Hi Anant if you observe the recent trend - Demand is shifting from large scale stainless steel bioreactors to singe use fully disposable reactors/technologies. Can this affect GMM. Please enlighten Thanks

Nice to hear positive comments during present crisis:

Complete plant shut down for 12 days. Got permission from local authorities as essential service provider to pharma.

50 employees working in GL division . Final equipment is not ready yet due to logistics issue

Waiting for some approval from authorities to slowly ramp up operations

Pharma and chemical industry:

Pharma sector is picking up. Customers are approaching GMM for reactors.

Companies/MNCs to invest in India to reduces dependency on china for RM and intermediates.

Order backlog increased.

Finalised few large orders recently.

To set up another facility at Hyderabad.

Overall bullish on pharma/chemical for next 3yrs

Positive guidance for FY21.

7 Likes

Great post - GMM Pfaudler is already back to 56x p/e post-corona. Once the PMS and MF managers dump this on retailers, expect to see a “bubble in small cap quality” report ![]()

GMM has issued a 5 year plan called UDAAN which talks about reaching 1,300 cr of revenue in FY 25 – 17% CAGR. Assuming they maintain margins and achieve this target, the stock is trading at 26x FY 25e earnings…

5 Likes

2 Likes

I have exited GMM Pfaudler purely because valuations elsewhere were more attractive. I also think in the short term Mavag operations will get disturbed. I still continue to hold the view that GMM continues to have tailwinds and will do extremely well earnings wise in the coming years. As said earlier my exit call was purely driven by valuations.

DIsc.: This is not a buy/sell call. I am not a SEBI registered analyst.

17 Likes

Anant pl answer my question I know you have lot of domain knowledge on this stock. I would like to know whether they will be challenged by disposable bio reactors. I could not understand this bit part of business.

I have a very little understanding of Bio reactors. My limited understanding tells me that the usage are for very different purposes. Do not see much overlap in use cases. Will be happy to be corrected.

4 Likes

A nice detailed analysis of Gmm Pfaudler done in a video

6 Likes

Hi

PFA the results for Q4FY20.

Rgds

5 Likes

The most dangerous combination to invest at this valuation - Highest Earning + Highest PE.

Based on my past experience of investment in such scenario (i.e. NATCO)- when investing in a company in the year of having highest earning (E) and highest P/E - means you are paying too much price for it!! For investors in such company, need to wait longer time for significant return as stock could go in price consolidations !!

12 Likes

the company has a few good qualities

Clean and honest management

the balance sheet is robust and are not involved in sharp practices

the product is of every industry need and is increasing

the market share is increasing and now no 1 in india in it’s niche segment and growing

The margins are high

company is virtually debt free and is growing from internal accruals

a small snippet from screener which is self speaking

Aur kaya chahiye BACHEY KI JAAN LOGE KAYA

Concerns :

Growing inventory ( valuation of inventory is very confusing I don’t understand it fully )

Debtors days are high ( yet that os company has improved but ROKRA to JALDi BAPIS ANNA CHIYEY )

Low inventory turnover - the fixed cost per product goes down if the inventory is replaced faster and same set of machinery can be utilized for creating additional products so there may be some downtime or bottom line may be improved yet with a such a long history of operations company has not improved on it .

disc : not invested observing from sidelines and looking to be in my purchase limits if not came than DUNIYA MAIN AUR Bhi STOCK HAI . This is not any recommendation to buy sell or hold

Regards

6 Likes

All looks good except 1 year stock price CAGR of 199%!! So if you are current investor, enjoy the ride. But for new investor, time to wait for stock price growth to match compounded profit growth…

Disclosure : not invested, in watchlist

3 Likes

I just laugh at the market volatility these days -14% in 5 trading minutes.

My question to you guys since many of you would also have been following HLE Glascoat, as its the biggest & the only competitor to GMM.

What are the things that HLE is doing wrong when compared to GMM, just a pointer to the main issue would be helpful!

1 Like

OPM for the proprietary products(~30% revenue from this) have taken steep fall from 13-15% to < 5%

although heavy Engineering were at loss but that compromises just 7% of revenue.

Anyways the Pharma sector boom is going to be very good for the Glass Line Equipments!

Could someone help me with the valuation of the company as per the quarter trends, I am just a noob, not well versed in valuation hence the help needed?

2 Likes

Q4FY20 concall notes:

Order backlog and guidance: 350Cr of order backlog which is +40%YoY. Order book evenly distributed among GL/proprietary products and heavy eng. FY21 growth guidance of 15% with similar or slightly improved margins. Q1 results may be slightly low.

Covid impact: last 12 days of production in March due to lockdown. Shipments of orders were impacted. Impact on revenue during Q4:30 cr.

April: 15 days of work was impacted. Restarted operations slowly after Govt approvals and following social distancing norms. Labourers/unions are cooperating well. presently 600 people working. GMM has less dependency on migratory workers.

