While this is in no way comprehensive, this is an attempt to understand the business of Gillette India. The company is engaged in the manufacturing and sale of branded packaged fast-moving consumer goods in the grooming, portable power and oral care businesses.

It commands a 70% market share in the blades and razors segments and 28% market share in the toothbrush segment

80% of revenues come from grooming and 20% from oral care

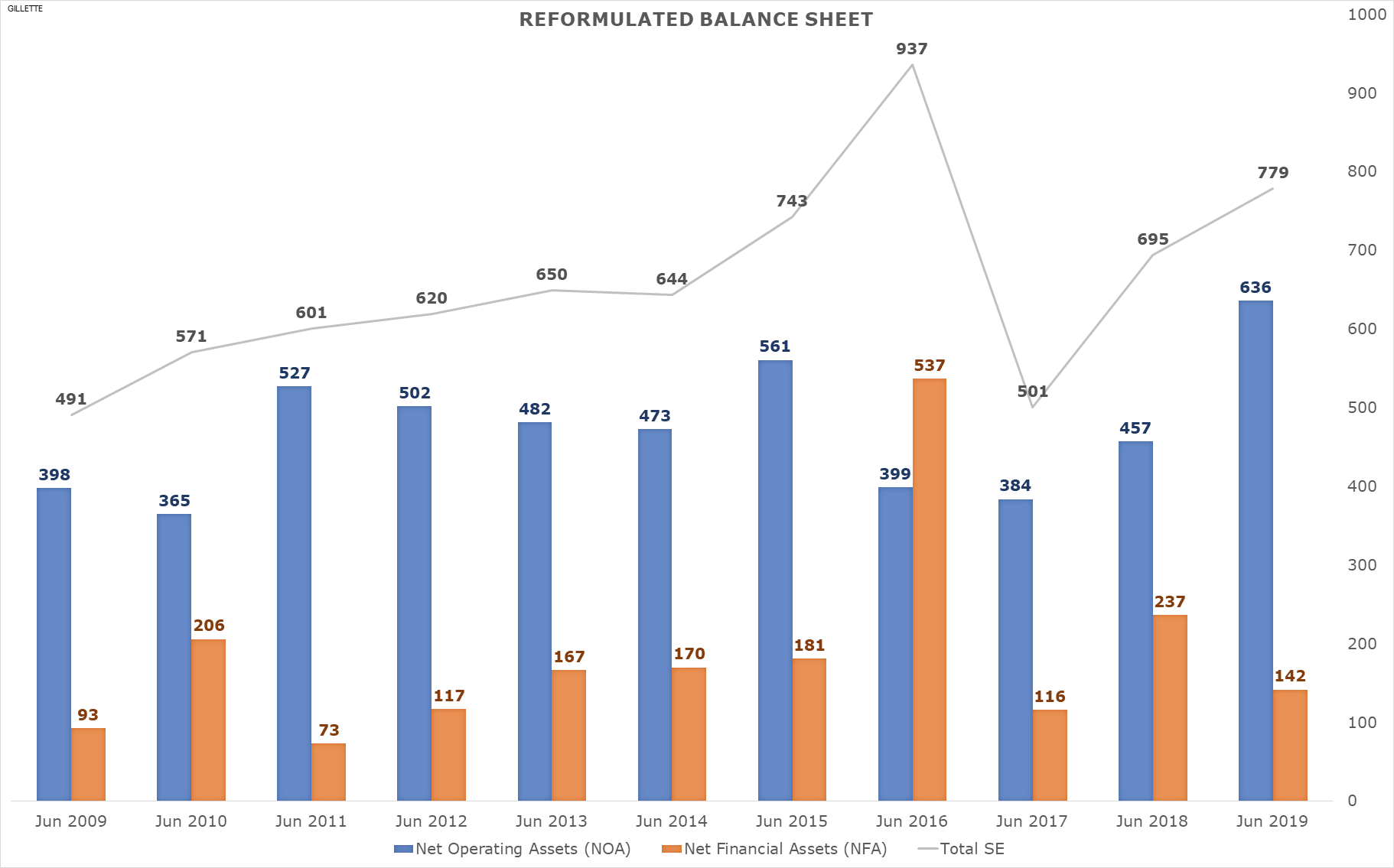

The company has a good balance sheet strength

The company has 2 manufacturing plants, one in Rajasthan and one in Himachal Pradesh

Headwinds

More WFH, lesser social interactions, men shave less

Competition in trimmers and oral care

Consistently losing market share over the last few years in the US

Tailwinds

People will tend to avoid salons, buy razors and blades and shave at home

Consumer behaviour

Facial hairstyling is the trend for the last few years and Gillette has not shown aggressive product placements and launches.

