GNA AXLES LIMITED (‘GNA’) is one of the leading manufacturers of automotive transmission components, like rear axle shafts, other shafts, and spindles. The stock got listed in the year 2016.

Sales of the company are consistently increasing- from 400 crores in 2011-12 to 928 crores in 2012-19. Net profit in the duration has increased from 16 crores to 65 crores. With increasing sales operating margin has increased from 13% to 16%. The average ROE for the last seven years has been 14.25% with cyclicity. Even in the automobile slowdown, the company did manage well. However, in December 2019, sales/net profit have decreased. Management expects pain for another 1-2 quarters.

Exports account for almost 55% of the sales/profit. Debt is under control. Interest expense was 8 Crore out of OI of 145 crores. The company is working on almost 80% of the capacity utilization. Capacity is being enhanced. Capital work in progress amounts to around 245 Crores. 2019 marked entry into LCV/SUV segment.

Management is not known. Management remuneration looks a bit on the higher side. However lately management shareholding has gone up a bit. A small percentage [12%] of management shares is also pledged. Trade receivable has gone up to almost 30% of annual sales, however, most of the receivables are of less than 6 months.

Five mutual funds, including HDFC and Sundaram, holds around 9% of shares.

Investment Theme:

(i) The stock look undervalued at trailing p/e of 7, around 0.6 price to sales.

(ii) Past performance inspire confidence in future.

(iii) As capacity is being enhanced, sales and profit are likely to go up once the auto cycle turns.

(iv) The stock, if not a value trap, deserves rerating to a better PE of around 12.

Posting for the first time in this amazing forum. Kindly accept my apology if I break any rules related to posting.

I have come across GNA Axles while researching on automotive and related industries (the only industry currently under my circle of competence). As many have pointed out earlier in this forum, GNA seems to be doing something different than the industry as a whole. The numbers seem to indicate it too…higher operating and net margins than the industry average, more export oriented sales (which gives a higher margin than the domestic sales), healthy enough balance sheet to weather this Covid induced storm in the industry.

Even for the June 2020 quarter, the company had a slight operating profit when others in the industry (even its client, Automotive Axles) suffered operating losses. The company might also benefit through the government’s push for exports.

The company seems to be beaten down due to its link to the CV industry, which is facing its toughest times. Though the company does serve the HCV/Bus industry, 70% of its domestic income comes from the tractor industry, which is doing considerably well.

I notice that this forum section for GNA is not active recently. I am wondering if this is because of the downturn in the industry or have the experienced people here realised that the company is a value trap. I am hoping its not the latter.

Is anyone tracking the company? Q2 numbers look decent and this company seems to have weathered the auto crisis during 2019 much better than other auto companies. Valuation is attractive as well.

There are a lot of parallels between GNA and RACL Geartech. Both have a play in the export tractor market and have sticky clients. Similar valuations on Price to Sales basis and similar margins. RACL seems to be picking up momentum of late, but action on GNA seems absent.

Results look great. Considering SUV segment also to start showing results from FY22, seems the company is on a good trajectory.

Just a caveat, Q3FY20 sales were low, hence y-o-y numbers look optically higher. However, company’s best ever sales were INR 258 Cr and current sales of INR 276 Cr is a growth of 7% augurs well for the future.

This is a very high quality company in my opinion. The CV up cycle (if it happens) will probably re-rate this from 10x PE to 16-20x PE. Meaning price can go to 650-800 in a best case scenario.

See limited downside from CMP given the strong results and demonstrated quality management.

Management commentary on Q3 numbers and Q4 expectations. On the same day 14th Jan promoter released 3.5 Lakh pledge shares out of total 14 Lakh shares pledged. Positive for company.

The release of the pledged shares is positive news indeed. I guess the promoters have used the sudden massive surge in share price to their advantage since the price might come down again.

One thing I have noticed in the commentary given to ET Now and CNBC is that the management seems worried about the rising raw material prices eating into the margins. In the CNBC interview, Mr. Kulveen also hinted that the company might not be able to pass on the rising costs to the customers. Hopefully the income manages to keep up.

