for a stock that is dipping every other day, even sentiment boosters matter sometimes. Besides, this does not take away the fact that the company has performed very well in the last 2 qtrs since it has been listed. Why there is still little institutional investor interest in the stock, no one really knows.

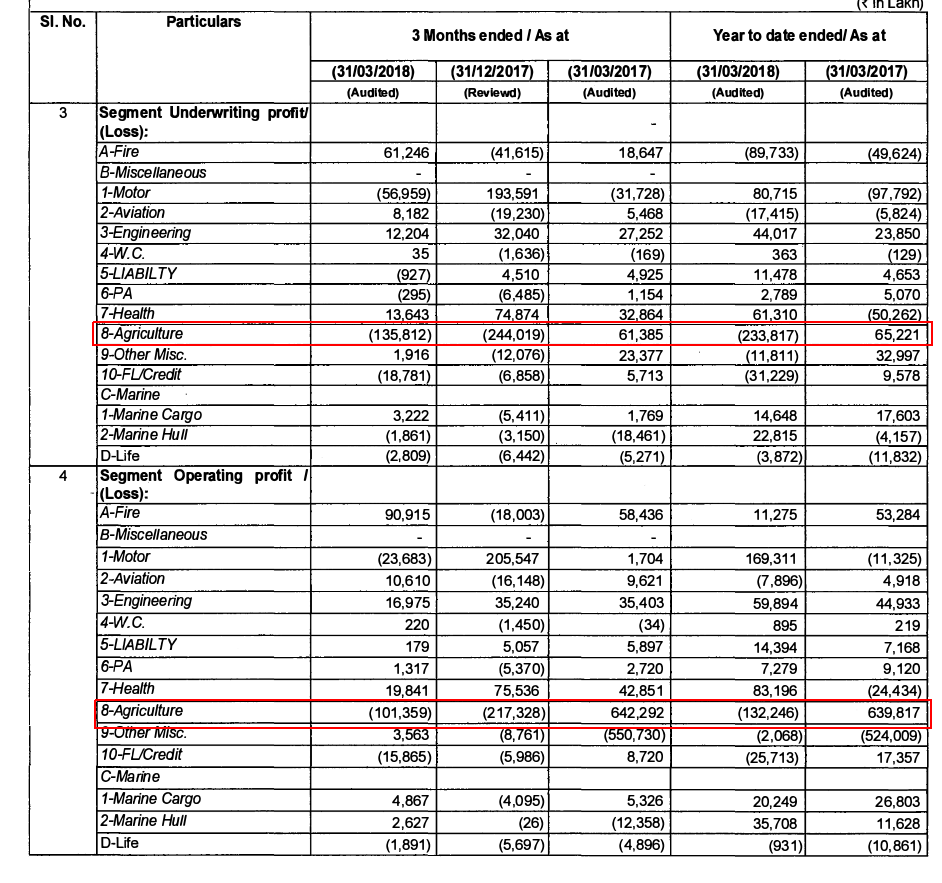

Company did losses both at underwriting and operating level in Agriculture segment, which is very discouraging, given monsoon was normal in fy18.

