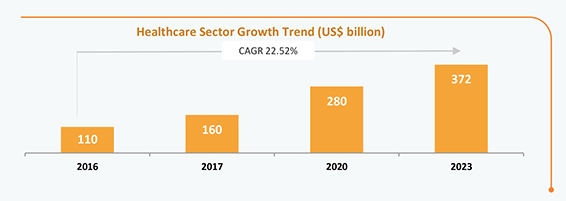

The Indian Healthcare sector market size is growing much faster than many other industries:

-

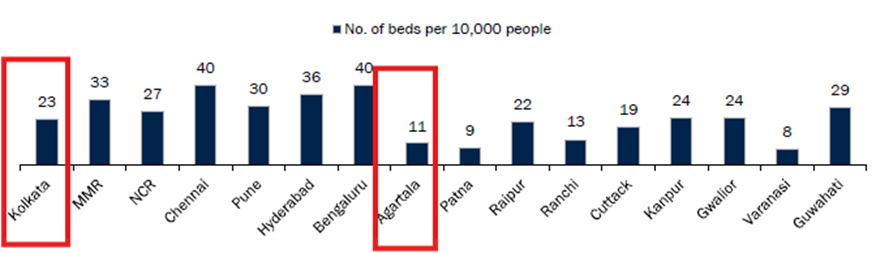

Even today, India’s healthcare system is inadequate. When compared to the Indian government’s defined standards, India is 16% below the number of primary health centers and approximately 50% below the number of community health centers it should have.

-

India is among the global leader destinations for international patients seeking advanced treatment. Indian medical tourism market was valued at US$ 7.69 billion in 2024 and is expected to reach US$ 14.31 billion by 2029.

About the company

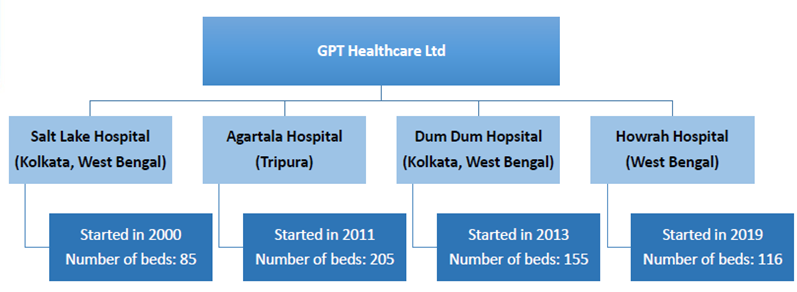

GPT Healthcare Limited is a leading healthcare provider with a strong presence in East India. East India is densely populated but under-penetrated when it comes to healthcare. It is a small-cap company with a market cap of just 1600Cr. Their current bed capacity is 561 beds spread across 4 hospitals. Their ambitious goal is to become a 1,000-bed hospital chain in the next two to three years with expansion plans to other Tier-2 cities of Eastern India.

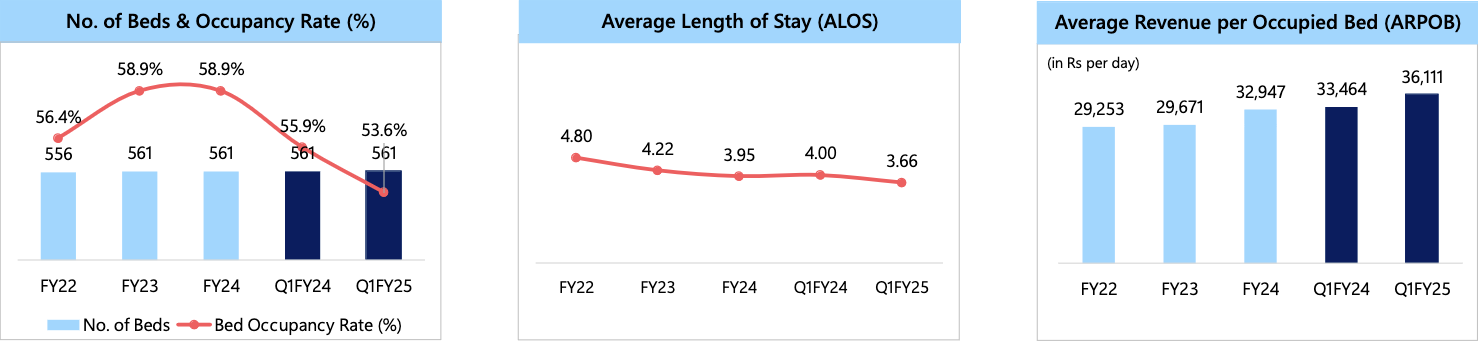

Operational performance of hospital chain

-

ALOS has consistently been on a declining trend, which is a major positive. Occupancy declining is also primarily because of ALOS reducing. But eventually, as the hospital starts taking in more patients, the occupancy increases, with lower ALOS leading to higher ARPOB.

