True, Corona has forced people to rethink where balancing point is between careers and personal life. It has created a definite shift of balance towards personal life if individual is not hard pressed for monetary gains career brings.

1 Like

It is too early to say anything and I feel we are ineligible to comment on a new person without seing the actions and giving reasonable time at that position. From what little I am aware, she has taken good decisions with Godrej Agrovet to bring in right leaders, she was with board of GCPL also since long time. She has the element of “kindness” and “calmness”, as evident from her opening lines at the helm of GCPL, that generally lacks in business leaders.

Very few business leaders have these qualities - Ratan Tata and Noel Tata are the only ones which come to my mind right now…and believe me, when kindness and calmness gels with business in the right proportions - the result creates history!

Disc: Above should not be considered for or against any new CEO/management. Above is only a perspective where any new person in any task should not be judged prematurely and based on profiling. Noel Tata was the least aggressive among all Indian retailers a decade back and investors were impatient. Bang came recession and many retailers perished. It was then that Trent rise began.

I also confess my initial reaction was to judge immediately as well, but then took a pause, read more, assimilated thoughts in perspective and came to above conclusion for now.

GCPL, Trent part of core portfolio so views may be biased

8 Likes

4 Likes

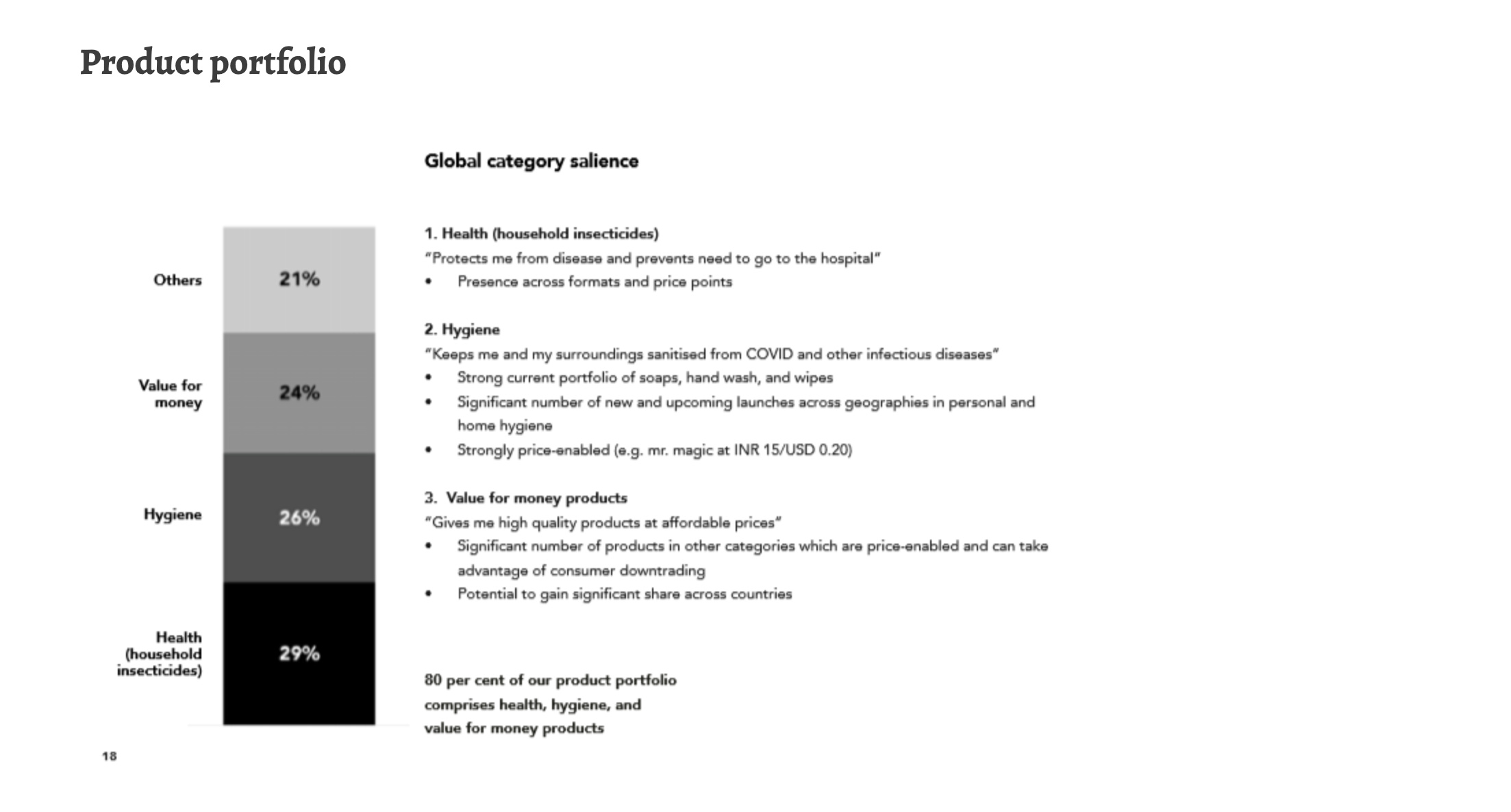

Godrej has launched some good needed health & hygiene products under Protekt range. I was particularly impressed with the W95 masks available on Flipkart. It shows their agility and confidence to chart into new territories. Apart from GCPL only wildcraft has launched a decent W95 so far. It is very much needed by consumers and masks, although part of its hygiene portfolio, but are a different segment all together. Good to see them bring it to market.

Disc: invested

6 Likes

As rightly said it’s too early to comment on Nisana. We are missing undernoted points:

-

GCPL is established player. Work being done right now would continue as there are many other moving parts in the wheel Other than MD.

-

Although in background, Mr Adi Godrej would keep an eye on working of MD A and where every required would do course correction.

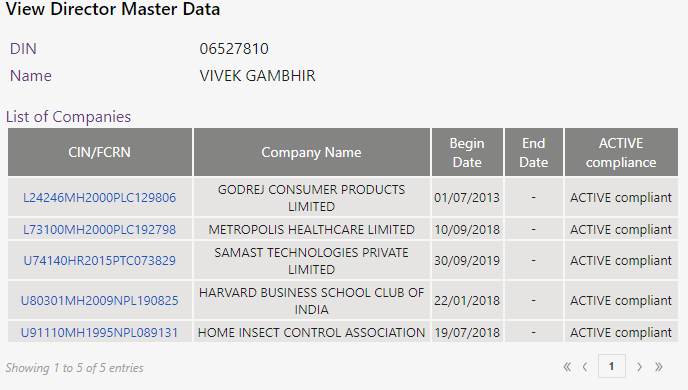

The resignation of MD create some doubts on the vision/thinking of MD and Promoter. As the The MD cite the reason of Health Issue and family problem, but still holding directorship in other company including in Metropolis Healthcare.

