GHCL ltd Concall transcript

Revenue for the quarter has been increased by 28% from 690 crores to 881 crores. Our profit after tax has increased to 113 crores from 78 crores compared to Q4 FY’16, registering a growth of 45%. In the inorganic segment, we would be glad to know that as indicated earlier we have completed our expansion of one lakh metric tones soda ash capacity in March ’17. Global industry scenario reflects that the Chinese industry is well balanced in terms of demand and supply resulting in a lower export from China. Even US and South American market is maintaining the equilibrium with the improvement in the domestic demand in that region. Europe’s own demand supply is also balanced; however due to supplies from Turkey, new capacities of 0.5 million metric tones and another 2.5 million metric tonnes scheduled to come up for production in the next few months. This can create a situation of oversupply in Europe and also to some extent in India.

The domestic industry witnessed a demand growth of over 5% this year and we estimate that this growth rate to continue for next 3-4 years.

Also with the increased production consumption of imported lime stone has also increased, this has resulted in an increase in the cost of production and impacted our margin.

Improved our profitability for the business owing to the higher volume coming from the one lakh metric tonne expansion.

“Textile business has started reflecting numbers”

Textile business has seen growth during the quarter with certain orders being dispatched from the last quarter and high volumes from the new order that reflected in the revenue growth of 39% over Q4 FY’16. The coming year would see certain challenges in the textile industry as a whole due to volatility in the cotton market and dollar devaluation, which may put pressure on the margin in the coming year. We have achieved a debt equity ratio of 1.04, the management has proposed a dividend of 50% on the capital which is 15.27% payout of the all profits.

Announcement of another 1.25 lakh metric tone of soda ash expansion at the existing capacity which will make us largest soda ash plant at one location in the country. FY2019 with an estimated capital outlay of 300 crores. Also, we would be glad to note that we have registered a growth of 49% in the profit before tax in last three year’s CAGR compared to our guidance of 20%-25%. I believe that we shall continue to maintain a growth rate of 20%-25% over the next 3-4 years.

In our inorganic chemical segment, we achieved a production volume of 2.24 lakhs tonnes during the quarter as compared to 1.95 lakhs tonnes of Q4 ’16. production of 8.01 lakhs tonnes compared to 7.49 lakhs tonnes registering a volume growth of 7% in production and sales of soda ash.

In our textile segment, we achieved a strong revenue growth of 39% and with a topline of 360 crores as compared to 259 crores of Q4 ’16. For the year, the revenue has grown by 16%

Working capital days increased to 68 days from 64 days of December 2016 largely on account of we have to keep a margin money in escrow account for our buyback and also one income tax refund which is due. The return on capital employed for the year is 21% as compared to 22% which is largely due to new capital investments in both the businesses. The RoE of the year has improved to 29% versus 25% last year.

“Textile industry overview”

Mr. Purushottam, let me give you my overview of about overall the textile industry per se. One, in terms of the cotton prices, my understanding is that if you look at last few, I would say that 15- 20 days the cotton prices have slightly softened. Of course, it has gone up as compared to what it was in the October, but then subsequently it has been softened also. International prices if you look at has dropped by almost I would say around 7%-8% in last few days. And therefore my belief is that the cotton prices are not likely to be very high going forward from here. But on the other side as you rightly said there are few things which is developing into this market, one is the dollar as you know, the dollar has depreciated in last few months, I would say from 67-68 to now 65. So that had definitely one concern which industry is facing and going to face further. But if you look at in terms of, as you rightly said there are lot of over demand, I would say the supply is more than the demand. A lot of new players are also coming in and also that US retailers as you all must have noticed, that the US retailers are not doing very well. Lot of brick and mortar stores are facing challenges and lot of retailers are closing their stores. And therefore there is going to be definitely a pressure on the pricing side from the retailers to maintain their margins. So overall I agree with you that going forward the industry is going to face pressure on the margin.

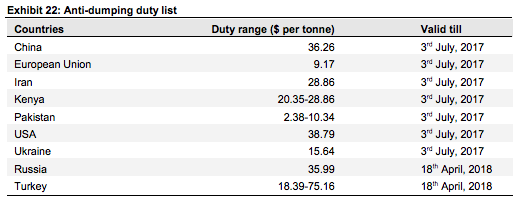

that there could be pricing pressures on the textile side and at the same time because of certain cost pressures even in the soda ash, there could be some softening of the prices and next month you are expecting I think the decision on the antidumping duty also. what kind of the overall pressure you expect or you are projected in the margins for FY’17-’18 that is current year.

So far the margin which you said, if you look at the Q4 margin, you will find that the Q4 margin has dropped by 4% as compared to Q4 16. Margin overall company as a whole, the margin is around 21%, EBITDA margin I am talking about. And this margin probably I would say that because of the volume growth and because of the other initiatives which we are taking, I think probably we will try our best to maintain those margins going forward.

Just one more thing on the Q4 numbers. Is there any element of the soda ash business or anything at all which kind of overflew from the Q3 into Q4 because of demonetization?

