Given the current context - where Small and Mid-caps have risen quickly (more because of higher interest in the space & valuations re-rating), it could normalise to long term (factoring in the risks)

While I have been quite bullish here (personal bias), trying to be value conscious as well now.

As the price of Gokex settles, a lot of the Earnings (that would increase) as well as the Valuations (Re-rating due to company’s improved prospects) might have been priced in.

With this, I’ll pause with another appeal to seniors to kindly share their thoughts

(having shared the context) Views invited

@Ruchit_Shah - What is Gokek’s value in your opinion?

Imo, this is an early start. The sector is coming from a downturn and the market trying to discount the real numbers is yet to start. Whether is it peak valuations or not, depends upon the investor’s time horizons. There are some triggers that are yet to be achieved such as FTA or even sector consolidation. Peak valuations are often made at peak margins and my understanding says that we are far from froth. Likely, the game is just starting.

West has been diversifying from China. Indian manufacturers haven’t been able to gain anything and the current numbers are not close to the potential. Gokek’s and the Ministry’s are focussed on the same geographies/params. The froth will likely be there once all the triggers are in place.

Disclaimer: I’m invested in Gokaldas Exports. Me & my family members may be invested in other stocks whose names may or may not be mentioned here. This isn’t a BUY/SELL recommendation.

Given the specific situation (as detailed above),

I would discuss the relevant factors i.e. numbers to get to the Valuation.

And happy to hear contra opinions here.

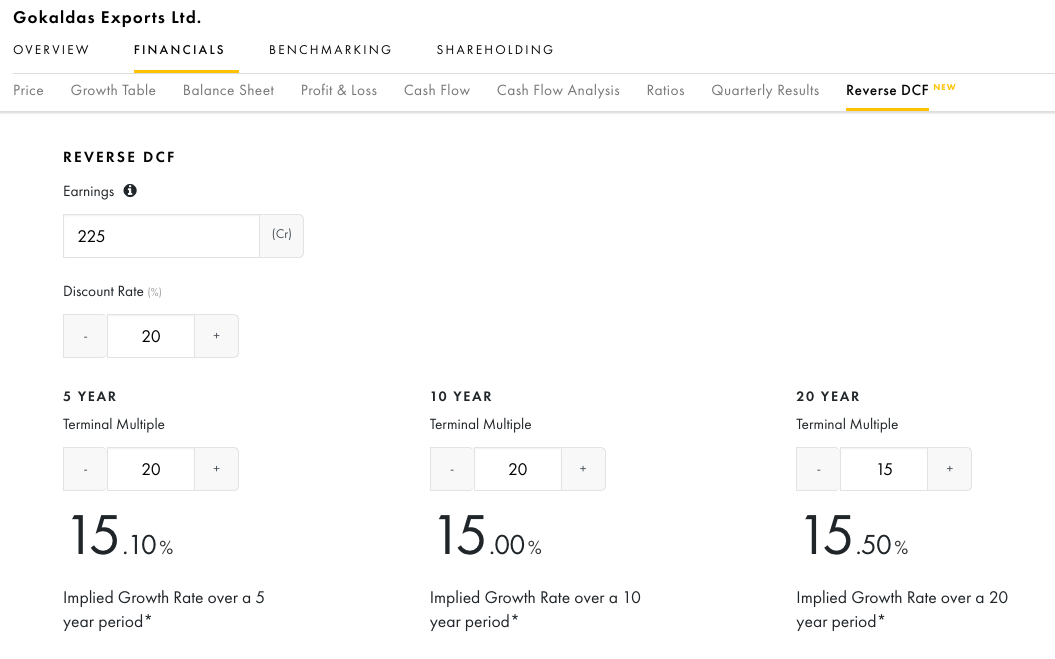

@wiseunwise shared the approach of Reverse DCF above.

It looks like a good way to look at Valuations.

I’m assigning the numbers that look rational to me.

Earnings

Atraco’s current earnings are 30% & 35% of Gokex’s revenue & profit’s resp

Adding a conservative 30% to last yr’s Profits of 173Crs, comes to 225Crs.

Let’s take 2 scenario’s of discount rates 15 & 20% (reasonably high benchmarks)

No of Yrs & Terminal Multiples go hand in hand

A. No of Yrs

Once the FTA’s are in place, the growth should sustain for a long time.

Let’s take the 5/10/20 yrs as scenario’s

B. The Terminal multiple – the average P/E from last 3 yrs, is around 20.

The way Gokex has progressed, by now, it looks like a formidable player.

So P/E of 20 looks like a conservative benchmark.

I’m assigning terminal P/E of 20 on a 5/10 yr period & 15 on 20 yr period

We get a Implied growth rate of 10/ 15% depending on the Discount rate.

The Management has guided for 20% growth rate for long term

(The MD, Siva Ganapathi ji looks conservative in his approach & quite credible, so far)

Onto the FTA, the Textile minister, and Geopolitical context.

The closure of FTA has been widely speculated since a while now.

I have been following Piyush Goyal ji’s mentions on newspapers since a while now, and surely there’s prominence to FTAs.

Also, G20 seems to have gone well, and further consolidates Inda’s position globally.

And daily we are looking at corporates validating India’s manufacturing Renaissance.

So India’s Textile manufacturing growth looks quite assured.

Given all of the above, I’m quite comfortable with the company’s current Valuation.

Disclaimer: Invested & Biased. Imho, the discussion’s primary focus is Valuation.

And in that regard, would humbly request to kindly highlight any apparent mistakes/ flaws in the approach/ thinking to avoid going wrong on a high conviction bet.

