Ghcl textile got demerged from Ghcl and it’s listings in stock exchange is still pending. Can any learned person can teach us how to arrive at the valuation of Ghcl textile which market is going to give?

Disclosure: Holding from 166 levels

1 Like

1 Like

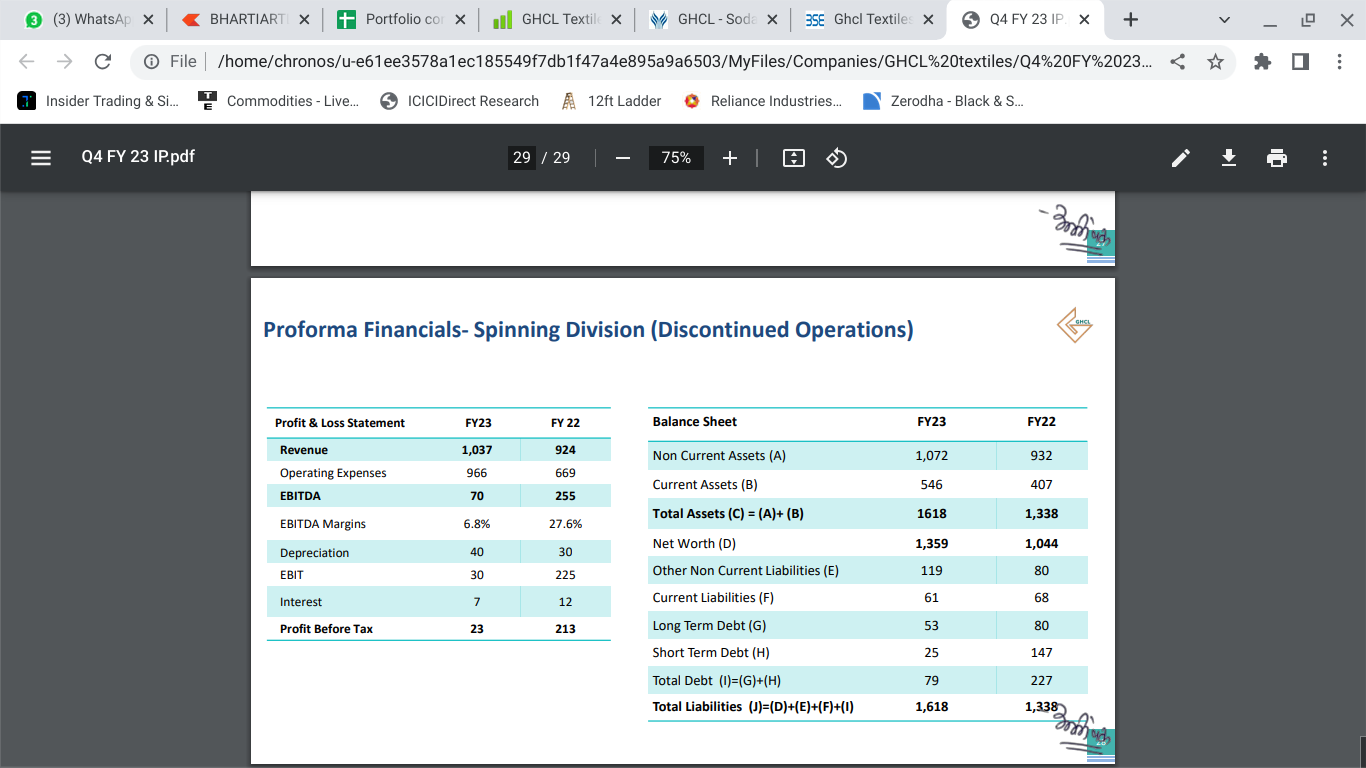

GHCL Textiles is trading at a market cap of Rs 639 Cr against its networth of Rs 1359 Cr, almost half the vaulation. See the financials of the GHCL textiles.

