Global Vectra Helicorp is India’s largest private helicopter company with a fleet of 29 aircrafts ranging from small light helicopters to medium sized twin engined helicopters seating 4 to 15 passengers. Of the aircrafts 7 are owned and rest are leased. Biggest customer is ONGC which is also a risk in terms of customer concentration. However, the trigger going forward is that the company has bagged a INR 550 cr 3 year contract from ONGC (http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/E6CE1259_6FB9_481D_B77E_F436423F853B_140731.pdf), which is expected to start kicking in from Q1FY18. Sound management with solid corporate governance (KPMG is the auditor which is rare for a small cap). Results for Q4FY17 were also good (http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/239f499d-8ccc-48ea-97b7-a0f4fea06bd9.pdf)

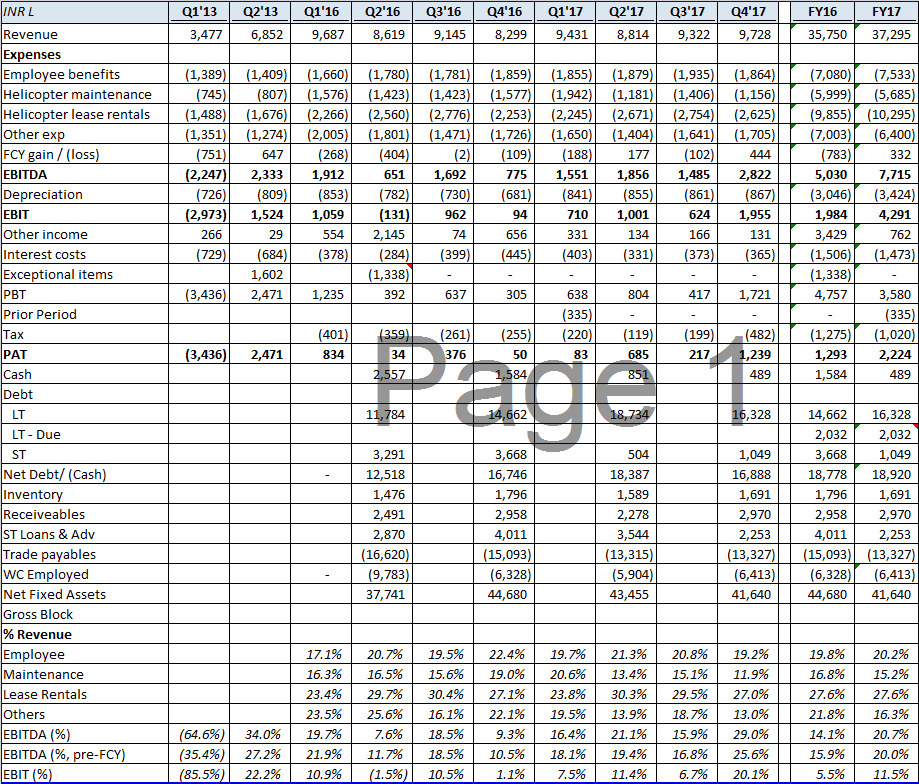

Below are the quarterly financials of the company. There has been a significant EBITDA margin expansion in FY17 over FY16. Despite a low growth this year, most of the costs have been rationalized in FY17 vs FY16. Net Debt levels are almost constant (assuming maturity of LT borrowing same as last year) with improving leverage ratios (Net debt/EBITDA) from 3.7x in FY16 to 2.5x in FY17. Pawan Hans is the biggest competitor, however unlike Pawan Hans, the company has no precedence of air accidents. With the ONGC order kicking in FY18 and with operating leverage, expect a re-rating of the stock in near term.

Disclosure: Invested