Overview

While this is in no way comprehensive, this is an attempt to understand the business of Gillette India. The company is engaged in the manufacturing and sale of branded packaged fast-moving consumer goods in the grooming, portable power and oral care businesses.

- It commands a 70% market share in the blades and razors segments and 28% market share in the toothbrush segment

- 80% of revenues come from grooming and 20% from oral care

- The company has a good balance sheet strength

- The company has 2 manufacturing plants, one in Rajasthan and one in Himachal Pradesh

Headwinds

- More WFH, lesser social interactions, men shave less

- Competition in trimmers and oral care

- Consistently losing market share over the last few years in the US

Tailwinds

- People will tend to avoid salons, buy razors and blades and shave at home

Consumer behaviour

- Facial hairstyling is the trend for the last few years and Gillette has not shown aggressive product placements and launches.

- Competitors like Philips, Havels, MI who are traditionally not into personal care are entering the space with aggressive pricing (Kodak moment?)

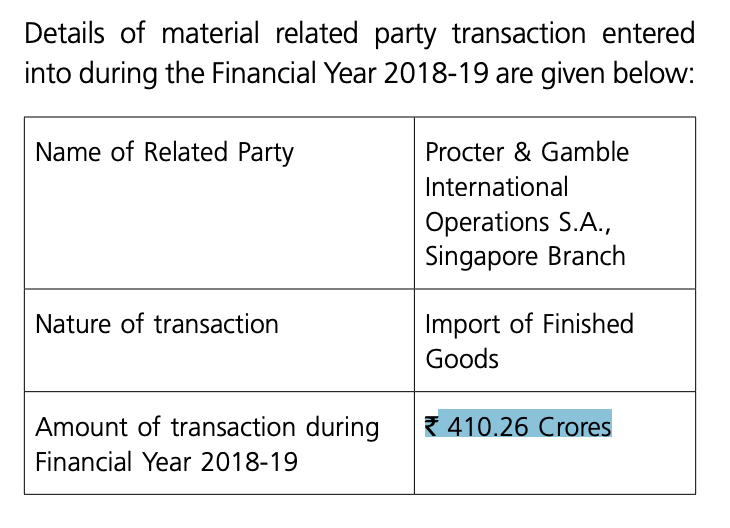

Related party transactions

The company seems to be importing premium razors from abroad. The local manufacturing facilities appear to be for high volume mass products.

Royalty

(in Crores)

| 2019 | 2018 | 2017 | 2016 | 2015 | |

|---|---|---|---|---|---|

| Royalty | 14.2 | 10.32 | 12.84 | 14.02 | 11.54 |

| Sales | 1862 | 1677 | 1733 | 1755 | 1875 |

| Net Profits | 158 | 214 | 253 | 229 | 253 |

| % of Profits | 8.98 | 4.82 | 5.07 | 6.12 | 4.56 |

Concerns

- No new major product launch after Proglide in 2014

- The company has seen a gradual slowdown in sales from 2015 onwards

- The company has a questionable track record when it comes to expansion and entering into new product segments.

- Gillette used to own Duracell which was sold off to Berkshire

- The oral care segment has intense competition from Colgate and is less profitable as compared to razors and blades

- The crux of the business model is to sell cheap razor handles and then charge customers with expensive cartridge refills. Historically they have evolved from the single blade, double blades, 3 blades and so on. With each incremental addition of blades, the cost of cartridge would also raise. However, it appears that there is not much steam left in this model and the company needs to look at other newer ways of improving margins.