Quarterly Update: 1QFY21:

We expect close to mid single digit, volume driven sales growth in the quarter.

Company has had flat sales/profits. My concern is that there is likely to be no-margin expansion in products priced so low

Wide range of Godrej Protekt Hygiene products are now available at Amazon India. Earlier those were available to purchase from their website.

Godrej Protekt Health Bath Soap

Godrej Protekt Health Body Wash

Godrej Protekt Germ Protection Dish Wash Liquid Gel

Godrej Protekt Germ Protection Fruit & Veggie Wash

Godrej Protekt Multi-purpose Disinfectant Spray Cleaner

Godrej Protekt Disinfectant Spray - Air & Surface Sanitizer

Godrej Protekt Multipurpose Disinfectant Liquid

Godrej Protekt Anti-bacterial Skin Wipes

Godrej Protekt Disinfectant Surface Wipes

Godrej Protekt P-W95 Reusable Face Mask

Need to watch these product links to understand product acceptance as most are Me-too products.

5 Likes

That’s a very nice collection of data. I am a bit curious that Godrej consumer is one of innovative indian FMCG MNC. Unlike a Dabur, Marico it focusses only on non food FMCG products. I see that they are not very rigid in their product ranges but they seem to always be on the non food side of the spectrum… something like a P&G which is more into home products than say a Unilever which has personal products as well a food segments. Somehow with the dynamics of FMCG business, I do not see any significant strength in sticking to any subsegment unless you are supreme market leaders like say a Colgate in oral care or a Reckitt in hygiene etc. While Godrej has that edge in insecticides but that’s supposedly not enough for their ambitions so why not a food segment yet? Any insights or thought process welcome!

3 Likes

Hi…

Just posting my thoughts on the issue -

GCPL has been present in the soaps mkt for a long long time now. Their old brands - Cinthol, Godrej No 1 seem to have plateaued.

They missed the bus when it comes to hand washes where lifeboy, Dettol are making a killing. Then they tried entering the space with the Protekt brand but coudnt do as well as expected. Susequently tried the same with Mr Magic…and boy, they seem to have struck gold. It has been flying off the shelves - due affordable pricing and inovative format.

Now the next challenge is to build the brand equity of the Protekt Brand. Once that is achieved in a descent way ( be it in soaps, handwashes, dishwash, sanitisers ) and a descent consumer mindspace is established, GCPL’s growth runway can really get extended.

