Not the right time to get into gna axel, fundamental detriorating and stock was pumped up. Current US policies on auto are coming under question mark, local growth in commercial may halt for a year due to uocoming elections, dont like this loan taken by GNA and capex anything goes wrong this might plummet heavily. Stay away as of now.

1 Like

CRISIL has withdrawn ratings on GNA Axles citing non cooperation by the company.

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/GNA_Axles_Limited_November_05_2018_RR.html

The company is also rated by CARE Ratings…maybe the company wants to continue their rating with one rating agency

Press Release by CARE

1 Like

Ya that’s what I thought. But at least they can respond that they don’t want the engagement to continue. Similar unresponsiveness to minority shareholders questions as well.

After IL&FS and DHFL rating case,difficult to trust these rating agencies,who is saying the truth.

My understanding- GNA is into the manufacturing of axle shafts, which are one of the components for rear axles.

Meritor or Automotive Axles are into the manufacturing of the whole axle assembly; They might be outsourcing the axle shaft.

1 Like

Class 8 trucks sales remain healthy.

I think the concerns around GNA are more geared towards a slowing domestic CV market with all major OEMs making new 52 week lows.

However, promoters seem to be unconcerned:

1 Like

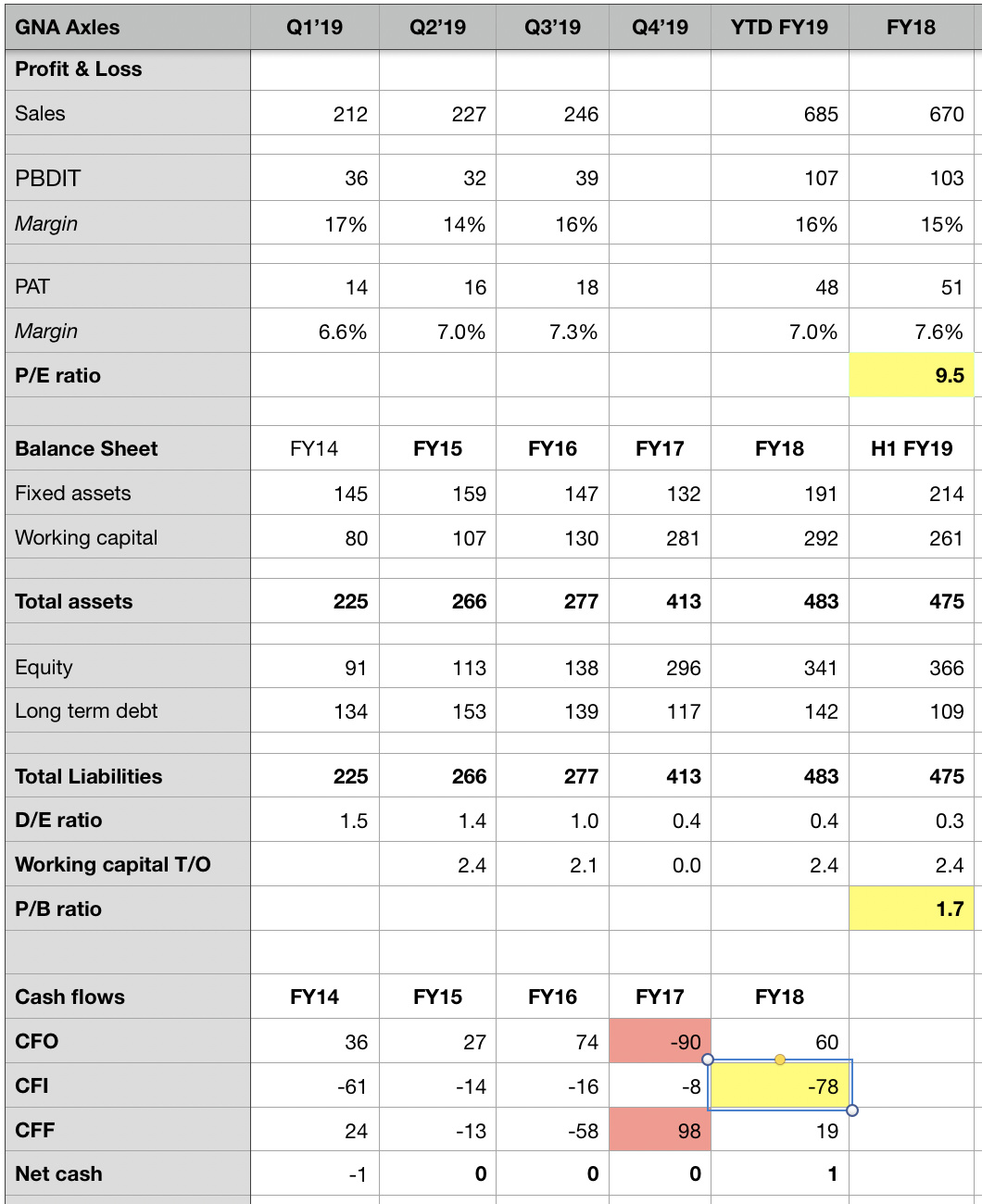

As I mentioned in one of my previous posts, I like GNA’s P&L which seems to be growing very well. Despite being a low margin commodity like business with poor bargaining power with buyers [big OEMs, long standing relationships], GNA seems to be holding its EBITDA margin at 15% roughly)

But I have a problem with the company’s high receivables and poor cash flow generation.

Valuation wise the stock might be at a very comfortable level (PE of 9.5 and P/B of 1.7 based on extrapolated 2019 full year earnings and Book value as of FY18 both standalone). But this being a small cap, we cannot deny the possibility of corporate fraud at any point particularly given that large caps like Sun Pharma and others have been found to be engaging in poor corporate governance practices.

GNA had 235 crores of receivables as of FY18. And looking at the cash flow statement of 2018, there are 125 crores of receivables in just one year and that too in the year of the IPO in which they received 130 crores some of which they used to pay down debt.

Now I understand a growing business has a high appetite for re-investment and their asset base is growing in tandem with growing sales. They have already undertaken Capex in the last 2 years consistently expanding capacity from 3.5M to 5M units per annum so all that is fine.

Combined with this, the debt/equity ratio is coming down as well and their working capital turnover ratio is pretty much consistent at 2.4 (refer table).