Competitors like Philips, Havels, MI who are traditionally not into personal care are entering the space with aggressive pricing (Kodak moment?)

No new major product launch after Proglide in 2014

The company has seen a gradual slowdown in sales from 2015 onwards

The company has a questionable track record when it comes to expansion and entering into new product segments.

Gillette used to own Duracell which was sold off to Berkshire

The oral care segment has intense competition from Colgate and is less profitable as compared to razors and blades

The crux of the business model is to sell cheap razor handles and then charge customers with expensive cartridge refills. Historically they have evolved from the single blade, double blades, 3 blades and so on. With each incremental addition of blades, the cost of cartridge would also raise. However, it appears that there is not much steam left in this model and the company needs to look at other newer ways of improving margins.

The simple thing about Gillette India is - It’s kind of a huge fish in big pond. It will grow only as the pond grows. Means its already a monopoly with major market share. The market knows about it. So its growth probably depends upon the growth of population. That’s it. Not more.

It’s better to focus on small HUNGRY fish in big pond. The chances of growth are more.

My personal opinion.

Vikas

Lot of new age startups like Bombay Shaving Company, The Man Company have shaving and other allied products. Another company Beardo (Marico) sells trimmers and other male grooming products. All these companies are very creative in advertising and have a very good brand recall, premium look & feel products. I think Gillette could have aggressively gone into male grooming space and missed the boat.

Gillette seems to have got its MOJO back…sustained 3 quarters of growth and profit increase . Out look for q121 looks promising with both grooming and oral.care doing well …expect renewed interest as from FII AND DII

Q3 & Q4 of FY 2020-21 has revived the expectation of growth in Gillette India. For FY 2021-22, Revenue may cross Rs. 2000 Cr with PAT touching Rs. 400 Cr. and similar cashflow.

Introduction of new brand ‘King C Gillette’ in premium personal grooming segment is a sign of management’s strategy.

Besides that, stock is trading at similar leval of 2015-16 with all the following characteristics;

Strong Brand

Daily Essential Product

Good Margin

It provides good margin of safety and if the revenue growth can be achieved, it can be a potential candidate of re-rating. Keep a close watch on results of next couple of quarters!

Only issue I see is that male grooming is not pure shaving anymore. There are lot of expensive trimming and related grooming products where future consumer money will go.

Unfortunately P&G has separate brand for the same and those products don’t come under listed Gillette India.

Darshan Gala:

Gillette concall notes(latest)

Business:

They are growing and creating value through a strategy that drives growth and value creation through five integrated choices:

A portfolio of daily use products, where performance drives brand choice

Superiority across product, packaging, brand communication, retail execution and value

productivity to fund this superiority

Constructive disruption of the entire value chain to future proof our business

A highly efficient and effective organization structure

The model is dynamic and sustainable

Products :

Gillette guard is their most affordable system razor designed in India for india, especially for rural consumer’s. It is designed keeping in kind the context that these household’s may not have access to running water and couple with their aspiration of confidence and dignity, they have continued to upgrade their product. Has the highest share in rural market this year

Orbal B- with their power oral care tooth brushes they have been able to provide their consumers with the most power packed brushing experience -A smarter way to brush that gives up to 100% more plaque removal, whiter teeth, improved gum health and with 3D technology, visible pressure sensor and a 2min professional timer. Along side this they are also educating their consumer’s on oral health practice’s.

In apr/may/june qtr saw the fastest fmcg consumption they have seen in the last 6 qtrs

Inflation is softening and volume growth is finally returning. the 7.5% volume growth in the qtr is great news for industry even the rural growth turned positive by 1.4% volume growth in the non food sector after four qtrs of significant volume decline.

Cautiously optimistic is the term is what describes their situation

Expanded direct reach by over 65% vs where it was 5 years ago

They have started smart distribution. They have developed in house data science engine powered with artificial intelligence (AI) and advanced machine learning models (ML), which enables it to equip it’s diverse store network with a customized range of product offerings, bases on the demonstrated preferences and needs of the consumer’s in the vicinity of these stores. The innovation aims to help kirana store owners in efficiently optimizing their stock inventory, significantly reducing non-moving stock, and enhancing business operations by serving consumer’s better.

Their market share for Gillette is at highest ever level upwards to 60%

This year brought products like Mach 3 Charcoal, Venus swirl and Braun BT5 launches. And Introduction of Oral B sensitiveX - a premium sensitive toothbrush, and a relaunch of Gillette fusion as a styling tool. They continue to upgrade their propositions, including Gillette guard, Oral B criss cross and Oral B kids electric toothbrush.

