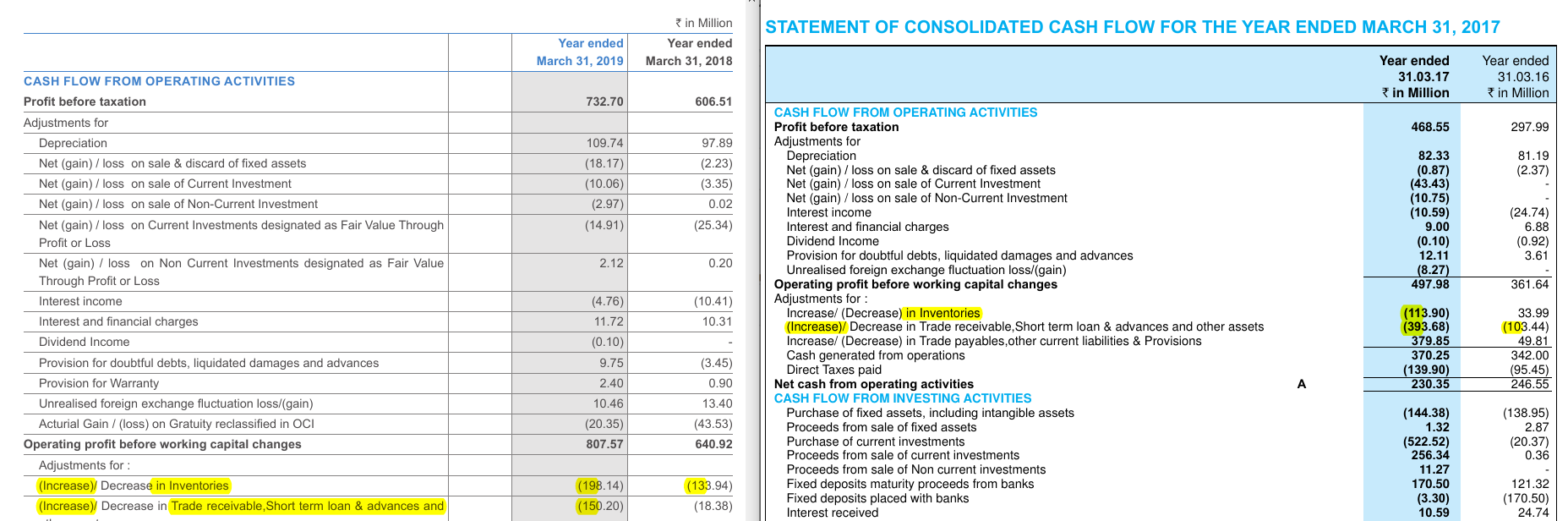

Operating Profit/CFO(Cash Flow from operations) ratio of more than 60% is considered good. Above 80% , it is excellent. I have tried to check it for a long period of time(FY08-FY19) for GMM Pfaudler and I found it to be 77%, which is good. Here are the details:

3 Likes

I do not see any malice in CFO’s explanation. Initially, he erred but the BOSS provided the clue and post that he was spot on. As per AR’s, WC has ballooned and business has indeed consumed additional capital of 40+Cr in Inventory and 66+ Cr. in ARs. I think the interested investor should focus upon the rationality of an increase in % of WC (both Inventory and AR) w.r.t sales growth during this duration.

Here are the numbers, highlighted in yellow, for ready reference:

Disclosure: No Investment. Spending time with financial statements of various businesses and could not resist to look at this seeing the tone of the discussion.

2 Likes

What’s likable in this business?

- 75% Promoter Holding

- No Borrowings

- Cash rich

- Improving NPM and hence ROE over the years.

- 20% compounded Sales growth over last 3 yrs

- Improving Cash Conversion Cycle

- 15% of the balance sheet is funded by advance from the customer

- Reputed Auditor

What’s not so likable?

- Ballooning WC which is required for a growing business but does carry a higher risk

- Valuations as of the date

5 Likes

How can a company with 1 year of advance orders have increasing inventory?

One of the things to look at while analyzing operating cash flows of a company beyond payables, receivables and inventory is to look at customer advances under current liabilities. As a bonus looking into this figure can also be used as a proxy for order book.

8 Likes

I am sorry I dont see much value of these charts. A table + excel which could capture this data would have been more helpful.

5 Likes

GMM entered into binding term sheet to acquire De Dietrich ltd at Hyderabad.

De Dietrich is primarily manufacturer of Glass lined equipment.(France based company whose India business was doing well)

cost of acquisition: 6.25 million Euros.