-

Increasing ARPOB is a result of company’s consistent revision in pricing of services, along with improved case mix. Apart from that, the starting of speciality cases like robotic or replacements, even to an extent the oncology services has contributed to ARPOB improvement.

-

Total patient volume has grown at a CAGR of 18% over the last 3 years

In the coming section let’s dissect each of the 4 hospital’s performance in detail.

#1 – Salt Lake Hospital, West Bengal

- Number of beds – 85

- Occupancy – 61% (FY24), 56% (Q1FY25)

- ARPOB – Rs 34,083 per day (FY24). Has already increased to Rs 40,000 for Q1 FY25.

- ALOS – 2.78 days (Q1 FY25) compared to 3.32 days (Q1 FY24).

- Recent tech advancement: Investment in surgical robot in this hospital.

- New services offered: has revamped its Gastroenterology Department infrastructure to attract more patients.

- Take away: Diversifying specialty mix. The reduced ALOS was a strategic effort and hence has also lead to a reduction in occupancy this quarter, serves as a good runway to take in more patients.

#2 – Dum Dum Hospital, West Bengal

- Number of beds – 155

- Occupancy – 77% (FY24), 70% (Q1FY25)

- ARPOB – Rs 38,164 per day (FY24). Has increased to Rs 40,328 for Q1 FY25.

- ALOS – 4.6 days (Q1 FY25) compared to 5.3 days (Q1 FY24)

- Recent tech advancement: invested in 3D cath facilities to enable interventional

- neurology cases in this hospital.

- Take away: Higher occupancy is due to higher number of tertiary cases (well known for renal transplants), hence bringing down ALOS was a strategic move which has played out well. They expect to increase the number of admissions with the same bed count due to decrease in ALOS.

#3 - Howrah Hospital, West Bengal

- Number of beds – 116

- Occupancy – 44% (FY24), 37% (Q1 FY25)

- ARPOB – Rs 27667 per day (FY24). Has increased to Rs 32,818 for Q1 FY25.

- ALOS – Figures are not mentioned

- Take away: Lower Q1 occupancy is primarily due to the effect of elections, for Q2, they are guiding for more than 50%. Hospital revenue and patient volume is rising. It is a fairly new hospital which has not yet hit maturity. 1,200 admissions in FY24 compared to 1,100 for FY23.

#4 – Agartala Hospital, Tripura

- Number of beds – 205

- Occupancy – 53% (FY24), 47% (Q1 FY25)

- ARPOB – Rs 29,134 per day (FY24). Rs 31,041 (Q1 FY25)

- ALOS – 4.74 days (Q1 FY25) compared to 5.19 days (Q1 FY24)

- New services offered: Plans to open a new Cancer Care Department (Radiation Oncology), PET CT and the LINAC early in FY 2025. Equipment installation has already commenced. The company also intends to commence a state-of-the-art diabetic clinic in this hospital to strengthen its offerings.

- Take away: Their largest hospital, the only corporate hospital in Agartala. Guidance to boost occupancy to 70-75% matching Dum Dum numbers. Occupancy has already improved to 50% in July. Around 5-7% patients come from Bangladesh which may be temporarily affected due to the crisis there.

Capex plans

Two new hospitals being added:

-

Raipur, Chhattisgarh: 155 bed hospital in Pachpedi Naka (heart of the city). It is to be commissioned in FY25 itself (operations starting around Feb’25). In vitro fertilization (IVF) also a planned offering. Company has spent around Rs 5-7Cr on CWIP.

-

Ranchi, Jharkhand: 140 bed hospital to be set up on Line Tank Road (heart of the city). Planned to be commissioned in FY27. So far company has not spent anything as it is still on approvals stage (only initial security deposit).

Important points about the capex:

-

The company is following an asset light model with the land and the building. The land and the building is on a long-term lease from the developer. So that is why the capex per bed is about 40% cheaper.

-

The rental lease will be around Rs 3-4Cr per hospital per year with an agreed upon increase every 3 years.

-

Investment of Rs70-80 lakhs per bed.

-

Upfront expenses of around Rs 55 Cr per hospital.

-

Generally, the current hospitals have taken 8-10 months to break even. But since both Raipur and Ranchi are new (greenfield) territories, they expect it to breakeven in 15-18 months.

-

Initially, until the new hospitals break-even, company expect to sustain cash loss of Rs 5-10Cr, beyond which it will sustain itself due to negative working cycle, they do not need a lot of working capital for daily functioning.

-

Company expects the new hospitals to reach Rs 36000 ARPOB in 3-4 years

-

Company is also looking for inorganic expansion opportunities (brownfield), however, this would not be an asset light model. But the hospital will be operational from day 1. They are scouting for opportunities but did not comment on it further.

Management guidance

- Aim to be a 1000 bed hospital in 2-3 years

- Revenue growth of 12-14% expected in FY25 from the existing 4 hospitals

- EBIDTA Margin to improve to 24% in FY25

- ARPOB growth is sustainable and is expected to continue to grow

- Cash flow from operations to EBITDA conversion at 80% for FY25

- Agartala hospital occupancy to hit 70-75% in 1-1.5 years

- They are currently at a 36-40Cr monthly revenue run rate for Q2. Should be better than Q1, subdued due to elections.

