Esteemed Members,

I have been a member of Valupickr for some time now, but this is my first post proposing discussion on a stock. From being a “zero” in analysis of stocks, I have gained a little knowledge by being a part of this learning community. The fact that I am still a novice is entirely due to my own failings, and it has not been due to lack of trying on the part of the community, so no blame should be ascribed to the latter!

I must thank the Valupickr Community for being so selfless in promoting learning. I must also heartily Thank Messers Mittals for their invaluable tool, Screener, which I have made use of freely in my presentation, and at all times.

The objective of this short introduction was to not only convey my gratitude, but to also to request you to kindly guide me further in my attempts. I accept that I am quite fearful of the economic part (financial analysis, in other words), so I have not ventured too deeply into that field. There are many gaps in my presentation, so please feel free to correct me.

And finally, dear members, be gentle!!

Edible Oil: Industry Structure & Development:

The Indian vegetable oil economy is the world’s fourth largest after the US, China and Brazil, harvesting about 25 million tons of oilseeds against the world. Since 1995, Indian share in world production of oilseeds has been around 10 percent. Vegetable oil consumption has increased following a rise in household incomes and consumer demand. India imports half of its edible oil requirement, making it the world’s third-largest importer of edible oil. The country buys soya oil from Argentina & Brazil and palm oil from Malaysia & Indonesia. Currently, India accounts for 11.20 per cent of vegetable oil import and 9.30 per cent of edible oil consumption.

India does not even produce half of its edible oil requirements, mainly due to rainfed conditions, high seed cost, smallholding with limited resources, low seed replacement rate, and low productivity. The country needs 25 million tonnes of edible oils to meet its requirement at the current consumption level of 19 kg per person per year.

Out of the total requirement, 10.50 million tonnes are produced domestically from primary and secondary sources and remaining 60% is met through import. The oilseed production of the country has been growing impressively. Despite this, there exists a gap between the demand and supply of oilseeds, which has necessitated sizable quantities of imports.

To increase the domestic availability of edible oil and reduce import dependency, the government has proposed a National Mission on Edible Oils (NMEO) for the next five years. The proposal is based on achieving results in three key areas to increase production of oilseeds and edible oils from primary sources such as annual crops, plantation crops, and edible TBOs (tree borne oilseeds); secondary sources such as rice bran oil and Cottonseed oil; and consumer awareness for maintaining edible oil consumption constant at 19.00 kg per person per annum.

The government intends to increase production from 30.88 to 47.80 million tonnes of oilseeds that will produce 7.00 to 11.00 million tonnes of edible oils from primary sources by FY 2025. Also, it is expected that edible oils from secondary sources will be doubled from 3.50 to 7.00 million tonnes. Meanwhile, at present, crude palm oil is freely importable while refined palm oil and palm olein have been put under the ‘Restricted’ category for imports since 8 January 2020. The restriction is applicable to imports from all countries.

With an initiative such as “AATMANIRBHAR BHARAT” Government of India is planning to reduce dependence on the import as much as possible. With the combined efforts of government, industry companions we can achieve sovereignty and independence in the edible and non-edible oil industry. There is still a long way to go but with dedication towards corporate governance and business ethics day is not far away when we will achieve new heights by following the principle “Everyone will accompany, everyone will nurture.”

(Source: AR 2020)

Recent trends in edible oil show that the prices are increasing. According to the government data, retail prices of edible oils have shot up by 55.55 per cent in over a year and are adding to the woes of consumers already reeling under the economic distress induced by the COVID-19 pandemic (Source: Business Standard, here: Govt expects edible oil prices to cool off with release of imported stock | Business Standard News

Some news links are given below:

“The monthly average retail prices of packed edible oils – groundnut, mustard, vanaspati, soya, sunflower and palm oils – have soared this month to their highest levels in over a decade, according to official data” - Indian Express

Link: ‘Concerned’ as edible oil prices soar to 11-year high, government takes stock | India News,The Indian Express

In this scenario, I am proposing initiating a discussion on Gokul Agro Resources Limited (GARL) for your consideration. Details are given below. The main sources are the Annual Reports of the company, ICRA, Screener.in, and company website, unless otherwise stated.