Pharma and chemical industry growth : continue to see significant investment by pharma and chemical companies. GMM is the sole/majority supplier to all well known names in the industry… Capex continues in pharma intermediates and chemicals due to the China issue and many companies looking at India as an alternative.

Many companies are for preponement of supply from GMM.

20 to 30% of plant and equipment cost of new Pharma/chemical company capex is the revenue potential for GMM which includes supply of GL,drying,filtration and other equipment.

Due to the new generation of promoters,change in mindset and FDA issues, most of the pharma and chemical companies are focussing on quality,service of Glass liner equipment rather than cost alone.

Capacity: 2400 units. Two additional furnaces by July capacity will increase to 2800 EU at Gujarat factory.

Focus is to reduce the backlog of orders to 500 EU per month from current level of 1000 EU.

Normal maintenance capex of 20 cr.

New factory at Hyderabad: Capacity of 500 EU. 50Cr investment by internal accruals. 60 to 70 cr of revenue during 1ist year of operation(max up to 100 cr). Hyderabad pharma city is one among three clusters approved by the government to reduce the dependence on China. 20k cr acre of land has been allotted. Actual investment by pharma may take another 2 years to materialise. GMM is in an advanced stage with Telangana govt for land finalisation. New facility will help to serve better the already existing customers and pharma city. It also helps in saving transportation cost.

Heavy eng: good order book(~90cr). Large orders to the middle east were impacted during March.

Mixing soln: 55 cr revenue

Mavag: expect same growth as FY20. Order book of 12M swiss franc. Mavag was not impacted due to covid lockdown except one shipment from GMM.

Udaan strategic plan: No change in target of 1300cr revenue by FY25.

Competition: De-dietrich have stopped accepting orders and decided to exit India.GMM has picked some good people from them. All other competitors have good order backlog but had bit difficulty in restarting their factories compared to GMM.

Exports: 10 to 12% of revenue. Most of the export is from HE . Pfaudler has also shown interest in the GMM HE division. Working with Pfaudler in sharing technology,M&A opportunities and catering to other countries.

Discl: invetsed and done transactions recently.

4 Likes

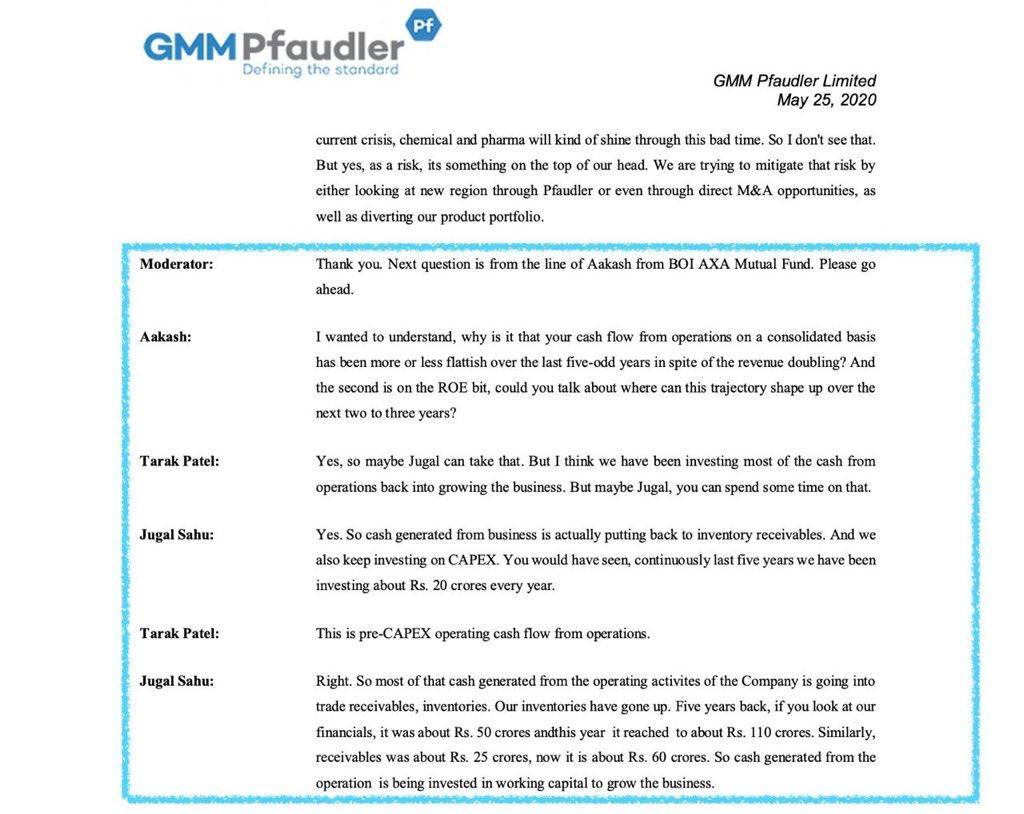

They can’t understand what is definition of cash flow from operations, and what is investing CFO into inventories and recievables…

2 Likes

Or most likely they don’t want to disclose the real answer of where cash is getting deployed… ![]()

4 Likes