Please do add sources like link to videos or articles when posting some thing like this, this builds credibility and allows us to check the point of view of management

They shared this in Bharat Connect conference, hosted by arihant capital . The recording is not shared to public yet, they may do so next month in their youtube channel.

2 Likes

Q4 FY24 results

Rev up 18%, EBIDTA up 21% YoY

EPS at 11.3 vs 10.3 YoY

Value added products sale volumes increased

by 39% in FY24+Strong demand for critical steel bridge

+VE commentary for Defense+Aerospace arm (New facility progress under schedule)

CFO - (46 Cr) vs 65 Cr

Receivables saw a sharp hike, need to be tracked

FY24 EPS - 46.41 vs 33.31

Saw large volumes today in last 30 minutes. valuations doesn’t look stretched and with demand in future, I feel management is walking the talk.

whats everyone’s opinion on this?

Discloser : having tracking position, not any investment advice.

9 Likes

https://www.youtube.com/watch?v=IT6GbVMwA1Q nice interview

optionalities of hydrogen also being discussed

Disclaimer

- We are not sebi regd

- Educational post only, not an investment advice

- Plz consult your financial advisor before making any investments

8 Likes

- Q1 FY25 dispatches crossed 1 lakh ton for the first time

- Year-on-year growth of 17% in volume and 27% in profit

- Total operating income (standalone) of 904 crores in Q1 FY25 vs 846 crores in Q1 FY24

- EBITDA of 79.65 crores in Q1 FY25 vs 70.87 crores in Q1 FY24

- 17% year-on-year revenue growth

- EBITDA margin of 8.8% in Q1 FY25

- EBITDA per ton of Rs 8,350 in Q1 FY25 vs Rs 7,800 in Q1 FY24

- Value-added products contribute 57-58% of revenue

- Capacity utilization: Infrastructure 70-80%, Automobile tubes 80-85%, Solar 50-55%

- Expanding into defense sector with 155 mm gun shell production

- Commissioning new auto tube plant

- Focus on value-added products and sustainability

- Strong domestic demand in India

- Government focus on infrastructure spending

- Increasing demand in defense sector

- Logistics challenges in exports

- Price pressures

- New auto tube plant with 50,000 ton capacity commissioned

- Defense plant for 155 mm gun shells (1.5 lakh shells per annum) to be commissioned by March 2025

- Logistics challenges, container shortage

- Expected revenue of 4100 crores in FY25 and 4800 crores in FY26

- Auto tube plant expected to contribute 250 crores in FY25 and 500 crores in FY26

- Healthy order book reported

- Aiming for 15-20% growth

- 200 crore investment in auto tube plant

- 200 crore investment in defense plant

- Defense sector growth

- Infrastructure development

- China Plus One strategy benefiting Indian manufacturing

- Q: Impact of elections on business? A: There were some disruptions, but overall demand remained strong. Logistics issues affected exports.

- Q: Current total borrowing and future debt expectations? A: Total borrowing is 608 crores. May need more funds as production increases, but will try to manage within available means.

- Q: Value-added product contribution? A: 57-58% of revenue, with 17% year-over-year growth.

- Q: Auto tube plant details? A: Commissioning by September 1st. Expected revenue of 250 crores in FY25 and 500 crores in FY26.

- Q: Defense business details? A: Initially focusing on 155 mm shells. Capacity of 1.5 lakh shells per annum. Expected revenue of up to 300 crores.