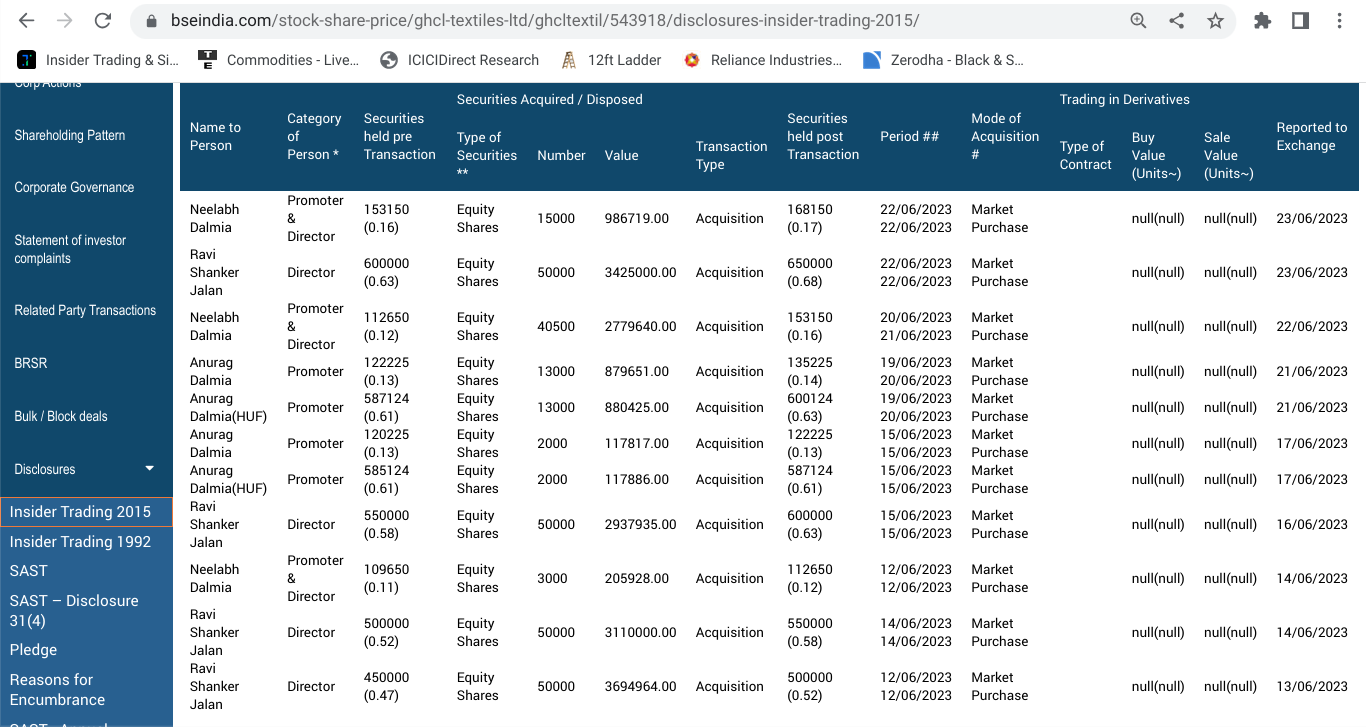

Since its listing, the promoters have been buying almost everyday. Is that the big guys are getting out of the stock because of low market cap.

Disc: Have been following the promoters and accumulating.

4 Likes

I was researching GHCL Ltd due to its enticingly low PE ratio along with other factors (clean & conservative management, ~26% market share in the soda ash market, increasing OPM, Increasing dividends, increasing EPS, textile segment separated- hence getting rid of diworsification, etc.,).

But right now, the company still looks un-investable due to the following reasons.

-

Soda Ash prices have been reduced twice (once in Nov 2022, & then in April 2022) [Everyone in the industry – Listed (Tata Chemicals) or unlisted (Nirma) is reducing the same]. The management is saying that the input prices of raw materials have also been reduced by the same amount – hence this price drop won’t affect the margins. But overall, seems like GHCL is a price taker.

