Investor presentation

2 Likes

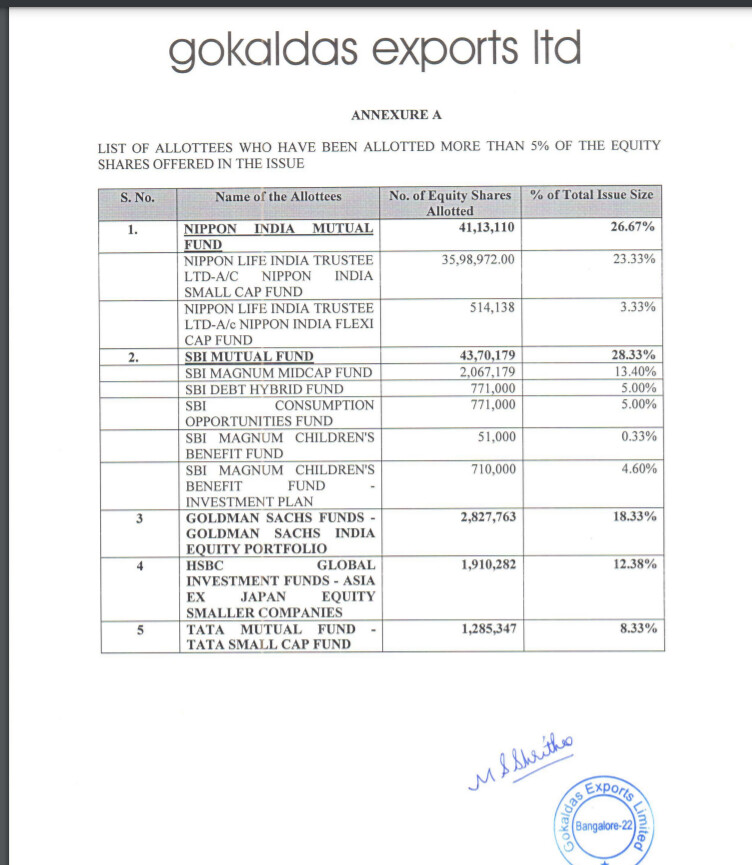

Company has closed in massive QIP of Rs 300 crores which is roughly 1/3rd of the pre-money market cap.

Marquee names of Mutual Funds among the allottees.

So far Clear Wealth seem to have done a good job of turning around the operations of the Company with notable improvements in number of metrics such as product quality parameters, increase in % business from top clients and ofcourse operating margins.

With the infusion of funds hopefully retiring a lot of the heavy debt and planned capex of more efficient factories - there is scope for profit expansion in next few years - as long as execution remains on track.

5 Likes

The Q2 results clearly demonstrate that the company will be at least 2x its size in another 18 to 24 moths with further improvements in margins

Disclosure: Invested

3 Likes

Company delivered another strong quarter and is clearly gaining market share in US exports over competitors.

Another good news is post QIP - Company has reduced Gross debt in half and in fact is now Net Debt free at least for now - before the next phase of capex kicks in.

Company is now operating at 10-12% operating margins - aided by increase in volume - to which Clear Wealth management deserves credit as they have delivered what they had promised in con calls. Interesting thing is to note that it is still a far way behind the likes of KPR and Kitex operating at 20% + margins, although they are backward integrated better than Gokex.

At the current run rate of Rs 30 crores PAT per quarter (120 crores per year) - Company still trades at 20x PE. With plans for expansion and possible margin improvement ahead - it can still re-rate to higher levels.

In hind sight it was a rare low hanging fruit available post Q4 FY21 results.

Disc - invested, biased.

5 Likes

What is also important is that the company continues to invest heavily in expanding capacity and adding value. Capex in last 9 months is 52 Crores. Its new capacities coming up in FY23 will further accelerate growth

1 Like

Suddenly, there is tremendous institutional interest in this stock. SBI MF has acquired as much as 9.5% stake in this company

1 Like

Another very good result with good growth in volumes and surprisingly strong margins.

Company is a key beneficiary of increasing online apparel purchases in the US.

Interesting charts in the investor presentation.

Market seems to be finally recognizing the good work done by the Company in last few quarters.

3 Likes

Q4 Concall Notes:

Demand Outlook

-

Marked share increased. We look at market share per customer: for eg: What is my market share with GAP, with Walmart etc.

