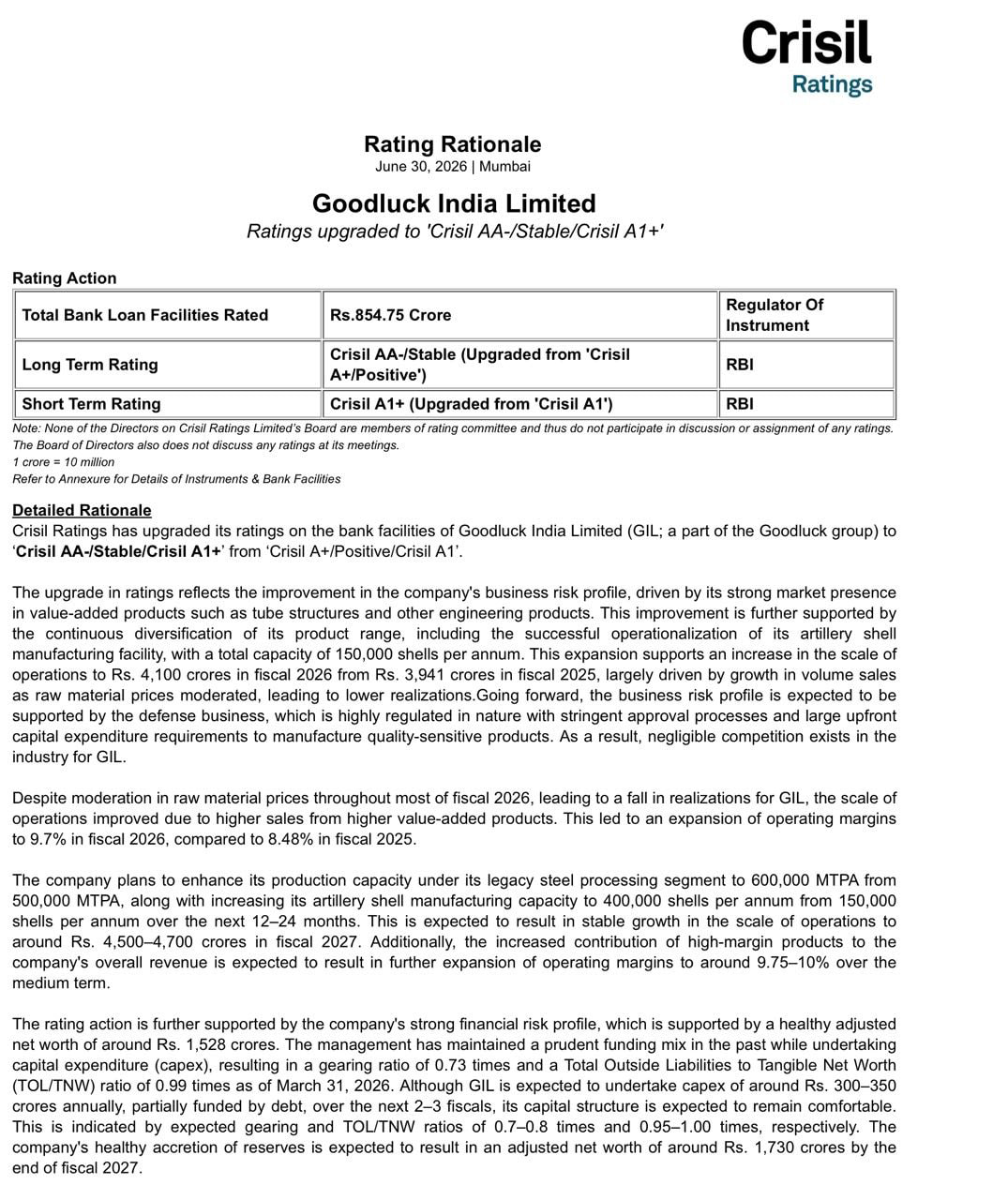

7 months old but good comprehensive analysis of Goodluck’s business. I think PE expansion is unlikely from hereon in near term due to lack of such a trigger from both revenue as well as margin front. At this price stock seems to be a 15-20% compounder.