Valuation

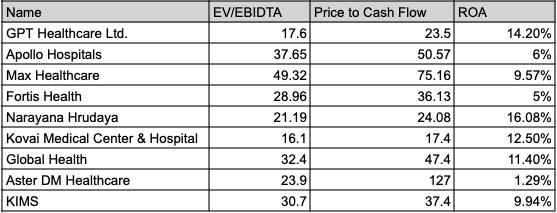

I’ll use this section to help value the hospital industry better. Hospitals and healthcare, much like the hotel industry, is an asset-heavy industry. In asset-heavy companies, you have to account for asset depreciation! Depreciation cost for GPT Healthcare in FY24 was Rs 18Cr, while the operating profit itself was Rs 87Cr. Hence, the P&L statement looks optically depressed, even though, the assets last for several decades and are non-cash expenses! For this reason, along with PE, we also look at EV/EBIDTA which is a better metric for comparison in asset heavy industries.

Another interesting point is that hospitals are cash rich. GPT Healthcare’s net profit for FY’24 was Rs 48Cr while its cash from operations was Rs 69Cr! This is again because of high depreciation cost which is non-cash expense. Then don’t you think Price to Cash flow is a better metric for comparison of hospitals than PE?

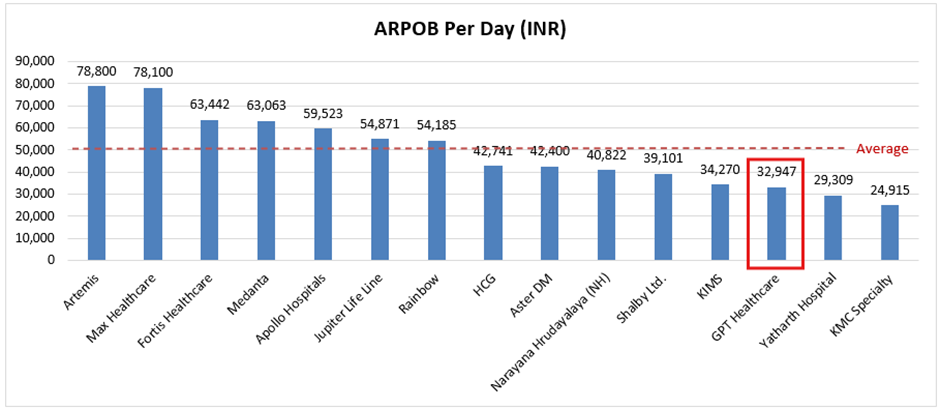

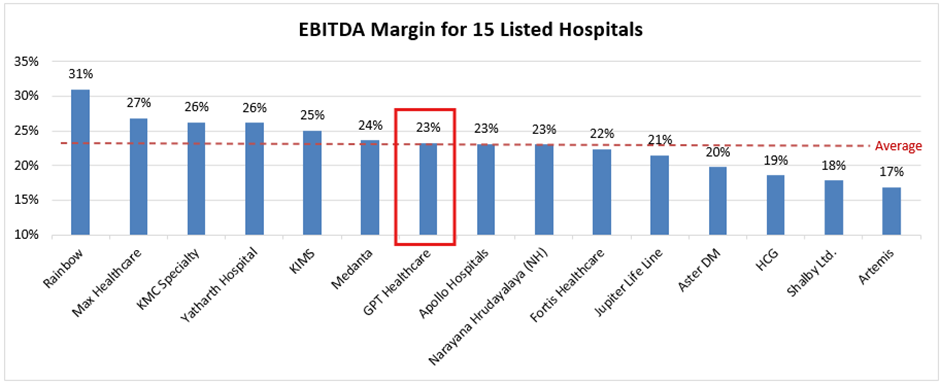

Let’s compare GPT Healthcare to some of its peers:

Risk analysis

-

Often, the most successful hospital chains follow a Hub & Spoke expansion strategy in a city where you have one big hospital as a hub and several smaller hospitals that act as spokes to serve the local population in that region. In case of specialized treatment or complicated cases, the spoke can redirect the patient to the hub with better facilities. This eventually aids in cluster based expansion by implementing hub & spoke strategy in every State. The spoke also has a lower capex per bed. GPT Healthcare however have chosen the greenfield capex route early on in their expansion to Ranchi and Raipur justifying the severe under-penetration of healthcare in the entire east region. Was cluster based expansion to capture one of the cities a better option?

-

Beyond business profitability, the company is deeply committed to making healthcare affordable to the community. This is in contrasting view to pure play capitalism, and might affect decision making towards the interest of the public rather than the company.

Disclosure

Invested with 5% of portfolio allocation in the company from lower levels

What do you guys think of the company? ![]()