-

Our market share is tiny – there is immense potential.

-

Export revenue growth of 58% for FY 22

US – market showed most recovery

EU – market yet to reach pre-pandemic level

In past we had more revenue from US.

In EU – we compete with Bangladesh which has no duty whereas we have 10-11% duty in EU – hence it becomes low margin

US – Post covid US experienced strong rebound. In near term headwinds may be there due to high inflation , lower disposable income with people.

Going forward we could see trend reversing (higher growth from EU) – based on FTA expected with UK and possible FTA with EU.

-

Anticipate higher growth in non top-5 accounts

-

Woven products can gain more traction with opening up of economies

Growth

- Volume growth is not so much but Revenue has grown

Company focussing more on high value garments

Realisation growth is 17% in Q4 - YoY

Outer wear is 41% of total turnover – is a more complex garment. Can be equal to 10 regular garments in terms of value.

Hence no of pieces – YoY comparison may not be apple to apple comparison

- Growth visibility

Going ahead – Quarterly run rate will increase.

Revenue growth in FY 23 ‘is assured’.

In Q4 we were at full capacity utilization (except 3 new plants).

MP will start contributing revenue from Q3 of FY 23 – will ramp up gradually.

TN Knit Fabrics unit – will get commissioned by end of FY 23 – will contribute from FY 24 onwards.

We can have operations in Bangladesh

We are also looking at further new capacities (will announce in due course).

Typically revenue can be 4-4.5 times capex at full utilization.

We have good visibility for H1 – order book is good. (Fairly full capacity is booked). Normally Q3 and Q4 are better months (since we produce for Spring Summer in foreign countries)

On Competitive Advantage

-

Company benefits from covid related shutdowns in China and South Vietnam. Longer time – we can benefit from cost increases in China and Vietnam. However India still doesn’t have a Fabric Ecosystem as good as these countries. Apparel manufacturing is labour intensive - In India labour cost is 160 USD per month, in China it would be 350-370 USD per month. In Vietnam it would be 250 USD per month. Also trade actions against China (for eg: Banning of cotton, increased taxes against them etc) favours us.

-

Not directly benefitting from disruptions from Sri Lanka and Pakistan as they are more into knit garments.

-

Not withstanding short term issues like inflation in US, war in Europe ( which can affect for 1 year or so) – In the Longer term – we would like to keep growth momentum.

-

Challenge is not getting business – challenge is in executing – getting capacity, adapting to newer products (keep changing) and executing on time.

Margins

- RM

Cotton prices are up

But Yarn prices are not up that much

We only buy fabric (not cotton)

Cotton is 60% is total fibre mix.

Linen and Viscose is another 10-12%

Rest will be MMF (Polyester, Nylon etc)

Woven fabrics – price increases are in the range of 10% YoY – as cotton content is that much

Have long term contracts with suppliers

Have the ability to pass on cost increase to customers

- Labour – Once a year – we give wage increase

April 2021 – Wage was increased by 4.5%

April 2022 – Wage increased by another 4.5%

We typically offset this by productivity growth – It has been 3.5% p.a. over last 5 years

- Margin - Other points

Weakening rupee partially helps in margin improvement

Gross margins fluctuates based on products

In Outer wear – RM content is higher

Q4 sales had higher proportion of Outer wear

On absolute basis – costs are lower QoQ

Employee cost -

Employee strength is now 32,000 +

In Q1-Q3 – we made higher employee terminal benefit provision

Provision was party reversed in Q4

Margin in Q4 is overstated by 1% due to above

Guided for employee cost of 30% of sales going forward

Margin Guidance - Cost pressures are there going forward. For eg: Wage increase – but can be offset by productivity gains.

Overall for FY23 – should be at par with FY 22 levels

(Not factoring additional ESOP costs – issued recently – vesting period is 3 years – can be approx. 5 crores per quarter – i.e. 1% of sales.)

When sales order is accepted – we do costing and lock material prices with suppliers – so to that extent RM costs are passed on to customers. (around 25 min mark). Prices are locked for ~ 2 months with suppliers.

A Lot of our RM suppliers are nominated suppliers – We get into 3 way discussion with Customer, Company and RM suppliers.

All these safeguards allow us to price the products as per our requirements.

Working Capital Days

Debtors days to be 25-28 days going ahead

(Reset from ~ 50 days previously due to early payment programme initiated by the Company)

Also got better terms with suppliers – have increased payable days.