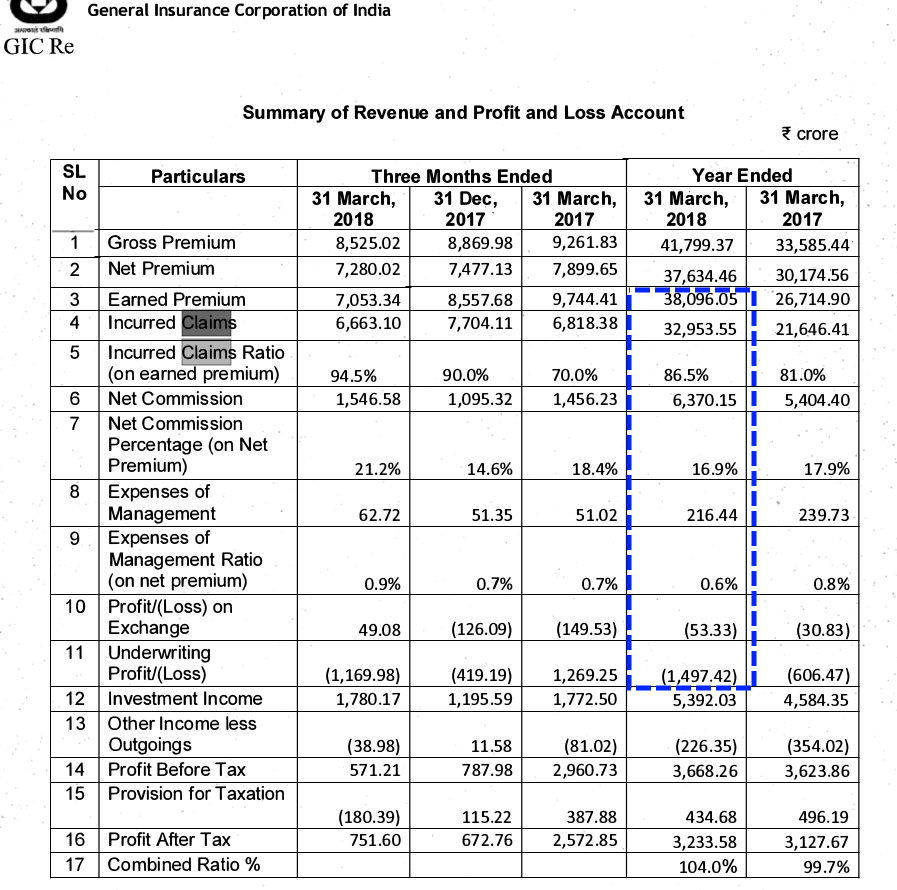

Book value growth was just 7.5%, which is not quite encouraging.

Moreover combined ratio jumped to 104%.

2 Likes

Poor agri performance is due to previous years claims coming in the current year

Excluding that combined ratio for agri in this year is 105%(vs reported 120%)-however this time the mgmt claims they have already included potential Rabi claims and provided conservatively.(this needs to be verified)

So over 2 years of the scheme average combined ratio is 107%

Now they have reduced the commisions rate by 7% for the agri business(direct improvement in combined ratio) and are working on renegotiating the rates for retrocessional insurance in agri segment. This,in the opinion of the mgmt,should lead to drop in combined ratio to 100-105% in the agri segment

In FY19,they aren’t looking to grow much in agri segment(they have 46% market share of agri reinsurance market).Overall growth should be 16-18% in gross premiums.

International combined ratio at 115% has been poor because of the large number of natural disasters in 2018 primarily the USA hurricanes. This is expected to improve in FY19

Source:Q4 concall

3 Likes

In strict sense Combined ratio is not as stated by you earlier.

As we can see Incurred claims are less that earned premium.

Therefore Combined ratio = (Incurred Claims + Other Expensed) / Earned Premium

where, Other expenses are

- Net commission

- Expensed of management

- Forex gain/loss.

On separate not why GIC has to pay so much commission!!!

