High grade pellets would be around 10k per ton rate now.

Annual EPS at this rate is around 100 including savings from Solar power plants.

This is today’s update.

High grade pellets would be around 10k per ton rate now.

Annual EPS at this rate is around 100 including savings from Solar power plants.

This is today’s update.

GPIL Q2FY23 highlights:

Source: Q2FY23 – INVESTMENT VALUATION UPDATE – Financial Odyssey

GPIL’s revenues from operations increased by a meagre 2.57% YoY and decreased by 21.56% QoQ to ₹1307.14 Crs, its operating income (EBIT less other incomes) fell to ₹197.19 Crs (-53.97% YoY and -54.46% QoQ) resulting in a 15.09% OPM, its net profits plummeted to ₹168.64 Crs (-42.23% YoY and -48.46% QoQ) meaning a 12.65% NPM.

YoY, the company’s cost of goods sold (71% of the expenses) increased by 41.55%, employee benefit expenses increased by 24.47% and finance costs declined by 76.54% hence, the majority of the fall in profitability seems to be caused by the apparent increase in COGS (caused by volume growth) but the real reason is the fall in the realisation.

The biggest contributors to the decline in cash flows are a decline in operating income, payment of dues to trade payables and other current liabilities and an adverse change in other current assets.

GPIL imported about 150000 MT in Q2 and the average price was about INR18,000 landed to plant.

The company aims to keep its stake in Hira at a similar level but would like to fully acquire Ardent.

Crisil has revised the outlook from ‘stable’ to ‘positive’ in their recent rating.

When the stock price is down, the risk is less.

Also, the PE has moved from 2.5 to 3.5 now.

Let us see, if selling at low PE works in GPIL or not. (popularized by some advisory service who consider themselves as expert in cylicals)

There’s a difference between known risks and unknown risks. When the export duties were first announced, it was extremely difficult for anybody to make a call with certainty on the future of the business - even the management themselves. You could take a punt by buying the pessimism, but could you know for sure whether the probabilities were in your favour - in both the short and long term? I could not and I’m sure it was the same case for many investors who had been tracking this closely for a lot longer than I have.

By exiting then, I protected myself from the ~20% drawdown in the stock price that followed.

Once we heard from the management, I was more than happy buying back - this time increasing my overall position size.

It’s important to note that the recent rally in the stock came after the duties were rolled back. So without this trigger, who knows how long it would have taken for the stock to get moving again.

GPIL is not a buy and hold stock for me. As much as I love the business and am confident in its future prospects, I’m happy selling and leaving money on the table rather than facing drawdowns in a downcycle.

My conservative rough figures:

Market cap = 5138cr

Cash by end FY23 = 500cr

FY23 EBITDA = 1200cr

FY23 EV/EBITDA = ~3.8

Disc: Invested at 8% of portfolio, looking to trim post 6000cr market cap. This is not a buy or sell recco. Process over everything. ![]()

I’ve figured in 12+ years of investing that it’s almost impossible for me to avoid from drawdowns or time entry/exits. Though sometimes I’ve been able to sell and avoid near-time draw-downs I’ve seen the stock go up within months or an year.

With GPIL though I can never track factory/shipment movements it’s possible by spending 30 minutes a week to understand the trend by following steelmint and especially domain experts like @Rakesh_Arora who have been willing to share their knowledge and give multiple ways to evaluate the company. It doesn’t hurt that GPIL (and peers like Shyam, Sarda) share lot of info.

I’ve been building up my position to < 20% slowly and intended to build it to even ~35-40% when the levies were surprisingly revoked. Not going to chase the stock till more clarity emerges, though with ~160 MT ore reserves at old rates, there’s a long runway.

I’m assuming Q2FY23 is the low point for some time in the future and Q3 FY23 may only be slightly better than Q2. GPIL’s book value will keep going up and it’s always a buy at 1 P/B.

Also trying to figure out if there are turn-around candidates like GPIL was in 2019-20, they may offer higher appreciation, but GPIL with captive mines offers lower risk.