In FY 22 – Inventory days was not optimal due to logistical disruptions – Can improve going forward.

PLI Scheme

We applied for PLI – under MMF category

Factory is under construction in MP

Will take atleast 1 year before Factory commences operations.

Target revenue for HS codes covered in PLI is Rs 200 crores.

Govt will give 11% P.L. Incentive in Year 1. In Year 2 – Govt expects 25% growth over Year 1 – Total revenue – Rs 250 crores and for incremental revenue they will give 9%.

For 5 years – it becomes 11%, 9%, 7%, 5% so on sequentially – Incremental 25%

By the time the benefits are realized – it will be FY 25.

Further investments beyond 100 Crores – not required to realise PLI benefits.

Capex

Will encash all FDs in FY 23

3 New Units in Karnataka and TN – Ramping up well – Contribution from all 3 new plants in Q4 was 40 crores. Utilization level for these plants was 50-60%. Annual run rate can be 220 crores per year when fully utilized. In these plants – capex is lower (asset turns of ~ 10 times) as some of it is leased – proportionately opex would be higher.

Initiated work for Greenfield capex in MP – should be completed by end of June or July post which it will be under trial productions. Full ramp up expected in 9 months.

FY 22 – for new plants we invested 22 crores. In existing plants (capacity expansion and modernization) – invested 18 crores. Also invested 30 crores in New projects not yet operationalized – MP and TN Knit Unit.

FY 23 – total investment plan is 160 crores. Normal capex in existing plants – 20 crores (for productivity improvements, modernization) . New projects (MP etc) – 70 crores. Another 70 crores in TN Processing Fabric unit.

Contemplating whether to buy or lease manufacturing unit in Bangladesh

6 Likes

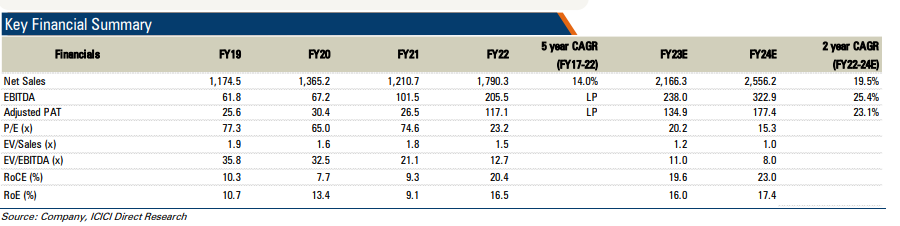

Based on management commentary in Q4 concall - Next 2 years projections by ICICI Direct in research report. (Report in public domain)

I feel topline can be higher in FY 24 based on below back of the envelope calculation - as long as utilization remains at current levels (close to full)

Existing Revenue for Q4 FY22 annualized = 585*4 = ~ Rs 2300 crores

Add: Incremental revenue from 3 new units in KA and TN = Rs 80 crores

Add: Revenue from new Greenfield unit in MP = 400 crores

Total - approx Rs 2780 crores.

This does not include revenues from unit in Bangladesh and New Capex for Knit fabrics in TN (management had indicated in Q3 concall that some of knit fabrics production would be captively consumed but overall RoE on that capex will be 20%)

PLI benefits on new unit in MP - directly adds to margins.

Mr Sivaramakrishnan Ganapathi has so far walked the talk and in fact delivered better than promised. Near term challenges in end user demand will remain but Company seems to be well poised to cater to demands of global chains like GAP, HM, Walmart etc by delivering quality garments, within given timelines and most importantly with the operational efficiency that is flowing down to its bottomline.

Management explained the business dynamics in an extremely clear manner in Q4 concall.

(link - Gokaldas Exports Ltd Q4 FY22 Earnings Concall - YouTube)

Disc - Invested from lower levels and biased.

8 Likes

The latest Q1 FY23 call provides great insights into the company’s plans. It’s firing on all cylinders. With expansion in Karnataka, TN and MP on schedule, and the possibility of the Bangladesh plant in FY24, Gokaldas has the potential to be the leader in Garment Exports. It has so far kept all promises. The MD has a tremendous understanding of the industry and is on the top of things. Barring reasons such as logistics challenges, it should see a topline and bottom line growth of over 20% CAGR for the next five years

6 Likes

Clearly a decent set of numbers in Q3 FY23. Now, with additional capacities implemented , we can perhaps expect higher volumes in Q4. The only spoilsport could be the looming recession in US

Gokaldas is one of the most consistent players in the Garment space

Disclosure: Invested

3 Likes

Stock is up 10% in past two weeks. Is anybody aware of any material news that is in the offing.