-

96% of the company’s revenues are from India. And in India, the demand for soda ash is going to be the same for the next few years (~5% CAGR, mentioned in the earnings call by MD). The electric vehicle application for soda ash is not fully ready and will take time for the tech to be ready as per management themselves.

-

A lime kiln broke down resulting in a loss of two months of production from that plant. So, for FY2024, the production volume will be similar to FY2023 (& hence the sales). The utilization currently is also 94%. So no further room for an increase in capacity utilization as well. [Source: Page 4 in the earnings call, Earnings call, GHCL]

-

As others have pointed out earlier, GHCL’s MD has been conservative. But read what he said 6 months ago. “a major growth in the soda ash production is not likely to happen in the next two-three years – up to 2025-27.” They are expecting more of a margin expansion. [Source: MD on GHCL]

-

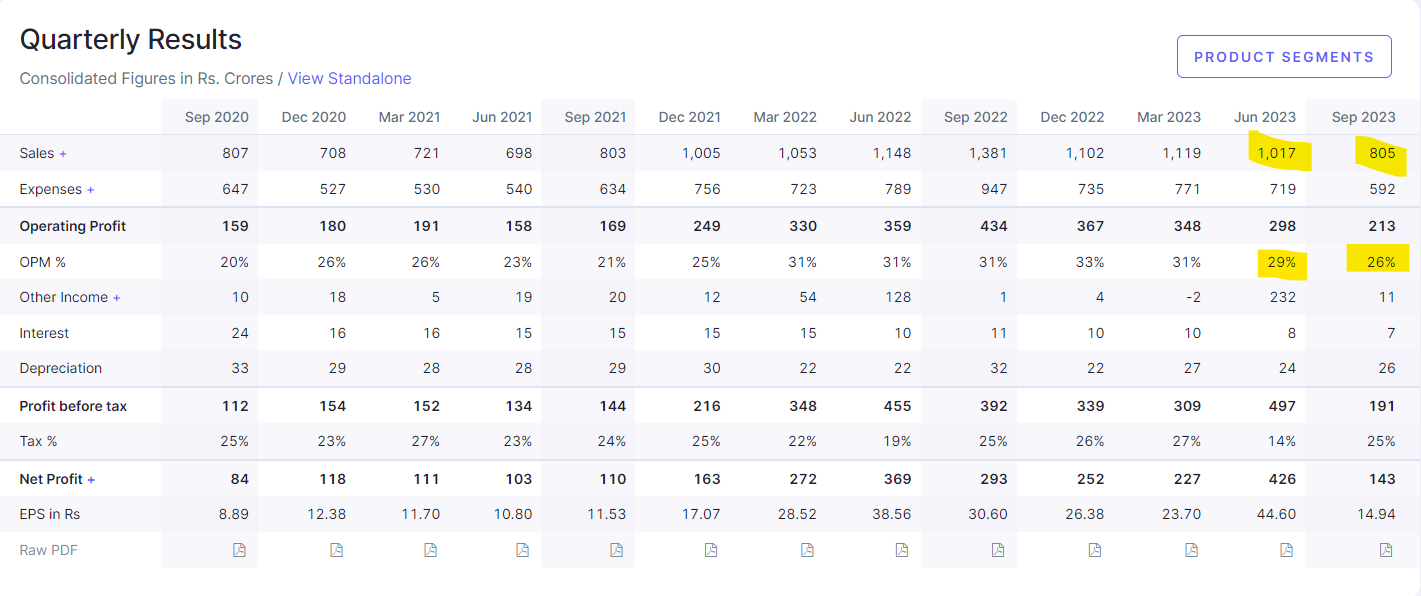

I also think the burst of sales from 3052 crores in FY22 to 4545 crores in FY23 has already been factored into the price of the stock. At this point, I am not so comfortable buying this stock. I would probably call it a “Slow grower” (Peter Lynch’s sluggards) & definitely not a multi-bagger.

Please let me know what you think of these points. Would be happy to learn.

