Company

• The Company is engaged in the business of manufacturing semi-finished plastic lenses. They import currently raw material from Eurpoe and USA, earlier they were doing the same from china.

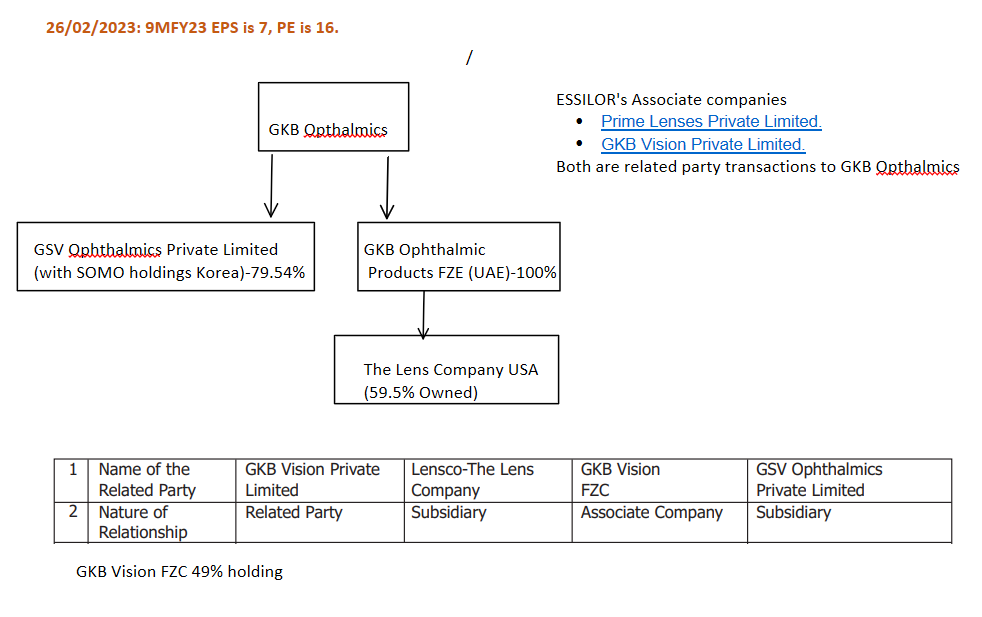

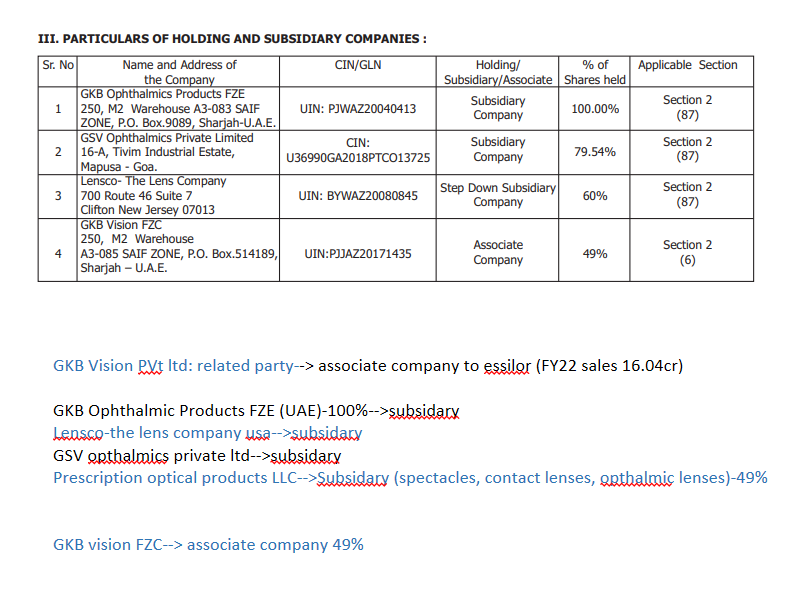

• Prime Lenses Pvt Ltd, GKB Vision Pvt Ltd are run by the two sons of Managing Director Mr. KG Gupta. Key to note here is that these two are associate companies of ESSILOR, which is highly renowned company(similar to specsavers in the UK) for its sales of finished plastic lenses, spectacles and contact lenses.

• Mfg capacity expansion: currently producing 18k/day–>24k/day by end of FY23–>30k/day–>40k/day eventually by the end of FY24.

• 67% consolidated revenue from outside India, 33% within India.

Valuation:

M.cap as on 04/03/2023 is 50cr. or 9MFY23

Sales is 55cr

EPS of 7, P/E for the same period is 16

Tailwinds

Imposition of anti-dumping duty in mid Jan’23.

FY22 AGM Notes

• 2nd Lockdown restricted plans to travel to Korea. Due to this couldn’t execute the plans.

• Said Indian economy bounce back provide good hopes. Hinted that open of optical shops provides GKB business

• Faced problem like interruption of raw materials, collapse of vendors etc. Dependence on China for raw materials till date is true. Efforts should be put to grow this in India.

• Said company sees immense potential of sales.

• Govt. imposed anti-dumping duty on plastic lenses.

• Financial performance: USA, UAE subsidiaries have done well despite pandemics. Mgmt. is focusing in operating efficiency, manufacturing costs.

• Company has established raw material supply outside china. In the past the price from europe and USA are expensive. However, GKB has stroke a negotiation with these supplier for continuous supply with a slightly higher price than China.

GKB Ophthalmics Ltd - AGM 2022 (from 19 mins onwards)

• Company said they have increased the prices of finished products due to increase of raw material prices and said that this will be reflected in sales figures starting from Q1FY23. However, the Q1FY23 revenues were similar to the quarter before. Net profit is improved.

• Mfg capacity expansion: currently producing 18k/day–>24k/day by end of FY23–>30k/day–>40k/day.

• Forecast a revenue growth of 40crs in FY23. However it didn’t happened until Q3 of the same. FY23 shall show much better results. Korean subsidiary has become financially unviable. New expansion is being planned in the same company instead of another subsidiary.

GKB: Has 60years history. Mr. Gupta assured no need of apprehension on this stock.

Promoters

• Salary cuts of its employees during covid: Company made pay cuts for all employees for couple of years during covid. However, despite no request from employees to repay the portion of the pay which was cut during covid, promoters kindly announced that they will pay back all those pay cuts now.

• MD of the company, Mr KG Gupta has ensured that this business endured the ups and downs over the past multiple decades. A number of other peers winded up their business in the same time period.

Risks

• Company has been announcing about capacity expansion from the past few years but couldn’t materialize until the end of CY22.

• foreign exchange fluctuations. Since the Company also depends on exports, the economic situation in exporting countries is likely to affect the performance of the Company.

• Domestic revenues can be impacted by supply from unlisted players

Apparently, their Korean subsidiary is selling off 3% of their holding, which played a key role in it’s fall in it’s share price from 180 to 99rs

Disclosure: Invested in tracking quantity