A substantial portion of their sales is locally manufactured locally and they are always on the lookout to bring more parts of their biz under local manufacturing.

As per capita income rises in the nation, discretionary spending rises accordingly, which is when consumer’s are able to pay higher for product superiority, a phenomenon theh summarise as premiumization

The premiumization trend has been positive for Gillette as well as Oral B, as they have seen per capita incomes rise in the country and consumer’s willing to pay for superiority. This is reflected in their growth of premium products.

There is alot more room for premiumization in oral care

Braun today has the world’s best tech when it comes to shaving and trimming

The royaly agreement is towards the use of intellectual property of the parent that they use in India.

Female hair removal is actually a large market, but razors compete with creams, in-home waxes and salons. Their focus has been on the in-home hair removal segment. In the last 3 years, razors as a sub segment have seen fastest growth.

Venus India has grown 10X in P10Y. Most recently, in their quest to provide the best possible shaving experience, we introduced Venus Swirl. This is a 5-bladed razor – 1st in the category with a rotating head that helps provide a

Darshan Gala:

clean, smooth shave.

Management:they are also making headway with what we call SMART distribution. An in- house developed artificial

intelligence and machine learning algorithm that analyzes consumer behavior and pattern to

customize a range of P&G products at a store level. With this, we have transitioned from a cluster-

based planning to a store/neighborhood-based planning. This win-win model is helpful for the

consumer in making their desired products available and helpful for the store owners, helping them

optimize inventory and significantly reducing non-moving stock. This is how we are improving

The strategic need to keep investing in superiority, the short-term need to manage through a very

challenging cost environment and the ongoing need to drive balanced top- and bottom-line growth,

including margin expansion, underscore the importance of ongoing productivity.

We have developed a strong productivity muscle over the years. Productivity is now fully embedded

in our operating model and is embraced in every part of our operation. Specifically, last year, through

our productivity interventions, this company achieved savings of over Rs. 55 crores.

Their organization structure is designed to focus our human, technical and financial resources on our

biggest opportunities for growth. The structure yields an empowered, agile and accountable

organization with very little overlap or redundancy - flowing to new demands, seamlessly supporting

each other to deliver against our priorities in the communities.

Therefore, they keep upgrading their bouquet of policies and programs to cater to our diverse workforce

so that every single person can bring their whole authentic selves to work every day. For example,

Their Lead with Care program offers a holistic and support to employees who are caregivers to children

with disabilities and special needs, including neurodevelopmental, cognitive, behavioral or physical

impairments. The program includes medical coverage, specialized and trained day-care support via

certified partners, and an employee assistant program( EAP) available 24X7 to all employees and their

families to navigate this journey.

Our longstanding commitment to education is also a way of contributing to the social development

of the country brought to life via our flagship CSR program, P&G Shiksha.

P&G Shiksha is a holistic educational program that addresses critical barriers to achieving universal

education. Over 18 years, Shiksha has helped reach thousands of schools in communities, impacting

over 35 lakh children.

Environmental sustainability has been embedded into P&G’s business practices and we consistently

strive to minimize our environmental impact, encouraging consumers and suppliers to do the same.

Their goals:

• We have committed to accelerated efforts to combat climate change as part of ambition 2030.

• We have committed to be Net-Zero by 2040.

• Our global water strategy aims to restore water in water-stressed areas around the world.

• Today, we are collecting back more plastic packaging waste than we put out in India and

leverage renewable energy in our operations.

• Our brands are incorporating sustainability in serving consumers with superior products, for

instance, by leading the use of recycled plastic.

Management expects volume consumption growth within FMCG category to be in the mid single digits over5-7years.

There are several other category where consumption is underdeveloped, whether they look at the potential to further improve and impact consumer lives, or if they compare to other countries with similar per capita income. They see an opportunity to grow these categories double digit. To make this a reality, the role they see companies like P&G play is to continue to drive

awareness and education, make our products available to consumers at varied price points and retail

channels, and continue to delight them with superior propositions at the right value.

Expect oral care as a category to demonstrate market growth of mid single digits, in line with FMCG market growth,

It looks like Gillette India uses the distribution network of P&G. There is a lot of negligence as the distribution under PG. Gillette prouducts are not being placed as they should have been.

It should have an independent distribution networking, and this is my opinion. After having discussed with many retailers, this is my thought.

Disclosures:- Invested with hopes that the product does get it’s due recognition!!