4 Likes

The stock has corrected more than 18% from tomorrow based on the guidence given by the promotor. Earlier, they mentioned their topline would be between 15-20% and based on the yesterday guidance it would 12% for FY26. Merely, difference of 3% the stock has correct so much. Am i missing some thing here? or approval of defence division would be taking longer time than expected

Three major points to note:

- Guidance revised downwards

- Defence approval still pending (market was presuming this has already come, especially after the recent entry by SBI Funds Management)

- Low float leading to slight overreaction

Overall, the interview was a little disappointing and was far from something that would increase the confidence of the investors

Disc: Not a recommendation

5 Likes

just fyi the interview Devesh mentioned

1 Like

Expansion in production capacity to manufacture empty shells from 1,50,000 Nos. to 4,00,000

Nos. within one year with an investment to the tune of approx. Rs. 500 Crore.

Context - from the Q1 FY26 concall held on July 23rd:

" Mahesh Chandra Garg: As per our perception, there is a huge appetite for this kind of shell. Very huge appetite today"

and

“Ram Agarwal: The revenue, which we are expecting, it is just on the basis what the future will tell, but we hope it should be between – when full capacity will be utilized, it should be almost INR270 crores to INR275 crores”

So if we take 275 crores, 400000 shells at peak capacity should bring in around Rs 733 crores annually (of course domestic vs export mix would change the realisations).

7 Likes

In recent interview of Ram Aggarwal in NDTV, he has mentioned that they have acquired relevant licences for new plant. And are looking to start trial run from Q3 of FY2026

2 Likes

Solid concall for the quarter, good insights on Defence and Aerospace vertical:-

- Hopeful of H2>H1 and demand revival in H2.

- Debottlenecking a constant process, 50,000 tons capacity addition will be across the board.

- AMCA EOI bidded under Goodluck India, if won revenues will flow into Goodluck India.

- Hydraulics Plant: Expansion to 1 Lakh tons will happen once 80 pct utilization is done. Expect 70% utilization by the end of FY26. Q3 was 50% utilization.

- 100 Crores revenue expected from Defence vertical in FY26. There was an article recently that said we have also bid for Ramjet 155 MM Munition as well. Denied

- Operational:

a. Monsoon, low steel prices, geopolitical tensions led to subdued performance

in the quarter.

b. EBITDA margins improving by around 2 pct YoY. - Goodluck Defence:

a. 100 Crores revenue from Oct to March 26 . 30-40% utilization in FY26.

c. 400-500 Crores Capex. Equity:Debt- not finalized. Will finalize soon.

d. Margins will be 30-35% in Shells. Peak turnover will be 1000 Crores post this capex and ebitda will be 30-35%.

e. The entire capex of 500 Crores isn’t only for defence. Will be doing some outer parts of the missile. (More clarity pending here).

f. Expecting it to cease to be a subsidiary post public issue. Current shareholders will be rewarded with whatever ratio the company decides.

g. Aerospace: These pdts are being used by HAL, DRDO, Tata and Godrej aerospace. Expecting 800 Crores from Shells and 200 Crores from other businesses including Aerospace. - Solar Structure: Expect 500-600 Crores business from the solar structure business

alone in the next 2 years.

Goodluck India trades at a Mcap of 3700 Crores odd ; The core business will grow in lower double digits and Defence and Aerospace will add significantly to the company’s EBITDA and bottomline not as much to the topline in comparison. Fair to assume a utilization of 70-80% in FY27 (250-280 Crores Defence revenues at 30-35% EBITDA) and in H2 FY27, expect new capacity to kick in (Total 4 Lakh Shells capacity). FY28 can be 60-70% utilization(in case dedicated capacity for clients) on total capacity that brings about 2.5-2.8 Lakh Shells in FY28.

Each shell costs 25-28000 INR at current prices, a bit more for exports(and in some tenders upto 35k per shell). At 25000 Rs and 2.5 lakh shells sold- Revenue itself can be north of 600-650 Crores from Defence in FY28 and 180-220 Crores of additional EBITDA on consol level.

Hiving off the defence vertical will ensure no Hold Co discount for Goodluck India shareholders and better value unlocking by separate listing (that’s the indication given in today’s call). Good days ahead.

Disc: Invested and Biased

11 Likes

How the ipo of defence and aerospace benefit to existing share holders instead of demerger?

try to understand

Goodluck India -

Q2 FY 26 results and concall highlights -

Q2 outcomes -

Revenues - 997 vs 980 cr, up 2 pc

EBITDA - 98 vs 75 cr, up 30 pc ( margins @ 9.8 vs 7.7 )

PAT - 42 vs 36 cr, up 18 pc

H1 outcomes -

Revenues - 1951 vs 1871 cr, up 4 pc

EBITDA - 193 vs 155 cr, up 25 pc ( margins @ 9.8 vs 8.2 pc )

PAT - 82 vs 72 cr, up 15 pc ( adjusted for exceptional items )

