I think it’ll further go down.

Disc: Not invested.

I think it’ll further go down.

Disc: Not invested.

Management is very confident about future profitability and growth.

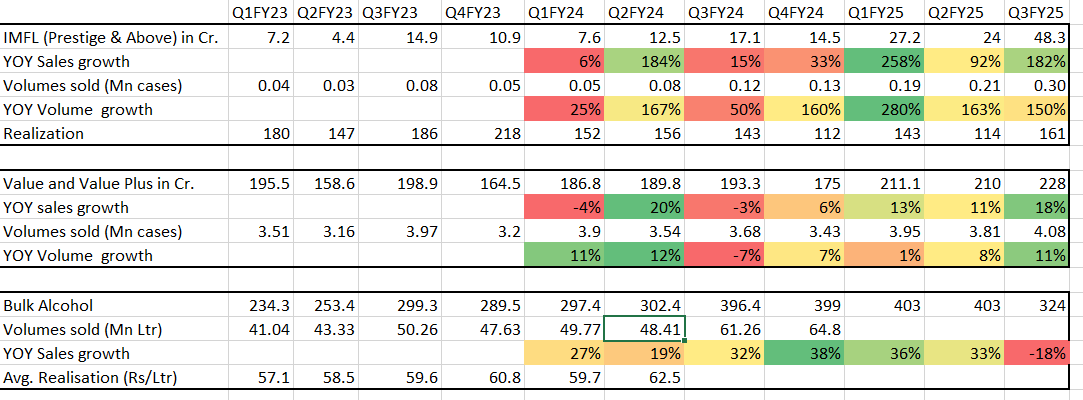

→ Prestige and above segment has shown highest ever growth number of 145% year-on-year and 100% quarter-on-quarter.

→ The management believes that the profitability of the manufacturing business will stabilize in the range of 5 to 7 rupees per liter with additional margins that Ena bring.

→ The government’s pricing of rice through the Food Corporation of India (FCI) will reduce the volatility of raw material prices and stabilize margins. This is because FCI is now a supplier of rice, providing a new source of raw material at fixed prices. This creates a ceiling on raw material prices and a floor on margins.

→ IMFL business segment will breakeven in the coming Quatres and continue to grow in double digit. IMIL will continue to grow in mid single digit. Manufacturing will see a de-grow from ~2027 onwards (and its a good thing as it will bring down the volatility in the margins.)

→ The main growth driver will be prestige and above segment.

→ listen to the concall lot more points, interesting.

WWhiskiesA25-WinnerList-A4-v3.pdf (1.5 MB)

Search by Doaab. Received Bronze in its category.

Globus is coming into low alcohol beverages category and also launching beer so they will complete portfolio of brands and this will help them in being present in most of alcohol categories present in India

For rice you have multiplied by 2.2kg, but for equivalent qty of fuel lesser maize will be required to process is it not?

And, in current pricing terms

FCI is releasing rice at 23, and OMC offtake at 59 (rice) , plus DDGS is 16/kg

Given above pricing GM% remains the same, so can we say that going ahead numbers will revert up.

Notes on Global Spirits

https://www.bseindia.com/xml-data/corpfiling/AttachLive/a13002db-46a1-404c-94b0-1c4174e7576d.pdf Another award for Doaab and Terai at international stage. Long way to go.

Carib in India now. Commercial production started in UP. https://www.bseindia.com/xml-data/corpfiling/AttachLive/1d61659d-8d77-410b-9416-37393a612edc.pdf

Requesting someone to upload the investor presentation here. For overseas persons, Bse and Nse websites are blocked. Thanks in advance.

Globus_Spirit_Q4’25.pdf (3.2 MB)

You can get the investor presentations and concall transcripts from Tijori finance as they are storing the data on amazon aws cloud server