Further release of 5.5 Lakh pledged shares on 12th Feb by promoter reported to exchange. Total pledged shares came down now from 14 Lakh to only 5 Lakh.

Exceptional Q1 numbers by company. 6.5 cr loss to 29.4cr profit.

Lifetime high revenue(breaking previous qtr record). Margin improved both QoQ and YoY.

No such 2nd wave lockdown effect.

Promoter releasing pledge gradually.

Majority Export business playing it’s role.

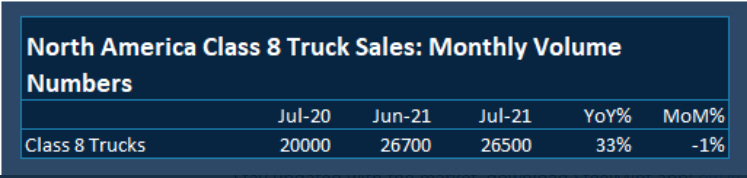

North America class 8 truck demand in upwards trend.

Multi year CV cycle in upward trend.

Favourable tailwinds.

The numbers are good as expected.

However, I am particularly interested in the status for the SUV axles. The management has been quite silent about this over the past year. Let’s see if the management provides a status this time.

GNA has seen a massive rally handily beating even the bull run that thr market has had since start of the year.

This quarters results were mixed with revenue about flat qoq (50%increase yoy) and margins under pressure.

I wanted to understand the long term prospects of this company.

Seems like the majority of the revenue comes from class 8 trucks, tractors and commercial vehicles but how sustainable is that?

The move into SUV vehicles is encouraging given higher margins and another revenue stream but no numbers around that shared so far.

Finally what would be the impact of EVs on this business?

Revenue Cagr over last 5 years is around 19% but since growth is heavily dependent on infrastructure based vehicles how much growth can we expect?

Can we assume around GDP level growth- say around 6% a year which leads to just about 5% cagr over the next 5 years or are there some major tailwinds to assume a higher revenue growth rate.

Also is margin pressure a worrisome things or is it more of a short term effect and we can see increase given its leading market position?

At about 1500cr by 2026, at 8% net margin and even taking a 20 pe we’re looking at a 2400 cr market cap, which is just about a 30% increase compared to today.

Thank you.

Discl:

Holding with avg price of 250 and thinking about selling a little.

Greater than 20% of portfolio

PE of 25 for a semi-cyclical industry might be aggressive. 15-20 would be realistic, even then there is significant room for upside from current levels. If we know management’s Capex plan and view on SUV business contribution, then there could be further valuation upside.

Can you share source where management has indicated 30% growth for next 2-3 years?

They had said 30% growth for FY22 which brings FY22 rev to about 1200 cr and they are on track for that (slightly more)

Post FY22, I am assuming mid to high single digit growth for the next 2-3 years and that’s how I’m arriving at about 1600cr by fy25.

Hope it exceeds that but unless the SUV business really starts firing or the class8 truck demand remains very robust, will be tough to get even 8-10% growth annually I think.

The Q2 results were not as bad as the beating taken down by the stock. With recent correction the valuations are again getting attracted. Does anyone knows if the impact on margins is due to RM price as steel being the major RM and company can pass on the price hikes with a lag so hopefully in next quarter margins should improve. This along with US senate passing down infra bill could help in improving demand for class 8 trucks.

Disc : Invested earlier but sold off at higher levels around 1100. Now bought a tracking position again

10% dip in sales in Q3 and Q4 were highlighted by management in the interview before the results as well. Interview.

He had given the various reasons for dip in sales in North America - semiconductor shortage, driver shortage, metal price increase, inflation overall. But even with this management had maintained the guidance of 35-38% growth in sales which they are still maintaining and PAT growth of 30%.

I have found management to be quite honest about the numbers over last 5 years and still PAT has grown from around 30cr in 2016 when they did IPO to 95+cr today. Sales have also more than doubled.

So, I wonder why market is not willing to give more than 15-16PE to this company? Is market concerned about the viability of this business in future? Wanted the opinion of fellow members on this company. @ayushmit - Would highly appreciate if you could share your thought process here since you have been following this company since few years as well.