Key financials:

• Market Cap₹ 365 Cr.

• Current Price₹ 27.7

• High / Low₹ 31.8 / 9.70

• Stock P/E 7.98

• Book Value ₹ 26.2

• Dividend Yield 0.00 %

• ROCE 23.5 %

• ROE 13.8 %

• Face Value ₹ 2.00

• Price to book value 1.06

• Pledged percentage 16.3 %

About the company

GARL was established following the demerger of the erstwhile GRSL in July 2015. It is operated by Mr. Kanubhai Thakkar and family. The company is in the business of refining and marketing edible oils. It has a seed processing capacity of 2,800 tonne per day (TPD), cake extraction capacity of 850 TPD, oil refining capacity of 1,900 TPD and vegetable oil manufacturing capacity of 100 TPD at its Gandhidham plant.

The erstwhile GRSL was jointly promoted by Mr. Balvantsinh Rajput and Mr. Kanubhai Thakkar in 1982 as a small unit for seed processing and trading in edible oils. In 1992, it was incorporated as Gokul Refoils and Solvent Private Limited. Over the years, it expanded its refining capacity and also set up crushing and extraction facilities at different locations. GRSL demerged its Gandhidham unit into GARL.

Business Profile

Gokul Agro Resources Limited is listed on Bombay Stock Exchange (BSE) & National Stock Exchange (NSE). The company is engaged in business of Manufacturing & Trading of Edible & Non-Edible Oil, Meals and other Agro Products.

GARL offers soya bean oil, cottonseed oil, palm oil, sunflower oil, groundnut oil, vanaspati, etc.; and other industrial products, such as castor oil of various grades and its derivatives. It also provides castor seed and soya bean meals; hulled, natural, and black sesame seeds; fenugreek, cumin, and ajwain seeds; and wheat, rice, barley, maize, and chick peas. The company offers its products under the Vitalife, Zaika, Mahek, Pride, Richfield, Puff Pride, and Biscopride brand names.

GARL is a certified ISO 22000:2005 company and its product range consists of all the major edible oil consumed globally and among the Non-edible segment they are one of the largest Castor Oil producing companies. They cater to the Feed Meal industry by supplying high quality meal of Soybeans and at Castor producing unit they produce high quality Castor Meal which is an Organic Fertiliser by itself. GARL is present in more than 20 different states of India.

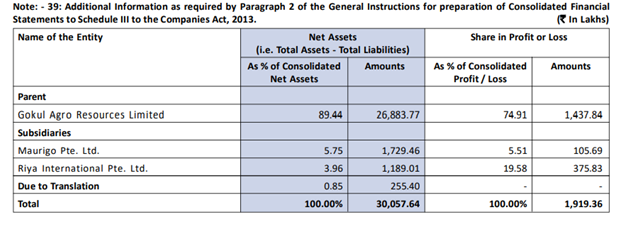

As on March 31, 2020, GARL has one Subsidiary Company namely Maurigo Pte. Ltd., Singapore and one Step Down Subsidiary Company namely Riya International Pte. Ltd., Singapore in order to cater its international trading operations in the key parts of the world.

The company supplies its products to United States, South Korea, European Union, China, Singapore, Indonesia, Malaysia, Russia and Vietnam.

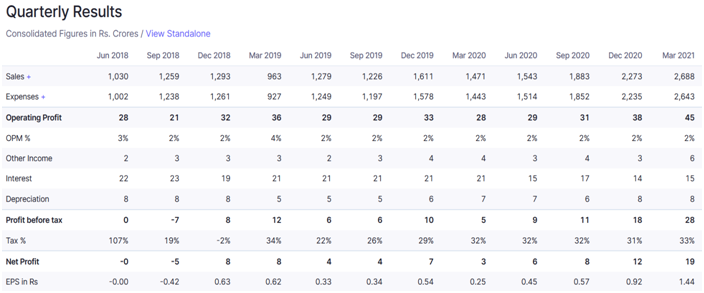

Financials - Results

Highlights of results:

