Thanks for a very exhaustive write-up. I am sharing some of my insights (which are not already covered in the post). All the figures are taken from the DHRP of Gland Pharma. The DHRP is a very good read to understand industry dynamics of injectable space.

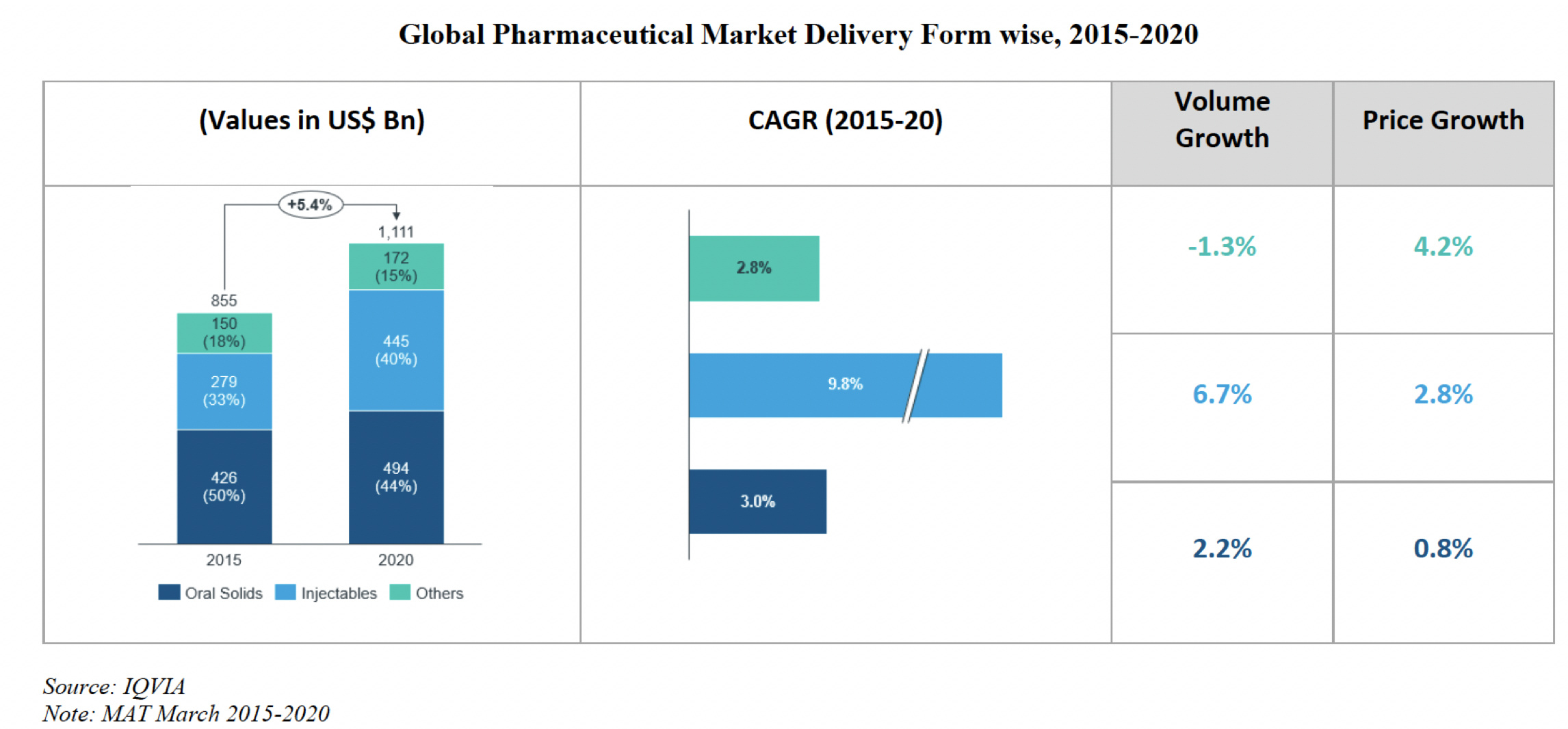

Injectable business growth

Of the major forms of drug delivery method, injectable form has grown at a higher pace in the past 5 years compared to oral solids, mainly due to higher volume growth.

The growth has been strongest in US (both volume and price wise) followed by Europe.

In the previous 5-years, $34bn of injectables have gone off patent and in the next 5 years, $68bn of injectables will go off patent. This is the reason why a lot of Indian generic players are going big in the injectable market. The products currently manufactured by Gland addresses a market size of $8-9bn in US.

On drug shortages for injectables vs non-injectables over the last 5-years, there is no clear trend.

The penetration of generics injectables is lowest in US (at 73%) and the highest level of penetration is in China (at 89%). For context, the current generic penetration for oral solids is about 88% in US. This leaves a large scope for increase in generic injectables (both in terms of market share and market size because of $68bn of injectables going off patent in the next 5 years).