Company’s capacity utilisation stood at 90 pc at the end of H1 FY 26

H1 breakup of domestic : international revenues @ 73:27

Breakup of segment wise revenues -

Engineering structures and fabrications - 23 pc

Forgings - 16 pc

Precision pipes and Auto tubes - 25 pc

CR sheets and pipes - 36 pc

Company’s key clients and End user industries -

Precision Tubes and Auto tubes - BMW, VW, Skoda, Audi, Mercedes, GM, Renault, Toyota, Mahindra Electric, Tata Motors, Bajaj Auto, TVS, Ashok Leyland, Talbros, Gabriel, Suzuki

End user industries - automobiles, aerospace, defence, railways, oil and gas

Forgings - L&T, RIL, IOL, Toshiba, Mitsubishi, BHEL, GE, Allied Group, Saint Gobain, Bharat Petroleum, HAL, DRDO, ISRO

End user Industries - aerospace, defence, construction and earth moving equipment, nuclear power, oil and gas, general engineering

Engineering Structures - GMR, ABB, L&T, RIL, Toshiba, TRF ( Tata group ), Power Grid, Reliance group, Indian Railways

End user industries - roads, railways, telecom, boilers, turbine generators, steel and concrete grinders, solar energy, building structures

CR Coils and ERW Tubes - various Public and private sector EPC players involved in infra build up in the country, state Govts, NHAI, Railways

End user industries - railways, road bridges, support structures

Manufacturing plants -

06 plants near Delhi ( Sikandrabad and Dadri )

01 plant in Kutchh ( Gujarat )

05 major warehouses located @ Faridabad, Rudrapur, Ludhiana, Nahsik and Aurangabad

Key Business segment capacities ( as on Mar 25 ) -

Engineering structures and precision fabrications capacity @ 85k MTPA

Forging products capacity @ 30k MTPA

Precision Pipes capacity @ 170k MTPA

CR Coils, Pipes and Tubes capacity @ 215k MTPA

Comments from year ending Mar 25 Concall -

New Plant - In January 2025, the company commissioned a state-of-the-art hydraulic tubes unit in Bulandshahr, Uttar Pradesh, with a 50,000 MT capacity. These high-precision tubes serve as an import substitute for seamless tubes, supporting foreign exchange savings and driving topline and bottom-line growth for the company

Goodluck India Ltd will begin trial production in Q1 FY26 at the new facility of its subsidiary, Goodluck Defence and Aerospace Ltd, in Sikandrabad, Bulandshahr (U.P.). Designed to produce ~150,000 precision components annually; commercial production expected by end-Q2 FY26

Precision Pipe (CDW) Ramp-Up - CDW ( cold drawn welded ) facility is currently in the production ramp-up phase, with full-scale production expected by Sep/Oct 2025 to meet targeted demand

The new Defence manufacturing plant has a peak revenue potential of aprox 270 - 300 cr ( should be able to achieve the same by FY 27 ). Should be able to clock 100-120 cr revenues for FY 26. Company may go for further expansion on defence manufacturing capacity once they achieve > 70 pc plant capacity utilisation on this plant. The Defence manufacturing plant should clock EBITDA margins in the range of 20 pc or so

In medium term, company hopes to start clocking double digit EBITDA margins. Most of the fresh capex ( in near future ) shall be dedicated to Auto tubes and Defence manufacturing units. These segments have 12-13 pc and 20-21 pc kind of EBITDA margins respectively. These should pull up company’s consolidated EBITDA margins

Company is already supplying 155 mm Artillery shells to MoD and metal parts for Brahmos Missiles. Seeing a lot of interest from multiple customers wrt the upcoming defence manufacturing facility. Utilising those capacities should not be a problem for the companies. In all probability, they ll have to go for additional capex in not so distant future

The CR sheets and coils business clocks a 4 pc kind of margins. It’s a legacy but stable business. Even in this business, company is looking @ 100 bps kind of margin expansion over next 2-3 yrs

Margin profile for their engineering structures business is 9-10 pc

Comments from Q1 concall -

The hydraulic tubes plant in Bulandshahr, commissioned in Jan 2025, contributed meaningfully in Q1 FY26

This facility is an import-substitute initiative aimed at reducing India’s reliance on seamless tube imports,

while enhancing Goodluck’s margin profile

Notes form Q2 concall -

Goodluck Defence and aerospace ( plant inaugurated in Oct 25 ) has got license from MoD to artillery shells across all calibers ie 105 mm, 120 mm, 125 mm, 130 mm, 155 mm. Current capacity @ 1.5 lakh shells / yr. Plan to scale up production to 4 lakh shells / yr in next 12 months. This plant commenced production in Oct itself