Disc: invested and tracking

Gokaldas Q4 investor presentation (https://www.gokaldasexports.com/wp-content/uploads/2023/05/Investor-Presentation-Q4FY23-Gokaldas-Exports.pdf) slide no 17 to 27 is a gold mine on macro indicators for the textile industry and must go through for any investor looking into the textile sector. The Indian textiles sector has been benefiting from china+1 story over the last few years(China has maximum market share in global apparel export).

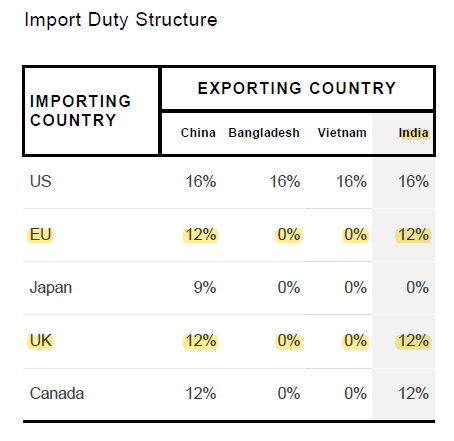

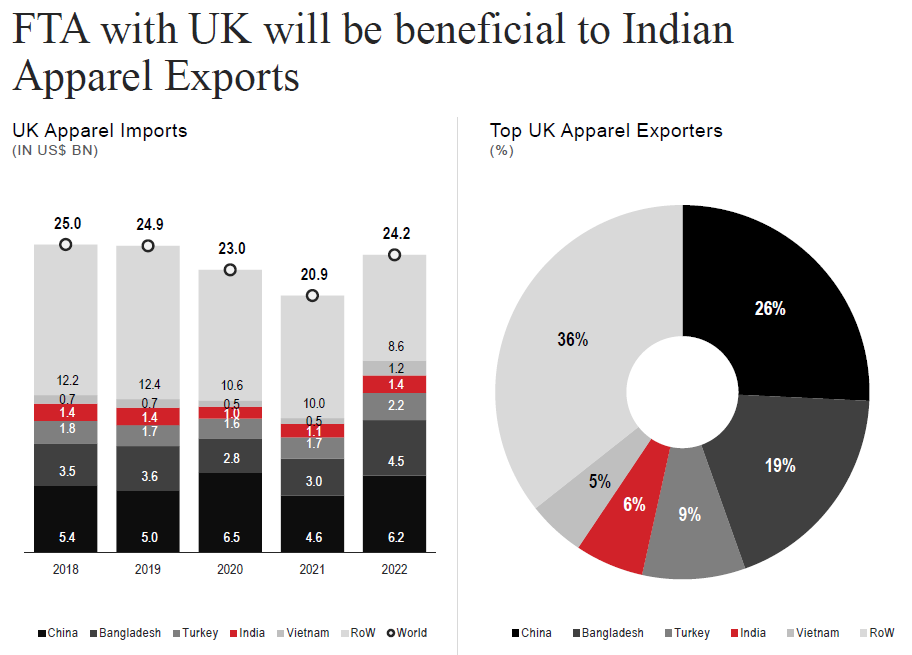

Another interesting opportunity for Indian players is to compete with countries like Bangladesh, Vietnam who have significant market share in the UK/EU region.

Currently Indian textile companies exporting to the UK/EU have 12% duty compared to 0% on countries like Bangladesh and Vietnam.

With the ongoing free trade agreement between India and UK, if the import duty structure is removed then it will put Indian companies at par with Bangla and Vietnam. Currently they have 26% and 9% market share respectively compared to 6% by India.