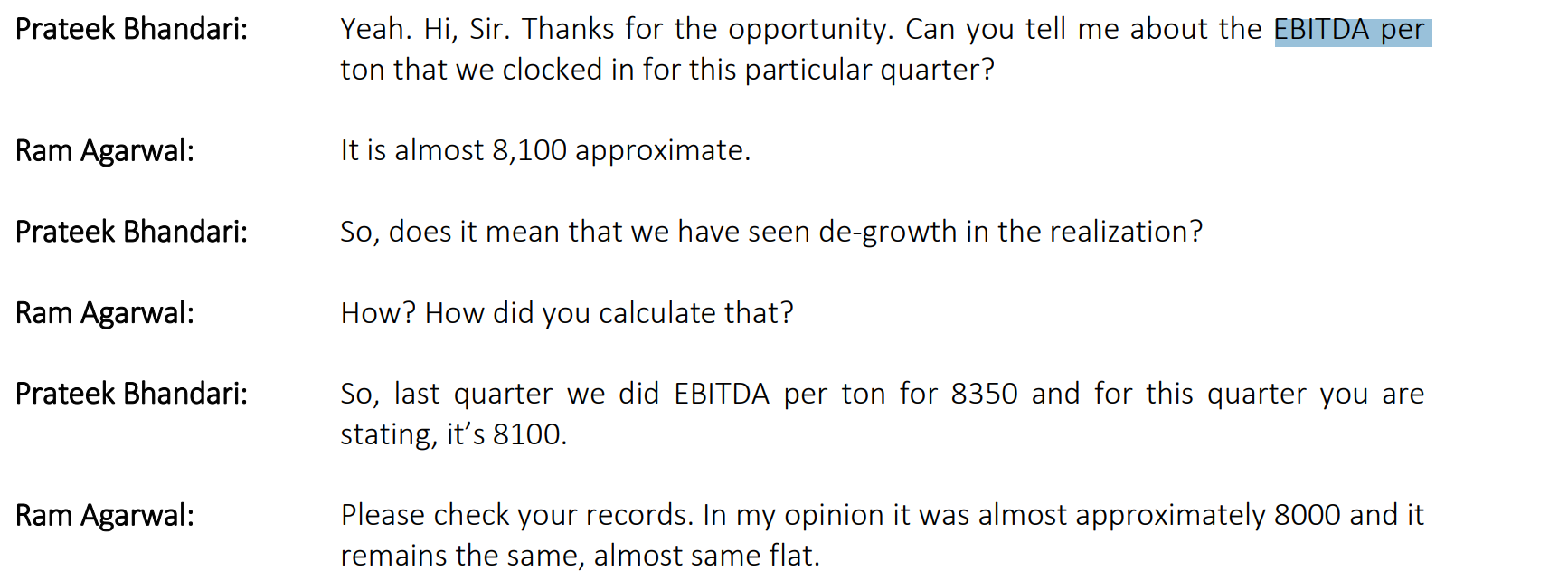

- Q: EBITDA per ton? A: Around Rs. 8,350 per ton in Q1 FY25.

- Q: Timeline for becoming a billion-dollar revenue company? A: Target may be achieved by FY28 instead of FY27.

- Q: Capacity of new auto tube plant? A: 50,000 tons, increasing total capacity to around 4,50,000 tons.

- Q: Traction in solar fixtures and tubes? A: Good growth reported, but specific numbers not provided.

- Q: China Plus One impact? A: Positive impact on Indian manufacturing and infrastructure development.

- Q: Defense product range and competition? A: Initially focusing on shells. Competitors include government facilities and Baba Kalyani group.

- Q: Qualification requirements for defense production? A: Arms Act License required, application in process.

- Q: Export potential for defense products? A: Will supply to authorized exporters who will handle overseas sales as per government policy.