Company was expecting Fed rate cuts, which haven’t happened - this will likely impact consumption in US, specially in apparels without discounts (which is how the industry made money in near term).

Looking at all thes numbers and commentaries - are we looking at a few subdued quarters unless export economy picks up ?

Disclaimer: Invested with a small tracking position, and biased.

While it’s not the UK or the EU FTA, signing of India EFTA (Switzerland, Norway, Liechtenstein and Iceland) indicates that UK and EU FTA are realistic possibilities. Deepening trade relations is going to be a positive for garment manufactures from India.

What’s your views on current valuations ?

It has corrected 20-25% from highs and results too have improved compared to Q2 and management guidance of doubling revenue in 2026.

To me valuations look alright especially after acquisition numbers are accounted for. Bet is on management execution and they have done well so far. It can still double from here if execution remains intact and some demand tailwinds come back.

Consolidated EBITDA grew by 48% YoY, but margins were affected due to seasonality and currency impact in acquired entities (kenya).

Generated INR 155 crores in cash from operations in H1 FY25.

Strong order book and favorable market tailwinds.

Revenue growth driven by export recovery, particularly to the US (+33% YoY growth).

Consolidated EBITDA margin was 7% due to seasonality; standalone EBITDA margin at 11%.

Management expects consolidated EBITDA margins to exceed 10% in the near term and reach 12% at steady state.

Targeting annual revenue growth of 15%, supported by capacity expansion and strong demand.

Consolidated production volumes: 14.95 million pieces in Q2; standalone entity contributed 8.1 million pieces.

Standalone revenue capacity for Q2: INR 650 crores, with potential to reach INR 700 crores per quarter at full utilization.

Madhya Pradesh Unit 2 expansion to contribute INR 175 crores annually .

Leveraging global shift in sourcing from China, Vietnam, and Bangladesh to India.

Strategic relationships with major global brands like GAP, JCPenney, Carhartt, and Columbia.

Focus on growing market share with existing top-tier customers and diversifying product offerings.

Approximately 80% of receivables covered under ECGC or supply chain finance programs.

Consolidated inventory strategies supported by robust order book and capacity expansion plans.

Standalone EBITDA margins expected to improve by 1% YoY over FY26 and FY27.

Current facilities operating at full capacity; new expansions underway to meet demand.

Margins expected to improve as global inventory levels stabilize and demand strengthens.

Blended tax rate expected to remain around 22% due to tax benefits in specific locations.

Top five customers contribute 65%-70% of revenue, with significant runway for deeper penetration.

Investing INR 100 crores in FY25 for capacity expansions, including new units in Madhya Pradesh and South India.

Enhancing vertical integration through investments in BRFL fabric processing to reduce lead times and improve cost efficiency.

Increasing automation to boost productivity and operational efficiency.

Strong demand for high-margin products like women’s fashion and sportswear.

Seasonality and currency fluctuations, particularly in acquired entities.

Freight costs and reliance on imported raw materials for certain operations.

Madhya Pradesh Unit 2 construction to begin in Q3 FY25 and operational by H2 FY26.

Incremental capacity expansions at Atraco and Matrix to increase consolidated revenue potential.

Exploring leased capacities in South India for quicker expansion.

25% of standalone raw materials are imported, with higher reliance in Q1/Q2 for winter programs.

Tariff changes and potential policy shifts in the US could further boost India’s export competitiveness.

Order book remains robust, with strong traction in Q3 and Q4 driven by spring 2025 production.

Management confident in maintaining growth momentum into FY26, targeting INR 1,250 crore annual run rate from new capacities.

Expanding relationships with strategic customers for high-value products. Risks:

Dependence on a few key customers (top customer contributes ~27%).

It’s professionally owned. I’ve added the snippets previously mentioned from the post above

Hinduja Family, now running Capital Float- one of the largest Fintech company, was the original Promoter of the company. The company had come up with an IPO in April 2005 with a fresh issue of 31.25 lac shares at Rs 475 per share aggregating to Rs 133 crores for expansion. The total no. of outstanding shares after IPO was 171 lac shares of FV 10 aggregating to Market Cap of Rs 816 crores at Rs 475 per share. The promoter holding after IPO reduced to 76.90%. The turnover was Rs 720 crores with a reported PAT of Rs 39 crores in 2004-05. In FY06-07, the shares got split into FV of Rs 5.

Between 2007 to 2009 Blackstone PE bought ~68% stake in the Company at Rs 275 per share from existing promoter and got classified as a promoter with Hinduja moving out and selling its stake over the period.

In FY 2008-09, the company reported hefty foreign exchange loss of Rs 70 crores on account of volatility of currency and reported profit of Rs 3.45 crores. Post that the company continued posting hefty losses in FY11, FY12 and FY 13 of Rs 88 crores, 132 crores and 108 crores respectively with revenue decelerating, lower absorption of fixed cost and original promoter moving out from the business after selling stake to Blackstone PE.

From FY 14-15 onwards , even Blackstone started offloading its stake in open market and its holding reduced to 39.96% in FY16-17.

In FY 17-18, the Director of Blackstone PE fund, Mr. Mathew Cyriac bought Blackstone PE’s stake in the Company in personal capacity with few other investors through Clear Wealth Consultancy Services LLP at Rs 42 per share aggregating to Rs 58.61 crores. Also made an open offer at Rs 63 per share.

With Blackstone moving out, Mr. Mathew has brought experienced professionals on board to run the organization. The professionals started undoing things which went wrong during Blackstone era.