What is stopping this stock amongst the bull run that we are seeing and the cheap valuation. Seems big guys are accumulating. Waiting for the Mar end quarter SH disclosures.

Discl. Invested

What is stopping this stock amongst the bull run that we are seeing and the cheap valuation. Seems big guys are accumulating. Waiting for the Mar end quarter SH disclosures.

Discl. Invested

Does anyone know when is court verdict on ADD removal case? Is heart breaking to see all good stocks are performing very well except GHCL even after cheap valuations.

Isn’t it also better to encash some overvalued stocks and invest in under-valued ones. I am beginning to start some portfolio re-allocation.

Is there any specific reason for weakness in Caustic soda based companies when Nifty is at all time high ?

I did try to find some news around Caustic soda outlook and didn’t find anything concerning.

Caustic soda and Soda ash are two different chemicals and together forms the chlor-alkali industry. Caustic soda is commoditized with many smaller and bigger players hence prices follow a cyclical pattern more compared to soda ash which is an oligopoly industry with GHCL and Tata Chem with highest market share. Market concerned about caustic soda companies which have run up quite a lot. For GHCL, as there is no direct comparable, Mr. Market is taking sometime to give the right multiples and also seem to be concerned of removal of ADD however looks a promising long term story with growth coming in from both soda ash and textiles business; triggers in the form of de-merger possibility, re-rating, biggies entering the scrip

Discl. Invested ~10% of PF

Results are out … though slightly below my expectation but good growth in EPS due to some tax related adjustments and sllight reduction in number of shares due to buy back.

EBITDA margins are little less as compared to QoQ and YoY

Textile is showing decent growth.

Soda Ash capacity increased by 1 lakh tons… not sure how much they will be able to utilize.

Dividend declared INR 3.5 .

Any reason GHCL trades (PE of near 7x) half the values of Tata Chemicals (PE of near 14x).

Only reason I could think of is tainted past of its management… though its professionally run now(as it appears). Market may take some time to discover true value.

Here is my latest read on this company

overall this continues to be a wait and watch story.

@Yogesh_s interestingly as per the latest presentation of the company, they seem focused on maintaining profitable growth :

my take is the negatives highlighted should get compensated by scale advantage due to capacity expansion and interested cost reduction on overall profitability basis. Overall, Q4 margins look sustainable unless ADD dampens margins further. Also, next 2 year total capex plan is 300 crores whereas 2 years of cumulative cash flow should be around 900 crores. 40% of this if goes in divdend that is approx 360 crores. So, 660 crores goes in capex and dividend , so, they can bring down debt by 260 crores which should lead to approx 26 crore in interest saving which should add to profitability. From FY 17, profitability of Rs 387 crore, if remove one time tax gain of 40 crores, then, on Rs 347 crore profit , this 26 crore is almost 7% of current profit. So, 7% incremental profit excluding one time tax gain can come from reduction in debt. Though thsi was not directly mentioned in concall but when asked what you will do with left over cash, will it be used for debt reduction, management sounded positive on that. Currently, they are working on 96% capacity in soda ash and 90% capacity in textiles. If additional capacity can be converted into sales, that should lead to increase in profit.So, expecting a 5-6% addition to profitability from expansion. Capacity expansion in turkey could be spoiler though. Overall, even if margins remain flat at Q4 level which is 2.5% lower than previous quarters (same was communicated by management today on news channel), with that margin, due to interest cost reduction and additional revenue, still, there is scope for 10-15% PAT growth excluding current year one time tax gains as base profit. Disc : Invested with multiple transactions during last 12 months

@suru27 @ayushmit

company is projecting 20% profit growth backed by revenue and margin growth which in turn is backed by capacity addition. I am not so sure if they will able to sell everything they make as rupee, ADD and Turkey capacity expansion is not in their control.

Based on my calculation, their capacity addition is about 5-8% per year so some of this profit growth has to come from margin expansion. I am not sure if that can happen.

India imports soda ash not because we can’t keep up with domestic demand but because we are not price competitive wrt China and Turkey. ADD helps domestic producers earn a decent ROE as govt does not want imports to wipe out the domestic production. But govt has to balance interest of soda ash producers vs soda ash consumers. Normally ADD rate is decided such that producers earn a decent ROE but 30% is high. GHCL is low cost so others may not be earning as much but there is a good chance ADD will be cut. Overall, the threat of ADD cut will be overhang on this company. Otherwise, valuations look cheap.