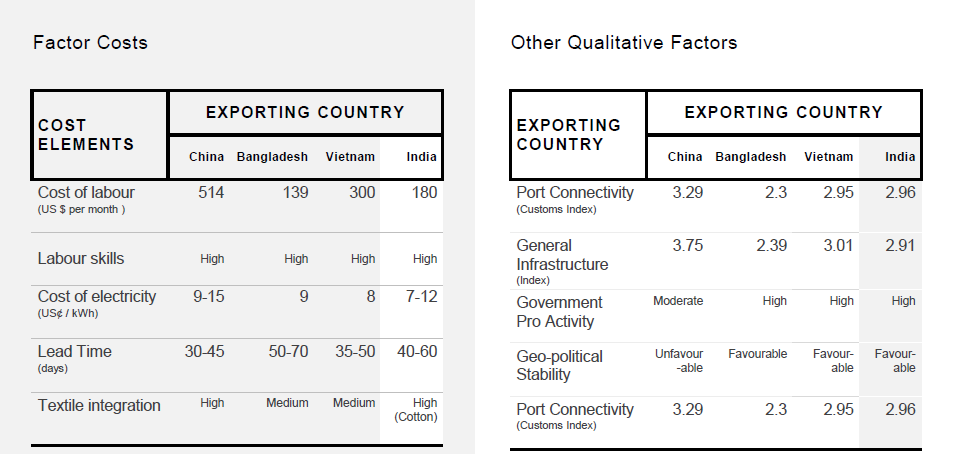

India is reasonably comparable/better to other countries in terms of labor cost, skills, textile integration, port connectivity and govt support.

Currently India has done 9 rounds of FTA negotiations with the UK and four rounds with the EU. Let’s hope for some final deal which can help Indian textile companies like Gokaldas.

Disclosure: tracking quantity.

12 Likes

Can’t see FTA with the UK happening by the end of 24

- There seem to be 26 chapters that have to be negotiated [Source: Indian Express]

- 14 out of 26 have been finalized in all the talks - till a couple of months bach

- From what I understand, usually one round of talk happens in one month. Not all talks bear equal fruits.

- Remaining year has G20 and then elections. Assuming the focus will be lesser on FTA due to the nature of politics.

https://twitter.com/pforproduct/status/1686079723989090305?s=20

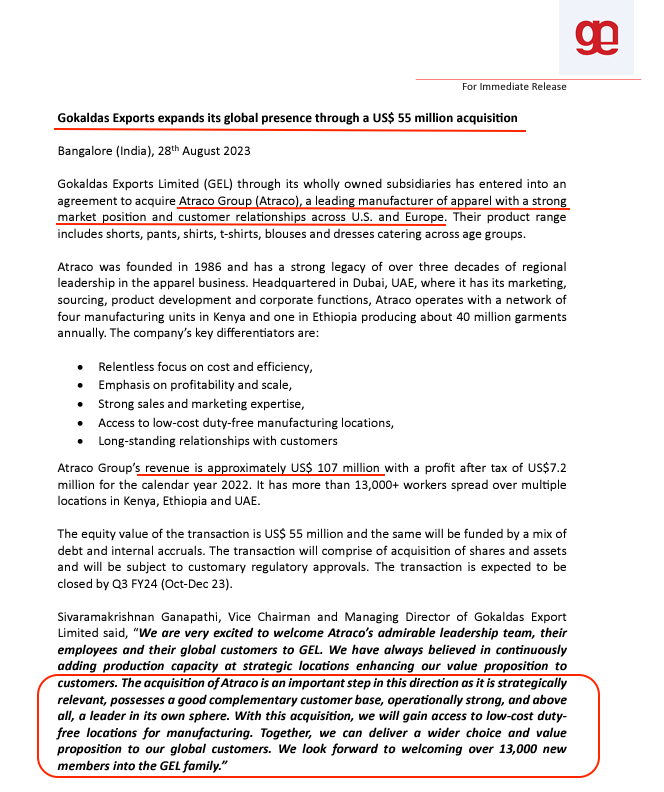

Announces a substantial acquisition of the Atraco Group (est. in 1986) at an attractive 0.5x P/S

During the Q1FY24 concall management had indicated they will deploy the excess cash towards an inorganic opportunity if they could foresee market traction in H2 FY24 and a strong FY25. This news could be an indication of what is to come.