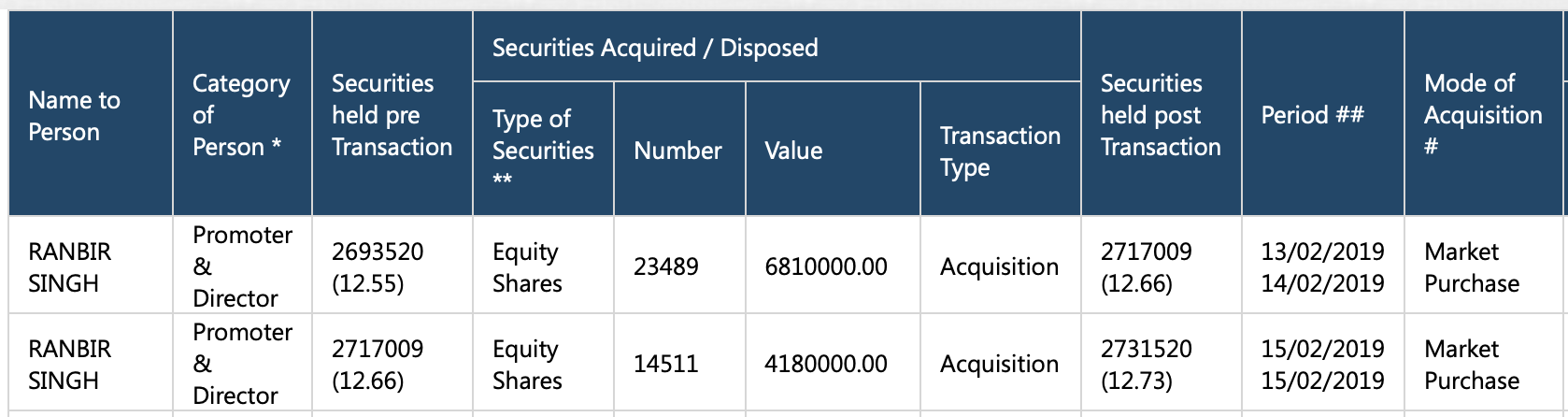

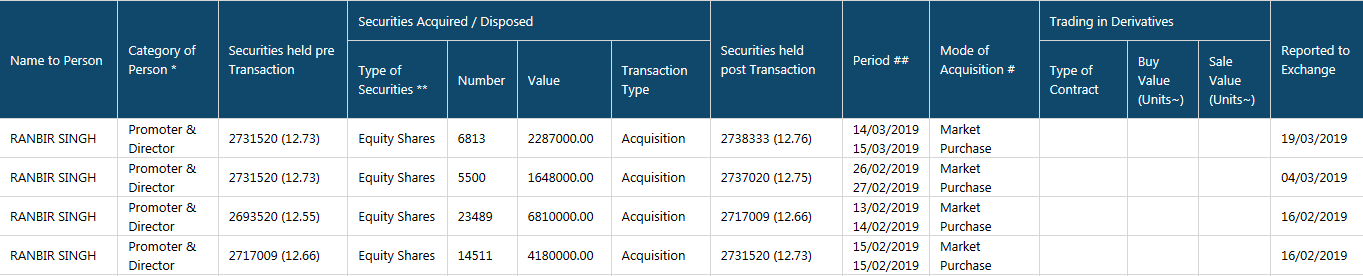

Also, the promoter is buying at current levels (refer previous post).

I would request experienced boarders here to comment on the stock and share their insights if they follow this story. @hitesh2710 @vivek_mashrani @dd1474 @bheeshma @basumallick @phreakv6 @aveekmitra @Yogesh_s

Disc: Invested but not looking to add before I get some comfort around their high receivables.

Hi @AKGupta,

Apologies, but not following the co. However, the co seems to be well managed with good cash flows. The high receivables are offset by the high payables. Even so, the cash cycle of the compnay has increased quite a bit from 22 days in 2015 to 83 days in 2018 which should explain the low PE its available at. Some more work probably needs to be done to understanding whether exisiting cash flows along with judicious borrowing will be sufficient to cover both capital investment and working capital needs.

Best

Bheeshma

1 Like

Full year results announced :

Topline growth at 36% from ₹680 crore to ₹928 crore in FY19 (They were targeting topline of ₹1000 crores by FY20. Seems the company will be there a bit early)

Net Profit at ₹66 crores in FY19 vs ₹51 crores in FY18 (growth of 30%). Net profit margin at 7% same as last year.

Net worth at ₹400 crore (Mcap of ₹580 crores).

Working capital at ₹200 crore (Receivables at 312 crores; inventories at 160 crores)

Inventory turnover ratio : 6X

Debt at 73 crores (D/E ratio : 0.18)

Interest cost ₹8 crores (Interest coverage @ 7.5)

Dividend at 2.75/share vs 2/share last year

Discl. : invested

2 Likes

I gave a presentation on GNA Axles at ValuePickr - Chintan Baithak 2019 - #31 by pratyushmittal.

GNA Axles (VP).pdf (841.2 KB)

Notes from presentation:

- GNA Axles manufactures rear-axle shafts. While passenger vehicles are back-wheel driven, the commercial vehicles (CV) are front-wheel driven. In commercial vehicles the rear-wheels are responsible for torque. GNA specialises in these rear-axle shafts.

- Tractor rear-axles are the bulk of GNA’s sales.

- Automotive Axles is a customer of GNA. GNA only provides the shafts which are then bundled together with the housing, spindles and other parts together forming the complete axle.

- GNA is also putting up a capacity for SUVs since they are also front-wheel driven.

- The company mentions that 100% of its customers have been with the company for over 15 years. The clientele is impressive.

- From the Red Herring Prospectus (RHP), we see that company keeps adding a new customer in form of new plants to supply. For example, though the company might be supplying to Dara from before, they started supplying to their Brazil plant in 2014-15 and their Australia plant in 2015-16. This might be a driver for growth.

- Company came up with an IPO in 2016 @240 and raised 120 Crores.

- Company has increased the capacities consistently over last 3 years.

- Company seems to be doing very well even for the last 2 quarters when the whole CV industry is facing headwinds.

- Management seems positive about maintaining 10-15% growth in 2019-20. They mention in the Bloomberg Interview that a lot of business is shifting to India from Europe to cut costs. This is providing not just the industry growth but also the increasing market share.

RISKS

- Commercial Vehicle industry has been very volatile and cyclical over the years. It is largely dependent on the customers and margins can be under pressure sometimes.

- Auto ancillary businesses are not very scalable as they can’t broaden their product basket easily. Their addressable market is constraint.