If you remember that there was a small quantity which was there in the Q3 around 10,000 tonnes because of the demonetization that has been shifted from Q3 to Q4. But overall also, we have increased our production from 191 to 224. So we have significantly increased our production also during the quarter.

So sir that increased inventory and working capital, would that be on account of more finished goods in the system or there is something else?

one more point is we have one income tax refund of almost 40 crores which was in the current asset side that has started coming post closing and also there was around 27 crores which was held in the margin account on account of buyback. So these two things are also pairing which are equivalent to cash only, that currently has stuck up on the current asset side, almost Rs. 60 crores.

can you tell the sale volume for soda ash for this quarter as well as full year?

For the quarter, it was 188,000 in the last year vis-à-vis this quarter was 2.22. That means it has gone up by roughly around 34,000 during the quarter as compared to Q4 16.

And for the year as a whole, 7.01 lakh tonnes to 7.5 lakh tonnes, I am talking about only soda ash sales. Extra 49,000 tonnes means from 7.01 lakhs to 750,000 tonnes.

So 90% of that may come in next year?

Out of that, some benefits we have got in the last quarter, Q4 FY17, so balance quantity we will be getting this year.

See if you look at my earlier guidance was around 15% during the year 16-17. Against that 15% guidance, we could achieve 14%. We are short by 1% in our guidance. As you know that dollar depreciated and volatility in the market and new things which has happened in the US market, like I said this business at this point of time lot of new things are happening. As you know that GST is also coming into play, what happens to the export advantage which is available at this point of time, how that shape up and how the US market will be there in the next, as you know that new administration has come into the US. All this put together at this point of time it will be very difficult, but like I said in my discussion that the business looks some challenging there, but if I can say for the longer period of time as we have said in the past also, we are very bullish on this business.

Like I said, the Turkey production is coming in, how that shapes up and when it comes what happens to the antidumping duty. Those are the question marks which will be there in the business, but as we have been maintaining always, we have seen that 49% CAGR growth in the last 3 years and our overall guidance is that in a longer period if you look at will always try to keep growing our business where the bottom-line it grown by 20%-25% on a longer term perspective.

Lastly, what will be the CAPEX for the next 2 years, this 300 crores will come in 18 and 19?

“Capex next two years”

This major portion will be coming in the next year I would say that because the lead time for any project takes around 1.5-2 years’ time and we are going to spend around 300 crores only on soda ash in next 2 years and overall in the other businesses as well, we will be spending money on our textile business as well. So all put together in next 2 years, we are planning to spend around 600 crores to keep our momentum of the growth in the topline as well as in the bottomline. And we have sufficient resources to put in this money.

we have already invested around 50 crores in buyback and let me be categorical in this there is no management and no inside equity selling by anybody. So as far as the pricing of sales are concerned that is the investors call, our role is only to give a performance to our stakeholders and I am just happy to inform here is that we have been awarded certification of a great place to work and which clearly indicates that this is a very prestigious award for any organization in India. because we believe that our role is to create a value for all our stakeholders and we will continue to do that. In terms of the dividend, like I said in the past also our endeavor is always to reward our shareholders and give better dividend going forward. Last year we have given 35%, this year we have given 50%.

I think our debts are well within the norms and our interest cost is also is nine and half percent overall and we are also trying to improve on our interest rates and so that it becomes very effective and as you know equity is always is a high costly servicing. So therefore reducing the debt and not doing the optimization on the equity is will not be the right thing.

In terms of your incremental capacity which has come on stream, how much of that was there in actually the Q4 results?

Mr. Gandhi, thank you very much first of all and out of the total I would say that roughly around 20,000 tonnes we have been able to achieve in the last quarter out of 100,000 tonnes.

out of the total capacity of 20,000 tonnes we have already achieved in the Q4 and obviously that 20,000 will continue in the going forward and in addition to that, there will be additional production as well. Overall what we are estimating is this year in 2017-2018, we used to be in the position to achieve around 80% to 90% kind of a capacity utilization from the new capacity.

you will find that the growth of this numbers we will be able to achieve this year probably might not going forward. Like I said, we are expanding on the soda ash. Our business in the textile also will not be as it is today we are adding the volume, there also we are adding the volume in our consumer product division also. All put together we believe that we will be able to create and some of the area which weare doing on the cost side will also help us to improve our margins.

“Variables to track”

Global scenario of the Turkey, US scenario of the textile, cotton scenario, Dollar, nobody knew that the Dollar will be in the situation.

“Need to track this”

The matter is in the consideration of antidumping authorities. How this will shape up in next one or 2 months it has to be seen.

The sunset review is being accepted, then this duty will continue for another one year and then in the meantime, they will be doing all this internal assessment something like that.

improvement we are seeing because of your rating upgradation which is likely to happen, I would say in the middle of the year. And also we are doing some rate restructuring and that will definitely help us to reduce the interest rate and in terms of the debt I would say that we will be roughly reducing the debt by around 100 crores. Overall put together, we believe that we will be in a position to have a better numbers next year.

Q&A:

Can you give us the sense for how much cotton inventory you are carrying currently and also what your FX hedges are for FY18?