10 Likes

Management Guidance

GoodLuck India

-

15-20 % REV Growth

-

Margin Expansion by increase in VAP

-

Defence next big opportunity

2 Likes

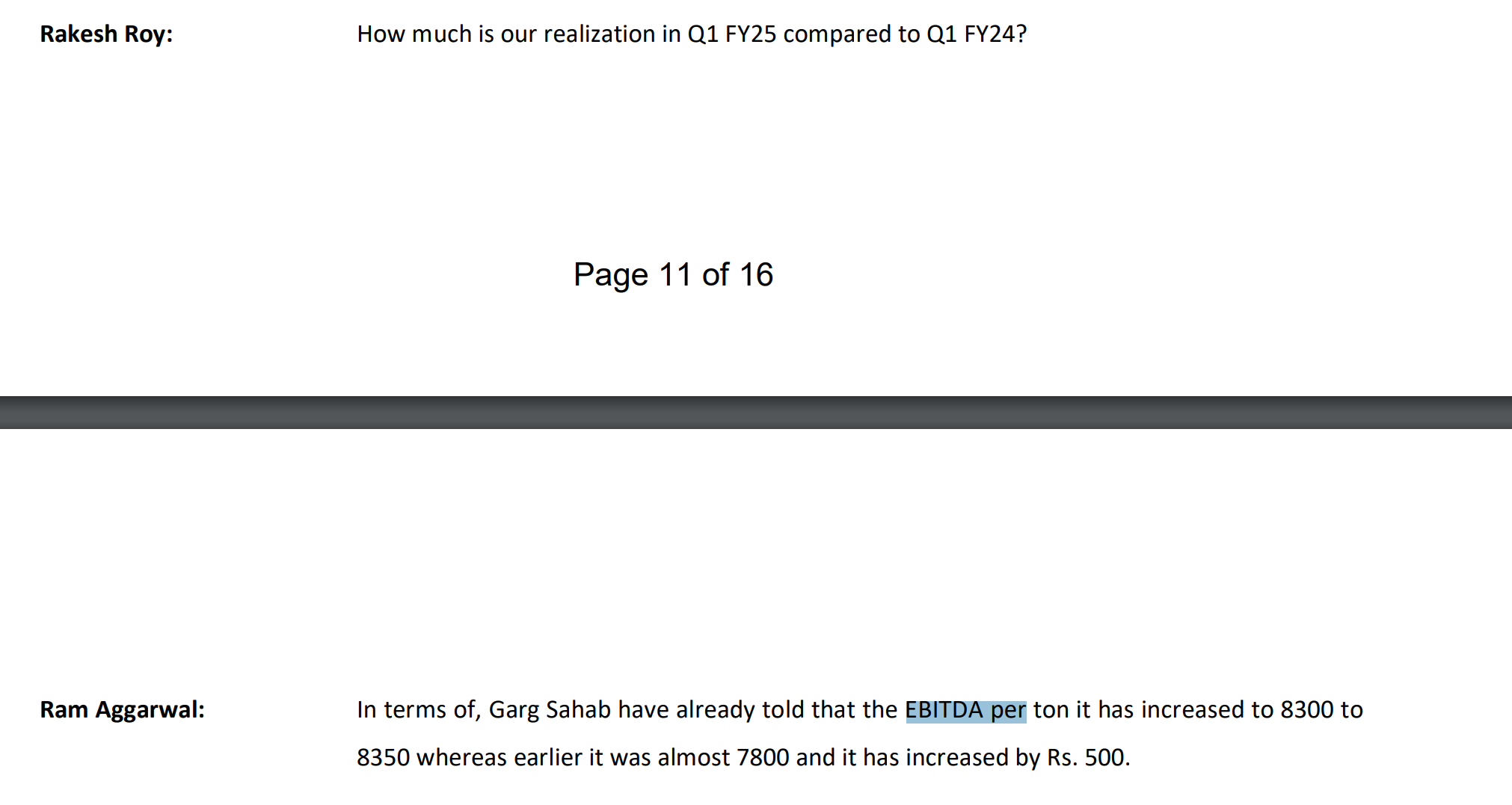

One small doubt on ebitda per ton

Last Quarter management commented that the ebitda per ton is 8350 up from 7800. Kind of 500 per ton increase

When the same was asked in this quarter they are saying current quarter has 8100 per ton and his flat from previous quarter which is 8000 per ton

Any issue with this? As the both statements contradict each other

4 Likes

Look like Ram is not sure of numbers.

1 Like

Value and good bet.

They can do PAT numbers of 180Cr and a PE of 18x i guess.

