About:

- Manufacturing and exporting of Jute & Jute allied products under three essential product classifications- packing textiles (largest), geo textiles, and other lifestyle products such as eco-friendly bags.

- Presently, Gloster’s main buyer is the Government of India that purchases bags to store food grains while the remaining 50% of their sales are to international clients.

- Two manufacturing units are situated at West Bengal - Main Unit (Gloster Limited) and the Ananya unit are in Bauria, Howrah.

- The manufacturing unit was originally set up in the year 1873. The House of Bangurs, one of the leading business conglomerates, acquired Gloster in the year 1954.

- Units/Mills extend across over 175 acres, and employ around 3919 people at the end of FY22, besides employing a considerable contractual workforce.

- Capacity to produce about 50,000 metric tons of finished jute products, annually [137 TPD] .

- Sources the raw jute from cultivation farms across West Bengal, Bihar, and Assam.

Value Chain:

KMP and their Remuneration:

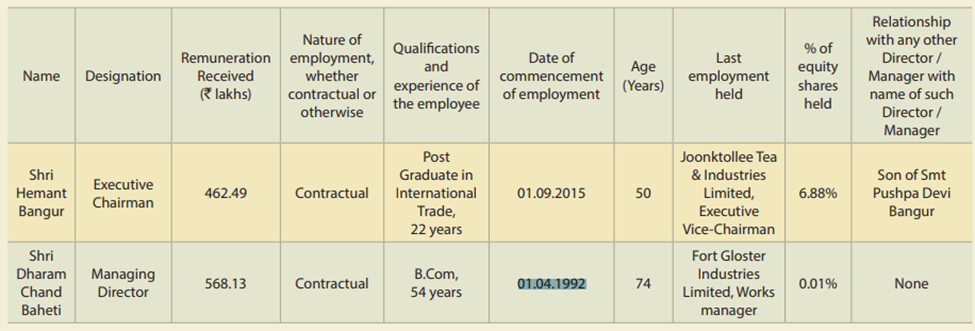

- Hemant Bangur: Chairman. Age 51 Yrs.

- D.C. Baheti: Managing Director, Age 75 Yrs. Leading from 1992.

FY22: Management Remuneration and Salary Hike compared to Other Employees and the Net Profit of the company:

PAT increased by 58%, including exceptional items and 42%, excluding exceptional items

What is interesting?

-

Allocated areas for a residential unit for workers, a fully functional market, two schools and a small clinic to tend to the needs of their employees, which has led to an all-round improvement of worker morale. The present workers are given the opportunity to recommend their wards for the training program. Hence, maintain a steady pool of skilled workers.