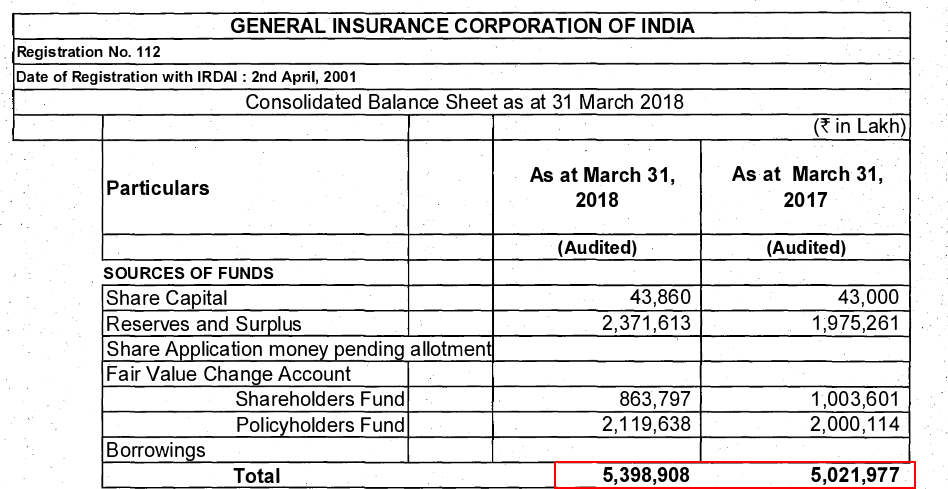

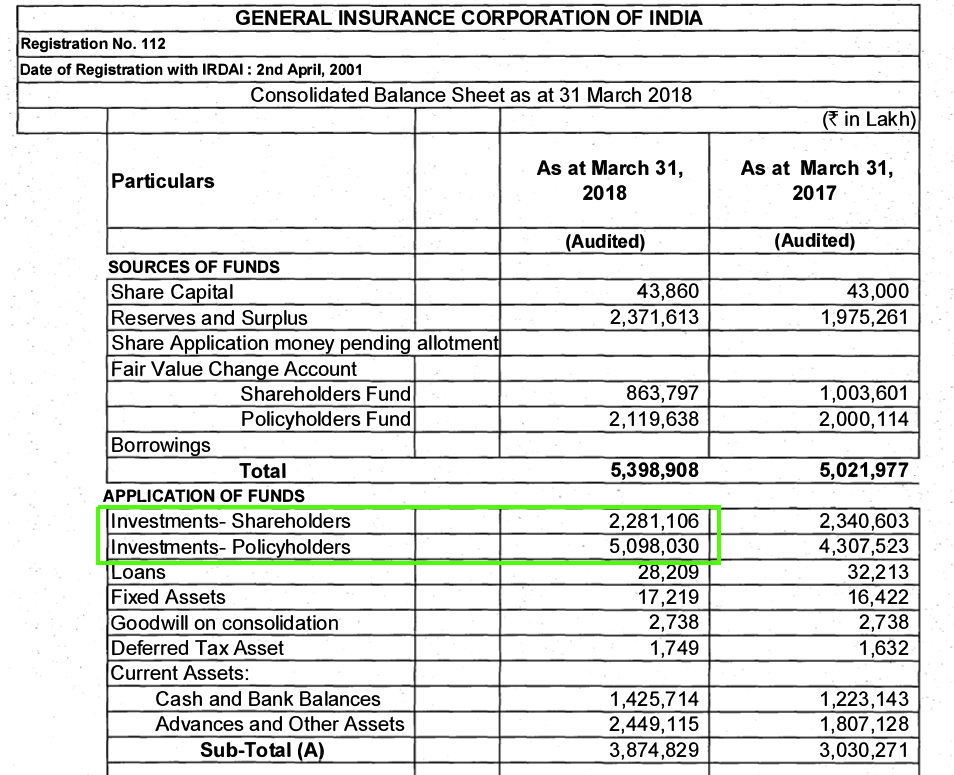

Float seems to be Investments - Shareholders + Investments - Policyholder

Therefore, Float = 73,791 crores

& Income from Investments = 5,392

which is 7.3%

this yields looks quite low.

I could not find any mention of trade receivable, therefore it is difficult to know if Govt has paid all the premium or not.

2 Likes

I have a doubt in calculating Book Value and RoE of GIC Re or for that matter any insurance company. There are 2 kinds of book value.

-

Book Value without including fair value change in policyholder fund which is the one mentioned in balance sheet. This book value is 138 and P/B = 356/138 = 2.58. Based on this BV, the RoE is 16%.

-

Book Value including fair value change in policyholder fund which is 285 and P/B = 356/285 = 1.25. Based on this BV, the RoE is 8% which is equal to investment Yield.

Am i right in my interpretation ?

If so, we cannot say GIC Re is relatively cheaper but is fairly valued at current price since in case-1, RoE is high but P/B is also proportionately high and in case-2, RoE is low and hence a lower P/B is justified.

Kindly clarify.

2 Likes

Its actually a good question and something I was also confused about.