Looking forward a good and lucky H2. In Goodluck’s defense, its aggressive bet on defense subsidiary is anticipated to do good. After luck favors the good and the brave

2 Likes

GoodLuck India -

H1 FY 25 highlights -

Key Business segments -

Engineering structures and precision fabrications ( capacity @ 85k MTPA )

Forging products ( capacity @ 30k MTPA )

Precision Pipes ( capacity @ 120k MTPA )

CR Coils, Pipes and Tubes ( capacity @ 215k MTPA )

Manufacturing plants -

05 plants near Delhi

01 plant in Kutchh ( Gujarat )

05 major warehouses located @ Faridabad, Rudrapur, Ludhiana, Nahsik and Aurangabad

Domestic : Export break up of sales @ 74 : 26 ( vs 70 : 30 in PY )

Company’s key clients -

Auto tubes - BMW, VW, Skoda, Audi, Mercedes, GM, Renault, Toyota, Mahindra Electric, Tata Motors, Bajaj Auto, TVS, Ashok Leyland, Talbros, Gabriel, Suzuki

Forgings - L&T, RIL, IOL, Toshiba, Mitsubishi, BHEL, GE, Allied Group, Saint Gobain, Bharat Petroleum

Engineering Structures - GMR, ABB, L&T, RIL, Toshiba, TRF ( Tata group ), Power Grid

CR Coils and Tubes - various Public and private sector EPC players involved in infra build up in the country, state Govts, NHAI, Railways

Segment wise revenues -

CR sheets and pipes - 40 pc

Precision Pipes and Tubes - 24 pc

Forgings - 15 pc

Engineering structure - 21 pc

Future growth areas -

Defence and Aerospace - company has inaugurated a new Hydraulic tubes manufacturing Unit with an installed capacity of 50k MT @ Sikandrabad. These are highly specialised import substitution products for the defence ( aerospace ) industry

Q2 financial highlights -

Revenues - 976 vs 885 cr

EBITDA - 87 vs 73 cr ( margins @ 8.96 vs 8.32 pc )

PAT - 45 vs 34 cr

H1 financial highlights -

Revenues - 1889 vs 1470 cr

EBITDA - 165 vs 113 cr ( margins @ 8.74 vs 7.73 pc )

PAT - 79 vs 46 cr

Company did perform very well in Q2 despite sharp volatility in Steel prices in Q2 + sharply reduced Govt spending + Geo Political tensions causing reduced demand in the global markets

The new Hydraulic Tubes plant costed the company @ 200 cr. It has a capacity of 50k MTs. The plant is expected to commence commercial production in Q1 FY 26. This is a dedicated facility for the defence and aerospace Industry

Sales volume in H1 FY 24 stood @ 200k MT vs 183k MT in H1 FY 23

EBITDA / MT in Q2 stood @ Rs 8100. Company believes - if the volatility in Steel prices subsides, EBITDA / Ton should improve by 10 pc

Company business of manufacturing and supplying solar panel structures to various power/ infra / OEM players is witnessing robust demand trends. Same are likely to continue going fwd as well

Company had earlier guided for 20 pc topline growth for FY 25. Despite the headwinds in H1, they still maintain that they should be able to achieve a 15 pc topline growth for full FY 25. That simply means that H2 should be strong

Now that monsoons are over, Indian + US elections are behind - Expect far better H2. As such, H2 is always better for the company vs H1

Company expects to achieve optimum capacity utilisation of their Hydraulics manufacturing plant inside 2 yrs. Then they plan to double this capacity. This particular line of products have huge tailwinds. These hydraulic products also find applications in the construction Industry

Comapny has got orders for supply of materials worth 22k MT for the Bullet Trains project. Company has completed production of aprox 65 pc of the material which should now get supplied to L&T over next 8-9 months

The CR coils and sheets business is a steady volume ( no growth ), low margins business for the company. They have committed clients for their products. They have been doing this for 25 yrs. Aim to continue to do the same. But this is not a growth area

Company is slated to supply 155mm Arty Gun shells to IA. They were earlier imported. Company intends to supply 1.5 lakh shells - to begin with. That should have a revenue potential of aprox 300-350 cr

Company expects their defence business to generate 20 pc kind of EBITDA margins. Currently, it contributes to only 2 pc of their topline. This is expected to start to ramp up wef next FY

Disc: hold a small tracking position, will ramp up position size / dump the stock depending on their H2 performance, not SEBI registered, not a buy/sell recommendation, posted only for educational purposes