-

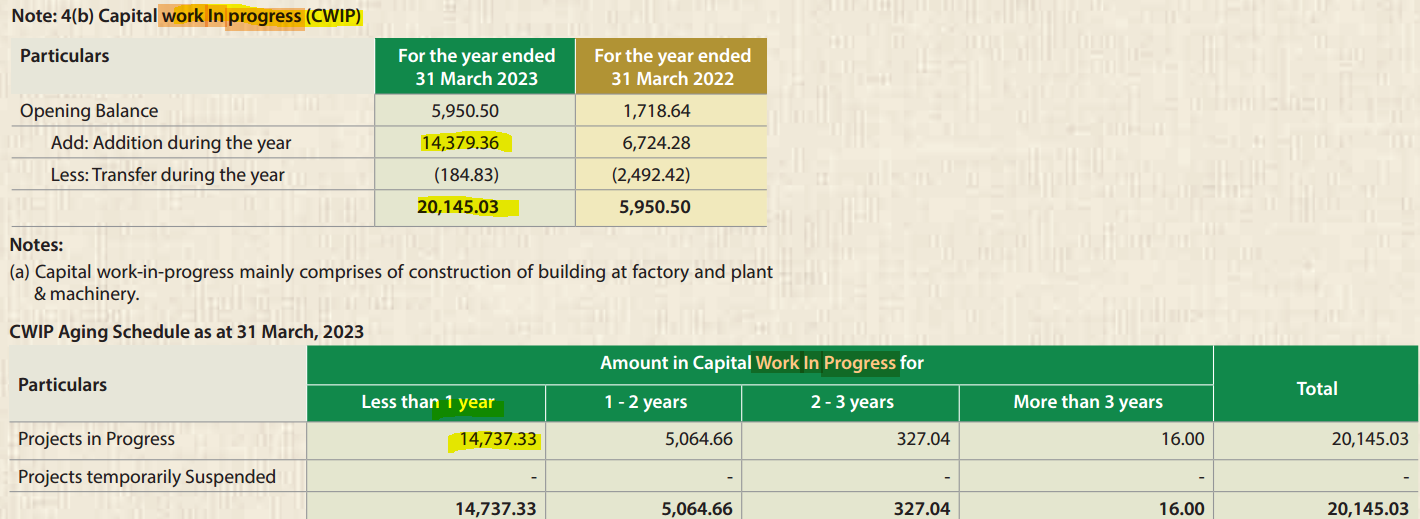

Subsidiary (Gloster Nuvo Limited) setting up a green field jute mill on infrastructure taken from Network Industries Limited (fellow subsidiary) and project work is in progress. Production capacity will almost double - expansion by 130 ton per day, entailing expenditure of around Rs 325 crore. The new capacity will be implemented in phases. Phase I (90 tonne per day) was likely to be operational from end of fiscal 2023 and phase II (40 tonne per day) from end of fiscal 2024.

-

Acquired 2 companies through Corporate Insolvency Resolution Process (CIRP) under Insolvency and Bankruptcy Code (IBC) yet contributing negatively to the PnL beside adding assets on the B/S: The Company was declared as the successful Resolution Applicant by National Company Law Tribunal, Kolkata Bench for 2 Companies under CIRP-

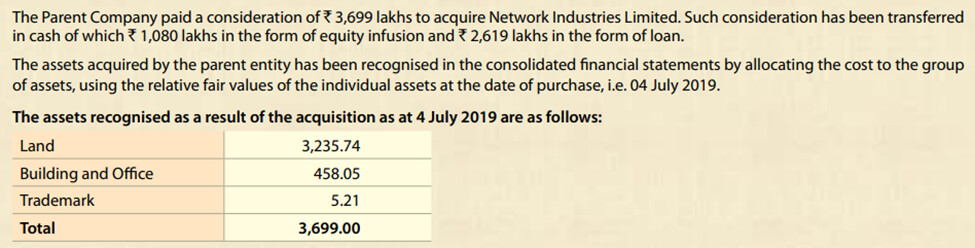

1- Network Industries Ltd:

2- Fort Gloster Industries Ltd: In FY22, steps for revival of existing Cable manufacturing business of the Company. Infused 123.70 crores towards Resolution and revival i.e. 72 crores as Resolution fund and 51.70 crores Fund towards revival of Cable business. In the 1st phase the Company would begin manufacturing of LV Cables and MV Cables at an estimated capacity of 100kms /month and 80 kms / month respectively by March 2023.

-

ROE Expansion Optionality, On the Face Value Vs Hidden Potential:

- Total asset on the BS that are yet to contribute to the PnL: In FY22 subsidiaries, Network Industries Ltd and Fort Gloster Industries Ltd, held up net Assets of 100+ Cr. and had a loss of ~7Cr. Sooner or Later these will contribute to the bottom-line.

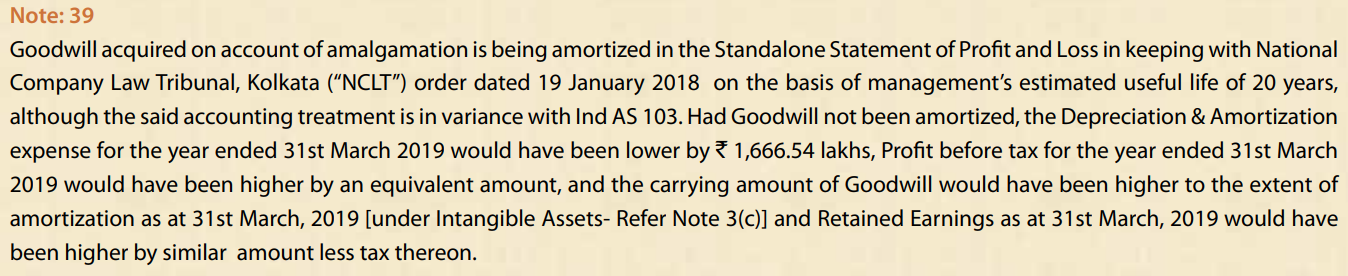

- Every Year consolidated PnL takes a hit of 22Cr. to amortize the Goodwill and Other intangible assets-Trademark, mainly due to its amalgamation with Kettlewell Bullen & Company Limited (KBC). Per schedule, this will continue suppressing the reported profits for another 12~13 Yrs.