But my opinion is that we would calculate ROE as PAT/Networth (excl fair value change)

So ROE of business on the core equity is 15-16%

However when calculating

When calculating price to book we also have to include the mark to market gains(this is not core equity of the company)

I know that I am taking best of both, but in other industries also we indirectly do this since we always calculate ROE on historical cost basis(assets are not marked to market in any other cost balance sheet ).Hence we are doing the same in this case.Investment yields will be calculated on the cost of investments which are included in the net worth. Thus only fair to calculate ROE on cost basis and not mark to market and then add the fair value change as a further investment(like we add cash for any other co)

But definitely your viewpoint should also be considered,this is debatable and I would request other forum members to enlighten us on this point

2 Likes

We do not do in all the industries. In banks all data is marked to market and in other industries it just a limitation that plant and machinery and other fixed assets are not marked to market and therefore book value hold little value in valuation.

I imagine if information is available it should be used and not neglected. We can also look at how competitors like ICICI Lombard are calculating RoE. @sambandham82

1 Like

But we do still calculate ROE on the book value/networth right? Am I missing something?

As far as I know,all insurance cos calculate ROE in this way but the impact is limited since fair value change account is nowhere close to GIC’s

Return on Equity = Net Profit / (Share Capital + Reserves & Surplus).

Book Value = Share Capital + Reserves & Surplus

Therefore, Return on Equity = Net Profit / Book Value

This is my understanding. I could not understand your question.

1 Like

The mark to market gains are the investment gains till date on the equity portfolio. Now the point being that until the profit is realised , no gains are included in the P & L as only the dividends received are included in the PAT .

Hence since the numerator (PAT) does not include additional income on account of the fair value of investments (this will only be added to PAT once equity investments are sold),we should not include the fair value in denominator (Book value) for purpose of computation of ROE.

This is because the ROE will be distorted and appear optically lower on including fair value change in book value since the PAT does not include the MTM gains on equity portfolio.

3 Likes

Your arguments seems logical and correct to me. @sambandham82 What do you think about the argument of @Anirudh72?

I think u r right. That is the way to value GIC.

Book value = 138, For a business with RoE = 16%, Dividend Payout ratio =18% (20 yr avg) and very high longevity, we can assign P/B = 2.5 and hence Value = 345 and fair value change per share = 147, Net Value = 345+147 = 492.

So IPO price of 456 was fairly and almost fully priced ?

2 Likes

Which IPO isn’t?

I roughly agree with your valuation but dividend payout will be 30%+.

i think RITES IPO was undervalued at 11 P/E which deserves 16 P/E for its asset light business model and robust balance sheet in a 25 P/E market. Its not a thumb rule that every IPO is fully priced.

The dividend historic average is 17% as attached data indicates and GIC never paid > 30% except in 2 yrs out of 20 yrs. RoE & Dividend based Expected Return.xlsx (19.2 KB)

.

But as per dividend policy for all PSUs, GIC may also give 30% in future.

1 Like

The Combined Ratio has risen to 104% as per the annual report for FY18.

I see the below risks to GIC business currently:

- The planned merger of the three general insurance companies, might help reduce their geographical risk and hence the need for less reinsurance, since risk is spread more evenly now

- The GI’s bargaining power should increase, resulting in less margins for GIC as a reinsurer

- SwissRe and other behemoths are constantly knocking on the doors of IRDA, its just a matter of time, when the preferred/first right of refusal is taken away from GIC

- Being a PSU demands that the valuation can never be higher than normal

Would be great to hear some positives, as i myself am invested from IPO days, and wondering if it would take much longer to recover the lost money here

3 Likes

Above a subscribed newspaper hence just posting link

1 Like

Interesting note on GIC RE

2 Likes

After reading note shared by @jinushah I am wondering why GIC is such an underperformer? It is available at fractional book value compared to 8x P/BV ICICI Lombard. Agreed that company is run by govt. employees who do not have passion and it is also evident that there is limited headroom for growth as it is has 75% market share in re-insurance. But still, it does not explains such pathetic valuations. Any strong anti-thesis is welcome.

2 Likes