Company is in active negotiations with domestic and international defence customers. Should unlock a significant revenue stream for the company. This also demonstrates company’s precision engineering expertise

Company is augmenting their capacity for solar support structures, including tracker tubes to cater to both domestic and export mkts. Over next 1-2 yrs, targeting a revenue of Rs 500-600 cr from this segment alone

Once the Hydraulic tubes plant reaches a capacity utilisation of 80 pc, company shall further expand its capacity by adding another 50k MTPA

Company expects its EBITDA margins to remain in the 9.5-10 pc band for foreseeable future

The eventual revenue potential of company’s Arty Shells plant ( @ production levels of 4 lakh / yr ) should be aprox 1000 cr / yr

H2 is likely to be much better than H1 as Govt orders and Private capex demand in H2 is always better + the weather is supportive

Company expects the newly commissioned hydraulics plant to ramp up to 70 pc capacity utilisation by Mar 26

Goodluck defence should contribute 100 cr and 300 cr in revenues in FY 26 and FY 27 respectively

Company as applied for ( EOI ) for supply of parts for AMCA program. Waiting for RFQ from GoI

Arty shells business is expected to operate @ > 30 pc EBITDA margins

Total capex requirement to reach an annual capacity of 4 lakh shells shall be aprox 500 cr ( out of which, 200 cr have already been spent to reach the capacity of 1.5 lakh shells / yr )

Still guiding for a 15-20 pc topline growth for FY 26 - indicating a strong H2

Wrt Arty shells, demand is > supply. Company has good visibility of revenues from this product for next 2 yrs. Should be able to realise 1000 cr in revenues by FY 28 from Goodluck Defence ( 800 cr from shells + 200 cr from aerospace parts )

Company shall also be manufacturing some aero space parts from the same facility ( ie of Goodluck Dfence and Aerospace ). Have not yet disclosed the details of those parts

Should clock 500 cr kind of revenues from solar structures and tracker tubes in FY 27 ( from 250 cr / yr at present ). EBITDA margins in this business are around 7-8 pc

Disc: not holding, planning to add, not SEBI registered, not a buy/sell recommendation, posted only for educational purposes