11 Likes

Goodluck India -

Q3 FY 25 results and concall highlights -

Revenues - 942 vs 878 cr, up 7 pc

EBITDA - 82 vs 75 cr ( margins @ 8.76 vs 8.62 pc )

PAT - 41 vs 32 cr, up 26 pc ( PAT margins @ 4.24 vs 3.61 pc )

Key Business segments -

Engineering structures and precision fabrications ( capacity @ 85k MTPA )

Forging products ( capacity @ 30k MTPA )

Precision Pipes ( capacity @ 120k MTPA )

CR Coils, Pipes and Tubes ( capacity @ 215k MTPA )

Manufacturing plants -

05 plants near Delhi

01 plant in Kutchh ( Gujarat )

05 major warehouses located @ Faridabad, Rudrapur, Ludhiana, Nahsik and Aurangabad

Domestic : Export break up of sales @ 74 : 26 ( vs 70 : 30 in PY )

Company’s key clients -

Auto tubes - BMW, VW, Skoda, Audi, Mercedes, GM, Renault, Toyota, Mahindra Electric, Tata Motors, Bajaj Auto, TVS, Ashok Leyland, Talbros, Gabriel, Suzuki

Forgings - L&T, RIL, IOL, Toshiba, Mitsubishi, BHEL, GE, Allied Group, Saint Gobain, Bharat Petroleum

Engineering Structures - GMR, ABB, L&T, RIL, Toshiba, TRF ( Tata group ), Power Grid

CR Coils and ERW Tubes - various Public and private sector EPC players involved in infra build up in the country, state Govts, NHAI, Railways

Segment wise revenues for 9M FY 25 -

CR sheets and pipes - 36 pc

Precision Pipes and Tubes - 26 pc

Forgings - 15 pc

Engineering structure - 26 pc

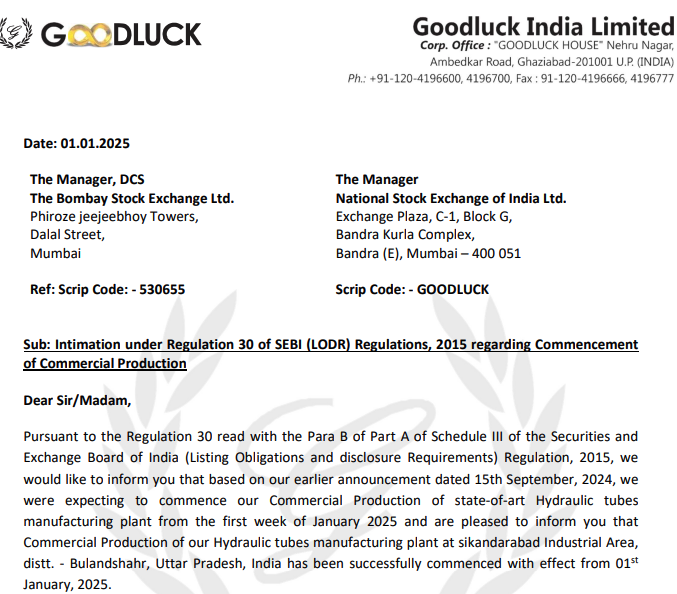

Future growth areas - Defence and Aerospace - company has inaugurated a new Hydraulic tubes manufacturing Unit with an installed capacity of 50k MT. These are highly specialised import substitution products for the defence ( aerospace ) industry. This plant has completed trial runs and has commenced production wef Jan. This plant has the capacity to generate revenues of upto 300 cr / yr by FY 27

Company’s business mainly caters to sectors like - Automobiles, Construction, Railway bridges, oil and gas, Solar and other renewable energy forms with Defence as the latest addition

Total capacity stands @ 4.5 lakh MT, slated to go upto 5 lakh MT in Q4

In the Auto sector, company mainly caters to Car body tubes, 2W and PV - shocker tubes ( Tesla is also a customer )