Beyond, Household insecticides, air freshners and hair dyes ( where they are mkt leaders ) , the turnaround in Protekt range of products is where the company seems to be investing a lot of energy.

Once this is achieved, only then will they venture elsewhere…thats my feeling.

In foods - Godrej Agrovet with their range of frozen foods and Jersy range of Milk products seem to be turning a corner ( courtesy - lockdown and increased In- Home consumption ) . Basically the foods franchise may remain under the Agrovet banner…thats is where it is headed as of now.

These are my just views.

Disc : invested in both - GCPL, GAVL

7 Likes

Indeed, the group seems to satisfy their food ambitions via agrovet. I think they are loosing significantly by having them under seperate roof like how when sampann was with Tata chemicals… anyways that’s a decision for to them to make, for me as a GCPL shareholder, would have liked to have a foods portfolio enjoy the massive existing distribution and brand strength, specially when they already have it within the group. Thanks

2 Likes

Godrej brand is the same in both. Also both enjoy the same distribution reach given that they are from the same group.

That may not be true considering GCPL and agrovet are seperate entities with different distribution networks. There should nothing be common between the two except the same group. That’s why groups restructure if they want to enjoy synergies and as per their visions…

2 Likes

They are both subsidiaries of listed Godrej Industries. Godrej Industries own ~25% of GCPL and ~60% of Godrej Agrovet. So, not sure if there is issue in sharing distribution network.

A different example is Zydus Wellness which uses the doctors network of Zydus Cadila to promote their health products. So, unsure if there is any technical problems.

4 Likes

3 Likes

Q3 results are out and largely inline with expectations, maybe slightly better.

One strange this is that dividend declaration was cancelled! Also, I see dividend declared in 2020 was much less than earlier years.

Anyone aware why dividend this time was cancelled and why it has been declaring lesser dividends? Any new policy from company under new management?

1 Like

They have a poor capital allocation track record something which has come to haunt them over the last few years.

Their India business is a cash generating machines. GCPL enjoys strong market positions in the bulk of their India business – #1 in Household Insecticides, #1 in hair dyes and #2 in soaps. The entire operation makes 75%+ ROCEs and grow in mid to high single digits. The business needs negligible capex and works on a negative working capital cycle – pay your supplies later and sell on cash to your distributors. On its own, this business is amongst the most profitable FMCG business in India easily comparable to HUL or Nestle. Given that the business grows barely around 10% and generates 75% ROCE, you can imagine there is massive excess cash being generated every year. The promoters could have chosen three ways to make use of this excess cash 1) return it to shareholders via high dividend payouts. But they haven’t – HUL and Nestle have 80-90% payout while GCPL has averaged <30% for most of the last decade 2) aggressively invest in their core operations – may be cut prices in insecticides to drive rural penetration or may be invest aggressively to build hair colour distribution in the salon channel where Loreal absolutely dominates them. Or may they make a ‘serious’ marketing effort to extend their Cinthol brand into adjacent personal care categories. My point is that could GCPL not live with a 35% ROCE instead of 75% but drive 15% revenue growth instead of a mid-single digit growth? The ‘optical ROCE’ drop by investing in core areas is not necessarily dilutive to intrinsic value as growth is higher and can sustain for longer. 3) GCPL has instead chosen the third route – using the excess cash to acquiring business in Africa, United Kingdom, Latin America and Indonesia. And that has not turned out well – the capital deployed there has earned sub-par return versus what shareholders would have hoped to earn was the capital returned to them.

People will point that its easy for me to say this with the benefit of hindsight. I won’t argue to that point except that base rates also suggest that inorganic international endeavours by Indian companies don’t work – no matter how convincing a story the management and the PR machinery portrays at the time of the M&A. Its surprising that even now GCPL management is open to more international M&A as stated on their recent results call.

Between FY10-20, GCPL invested bulk of its excess cash from India into international markets. As of FY20, international markets comprise 80% of the capital deployed and have earned an average of 7% ROCE over FY10-20. That is about a shareholder would make by investing in Indian FDs without the need to venture in exotic regions like Africa. A smart investor would have used the excess cash from ‘optimally paid’ GCPL dividends to invest in far better opportunities.

70% of GCPL’s business in Africa is selling hair ‘wigs’ to African women. Do spare some thought as to why an Indian FMCG company is selling hair wigs to African women in a commodity market rampant with imports from China. The hair wig busines is not even your typical FMCG business – it is more like fast fashion, low gross margins with fast changing styles.

Some people would again point that GCPL has screwed up in Africa but done better in Indonesia. I am afraid that’s only partly true. The Indonesia business on its own earns a ROCE of 45% but then GCPL did not get it for free. They paid the former sellers, right. It’s like if I invest in HUL at market prices, I don’t make a 100% ROCE like HUL reports, my ROCE is actually sub 5%. Coming back to GCPL Indonesia, the reported ROCEs for this business (including goodwill) are about 20%. This after nearly a decade of investing in Indonesia. Compare this to the 75%+ ROCE made by the Indian operation.