- Contribution to PnL after activation of green field jute mill and cables business.

- Inflated Assets on the Balance Sheet (B/S):

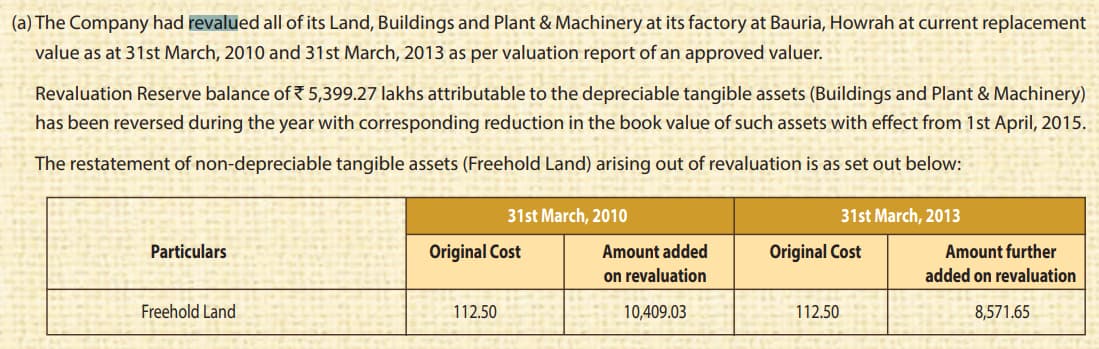

- Land was revalued twice [https://www.bseindia.com/bseplus/AnnualReport/538595/5385950316.pdf]. The same added 190Cr. to the B/S assets.

- Pursuant the scheme of amalgamation resulting in merger of erstwhile GIoster Limited with Kettlewell Bullen & Company Limited, goodwill of 400 Cr. was added to the B/S[https://www.bseindia.com/bseplus/AnnualReport/542351/5423510319.pdf]

:

- Land was revalued twice [https://www.bseindia.com/bseplus/AnnualReport/538595/5385950316.pdf]. The same added 190Cr. to the B/S assets.

Risks:

- Checkered History: https://mnacritique.mergersindia.com/gloster-merger-kettlewell-buellen/

- Capex Delays: Group has untaken to expand its production capacity by 130 ton per day, entailing expenditure of around Rs 325 crore. The project is being funded in debt-to-equity ratio of 3:1. The new capacity will be implemented in phases. Phase I (90 tonne per day) was likely to be operational from end of fiscal 2023 and phase II (40 tonne per day) from end of fiscal 2024. However, due to operational delay in setting up of transmission lines and import of machinery, phase 1 and phase 2 is expected to commission from March 2024 and March 2025 respectively.

- Regulatory risks: The domestic jute industry is highly regulated, especially in key areas such as pricing and sales.

- Easy access to cheaper substitutes: They primarily focus on the packaging industry, where they previously used to sell to local customers including the Government of India for food grain packing. But with the introduction of plastic into the market, several users switched to this cheaper substitute.

- Self Incentive Prevails: In FY20, Remuneration paid to Sri Hemant Bangur, Executive Chairman along with remuneration paid to Sri D.C. Baheti, Managing Director exceeded the limit of 10% of the net profits of the Company as prescribed in section 197 of the Companies Act, 2013. in view of the inadequacy of profits as aforesaid, Approval of Members was sought for the remuneration payable to Hemant Bangur and D.C. for the period 1st April, 2019 to 31st March, 2021 as minimum remuneration, pursuant to Section II of Part II of Schedule V of the Companies Act 2013 as amended from time to time. Reasons of inadequate profits assigned to General business condition and exceptional items.

Sources:

- Company Website [https://www.glosterjute.com/]

- Public Disclosures such as Annual Reports and Credit Rating Reports

- Internet articles such as Gloster and Prashant Westpoint - A successful partnership leading the charge in the jute industry - Future Textile Machines

Disc: Neither invested nor an IRA. Writeup not a recommendation, but shared for collaborative discussion.