Aim to do yearly revenues of 4500 cr by FY 26

Company is slated to supply 155mm Arty Gun shells to IA. They were earlier imported. Company intends to supply 1.5 lakh shells - to begin with. That should have a revenue potential of aprox 300-350 cr. The supplies are expected to begin wef Q2 FY 26

Company expects a major ramp up of their LDP ( large diameter plant for Auto Tubes ) wef Q1 next FY - this plant also have a revenue potential of aprox 500 cr per year ( can be achieved wef FY 27 ). This plant was commissioned in Jan and has added 50k MT to company’s total capacity ( taking it upto 5 lakh MT )

In the 9M FY 25, company has achieved a volume growth of 13 pc. Topline growth is lower because of fall in steel prices

Most of the growth that company is seeing and hopes for in the future is coming from / or is going to come from Infra, Auto, Defence, Oil & Gas sectors. Not expecting any substantial growth from ERW tubes / CR coils

The CR coils and sheets business is a steady volume ( no growth ), low margins business for the company. They have committed clients for their products. They have been doing this for 25 yrs. Aim to continue to do the same. But this is not a growth area

Disc: holding, biased, added recently, not SEBI registered, not a buy / sell recommendation

12 Likes

Q3 FY25 Concall short notes:

- Rev: 7.25%, PAT: 26%, EPS: 4.1% (YoY).

- FY26: 4500cr rev + defense rev (~150cr).

- Mgmt sticks to 15-20% vol guidance for FY25. (Rev% may be lower due to lesser steel prices)

- Defense unit starts production in Q2’26. (150cr in FY26, 250-300cr rev in FY27 at 25% EBIDTA)

- Hydraulic tube plant started (500cr rev in '26).

3 Likes

A clarificaiton please - Is the hydraulic tube plant expcted to acieve optimal utilisation in FY27 (as highlighted by previous participants’ notes) or FY26?

Thanks

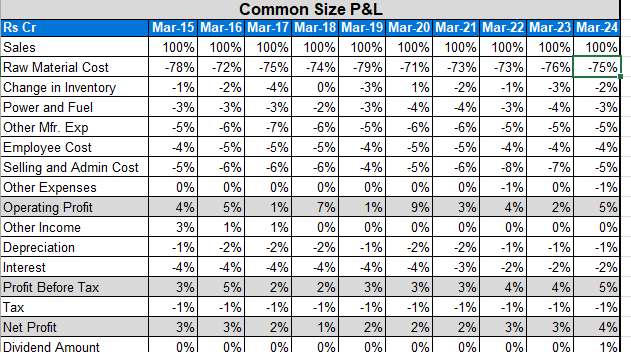

. The sales are 2.5X from Mar-20 to Mar-24 (1600 cr to 3525 cr), profits are also 2.5X as the company has constant OPM of 8% (128 cr to 282 cr) but the stock price/market cap is up from 150 crore to 2250 crore which is almost 15 times - driven by the P/E expansion from 5 to 15 which is 3X

Looking at common size analysis looks like further growth in sales due to increased capex and fall in raw material prices could be key to future prices. There has been huge capex of 195 crore in Mar 24 and this indicates future sales growth could drive more upside to stock if they can hold margins

2 Likes

Goodluck India -

Q4 and FY 25 results and concall highlights -

Q4 outcomes -

Revenues - 1092 vs 892 cr, up 22 pc

EBITDA - 93 vs 72 cr, up 28 pc ( margins @ 8.4 vs 8.1 pc ). Employee expenses were up 45 pc YoY

Depreciation @ 14.3 vs 9.4 cr, up 51 pc YoY

Interest costs @ 21 vs 16 cr, up 38 pc YoY

PAT - 42 vs 35 cr, up 18 pc YoY

FY 25 outcomes -

Revenues - 3897 vs 3488 cr, up 12 pc

EBITDA - 340 vs 292 cr, up 16 pc ( margins @ 8.7 vs 8.3 pc )

PAT - 161 vs 130 cr, up 24 pc

Achieved a volume of 442,619 MT in FY25, reflecting a 15.3% YoY growth compared to the previous financial year. This growth highlights strong demand across business segments, driven by increased sales of high margin value-added products and expanded international market reach