12 Likes

3 Likes

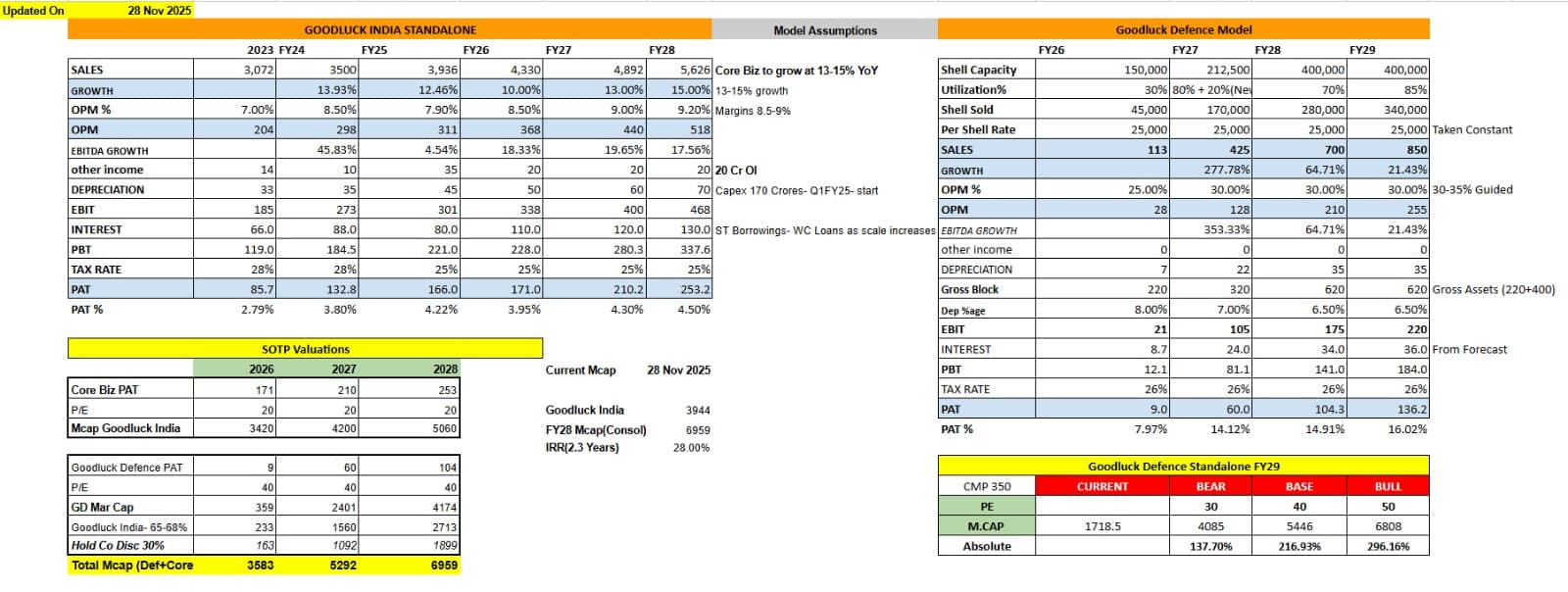

Here’s a quick model for Goodluck India:

The variance could largely be in the dilution that could happen in Goodluck Defence for the parent company during the 400-500 Crores fundraise. In the above interview Mr. Garg mentions his plans to forward integrate in the defence vertical (Complete artillery shell?- That’s where approx 2-2.5x value add is assuming 300-400 dollars for empty shell and 600-1000 dollars for complete artillery shell).

Only time can tell how the future evolves for Goodluck Defence as a company. Management although has guided for 800-1000 Crores topline at 30-35% EBITDA margins at peak however, one can assume 25-30% EBITDA margins in FY29, maybe trying to factor in the significant capacity additions expected across the industry.

In the near term, demand-side tailwinds remain strong, giving Goodluck India a window to capture meaningful market share and establish global customer relationships, especially as most new entrant capacities are still at least a year away from coming online. (Balu Forge, Reliance Infra, Tirupati Forge, Sunita Tools, Nibe Ordinance, Munish Forge etc). Domestic demand is largely tender-driven, which could lead to cut-throat competition as industry capacity expands but on export side- the vendor relationships, consistent quality controls, on time delivery schedules matters and might make cash flows predicatable and business sticky. Goodluck India is targetting export clients as well as planning to cater to the domestic demand.

Disc: Invested in Goodluck Defence, Biased!