- Company has a couple of unlisted group companies with decent size. They seem to be into gears. The company mentions that it has a common marketing team which is beneficial (from credit rating report).

- There are uncertainties around BS-VI rollout as many believe that there can a slump for a year after the roll-out due to increase in the prices of commercial vehicles.

Most of the work done by me has been from collection of comments from various interviews. I believe this is an interesting company to track as it has been doing well when others are lagging.

25 Likes

Management interview with BQ on good Q1 results:

1.Growth contribution from North American market. Our customers have grown …first preference for us in their new business.

2. Margins improvement by cost control,better manufacturing & exports with better margins.

3. Order book is full till December.

4. Tractor segment reached peak last year…don’t see much growth in tractor segment

5. European market is flat: 3 -4% growth.

6. Domestic market not doing much.

7. Growth guidance for FY: 8-10%. will maintain 15.5% margins

Discl: not invested.

4 Likes

If anyone attending the AGM next week, request you to question the management on following:

- Inventory days and receivable days have been very high since long time. Why are these so high? Is there any scope for decreasing these in the coming years?

- How confident are you of retaining market share in the next five years? What is your competitive advantage?

- Do you see new players emerging or getting stronger in the coming years? Are there are any entry barriers in the industry?

Some questions which may not be very appropriate to ask the management directly but worth digging are:

- Why is this company having such high market share?

Looking at the product, it seems to be a simple mechanical product which one shouldn’t find very difficult to manufacture. - Similarly, why are exports so high for this company? Not many auto ancillaries have achieved this feat. This company is definitely doing something special. Good to understand what that is.

Discl: No holdings. Just started tracking. Not a buy / sell recommendation

6 Likes

Results are out - https://www.bseindia.com/xml-data/corpfiling/AttachLive/b3875756-3a3b-4694-b6c9-37863c351f55.pdf

QoQ Revenue up by ~12%

Profit before tax is flat

PAT increased by ~37%

EPS 10.38 vs 7.57.

Margins has got hit but due to reduced tax rate, company has made good profit.

Excellent results during the auto down cycle.

Automotive axle’s revenue has come down by 50% and profit is down by multifold. It would be interesting to know how GNA able to manage in this tough environment. Appreciate if someone could share more on this.

1 Like

Class 8 truck sales picking up in US again,and half of GNA Axle business is export oriented. In comparison to Automotive axle which is being treated rival company, this number from GNA is remarkable. Government is boosting export to improve economy. We can see some major traction in share price which we can see for past few days before result announcememt.

3 Likes

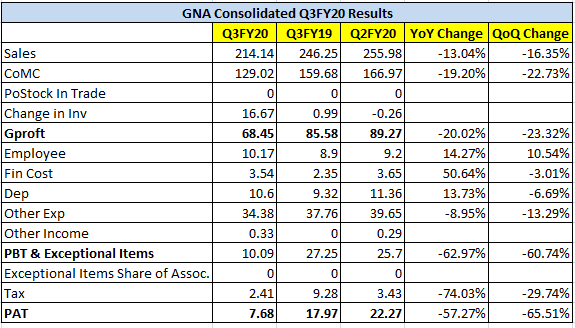

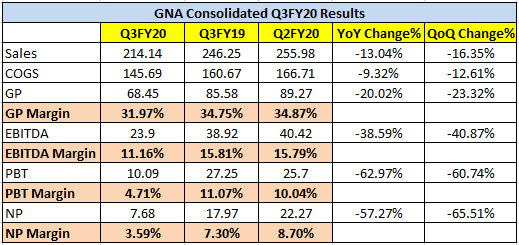

Q3 results are out - https://www.bseindia.com/xml-data/corpfiling/AttachLive/36b89ce4-7e93-406e-b83a-159b236b51c4.pdf

YoY Revenue down by ~12.9%

YoY Net Profit down by ~57.5%

One of the reason is the increase in raw materials cost which has hit the margins along with inc in employee welfare cost and depreciation. In 2018 Q3, raw material was 65% of revenue and now in 2019 Q3 it is at 68%.

1 Like

@sivaramtvl has already provided highlights of Q3 but sharing details for broader view of quarterly numbers. Higher fixed cost impacting EBITDA because of decline in topline. Gross margins impacted because of higher COGS.

Not surprised by soft numbers. Management had already guided for softer numbers for rest of the financial year, during Q1 results tv interview.

3 Likes