1 Like

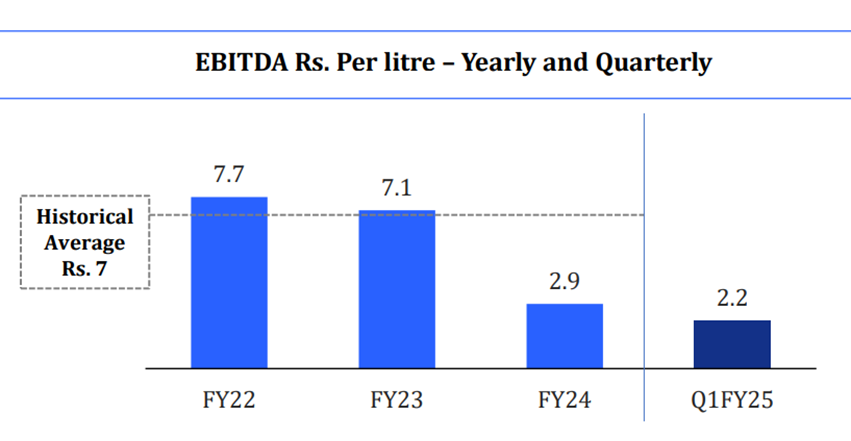

In the Q4 concall, I remeber Globus managemebt saying that margin will improve from Q2 onwards, especially because of Maize vs Rice.

Agree that management’s guidance hasn’t been great. Be it margins or completion of capex. I will like to point out a couple of things wrt margins. Raw materials prices esp rice prices has been the biggest dampener so far. This was the first quarter of increasing margins after a long time.

Rice prices and maize prices would be 2 major factors deciding margins. International rice prices have already started coming down. There may be a disconnect between the indian and International prices. Good monsoon along with increased acreage under paddy cultivation would mean lower prices after Kharif harvest( Oct to Dec). We may see some decrease in food inflation this year.

Discl: Invested and biased

After a lot of quarters of declining margin globus showed an increase in the margin for the first time. Even though, the margin increased only slightly its still good to see positive developments.

The company completed expansion of Jharkand and West Bengal facilities but couldn’t reach the same amount of volume as rice was replaced by Maize. The reduction in volumes is because the amount of maize that can be processed is lower than raize. The company is trying to increase this efficiency and may take a couple of quarters.

The company expects the margin currently to be at lower end and doesn’t expect the margins to go any lower. And expects the margin to trend upwards with the Kharif season harvest (end of Q3).

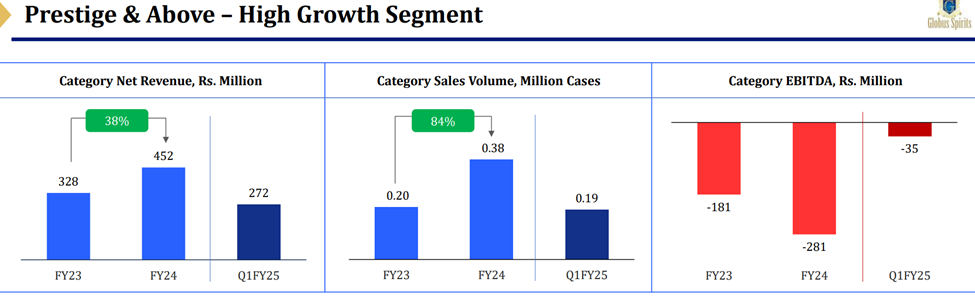

As for the consumer business, Rajasthan remains strong with 29% market share in country liquor and 68% market share in RML with a cumulative share of 35.5%.

Entered UP in the regular and other segments. UP is a very large market in terms of country liquor and for IMFL. As per management good traction to sales in UP.

Bottling unit in UP commenced production. Entire production for state is from the Unit. Started construction of an 80 KL distillery in UP at a capex of 120 crores. Can be run on either grain or molasses. Expected to be completed in 12 to 16 months.

Management expects loss for the P& Above division to be within 15 crores this year. Its launched in 7 states now, no additional state this year. Hoping for 2 out of 5 states where P& A was launched initially to break even this year.

Launching new products in the P& A division. Snoski and Mountain Oak was well received. Another Gin seems to be planned.

Not Out was launched in delhi.

Expected launch of Carib beer to be in Q1’26. Production to be outsourced.

Planning to improve byproduct recovery by producing corn oil and biodiesel expected to be completed by end of year.

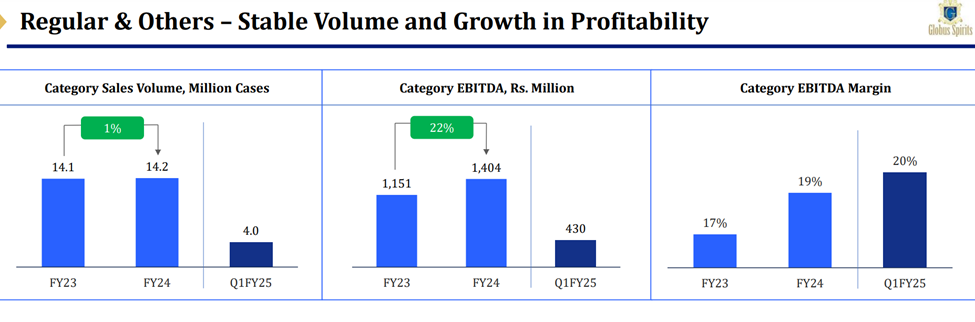

Regular and others

As per management bottling costs reduced by Rs.0.17 per bottle effective August.