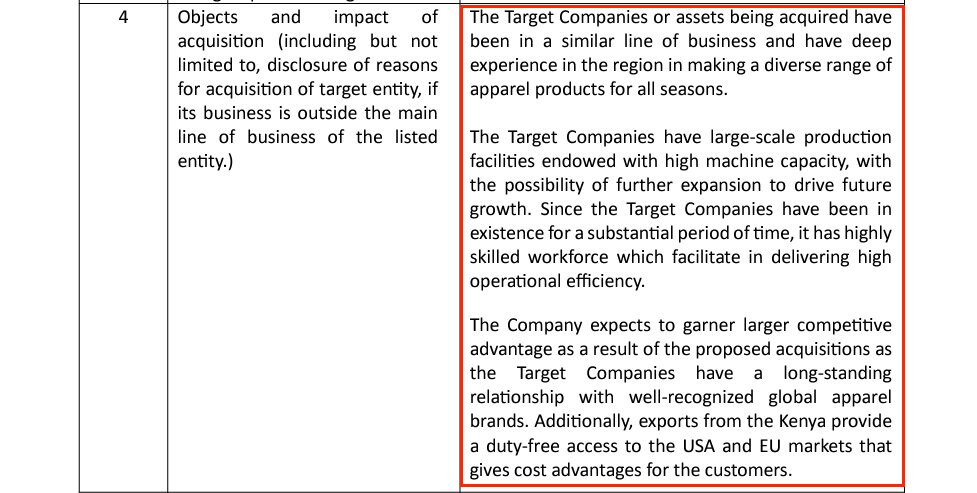

- Large scale production with high machine capacity

- Possibility of future expansion

- Highly skilled workers & high operational efficiency

- Established global brands as customers

- Duty free access to USA & EU markets (cost advantage)

The deal involves a group of companies operating across various geographies and thus require several regulatory approvals. However, deal is expected to be concluded by October - December 2023 (Q3 FY24).