Capacity of De Dietrich seems to around 600 eq units per year( not precise information from channel checks)

This should help GMM to reduce the delivery time of equipment’s to customers around Hyderabad.

With new furnaces Gujarat capacity will be around 2800 units, greenfield capacity at Hyderabad:500 units( may take 1-2 years)+ De Dietrich capacity of around ?600 units.

8 Likes

Q1 FY 21 Concall was today. I couldn’t attend due to sudden engagements. If somebody can help with highlights?

You can listen to the con call here

4 Likes

GMM Pfaudler - 1Q21 con call updates:

Points related acquisition:

Completed acquisition of De Dietrich Process Systems India (DDPSI) in Hyderabad, likely handed on 1st of September; this gives GMM a ready-made the glass line capacity in Hyderabad. It will improve presence in the region and help serve customers in a much quicker and prompter manner. Also, transportation cost will be lower.

Necessary steps are being taken to start production from 1st September 2020 itself.

This new facility will help to reduce the current backlog of Gujarat facility; backlog will reduce by about 200 to 300 units. This facility being closer to South India Customers, they can now supply equipment faster to their customers.

Expected capacity is around 400 equivalent units from Hyderabad facility in the first full year of business.

Full year of production can generate revenue anywhere in between 60 to 70 cr. from new facility. I believe this guidance seems achievable (400* per unit realization of INR 16 lakhs comes to ~64cr.)

And additional ramp up through operational efficiencies can be expected in the coming years. DDPSI processes, firing cycles for glassline were very different from GMM’s processes, so operations can help improving output after couple of years.

Additionally, this new facility has scope of additional capacity expansion (probably brownfield expansion plan). There is space available for new furnace which can help to ramp up production. (But no quantifiable number of time guidelines on the same)

Now that they acquired this facility and have ready-made access they will no longer make any investment in the greenfield project which was earlier talked about in Hyderabad for 500 EU.

Additional CAPEX requirement on this new facility is less, around 8-10cr that too spread across next 3 years.(Mostly new small equipments, small cranes, painting work)

Cost structure in Hyderabad will be significantly lower than that in the Gujarat facility.

Order Backlog:

At the end of 1Q21 order backlog was of 330 cr. 50% for GLE and 50% for Non GLE (HE and Proprietary Products).

Points related to Glass Line Equipments:

Two new natural gas furnaces have arrived on Indian shores, and should be operational in next couple of months. This is help to cater to GLE demand to maintain their market leadership.

Capacity in FY21:

- Gujarat: 2300 EU (I believe from next year this should increase by 300-400 EU considering new furnaces will be functional for full next year.)

- Hyderabad: 200 EU (400/2 considering only half year will be available for production)

No new orders from parent company in GLE segment as their focus is on booming Indian market.

Company received two very large orders for glassline equipment from Taiwan and from Malaysia this will be the range of maybe 10-15 cr. (Exports of GLE can be next growth trigger).

For GLE, equipment size in pharmaceutical is much smaller than equipment size in chemical and order value size could be significantly higher for chemical clients.

DDPSI was a major player which has left India, so there is a vacuum that’s going to be created. Market share for that is up for grabs. Since DDPSI were a technology leader it’s very difficult for a value player or a low quality player to take that market share. So that market share will automatically be catered by GMM.

Points related to Heavy Engineering (HE) Segment

Heavy engineering business has done extremely well. This is the first year that they have started the year with a very strong backlog in this segment which means that this is the first year that heavy engineering business will be performed up to the expectations that management expects from it.

For HE segment, Work in Progress created in 1Q will help to much better in the remaining quarters for the year on YoY basis.

Margin Improved for HE segment, as they hit significant volumes. so the absorption in terms of the fixed cost will finally come through and that will affect the profitability positively. Last whole year the topline in heavy engineering were close to 50cr but in 1Q they already recorded 41cr. So immediately one can see a big improvement in profitability.

Margins were also supported by good product mix (exports to Middle East, equipment related to carbon steel, stainless steel, etc). With right product mix company expects 150 to 200cr for a full year. They hope to pick and choose good margin business to support their revenue growth going forward.

No capacity expansion plans for the company in this segment in the near future.

In this segment they are diversifying from their legacy industries of speciality chemicals and pharma to oil and gas, petrochemical, etc.

On Proprietary Products

A very strong order book. Product mix is not of standard equipments. They have managed to really up sell this equipment and really go after technology and innovative products really trying to differentiate ourselves from our competitors

Orders are of good quality and high margins. Focus has shifted to high margin business to differentiate themselves from competitor’s standard products.