I am currently studying Sandur Manganese and Indian Metals & Ferro Alloys - both are in the metals space, have access to captive mines, possess clean balance sheets and are adding capacities which will come online in a few years.

Disc: Own tracking positions. Not a buy or sell recco.

While Rungta and Shyam steel have been explicitly mentioned, no details about the remaining 6

Kindly note that the prices of Iron Ore w.e.f. 30- 11 -2022 has been fixed as under:

i) Lump Ore (65.53, 6-40mm) @Rs. 4, 100/- per ton

ii) Fines ( 643, -1 Omm) @ Rs. 2,910/- per ton

Note: The above FOR prices are excluding Royalty, DMF, NMET, Cess, Forest Permit Fee and other taxes.

How much is Royalty, DMF etc??

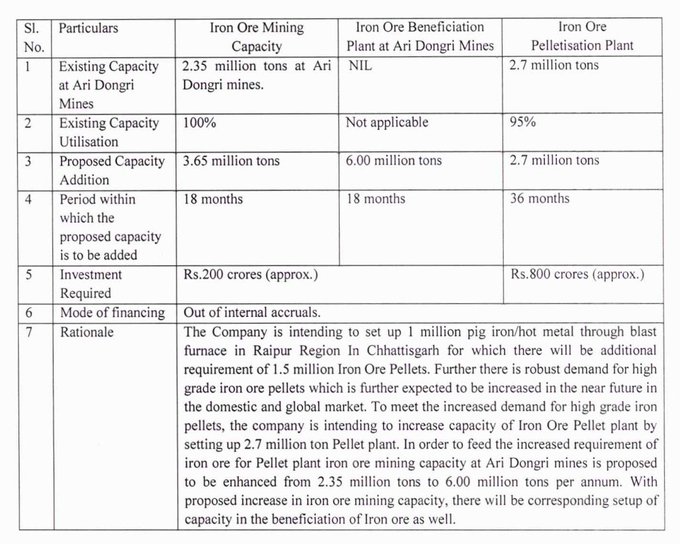

source of this expansion plan… has it been informed to the exchnages

I got to know about it on Twitter. Credible sources like GoIndia stocks etc were writing about it. I could only find this image, I don’t think GPIL has filed the plan to the authorities.

here this note of ours has full details and also the link to the exchange filing Building on competitive advantage...

I tried jumping back in but couldn’t buy much as I’m a gradual buyer, I can’t buy too much at one go. Quite a good qty of my holding is out now ![]() I feel bad about this as I feel GPIL is a good co with great execution…also there was so much of tax incidence for no benefit. This is the problem I’m seeing with several small mid caps. One may sell due to short term issues or overvaluation but after some time good cos make a comeback…it’s not easy to buyback into the stock.

I feel bad about this as I feel GPIL is a good co with great execution…also there was so much of tax incidence for no benefit. This is the problem I’m seeing with several small mid caps. One may sell due to short term issues or overvaluation but after some time good cos make a comeback…it’s not easy to buyback into the stock.

I was worried for few things:

https://twitter.com/Nigel__DSouza/status/1609791776717701121?t=8Dj5Mx7rnTeh6E1gdtvLzw&s=19

![]() Pellet Prices increased to ₹9200-9300/tn vs ₹7500/tn pre export duty removal

Pellet Prices increased to ₹9200-9300/tn vs ₹7500/tn pre export duty removal

![]() ₹1000cr capex will be incurred via internal accruals

₹1000cr capex will be incurred via internal accruals

![]() Selling 90% of production in domestic market, will review this in Feb

Selling 90% of production in domestic market, will review this in Feb

Abhishek was confident with pellet prices sustaining at this level going forward, they will be able to fund the steel plant capex of ₹2000cr through internet actually fully! And in parallel. Pretty strong commentary from GPIL.

A scenario analysis of ROI of 1000Cr CAPEX by - https://twitter.com/fin_odyssey/status/1609873607219609601?s=20&t=t8ZDOIUuc60ScpwMCnoTHQ

Looks like an 18-25% ROI is highly likely with modest assumptions.

@Kumar_manas Sir, do you think those assumptions are reasonable? I am not experienced enough to identify mistakes.