Gokaldas Exports Ltd 20th January 2020

About the Company

-

The company is one of the largest manufacturers and exporter of apparels in India. The company’s portfolio includes Jacket, Shorts, Pants, Tops/Shirts contributing 23%, 3%, 21%,46% respectively of the revenue. Women and Men segments contributes equally.

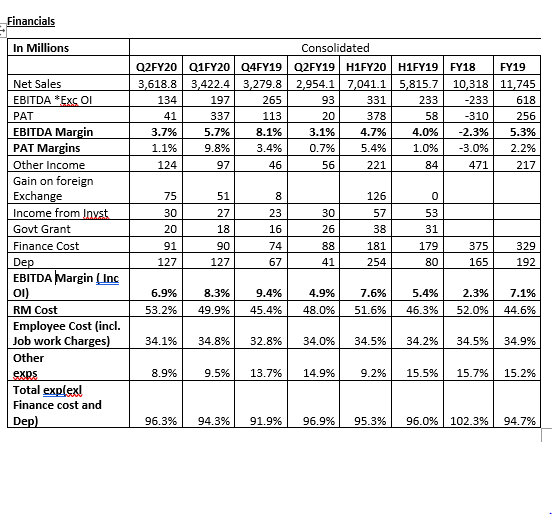

It has 30mn piece annual garment manufacturing capacity with turnover of ~Rs 1174.5crores in FY19 and ~Rs 704.1 crores for H1FY20. -

Clientele includes GAP, Columbia, ZARA, H&M, Adidas, Nike, Lee Reebok, PUMA, etc. Top 5 client contributes 65% of the Top Line.

-

Hinduja Family, now running Capital Float- one of the largest Fintech company, was the original Promoter of the company. The company had come up with an IPO in April 2005 with a fresh issue of 31.25 lac shares at Rs 475 per share aggregating to Rs 133 crores for expansion. The total no. of outstanding shares after IPO was 171 lac shares of FV 10 aggregating to Market Cap of Rs 816 crores at Rs 475 per share. The promoter holding after IPO reduced to 76.90%. The turnover was Rs 720 crores with a reported PAT of Rs 39 crores in 2004-05. In FY06-07, the shares got split into FV of Rs 5.

-

Between 2007 to 2009 Blackstone PE bought ~68% stake in the Company at Rs 275 per share from existing promoter and got classified as a promoter with Hinduja moving out and selling its stake over the period.

-

In FY 2008-09, the company reported hefty foreign exchange loss of Rs 70 crores on account of volatility of currency and reported profit of Rs 3.45 crores. Post that the company continued posting hefty losses in FY11, FY12 and FY 13 of Rs 88 crores, 132 crores and 108 crores respectively with revenue decelerating, lower absorption of fixed cost and original promoter moving out from the business after selling stake to Blackstone PE.

-

From FY 14-15 onwards , even Blackstone started offloading its stake in open market and its holding reduced to 39.96% in FY16-17.

-

In FY 17-18, the Director of Blackstone PE fund, Mr. Mathew Cyriac bought Blackstone PE’s stake in the Company in personal capacity with few other investors through Clear Wealth Consultancy Services LLP at Rs 42 per share aggregating to Rs 58.61 crores. Also made an open offer at Rs 63 per share.

-

With Blackstone moving out, Mr. Mathew has brought experienced professionals on board to run the organization. The professionals started undoing things which went wrong during Blackstone era.

Business Strategy

9. Mr. ShivaKumar Ganapati who joined Gokaldas in May 2017 is known as a turnaround strategist in Industry. He was mastermind in setting up of the GNFC chemical plant. Before joining he was the COO of IDEA. Mr. Ganapathi has been with the Aditya Birla Group for more than two and half decades.

Mr. Sathyamurthy is with the company since November 2015.

-

The company has raised ~Rs 70crores through QIP and allotted 77,08,000 shares @ price of ~Rs 90.94 per share on 3rd May 2018.

-

The company is focusing on four-pronged strategy

a. Strengthening of customer relationship by also catering to other brands of existing clients.

b. Operational excellence by reducing wastages

c. Cost effective capacity expansion. The capacity can be increased by two ways

i. Improve efficiency by de-bottlenecking the existing capacities

ii. Greenfield expansion. The company has already purchased 10 acres of land in Andhra Pradesh (labour subsidy is Rs 1,000-1,500/employee) and are also in evaluation process in North and central states for future expansion. The labour subsidy per employees in Jharkhand is Rs 7,000, in Madhya Pradesh is Rs 5,000 and that in Gujarat is Rs 4,000 per employee for five years.

d. Infrastructure – To put in place required IT and other support services which will yield benefits in next 3years. -

The company’s employee cost is ~33% of the sales which is higher than the industry standards. The average industry employee cost is ~25% of sales. Total no. employees as on 31.03.2017 is ~22,000 and majority are women.