10 Likes

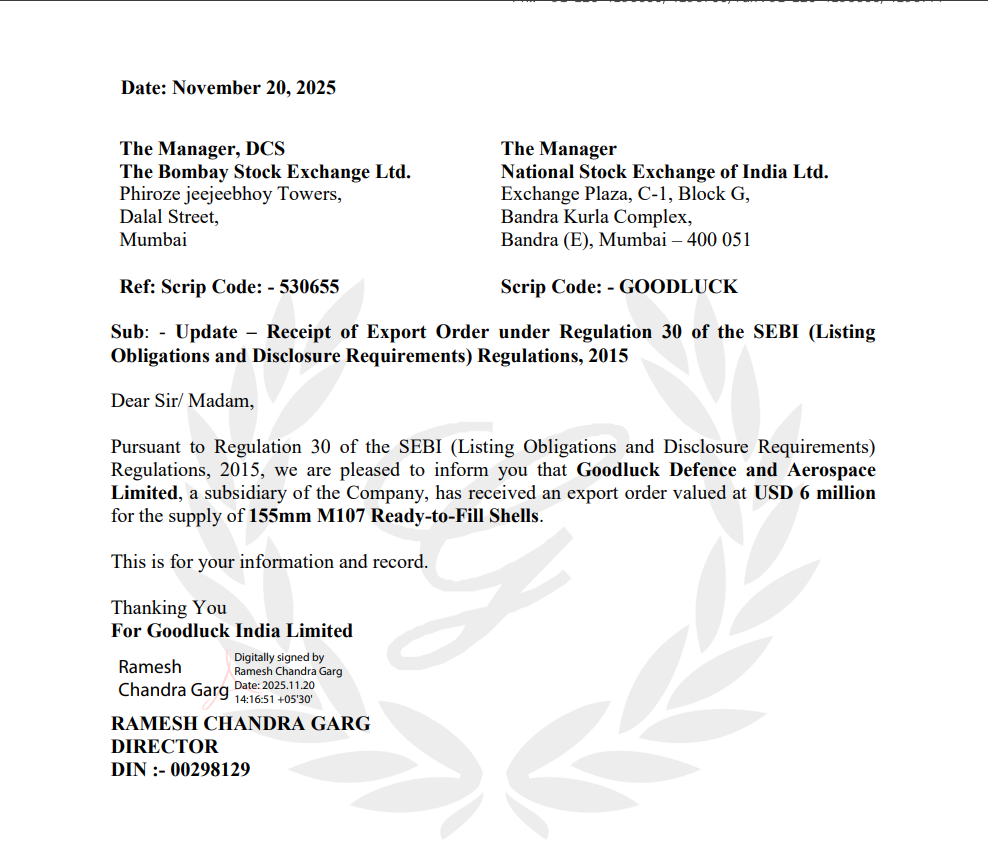

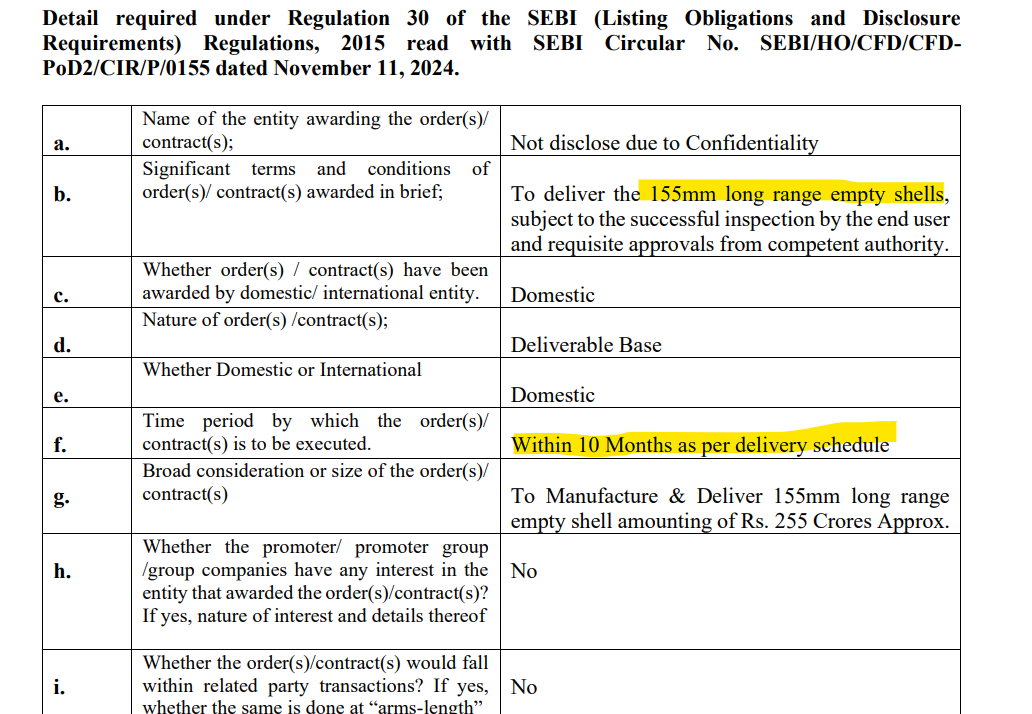

Export license received- first dispatch done. Successful commencement of the first overseas dispatch against order of USD 6mn- 155 mm heavy calibre empty shells by Goodluck Defence and Aerospace Limited, a subsidiary of the Company, from its manufacturing plant located in Uttar Pradesh. Subsequently, the Company successfully procured its first export order, obtained all necessary internal and regulatory clearances for acceptance and execution, and has now commenced dispatch. Mr. Mahesh Chandra Garg, Chairman & Managing Director of Goodluck India Ltd, formally flagged off the first batch under a USD 6 million export order.

1 Like

Probably this should be NATO order for empty shells which is reported by Balu Forge , Sunita Tools etc. The size of the empty shell (155 mm) corraborates with the orders reported by both Balu Forge and Sunita Tools. Since the quantity and value is not mentioned in the filing this could be a validation order.

Disc: Not invested .

1 Like

With these structural tailwinds, GIL through its subsidiary Goodluck Defence & Aerospace, has entered the defence manufacturing space, backed by an industrial license under the Indian Arms Act, 1959, to produce 155mm artillery shells. Within this category, GIL can manufacture advanced variants such as HE M107, ERFB, ERFB BB, and ERFB BIT shells. GIL has commenced production capacity of 1,50,000 shells per annum, with a commencement of its first overseas dispatches of ~US$ 6 million. Moreover, GIL has outlined plans to scale up capacity to 4 lakh shells annually by FY28E, supported by a capex of ~₹400-500 crore. This expansion is aimed at capitalizing on strong domestic and export demand. Thus, we estimate this defence and aerospace segment to generate revenue of ~₹817 crore with EBITDA margins

of ~27% by FY28E, contributing ~14% to revenue and ~31% to EBITDA.