• Net Sales-YoY Growth in year ended Mar 2021 is 50.10% vs 22.91% in Mar 2020

• Consolidated Net Profit-YoY Growth in year ended Mar 2021 is 132.88% vs 76.38% in Mar 2020

• Interest: YoY Growth in year ended Mar 2021 is -26.50% vs 0.16% in Mar 2020

• Operating Profit Margin (Excl OI): YoY Growth in year ended Mar 2021 has fallen from Mar 2020

• Operating Profit (PBDIT) excl Other Income-YoY Growth in year ended Mar 2021 is 18.81% vs 1.77% in Mar 2020

• Low Debt to Equity at 0.24, which has shown an improvement over the past years: 0.32 in 2018, 0.42 in 2019 and 0.40 in 2020.

A look at the ratios shows an encouraging trend:

However, some concerns:

• Low ROE signifies low profitability

• No dividend over several years. Management claims that they would like to conserve the funds for future expansion and growth. Although for some this could be a positive sign, but is it really?

• Promoters have reduced their holdings by 1.98% in the last quarter and now hold 69.82%. Non-Institutional Investors hold 29.43%.

• Pledged promoter holdings amount for 16.29%, and there are no FII holdings.

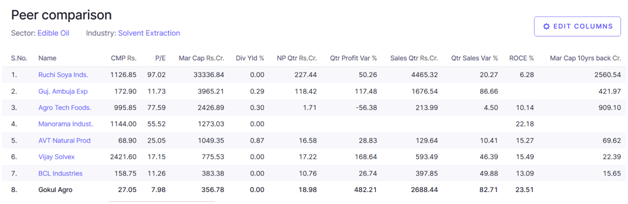

GARL is valued lower than its peers:

Credit Ratings

In August 2020, ICRA reaffirmed ratings of GARL as BBB-(Stable) for Fund-based loan. Ratings for the past three years are as follows:

Sr. No. Year Credit Rating

Long Term Short Term

1 2019-20 ICRA BBB- with stable outlook ICRA A3

2 2018-19 ICRA BBB- ICRA A3

3 2017-18 ICRA BBB ICRA A3+

Some excerpts from the ICRA Report may be of interest:

Established position of Gokul Agro Resources Limited (GARL) among the leading edible oil manufacturers in terms of scale with an extensive track record of its promoters in the edible oil industry and a diversified product portfolio.

It enjoys a good market position in the bulk segment of the edible oil market.

Location-specific advantage arising from it being close to ports and oilseed growing belt. The company’s manufacturing facility is an integrated facility at Gandhidham, Gujarat. The plant is strategically located in terms of its proximity to ports. It is very close to the Kandla Port (about 20 km away) and most of the imports and exports take place through the same.

Satisfactory operating and financial performance of the company with gradual improvement in the capitalisation and coverage metrics.

Categorisation of edible oil as an essential commodity during the nationwide phased lockdown GARL’s operations were not severely impacted, barring the initial few weeks of April 2020 when logistics remained a constraint.

GARL converted Rs. 45-crore unsecured loans from promoters outstanding as on September 30, 2019 into non-convertible noncumulative redeemable preference shares in Q4 FY2020 as planned, resulting in an improvement in the net worth position of the company as on March 31, 2020.

Diversified product portfolio across various types of oils imparts flexibility in changing product mix - GARL produces a wide variety of edible oils to cater to the needs of all consumer and geographical segments, which mitigates the seasonality risk associated with any particular product.

On the other hand, its product portfolio mainly includes refined oils (over 85% of revenues in FY2020), de-oiled cake, castor oil derivatives and vegetable cooking oil (vanaspati). The product mix under the refined oil segment is dominated by palm oil driving ~56% of GARL’s refined oil revenue in FY2020 (against 45% in FY2019). Other oils include soya bean oil, castor oil, mustard oil, etc. The production of soya bean and mustard oil reduced significantly in FY2020 due to lower margin available, given the revised minimum support price (MSP) for oilseeds. Consequently, their sale was replaced by that of palm oil.