Segmental breakup of revenues -

Engineering structures and fabrications - 23 pc

Forgings - 16 pc

Precision pipes and Auto tubes - 25 pc

CR sheets and pipes - 36 pc

Geographical breakup of revenues -

Domestic sales @ 75 vs 73 pc YoY

International sales @ 25 vs 27 pc YoY

Company exports to North America, EU, Russia, LAtAm, Africa and Australia/NZL

Company’s key clients and End user industries -

Precision Tubes and Auto tubes - BMW, VW, Skoda, Audi, Mercedes, GM, Renault, Toyota, Mahindra Electric, Tata Motors, Bajaj Auto, TVS, Ashok Leyland, Talbros, Gabriel, Suzuki

End user industries - automobiles, aerospace, defence, railways, oil and gas

Forgings - L&T, RIL, IOL, Toshiba, Mitsubishi, BHEL, GE, Allied Group, Saint Gobain, Bharat Petroleum, HAL, DRDO, ISRO

End user Industries - aerospace, defence, construction and earth moving equipment, nuclear power, oil and gas, general engineering

Engineering Structures - GMR, ABB, L&T, RIL, Toshiba, TRF ( Tata group ), Power Grid, Reliance group, Indian Railways

End user industries - roads, railways, telecom, boilers, turbine generators, steel and concrete grinders, solar energy, building structures

CR Coils and ERW Tubes - various Public and private sector EPC players involved in infra build up in the country, state Govts, NHAI, Railways

End user industries - railways, road bridges, support structures

Manufacturing plants -

05 plants near Delhi

01 plant in Kutchh ( Gujarat )

05 major warehouses located @ Faridabad, Rudrapur, Ludhiana, Nahsik and Aurangabad

Key Business segment capacities -

Engineering structures and precision fabrications capacity @ 85k MTPA

Forging products capacity @ 30k MTPA

Precision Pipes capacity @ 170k MTPA

CR Coils, Pipes and Tubes capacity @ 215k MTPA

FY 25 capacity utilisation @ 89 pc vs 93 pc in FY 24

Recent key developments -

New Plant - In January 2025, the company commissioned a state-of-the-art hydraulic tubes unit in Bulandshahr, Uttar Pradesh, with a 50,000 MT capacity. These high-precision tubes serve as an import substitute for seamless tubes, supporting foreign exchange savings and driving topline and bottom-line growth for the company. Goodluck India Ltd will begin trial production in Q1 FY26 at the new facility of its subsidiary, Goodluck

Defence and Aerospace Ltd, in Sikandrabad, Bulandshahr (U.P.). Designed to produce ~150,000 precision components annually; commercial production expected by end-Q2 FY26

Precision Pipe (CDW) Ramp-Up - CDW facility is currently in the production ramp-up phase, with full-scale production expected by Sep/Oct

2025 to meet targeted demand

Highlights from management commentary -

In Q4, capacity utilisation was @ 95 pc, Volume growth was @ 17 pc

Company has a good visibility of 15-20 topline growth ( based on orders at hand ) for FY 26 with margins @ similar levels ( with an upward bias ) as FY 25

The new Defence manufacturing plant has a peak revenue potential of aprox 270 - 300 cr ( should be able to achieve the same by FY 27 ). Should be able to clock 100-120 cr revenues for FY 26. Company may go for further expansion on defence manufacturing capacity once they achieve > 70 pc plant capacity utilisation on this plant

Have not recorded any inventory gains in Q4

Maintenance Capex + De-bottlenecking processes are continuously on at various company plants

The revenues from the Defence plant shall be over and above the 15-20 pc topline growth guidance given by the company

The Defence manufacturing plant should clock EBITDA margins in the range of 20 pc or so

In medium term, company hopes to start clocking double digit EBITDA margins. Most of the fresh capex ( in near future ) shall be dedicated to Auto tubes and Defence manufacturing units. These segments have 12-13 pc and 20-21 pc kind of EBITDA margins respectively. These should pull up company’s consolidated EBITDA margins