One very interesting thing to note is: Goodluck Astra Pvt Ltd held by Goodluck’s Promoters has applied for 247 Acres land- 1000 Crores investment in the Jhansi Node.

idirect_goodluckindia_convictionidea.pdf (672.5 KB)

5 Likes

A company that has never seen enough cash conversion due to elongated working capital cycles, continuous capex requirements in segments with low asset turns and EBITDA margins ranging 16-18% is now at an inflection point with Defence margins at 30-35% (and more for higher variants of 155 MM shell with higher range and realization). I have been tracking the space for 2 years now and still lot of the questions remain unanswered in terms of Demand for these Artillery Shells post the war scenarios are done with globally. Hopefully below pointers will provide a direction as to what holds for these companies.

I have met and visited the plant of Sunita Tools, Tirupati Forge, and a intereacted with the management of Munish Forge along with a few unlisted companies that have put up a plant or have done due dilligence on putting up an Artillery Shell Plant in India. Few pointers from these meetings and visits below:

- Demand through the roof for atleast 5+ Years is a constant from each management. What gives them confidence is these LOIs from several middlemen/Middle East/NATO countries that are ready to pickup production worth 100s of Crores as the plants go live. Estimates range from around 10-15 Lakh per annum shell requirement for Indian Players to cater to at this moment.

- Margins trajectory guided by each management is around 30-40% on EBITDA levels.

- The machinery setup differs- Goodluck has put up an expensive HBE line vs others like Tirupati and Sunita which are trying to put up a cheaper press by assembling components in house or using Chinese Presses (Which also are one of the best in the world).

- On Setups- Few companies have adopted the CMM, NDT, Hydrostatic Testing etc., CMM I felt is not a must for everyone unless the client specifies it.

- Steel used is special steel with only 2-3 mills in India developing it.

- Client relationships and first mover advantages can be extremely beneficial- Companies that are in the process of putting 50-100 Crores of these capex can find themselves late into the party with ROIs falling as competition and margins stabilize post 3-5 years. Also first movers like Goodluck India are in the know how being in touch with large global clients as to where the technology is moving ahead in future. Management has already indicated that they’re doing R&D in higher variants of Artillery Shell (More on this below).

- 155 MM Shell is the need of the hour. The older smaller diameter shells are not being used much- The systems are being upgraded to fire 155 MM Shells.

Now on Industry data points and inputs- Not a lot of data is readily available since these are extremely sensitive data pointers for a country to declare their stockpiles and inventory levels. On higher variants and advancements of these Artillery Shells read the below articles:

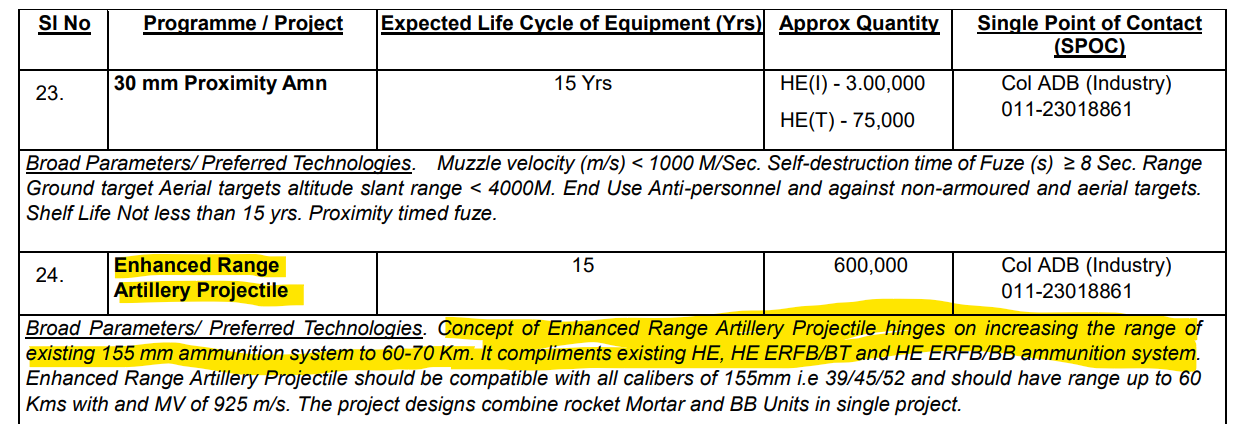

1. TECHNOLOGY PERSPECTIVE CAPABILITY ROADMAP 2025- Concept of Enhanced Range Artillery Projectile hinges on increasing the range of existing 155 mm ammunition system to 60-70 Km. It compliments existing HE, HE ERFB/BT and HE ERFB/BB ammunition system. Enhanced Range Artillery Projectile should be compatible with all calibers of 155mm i.e 39/45/52 and should have range up to 60 Kms with and MV of 925 m/s. The project designs combine rocket Mortar and BB Units in single project.