Disclosure: Only researched. Not invested.

9 Likes

Soda ash is highly capital intensive business and it takes almost 4-5 years to get commercial production from any greenfield project that’s why it always remains a oligopolistic business with 3 main players in india (GHCL,TATA CHEMICALS & UNLISTED NIRMA). Due to the above fact , it acts a barrier to entry for any new emergent to gain any meaningful market share. The renewable energy especially solar power needs glass on very large scale and soda ash is major raw material in glass production. I consider it as a proxy to Green energy.

Meaningful consumption of soda ash in lithium ion battery will further act a growth driver when the complete ecosystem of EV’s kicks in.

In the end Soda ash is commodity cyclical business and if you know the exact phase of cycle , you can get decent returns.

Disclosure: Invested and biased from 166 levels.

9 Likes

Promoters/Jalan ji have buyed upto 70 level, no buying reported after that. However it still looks highly undervalued. Accumulating at every meaningful drop.

Disc-Have become Top holding and may be biased.

2 Likes

Yeah, this should jump definitely, the stock is highly undervalued.

Disclosure. Holding from 166 levels with almost 7years of holding. Views may be biased& major part of highly concentrated Portfolio.

1 Like

However, GHCL management in Q1FY24 con call are too much concern about

(1) Oversupply due to additional capacity across the word

(2) Margin pressure

Firs few pages of transcript are only this concern read: https://www.bseindia.com/xml-data/corpfiling/AttachHis/59c5d6ca-7e2c-410f-8dc8-a7b7ad1ac8e7.pdf

2 Likes

Another positive for sod ash manufacturing companies as soda ash is major raw material for toughened glass production. This anti dumping duty will further support the soda ash demand in india.

2 Likes

Has anyone done competitive analysis of soda ash manufacturers (listed companies) in India? Kindly share detail here

I also need help and some data regarding the same

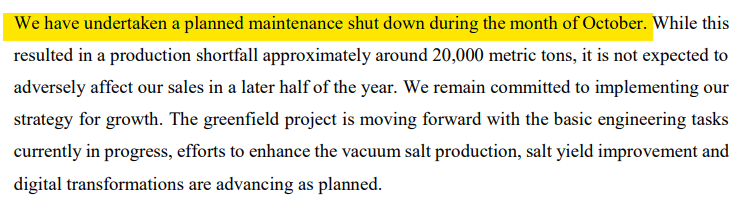

Recently GHCL already given bad result QOQ. In a recent concall they said that their one plant shut down during October due to maintenance. So can we expect more downside in GHCL?

And what is the major reason for bad results?

Is corporate governance still an issue for this company? Up until 2018 minority investors were moving to remove the promotor as per the news report. The promotor shareholding continues to be low

Started accumulating Ghcl textile today at around 69 rupees. In my opinion, this is one of the cheapest textile stock available in bull market. Its price to book value is 0.48. I think there is nothing much to loose in Ghcl textile at these current prices.

Disclosure: holding and biased both Ghcl and Ghcl textile from 166 levels before demerger.

What Ebidta margins can we expect from Ghcl Textile? Right now numbers not justifying the valuation as well as book value

1 Like

China +1 theory launched during chemical bull run, now boomeranging and hitting hard for all chemical stocks.

Lots of cheap dumping are eating top and bottom lines of Indian chemical industries. Companies having huge capex and more dumping going forward will give tough time for Indian chemical companies. Slow down in China, will make more worst situation as excess capacity from china and other producing countries will find easy way to India!

Let’s wait and watch for few more quarters… cheap might get more cheaper for entry!!

Is there a way to track soda ash prices in India

Check this out

trading economics most likely provides soda ash prices trading in china, however Indian soda ash prices may have come down quite dramatically due to imports from Europe. On the other hand soda ash prices in yuan terms is still lot higher from 2021 levels on the other hand GHCL is saying that soda ash prices are the lowest as compared to last few years and may expect a turnaround…

Hence wanted to check if there is a way to track soda ash prices in India