Mr. Shiva is working on controlling employee cost by

a. Centralizing each facility/unit, which was earlier decentralized brand-wise.

Illustration: Earlier they had dedicated facility for GAP and raw material procurement was exclusively done for GAP. Thus, economy of scale could not be enjoyed in case of multiple order and multiple vendor. Employees utilization would be at sub-optimal level in case of lack/non- continuous order flow from GAP.

b. Currently employees are not skilled and can only perform some part of garmenting. The company is planning to implement employees training program where each employee would be trained enough to do each part of garmenting. Eg. Currently employee stitching collar is not trained to do buttoning or bottom part, etc.

- The average rejection rate (including wastage) is around ~8-10% and defects are sent back to the company. The new contracts are made in such way that some part of defects would be borne by clients. Eg. New contracts will take care of + or -3% of rejections.

Competitors

-

In India, in garmenting, Shahi Exports is a leader with revenue of ~Rs 6,000 crores followed by Orient craft with revenue of Rs ~Rs 3,500-4,000 crores, followed by Gokaldas with revenue of ~Rs 1,200 crores.

-

KPR Mills, Kitex and SP apparels are not comparable on basis of employees cost with Gokaldas as all three companies are also into knitting which involve high capex. The average employee cost of these companies is ~20% and of Gokaldas is ~33%.

Capex Program -

The capex program for next 3-5 years would be around Rs 200-300 crore which would be met through internal accruals and debt and also the amount that will be received from releasing FD (FD -explained below). No need of further dilution in equity. The company enjoys 25% subsidy on Investment

-

The current capacity is 30mn pieces per annum. The company is operating around 90-92% utilization rate. The company would be increasing 15% capacity from existing facility by increasing efficiency. The Andhra Pradesh green field expansion project is in process and would be streamline by FY20.

Losing on Fixed Deposit -

In the past (8-10 years ago) the company hads secured loan against property, but the property was sold and thus FD of Rs 133 crores was put in place for the same. Due to bank’s complex compliance its not easy to release FD but the company is in process of releasing this FD and the new asset charge has to be created. New asset that will be purchased in future in capex program will be utilized to create charge and the FD will be released.

-

The company’s borrowing rate is ~7% after subsidy which is much better than going for foreign loan.

Client concentration -

Top two customers -GAP and COLOMBIA contributes more than 50% to the top line. The company is process of adding clients and reducing concentration risk going forward.

-

The company has added 5 customers during FY18. The revenue from these clients were 21crores during the year and potential is very huge.

Foreign trade policy and geographical presence -

As Japan offers duty free access to apparel from India, the company is evaluating ways to penetrate Japanese market. During FY18, revenue from Japan was 10-15 crores.

-

Europe levies 10% duty on imports from India and allows duty free imports from Vietnam and Bangladesh.

-

North America contributes ~51% to topline, Europe contributes 21% and Asia contributes 26%.

-

The company’s revenue from domestic market is 18-20% and this is during Q2 when the exports orders are low and the capacity is used to meet domestic demand.

Others -

The company hedges as and when the revenue is booked but MD is working on new hedging policy.

-

The company was having 35+ plants in 2008-09 and post that it started consolidating and today has 22 plants.

Industry size

28. The global apparel retail market is valued at $1300bn with China contributing ~$182bn and India contributing ~$65bn. China is de-growing by 5% and employee cost getting expensive augers well for Indian market. As far as low-cost producer countries are concern, Bangladesh and Vietnam are the direct competitor to Indian market. However, Bangladesh is only into garmenting and it has reached at saturation level. Vietnam is also at peak of its garmenting facility thus leave little headroom for the competitive edge it enjoys.

- State like Madhya Pradesh and Chhattisgarh has come up with various garmenting initiatives. These states are planning to give ~Rs 5,000 per day per employees for next 3years. Though company has purchased land in Andhra Pradesh, it is evaluating various states policy where benefits would be highest.

Triggers

- The company has potential to grow its business by 15% CAGR in next 4-5 years. Thus, expecting top line of Rs 25,000 mn with EBITDA margin of 10-12%.

- Professional on board to turnaround the company

- Rerating in Sales and P/E multiple.

- The global apparel export market is valued at ~$429bn in 2016 with China contributing ~$161bn and India contributing ~$17.4bn. US-China Trade war along with non-competitive labor cost will transfer some of the China’s business to other countries majorly India.

Disclaimer: This is not a buy or sell recommendation. Views are based on personal research from publicly available information

I am holding this stock