2. A linkedin article- Global demand will outstrip supply through 2030, with Ukraine’s consumption (2.1 million shells/year) exceeding combined U.S. and EU output (2.3 million shells/year in 2025). The global 155mm ammunition market, valued at $4.2 billion in 2024, is projected to reach $7.5 billion by 2034, driven by ongoing conflicts, stockpile replenishment, and NATO’s focus on interchangeability.

3. Indian Demand in a case of war: Lieutenant General Adosh Kumar, the Director General of Artillery, recently emphasized the military’s focus on developing indigenous ammunition to supply its varied range of 155mm artillery platforms, such as the Dhanush, K9 Vajra-T, and the DRDO’s Advanced Towed Artillery Gun System (ATAGS).

- Currently, the Indian Army is understood to possess an adequate stock of 155mm artillery shells, supported by a strong domestic production capability. The private industry, for example, is anticipated to manufacture over 300,000 shells each year by the 2027 fiscal year.

- However, the strategic outlook could change dramatically in the event of an all-out war with Pakistan. In such a conflict, military planners estimate the Army might need as many as 150,000 shells every month. This monthly requirement represents half of the total projected annual production from the private sector. A conflict lasting a year could therefore consume over 1.5 million shells, a figure four times greater than current yearly output, potentially depleting reserves if exports are not curtailed.

Read more: https://defence.in/threads/india-may-consider-halting-155mm-shell-exports-to-prioritize-army-needs-as-full-scale-war-threat-with-pakistan-looms.14043/

- India is continuously adding the systems to fire Artillery Shells and Strengthen the most traditional way of fighting a land invasive war- The Indian Army is preparing for what could become its largest artillery modernisation programme in decades, with plans to seek approval for the procurement of more than 300 additional K9 Vajra self-propelled howitzers in a deal estimated to be valued at around Rs 23,000 crore.

5. Who’re the Indian Players?:- Goodluck Defence is commercially producing and exporting it becoming the second private player in country to do so post Bharat Forge at scale. Tirupati Forge is putting up a plant but my understanding says they’ll take approx 12 months more to commercially sell these shells with large bottleneck being getting approval and License. Nibe has put up a great plant about which I have limited ground level knowledge but they’re yet to sell. Government companies like MIL and Yantra India lead the end to end shell production with them completing the final value chain and exporting to nations at large volumes. (MIL inks $225-million ammunition contract with Saudi Arabia government - The HinduBusinessLine)

Globally Rheinmetall (A key supplier to Ukraine) is putting up huge facilities with an estimated output of 1-2 Mn Shells per annum but my understanding is the cost differential between Indian Suppliers and these global giants due to several reasons will be atleast 2-3x.

Goodluck India is going from 150,000 Shells per annum to 400,000 Shells per annum with the latest order signifying it’s presence in higher variants of these shells.

All in all- A capex intensive business- approx 80-100 Cr odd capex ex land for 1.2-1.5 Lakh Shells per annum, licenses and approvals being the largest bottleneck followed by a cost and quality control with timely delivery of these shells globally. I feel Goodluck India is very well placed as the global market is up for the taking for these low cost Indian players (In a scenario where demand outsrips supply for 3-5 years).

Before you go- last article i would suggest you to read is the Ramjet Artillery Shell- Press Release Page | Press Information Bureau

Disc: Invested in Goodluck India

Sources:

- Comparative Analysis of 155mm Artillery Ammunition Development and Production in the Arabian Peninsula, Eastern Europe, and the Far East

- Indian Army seeks procurement of 300 K9 Vajra artillery guns at Rs 23,000 crore, Defence Procurement Board to meet this week - India Today

- Press Release Page | Press Information Bureau

20 Likes

2:1 Bonus proposed.

Corporate Guarantee of Rs 275 cr for subsidiary Goodluck Defence

Details regarding ‘corporate restructuring’ not shared. Management given the mandate to work on it.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/1d03be35-40dd-4959-9ac1-ef36e73afcbc.pdf

1 Like