- The scenario is always you cover the cotton from season to season and that season starts, of course it starts from October but the real quality comes in the month of November. We generally cover the cotton from November to October. So we have a sufficient inventory up to September, October. But when it comes to the some of the imported cotton, there we have the inventory even up to January and February as well. So, that we are covered very nicely on the cotton.

- On the exports side, we do approximately around 50% of our likely export for the year we cover. We do not cover the 100%, just to keep a fluctuation into the mind and on the imports side, we cover only 2 or 3 months which is the current and balance we keep on open because and this policy is something which we review, I would say weekly basis to see that how the Dollar scenario is looking like and we take it dynamic decisions on this coverage.

Does that point still hold with the 1 lakh tonnes you have done already and the incremental capacity of putting it?

- we believe that stability in the margin should remain

- Uncertainties whether Turkey supply coming in, additional dumping duty decision to be pending. Why are we expanding our capacity at this point of time?

- See, if you look at first the advantage which we have because our capital cost per tonne of soda ash vis-à-vis any new capacity which is either in India or outside India, we are at a much better position, almost around 50% in the cost which we are incurring per tonne of soda ash as compared to the competition, number one. Number two, as you know that Indian economy is growing and overall in a longer term perspective, we believe that ultimately this commodity needs to be supplied from domestic producers only , if you look at globally also and this project does not complete in 6 months, it takes almost around 2 years to complete the project. So unless we are ready for that we will be losing an opportunity when the demand picks up.

- Yes,but as on today my belief is that this is not much significant reduction in the pricing of a commodity, primarily because the cost pressure has always been to every player. Either be it is a China player or the Europe player, this cost pressure which has been happened coal prices, coke prices, these pressures are there with everyone. So therefore I personally believe there will be not much reduction in the domestic pricing going forward.

- volume growth will be in the range of around 10% this year because of this expense and which we have done. And in addition to that, in the textile also I would say that kind of a revenue growth you should expect. So, overall I would say that in a longer term period we should be looking at around 15% CAGR growth on the topline.

we were covered up with the cotton part, how could the margins were lower at around 8% net margin?

- First of all on the cotton side what you said, I had clarified in the past also. The cotton coverage starts in the month of November and it continues to be covered up to March because the season starts from November and this season remains means you get the good quality of cotton up to March. So, you continue to cover the cotton and build the inventory up to March. And after that, then you consume that inventory since up to the October going forward. So, hedging if you talk today, I would say yes my hedging is up to October. But if you say in the month of January, no I did not have an inventory coverage till up to October. That is the process of coverage, it happens in that quarter. In a way, I would say that the major coverage happens in the period between January to March because that is the peak period for the cotton quality.

- where the pricing pressure is also there from the retailers side and all put together that has definitely added to the margin pressure on the textile business.

Sir, but the revenue is up by 100 crores quarter-on-quarter, so just could not understand that …

- See, revenue growth what happens is the revenue growth like, that last quarter we had because of the some shipment was not shipped in the last quarter, which had also gone in this quarter as well as some new customers have been added into the basket and sometimes you do an aggressive pricing also to have the volume. So, this is what has been done in this year.

If I were to a rough yielding of this incremental capacity of 80,000-90,000 in Q1, Q2, Q3, Q4,what should I take as delta?

- Soda ash business is always a slightly seasonality in terms of the production. First quarter is slightly better, the last quarter is the best and the third quarter is better. In between the two quarters which are rainy season where the production is slightly lower. So that way this number will be spanning out in the next 12 months, 60% to 65% I would say that comes, I would say 60%. 60% comes in the 6 months from January to say I would say June and balance 40% comes into the July to December I would say that.

- the employee cost, employee cost generally every year it goes around 10% to 12% and this year it is slightly higher because we have provided for the ESOP benefit also to the people and that has been added to this and therefore this inflation of employee cost of around 10% to 12% if all this thing there. In terms of the other costs depending upon the inflation, some increase will always be there. But that is getting nullified when you are increasing the volume because per tonnes or per revenue per Dollar revenue it goes down because if your volumes are high. So, this primarily will be in line with this percentage of turnover.

the scenario changing up in terms of the coal prices and in terms of now you are deploying more capital for the working capital also going up because of the expanded capacity. How do you think that this the contribution from the interest saving from the interest and the power fuel is going to continue or that will have a dent on demand going forward?

- See, 2 things. One, in terms of the internal efficiency of the uses of any raw material or the any utility, our endeavor which has been continuing many years will continue whereas the pricing which is more dependent upon the international scenario will definitely be having an impact. And that is the reason you look at our margin during the Q4 is already top by 4%. My belief is that that kind of a margin of 28% we should be in a position to maintain.

- Modernization, we have plan for 2017-2018 as well and which benefit will be coming 2018-2019. So, this process of making the capital and investment getting the benefit out of this will be an ongoing process which will continue.

- it is also dependent upon your cotton pricing, it is dependent upon the Dollar/Rupee, it is dependent upon even shipping cost. There are many things which are dependent upon on this. But yes our endeavor as I said in the past, our endeavor should be that we should be maintaining this kind of a margin.

And our plants are working at 90%-95% utilization levels?

- Yes, it is running at the full.

Note: Questions asked were limited compared to management commentary.