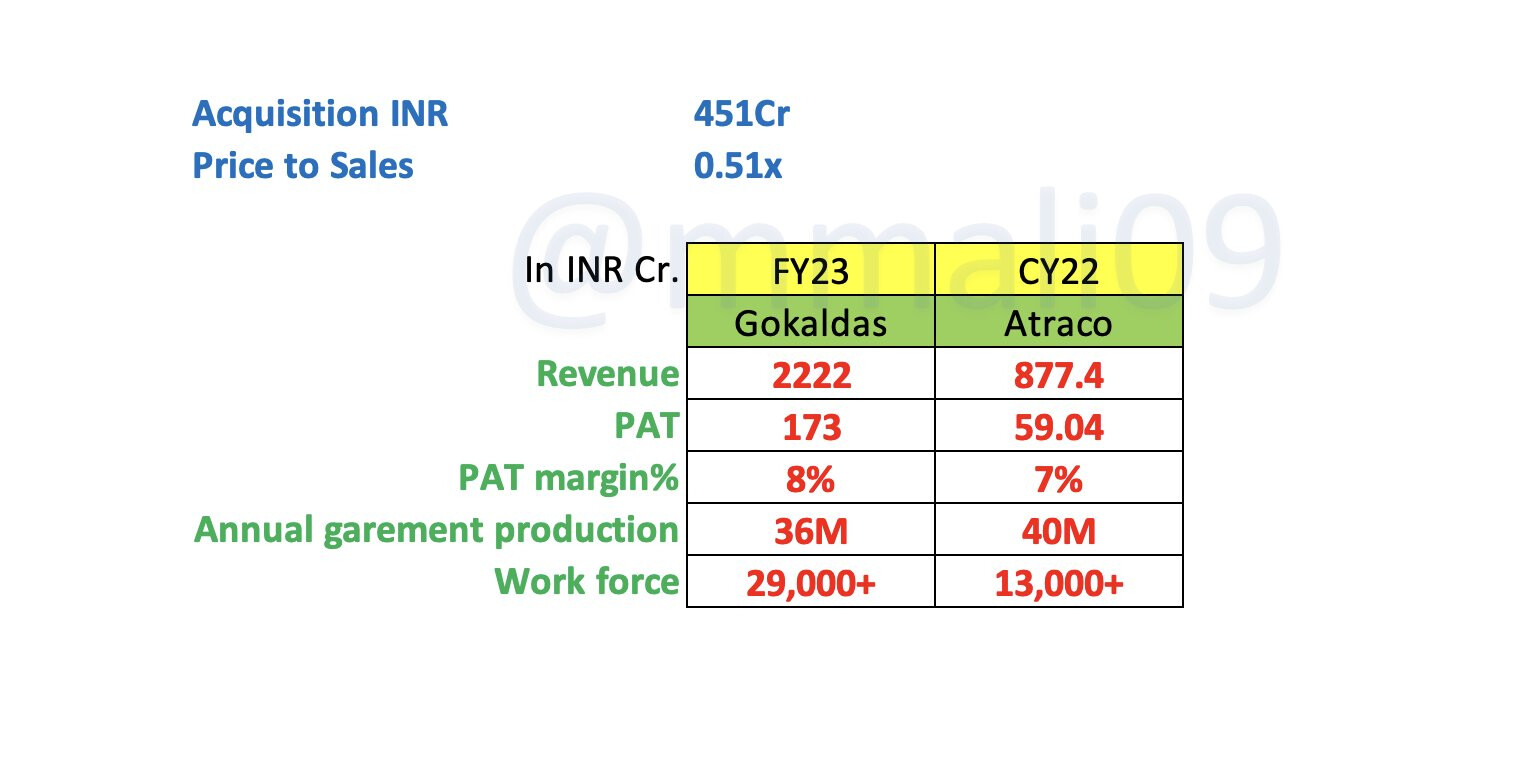

To give you a perspective on the Deal - Its BIG !!!

Approx. INR nos.

At a consolidated level this is a substantial deal, i.e., about +60% Revenue/PAT as a % of FY23 Gokaldas Exports nos.

Investor’s call is scheduled tomorrow. If someone attends, would appreciate if you could share some key highlights.

6 Likes

mp points in the concall.

- Financing of acquisition is done through 40mn of debt and the rest through internal accruals.

- The acquired entity has prod. cap of 40mn with closer to 90% capacity.

- Acquired entity has USD 15mn of wc.

- Bangladesh there is noise of minimum wage hike-if that happens it will benefit Gokaldas.

- 20 mn of revenue is expected to be add in future depending on the market conditions.

- Dec 2025- duty free access to kenya ends.

- The management is confident of duty- free access renewal as kenya has strong ties with US region.

- There is no tax on profit earned by the acquired entity.

- Labour cost in kenya is a little higher but productivity is more efficient.

- There is good revenue visibility of order book for the acquired entity.

- The client of acquired entity is different from Gokaldas barring 1 company.

2 Likes

Notes on Atraco Acquisition

(from Company release, Management Interviews & con-call)

Quick info on Atraco:

It’s a well-established Dubai-based garment manufacturer.

The HQ in UAE covers functions of Product Development, Marketing, with Manufacturing based in Africa (4 units in Kenya & 1 in Ethiopia)

The co produces about 40 Mn garments (with a 74:26 mix in Woven & Knit).

And the customers include 40-50% Children (newer segment for Gokex)

Co is tax-free, being based out of Dubai.

Customer base is 95% US based with only 1 common customer

The key advantage it offers is being a low-cost duty free manufacturer.

Kenya has duty free access to US. The agreement governing it, AGOA is due for extension in 25, The management is confident of the extension.

Ethiopia has duty free access to Europe, while US access has been temp suspended.

Financials

Group’s revenue is about $107 Mn with a profit after tax of $7.2 Mn for 2022. (after a 1 time cost of $1Mn)

That is at 30 & 35% of Gokex Revenue & Profitability base.

So the company is of a substantial size from Gokex standpoint.

The EBITDA (adjusted) – 10.5%

Could improve by 1.5 -2 % in 2-3 yrs from Productivity gains, Modernisation . Management expects a growth of 25-30% in next 2-3 yrs

And would be incurring Capex of 4Mn in FY24/ 25

The current utilisation is at 88-89%

Valuation

The deal valued at $55 Mn & expected to close by Q3.

It is funded by mix of debt (40 MN $) and internal accruals

They have Working Capital of $35Mn & Debt of $15 Mn.

That makes the deal’s effective cost to be $35Mn (55-35+15)

The Owner is aged & selling to ensure proper Succession to Legacy.

The Mgmt is seasoned & to continue.

Previous Expansion plans

Gokex had suspended the Bangladesh expansion plans for time being, with multiple factors in play – rising Cost structures (min Wages to be revised) & global perception becoming less favourable.

Capital Allocation

The Management’s clearly focused on anything being a strategic fit first -

Adding capabilities in Low Cost regions, and ensuring sustainability of operations.

Further, looking at Attractiveness of the Opportunity - this deal provides comfort as it is akin to Buying Growth at low Valn.