Discl: Have purchases in last 30 days. biased

2 Likes

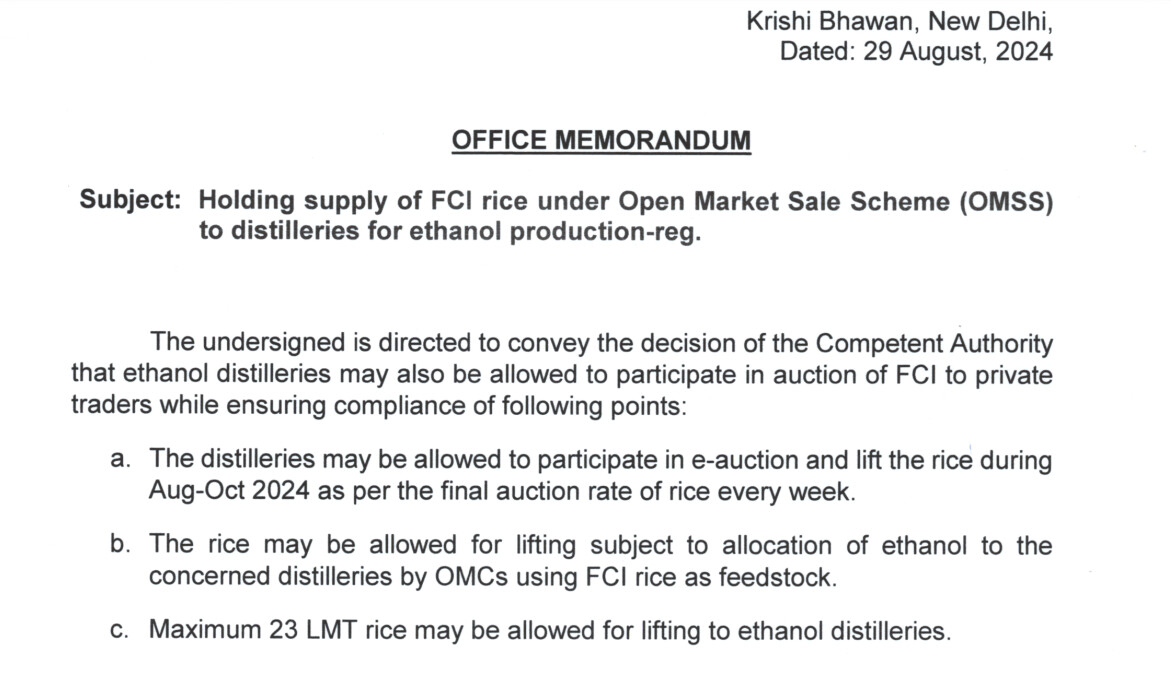

[Reason for yesterday’s jump. ] (https://indianexpress.com/article/india/ethanol-distilleries-can-buy-23-lakh-mt-rice-from-fci-govt-9540644/)

They can shift to rice from maize in a day! (but i dont think they will)

but Gain of around 5/- kg comparing Q1 Pur rate of rice.

Disc: Invested

1 Like

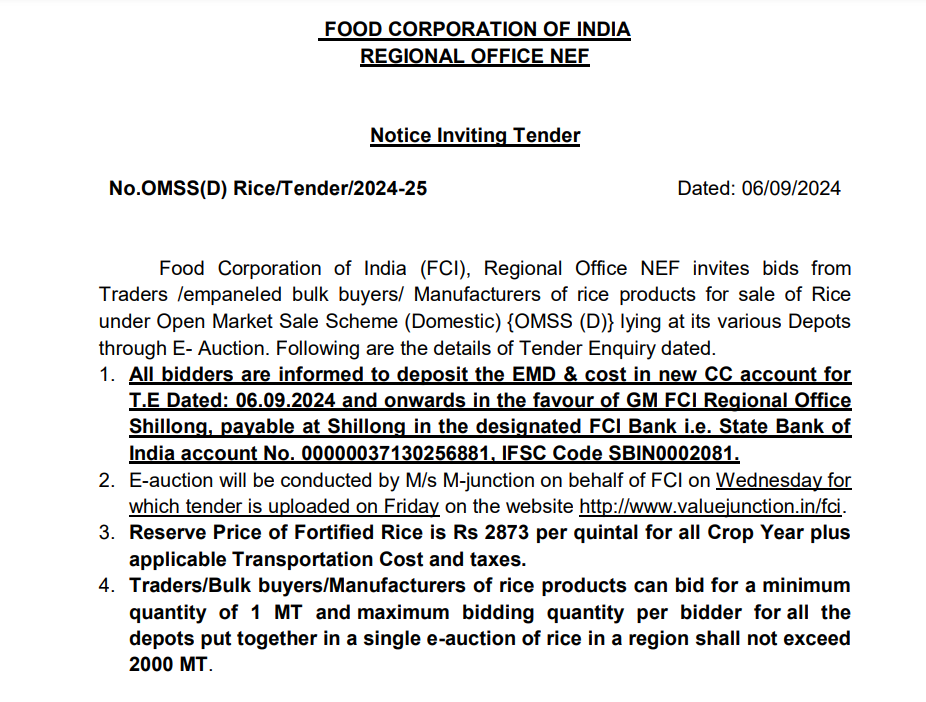

The Food Corporation of India had tightened supply of broken rice which has now been reversed. However earlier FCI was providing broken rice for ethanol @ Rs. 2250 /qtl flat where as now it will be acutioned as per latest circular base price is @ Rs. 2873/ qtl and will have a cap of 23 LMT for ethnol distillers.

News of FCI

New Circular -

My concern is regarding the offtake cap. We need to check with management whether FCI rice will cover the entire raw material requirement or only a part of it.

2 Likes

At this price distilleries are not going to improve margins. I am not sure if distilleries would be even interested in purchasing at this price. If the auction cannot go down the reserve price then I believe no takers for the broken rice at this price. My two cents.

1 Like