Lot of traction is seen for a recently launched a product called the spherical dryer. These are very high value high cost dryers but really show a significant improvement for the customer. Spherical dryer helps drying time of close to 36 hours to reduce by 50%.

On Subsidiary Mavag

Expect them to do extremely well this year both in terms of top and bottom line, supported by better backlogs.

Point related to demand: Traction is seen in pharmaceutical space in smaller players who used to order maybe one or two equipment are now going and ordering six to ten equipment. However, traction is lesser than management expectation for big pharma players. Indian companies looking at localizing production of intermediates along with government pressurizing Indian companies to look at manufacturing locally will lead to structural shift from China to India.

Government has also identified three clusters for intermediate and pharma manufacturing one of them like you know is pharma city in Hyderabad. Pharma city is still maybe a year and a half two years away maybe even more but now the government will definitely push to move that a little bit faster.

Replacement demand:

Pharma plants especially the older ones in Hyderabad have now reached their life cycle people are looking at upgrading these plans now with FDA issues coming in people are looking at revamping many of these plans so not only demand from new investment but even demand from replacement business will pick up in the coming quarters.

7 Likes

7 Likes

The last few posts have been adding little value to the discussion. Main crux of the posts is to discuss the price moves and whether it will sustain or not which is not adding any value to the thread. Please avoid such posts as it is making the job of moderators difficult. While posting we feel that it is not adding any value to the thread, please avoid posting.

15 Likes

Execution of definitive agreements to acquire a majority stake by GMM Indian co, in the global business of the Pfaudler Group.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=270485da-1491-4d1f-bc0c-a7365091ecd5

1 Like

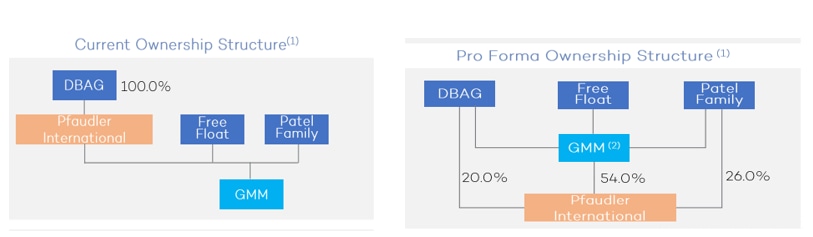

My two cents on this shares acquisition. Might be completely wrong in my assumptions but prima facie this is all i could understand.

The ultimate holding company shareholding after transaction would be 20% as

which means 30% of company’s shares would be transferred to GMM Pfaudler and Management will increase their stake from 24.56 to 26%.The cost of these 30% shares is

So, it menas 30% of company shares are worth 205 Cr.

which indirectly means 100% of the company’s shares are worth 205/30*100 = 685 Cr.

the current market cap of the company is 8704 Cr. which is around 12.6 times of the acquisition cost.

Means if the company would have considered minority shareholders at par and purchased/transferred the shares at market value they would have to pay 12 times more the current cost.

Comments welcome!

Regards

Sunny

3 Likes

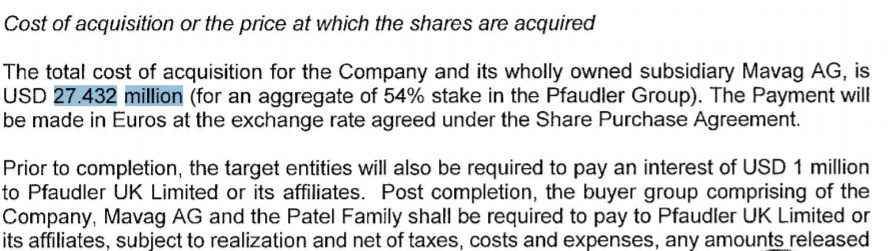

54% stake for 27.432 million

34.4% will be acquired by gmm and 19.6% via mavag( subsidiary of gmm )

Mavag is wholly owned by gmm

So you can say 54% acquisition for 27.432 million.

Interesting management interview

2 Likes

GMM Pfaudler offer for sale at 3500/- floor price

https://archives.nseindia.com/corporate/GMMPFAUDLR_21092020174345_OFSnoticeGMMPfaudler21092020.pdf

2 Likes

stock is at 105 PE… For an engineering company, it is unheard of… so normalization process will begin sometime sooner rather than later…

2 Likes

Ofs at 3500, does this indicate that the promoters value the share price at 3500 and not at current price.

Also earlier it was mentioned that debt was going to be taken for faudler takeover.

1 Like