Hi @Yogesh_s, I agree with your assessment. However, if you hear their concalls, they have been emphasizing on good profitable growth and though they have been cognizant of the expiry of ADD and competition from Turkey yet they also seem to be saying that the operational efficiencies and brownfield expansions will quite help them. Lets see how things pan out.

Regards,

Ayush

Today’s GHCL is different from 5 years ago.

Management looks aware and prepared for the business risks.

I think all the risks are already built in the price.

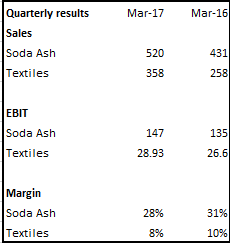

Looking at the each division in isolation - firstly it was very encouraging to see increase in topline for both textiles and soda ash…As far as textiles is concerned, every company has reported muted profits in q4 due to increased cotton candy price ,rupee appreciation and increased capacity in the sector…so one has to wait and watch what transpires for the whole industry going forward

As far as soda ash is concerned, clearly the company has been able to utilize the additional capacity shown by increase in topline which was missing earlier The margins have been a little below expectations though. The price reduction has been greater than 5% which is waht the management had guided. I believe they will maintain absolute EBITDA number this year of approx 500 cr.

Valuations though still remain compelling with limited downside. Assuming 50000/mt for a greenfield capacity the value of the soda ash business itself should be 4250 cr. For a market obsessed with growth this price can remain range bound for a while…however from a 2-3 years perspective this stock looks attractive still

Well, rising rupee is a short term phenomenon. Rupee will continue to depreciate in the longer run by 4-5% which is the difference in USD/INR bond yields.

Anyways, to save domestic industry Govt. would come in again with ADD if the margins get hit since there are majorly 2 players dominating the Indian market Tata and GHCL.

Discl. ~10% PF at CMP

That’s exactly how commodity companies work. They always try to maintain market share at any price. Just ask Airtel. With new capacity coming online, they will lower prices to grow their market share.

Keeping the issue of valuation aside. I think the results in 4Q have hardly added to any confidence, massive drop in the margins in one quarter and management guiding for that to be like the best case scenario in the coming year. In such a asset heavy play, EBITDA margin dropping from 24% to 20% will play negatively on the overall PAT.

Secondly, textiles commenrary was very weak - major headwind due to buyer behaviour - in case you all were wondering why a B2B player in textile should earn high RoCE like the likes of Trident, Indocount and pretty much everybody else - this is what the management had to say -“We are basicaully not able to pass the cotton price increase because of structural problems in our buyer segment - which is offline retailers - who are under pressure from the online retailers”. I think whats happening is that there buyers are squeezing them out and will continue to juice them - I dont think a Walmart will be stupid enough to let these guys earn the kind of RoCE they have been boasting off for long.

Soda Ash - Addition in Turkey of like 2.5 mn or something is massive - if the cost of plants are so expensive and this is capital intensive - I can guarantee you that Turkey guys would like to dump in India like anything.

Bottomline - Sometimes there are companies which look cheap based on earnings but then there earnings are at the peak of the cycle, that might be one important point to consider and form opinion about for somebody looking to invest in a company like GHCL - that are we seeing low P/E because of cyclically top EPS or can they sustain this EPS.

@8sarveshg I agree with you partially. I do no think anybody expected the margins in soda ash to remain the same post the ADD ruling. But a decline from peak margins does not necessarily translate into lower EPS as one has to consider the effect of increased capacity utilization. A comparison between the q4 16 and q4 17 results below illustrates what I am saying. Even though the margins have gone down a fair bit, the absolute EBITDA is still up due to increased capacity. Also buyback, although small will help in showing higher EPS too.

Rupee appreciation can be a major dampener to the story and play a spoil sport as it impacts both the segments as shown in this quarter. That said, I do expect soda ash to remain a strong cash generative business.

I am a little more concerned about textiles - not just the company but this sector in general. There has been a huge capacity ramp up lately. Price competition to increase utilization, appreciation in rupee, increasing cotton prices and buyers further squeezing margins can have a major impact on the profitability of the sector including the likes of trident, indocount etc.