Mgmt has been extremely focused on being Conservative & Execution oriented.

With this deal, GokEx moves towards being a truly global garment Exporter.

Disclosure – Invested & Biased.

Sources – Concall, Media release, Interviews on CNBC TV 18, BQ Prime.

https://twitter.com/CNBCTV18News/status/1696383371738599424?s=20

13 Likes

Gokex’s valuation has already risen 40% in the 2 days since the acquisition.

‘Value that Deal can provide v How much is Priced in’ might be seen overtime.

The thought process is to Invest for long term.

Best of Investors (inc RJ Sir) have added upwards to their Winners & made most Wealth in a few big bets.

How should one think objectively when they have a potential big winner?

And also prevent oneself from getting delusional in thinking something is a bigger winner than what it actually is i.e. When to consider Valuations as extremely Rich?

Views invited - Experienced individuals (generously sharing their wisdom) - would request to spare time to discuss here.

It would be extremely encouraging to understand the thought process.

Thanks in advance

2 Likes

Following this.

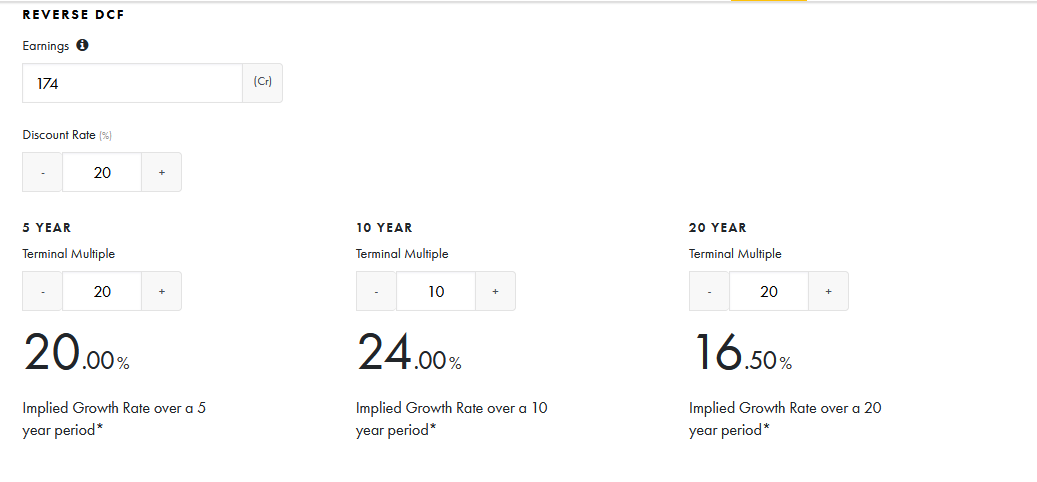

I just did the Reverse DCF for Gokaldas after the ~38% jump in share price over the past 2 days.

Used TTM PAT as the Earnings input (which is a conservative estimate only as net PAT over past 5 years divided by net CFO over the 5 years is 49%). Assuming that I wish to make 20% CAGR over the next 5 years, the implied growth rate still comes out to be 20%.

With the increased number of FTA agreements in discussion and likely to be concluded over the next few years, would it be fair to say that Gokex is still fairly valued?

Disc: Invested and Tracking. Noob alert.

2 Likes

Thanks for highlighting the overall approach of Reverse DCF.

(considering the context here is Valuation primarily)

I understand the tool is from Tijori Finance

The Earnings of FY 23 has been subdued considering the Global Macro’s and Retailers reducing the inventory.

Anyways, given the Acquisition, the future earnings would be benchmarked post Merger (including Atraco no’s)

Currently, that would increase the Earnings by around 30-35%

Coming to the other variables.

-

Discount Rate of 20%

-

Terminal Multiple - While historic reference usually would be a good measure, there are multiple reasons for Rerating of the Sector as well as the Company.

-

Implied growth rate over ‘x’ period No of Yrs before assigning a Terminal Multiple - how long the company grows at above the terminal growth rate.

Eg. FTAs provided Bangladesh with a long runway to grow above average. -

Once these are through, we get the Implied growth.

The management (who has been quite conservative so far in their guidance) has benchmarks of 20%

Considering the specific situation on each of the factors, (play of the Art & Science of Valuation) - looks like this would be interesting to explore in more Depth.

Disc: Invested & Biased.

1 Like