Company’s blended cost of Debt @ 9.5 pc

Margin profile for their engineering structures business is 9-10 pc

The margin guidance given by the company is on the conservative side. Most of the projected growth in FY 26 is going to come from Non CR sheets and coils business which should naturally exert upward pressures on margins

Oil and gas + Chemicals sectors are major consumers for company’s forgings business. With a republican govt in US, demand for their forging business is expected to remain strong

Company is already supplying 155 mm Artillery shells to MoD and metal parts for Brahmos Missiles

Seeing a lot of interest from multiple customers wrt the upcoming defence manufacturing facility. Utilising those capacities should not be a problem for the companies. In all probability, they ll have to go for additional capex in not so distant future

The CR sheets and coils business clocks a 4 pc kind of margins. It’s a legacy but stable business. Even in this business, company is looking @ 100 bps kind of margin expansion over next 2-3 yrs

Should be able to reduce gross debt by 50-60 cr by end FY 26

Disc: holding, biased, not a buy/sell recommendation, not SEBI registered, added recently

12 Likes

Goodluck India

Goodluck looks extremely cheap even with conservative estimates of 15% topline growth and double digit margins in 2 years

Sales can be around 5000-5200Cr in FY27

PAT can double in 2 years to reach around 300Cr

Trading at 10-11x FY27 PAT, <1x TTM sales and 0.6x FY27 sales

PEG 0.5x

Large Diameter Pipes and Precision Tubes plants are sitting on operating leverage

Defence biz will also pickup now - 40% utilisation in FY26 and 100% in FY27 (Peak revenue potential of 300Cr, 20% OPM)

Defence - “Not less than 3 customers visit our plant every day and want full capacity for years.” No demand concerns anticipated

Double digit margins in 1-2 years (driven by higher-margin segments (auto tubes: 12–13%, defence: 20%+))

Business will look very different in 2 years time

Medium term targets for the business is to reach 8000Cr revenue in 3-4 years with double digit margins and 20%+ ROCE

Extremely asymmetric in my opinion

Other income is around 35Cr - Largely operational (interest on deposits, export-related charges); not to be excluded from EBITDA, per management.

Management asserts other income is operational and should be included.

Even if you don’t include this, PAT should be around 275Cr in FY27.

Depreciation taken as 60Cr

Interest at 80Cr

Extrapolate your numbers till FY27

Exit multiples in the range of 20-30x

Think long term. If they achieve an 8000cr topline in 4 years.

PAT of around 400-500Cr.

Trading at less than 10x forward.

Even a 20x multiple means it can be an 8000Cr company trading at 1x sales. Rerating optionality can lead to unprecedented results.

Mental models: Margin of safety with fast growth, margin expansion, product mix change, sectoral tailwinds and the stock tensions relatively less discovered.

Risks:

- Economic slowdown

- Poor execution

- Defence business not living up to the promise

Disc: Not a recommendation

13 Likes

agreed 100%

GOODLUCK THESIS

- execution is there but not yet came up in numbers , main concern of the street is margin expansion

- this they are guiding that even their base CR business has margin expansion levers due to entry into solar tubes - 200 bps

- their defence is of 20% business (3 people are visiting their plant every day , just the commisioning is delayed )

- infra project is 9-10% business

- their auto pipes plant will be going to 60-70% utilisation

little reason to believe that margins wont inch up

watching the internals of the business - which suggest this business is on verge of inflection

- thus the valuation comfort

- we can get dual engines here

- call is full of reasons behind the structural tailwinds it has

peg comes to less than 1x with even .5% margin expansion and 15% growth in revenue as guided by management

fits the framework

-quantum of growth

-nearness of growth

-certainity of growth

-we should not be paying up for growth

11 Likes

Very few people know that they are entering into Hydrogen. Work is already in progress. I saw prompter’s interview where he mentioned this. Just like Goodluck Defence, Hydrogen subsidiary will also be put. Will share the interview link here if I find.

Found the link - Towards the end of this video you can listen the management mentioning about hydrogen

10 Likes