Inherently thin operating margins; margin declined in FY2020 due to increased trading activities. At a consolidated level, GARL’s operating margin moderated to 2.5% in FY2020 from 3.1% in the previous year mainly due to significant increase in the trading activities at its step-down subsidiary, Riya International Pte. Ltd., as well as at the standalone entity level. Such low margin trading activities resulted in a significant increase in operating income with modest addition to the operating profit.

Vulnerability of the company’s profitability to the duty differential between crude and refined oil and the climatic risks associated with the procurement of indigenous oilseeds and the regulatory changes with respect to domestic and the Indonesian duty structure. However, government of India’s directive to place the import of refined palm oil in India under the ‘restricted’ category since January 2020 has supported the domestic refiners to some extent.

Profitability is exposed to adverse fluctuations in commodity prices and exchange rates which may cause a loss despite its firm hedging policy.

The low margin nature of the industry, dependence on climatic factors for a good harvest and high import dependence for meeting edible oil requirements, affect the profitability of players like GARL in a volatile pricing scenario.

The contribution from the retail segment has remained low; although sustained efforts are being made to increase the presence of its retail brands, Zaika, Mahek, Pride, Richfield and Vitalife. The company has been continuously expanding its distribution network, which at present caters to several states through clearing and forwarding (C&F) agents and depots, several hundred dealers and retail points.

Key Management

Mr. Kanubhai Jivatram Thakkar is currently serving as a Chairman and Managing Director. Presently he is an office bearer of various committees like; SEA International Oil and Oilmeal Trade Council, SEA Imports Vegetable Oil Processors Council, SEA Castorseed and Oil Promotion Council. He is the recipient of the “Oil Man of the Year” award in the year 2005 from ‘Globoil India’. Mr. Kanubhai Jivatram Thakkar started as a commodity trader and has about 3 decades of experience in edible oils. He is actively involved in the business development activities and major expansion initiatives undertaken by the group. He plays a vital role in the hedging activities undertaken by the Company. He was instrumental in setting up & developing a subsidiary in Singapore to establish a presence in global market.

Mr. Jayesh Kanubhai Thakkar, Joint MD, is the son of CMD, Mr. Kanubhai Jivatram Thakkar. He has done Mechanical Engineering from BITS, Pilani, UAE and Masters in Management and Strategy from The London School of Economics and Political Science, London. He was awarded Merit Scholarship for B.E. (Hons.) in Mechanical Engineering from the Birla Institute of Science & Technology, UAE. During his studies at London, he had been a Member of Management & Strategy, Finance Society and Alternative Investment Society at LSE. He has been actively looking after the business of the Company and Future Planning and Strategies Formulation for the Company. He also holds the position of Director in Riya International Pte.

Mr. Dipak Kanubhai Thakkar is Director-EXIM in the Company with effect from September 18, 2017. He is also the son of the CMD. Aged 29 years, he is Mechanical Engineer, B.E. (Hons.) from BITS, Pilani at UAE and Master’s in Business Administration from Management Development Institute of Singapore. He has also been well versed with ExportImport Procedures and Documentations and Comprehensive Framework for Stock Market, Nifty, Currency, Gold, and Silver along with its Technical Analysis. He has overall experience of more than 3 years with leading Corpo rate at UAE and with Gokul Group as well.

Mr. Nilesh Kanubhai Thakkar, another son of the CMD, holds the position of Director-Marketing in the Company with effect from October 1, 2019. Aged 25 years, he is Master in Business Administration, (Family Business) from Nirma University, Ahmedabad. He has also been well versed with dealing with marketing of products such as edible and non-edible oil products as well as advertising and promotion of the same.

The above indicates that a succession plan is well placed, with the younger generation getting hands-on experience.