Obviously, following a large international playbook is risky and not sustainable and if GCPL got away with Indonesia, the larger subsequent bet in African hurt them badly.

This begs the question – why would have GCPL done this? The promoters have their own grand answers which you will find if you read the last 10-year annual reports. But here are some reasons I could think of 1) thinking they ‘own’ all the cash generated and would rather invest it somewhere than return it back to minority shareholders 2) investing in M&A helps build topline, increases international presence – this well serves promoter interests of being seen as owning a large multi-national business – the business press rewards revenue and market cap size and not efficient use of capital (RIL is the best example) 3) sometimes – it’s just plain overconfidence. Knowing well that others have struggled to do it does not deter them – it’s what Daniel Kahneman calls taking only an ‘insider’s view’: doing a biased internal assessment but failing to take other people’s opinion especially from those who have attempted something similar. Everyone succumbs to these biases – companies and individuals except that there is a minority among both who are better able resist these temptations or wager in smaller bets at a time.

Don’t forget that at the consolidated level, despite all the international adventures, GCPL makes a ROCE of 18-20% which puts in a good place and better than a vast majority of Indian businesses. The point here is that a potentially 75%+ ROCE business with consistent high payouts (which could have been re-invested by investors elsewhere) was reduced to a 20% ROCE business due to poor capital allocation. Adi Godrej in 2010 had guided for GCPL to grow its revenues by 10x in 10 years. Not only have they just about reached half of that mark but with sharply deteriorating incremental ROCE.

31 Likes

I must say excellent write up! With nisaba at the helm, what significant changes, positive or negative, do you see now? Also, why have a professional CEO system changed to bring godrej as CEO…is this some sort of red flag for you? Lastly, you talked about dividend…this year they even reduced it drastically and I don’t see any explanation from management anywhere about why…are you aware of any change in dividend policy?

Btw. Capital allocation is really a big big problem with almost all indian promoters…it’s really unfortunate and I think it comes from our developing mindset (unlike developed mindset of US/Europe) where in a developing mindset, we always tend to look at next business or next place to invest/grow while completely neglecting what we already have and nurture/sustain that. Above are just my thoughts and I maybe wrong in my assessment. Thanks

3 Likes

With nisaba at the helm, what significant changes, positive or negative, do you see now? Also, why have a professional CEO system changed to bring godrej as CEO…is this some sort of red flag for you?

Not a red flag per se but one would have liked to see a professional as CEO. Most Indian promoters have handed over CEO reigns to professionals after reaching a certain size (Asian, PIDI, Dabur, Marico and many more). There are exceptions ofcourse but unless the second generation is as passionate about the business and willing to invest 200% of their time, it is better to get in professional management. This is what GCPL had already done and now they have gone back in reverse. Also I have mixed feelings about Nisaba. Several of her pet projects have not done well - B-Blunt, Natures Basket in the past while some have done well like the Fast Card (but not sure if promoters wrongly hog the limelight for successes while putting the blame on professional managers). For example - Nisaba still thinks Africa was the correct decision and it was the failure of the African leadership to execute. She also called out their India CEO, Sunil on the recent call for poor HI performance. These dont speak highly of her leadership style I am afraid.

Lastly, you talked about dividend…this year they even reduced it drastically and I don’t see any explanation from management anywhere about why…are you aware of any change in dividend policy?

Dividend policy and payout would depend on their M&A. As I have mentioned in my note, the India and the Indonesia business are very profitable and were they do skip any M&A or over capitalising their Africa business, their payouts should like HUL and Nestle - 80% payouts. But if they do go for large M&A (they have clearly mentioned they are open), the payouts would largely be lower. They may maintain payouts by taking on debt to fund the M&A but that is just taking from one pocket and putting into another. A lot depends on the quality of the M&A also - they might get something which is strategically right but the risk is that they invest in more Africa ‘hair wig’ like companies.

Capital allocation is really a big big problem with almost all indian promoters…it’s really unfortunate and I think it comes from our developing mindset (unlike developed mindset of US/Europe) where in a developing mindset, we always tend to look at next business or next place to invest/grow while completely neglecting what we already have and nurture/sustain that.

Well what matters is to what measure - Pidilite, Dabur, Asian, Havells have all had their bad days with global M&A or entering segments which havent worked that well. But the commitment has been lower as a share of total capital employed and in some cases they have sold/pulled the plug on such endeavours completely. GCPL is not yet there it seems.

9 Likes