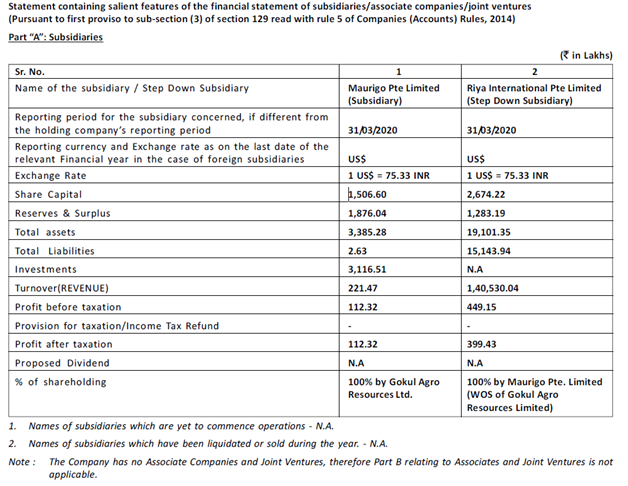

Subsidiary companies

According to AR 2020: As on March 31, 2020, the Company has one Subsidiary Company namely Maurigo Pte. Ltd., Singapore and one Step Down Subsidiary Company namely Riya International Pte. Ltd., Singapore.

Here is an extract from AR 2020:

Another extract is here:

I would appreciate if esteemed members could guide as to whether this information about the subsidiaries is sufficient or is the company obliged to give more information, such as what these companies do, etc.

Independent Auditors have stated that they did not audit the financial statements of Subsidiary Companies, and these have been audited by other auditors whose reports have been furnished to them by the Management. Their opinion on the consolidated financial statements and report, are based solely on the reports of the other auditors.

Is this something one needs to be concerned about?

Another area where I feel the company could have been more forthcoming is their vision and strategy. As per the ARs:

The above sentences appear without any change in several ARs. I feel the company could have defined their targets, elaborated their way forward, and spelled out strategies for achieving their targets. I would be grateful for advice on this.

The Auditor’s Report 2019-20 mentions that: The Company has granted loans, secured or unsecured to the companies, firms or other parties covered in the register maintained under section 189 of the Companies Act, the outstanding balance as at 31st March, 2020 is as under.

Sr.No. Name of the Parties Amount (Rs. In Lakhs) Remarks

- Gokul Refoils & Solvent Limited 86.35 Loan balance transferred to the company on account of demerger scheme approved by the Hon’ble High Court of Gujarat.

- Gujarat Gokul Power Limited 2,038.55 -do-

- Gokul Overseas 322.48 -do-

They have also certified that

(a) The terms and conditions of the grant of such loans are not prejudicial to the Company’s interest.

(b) The schedule of re-payment of principle and payment of interest has not been expressly stipulated as the same is considered to be on mutual demand and in the absence of such schedule; we are unable to comment on the repayment of receipt of principle amounts.

(c) As no re-payment schedule is expressly agreed, there is no overdue principal and interest. The Company has not granted any loans secured or unsecured, to firms, Limited Liability Partnerships or other parties covered in the register maintained u/s 189 of the act.

I understand that this would have been a part of the re-arrangement of the two Gokul companies, but should one be concerned about this? Views are welcome.

COVID Impact

As per Note to AR 2020, the company has stated that there is no significant subsequent event that would require adjustments or disclosure in the financial statements as on the balance sheet date. Being a part of the essential commodities industry, GARL was allowed to continue operations / manufacturing facilities of the unit with minimum labour and staff with a condition to provide food, shelter and safety measures; hence, the company was able to manage the same at optimum level. ICRA, in its ratings, has agreed with this assessment.

GARL has however, acknowledged that given the uncertainties associated with nature, condition and duration of COVID-19, the impact assessment on the Company’s financial statements will be continuously made and provided for as and when required. “However, a definitive assessment of the impact in the subsequent period is highly dependent upon circumstances as they evolve”.

Conclusion

GARL has given positive results for the past several quarters. It is operating in a high-demand sector, and the prices of the commodity is also increasing. On first glance, its valuation appears quite attractive, but it is tempered by the fact that the company is operating on very thin margins. However, to me the company seems undervalued at its present CMP. Members may kindly provide further guidance.

Thanks for going through this amateurish attempt. Just to clarify: this is not an advice to invest in this stock, but is an attempt on my part to learn stock analysis. I would be grateful for your comments.

Disclosure: Small position since lower levels.