Adding my research here:

GHCL is into manufacturing of soda ash and textiles.

Soda Ash Division- They are making light and dense soda ash (sodium carbonate). Light Soda Ash is an important basic industrial alkali chemical used in soap and detergents, pulp and paper, iron and steel, aluminium cleaning compounds, water softening and dyeing, in fibre reactive dyes, effluent treatment and production of chemicals. Dense Soda Ash is used in Glass manufacturing (Flat Glass, Container Glass, Plate Glass, deep processing to other high grade glass for example automotive glass, curtain wall glass), Silicate, Ultramarine, and other chemical industries. They are also making Refined Sodium Bicarbonate or baking soda, which is available in- Technical grade, Animal Feed grade and Food grade. Manufactured from light Soda Ash, it is used in a variety of industries like food, food dyes, poultry and animal feed, leather tanning, fire extinguisher, vegetable cleaning applications, blasting of metals, manufacture of chemicals, pharma, deodorizers and personal care products. The company is the second-largest domestic soda ash producer in India and meets around 25% of the domestic requirement for soda ash. This is a high margin business because they have backward integration with captive sources of key raw materials like salt, limestone & lignite. Soda ash prices have increased recently due to supply constraint (decrease in production in China due to pollution concerns; China has now become a net importer) and this has benefitted the company.

The higher prices will also reflect in Q4

They are doing debottlenecking to increase soda ash capacity by 1 lakh TPA as well as a greenfield capex of soda ash by 5 lakh MTPA (current capacity is 11 lakh TPA which is at 95% utilisation). Sodium bicarbonate capacity is being increased by around 60000 MTPA (current capacity is 60000 MTPA so capacity will double post capex).

For soda ash, no major capacity is coming onstream globally, so chances of price collapse due to excess supply seem slim.

Assuming demand growth of 2%, there will be an extra demand of 12 lakh TPA whereas new supply in FY23 would be only 7 lakh TPA

Even commentary from competitor- Tata Chemicals- about soda ash demand is strong:

Textiles Division - They are setting up a solar power plant of 10MW in the yarn segment (and an additional 12MW under progress). Current capacity is 185,000 spindles and they are increasing capacity by 40,000 spindles; this will increase the capacity in volume terms by 20%. This is expected to commence in June 2022. Within textiles there are two divisions- home textiles and spinning. Spinning is highly profitable and high-margin at around 29% EBITDA. Home textiles is not very profitable.

Though, management has stated that these margins in spinning segment are not sustainable.

Some of their clients in spinning:

Soda ash business is the high-margin, high-RoCE business

They are selling the home textiles business to Indo Count Industries and are doing a demerger of the remaining textiles business (spinning) into GHCL Textiles

Earlier they proposed to demerge the entire textile business into GHCL Textiles. But now, they are demerging only the spinning division while divesting the home textiles business.

Since home textiles and spinning would not be combined in GHCL Textiles entity (it would be only spinning), even the demerged entity would be having sound financials (margins and return ratios).

The process of demerger is expected to be completed in next six to eight months.

Both segments seem to be doing very well- soda ash due to demand and spinning due to increase in value-added products

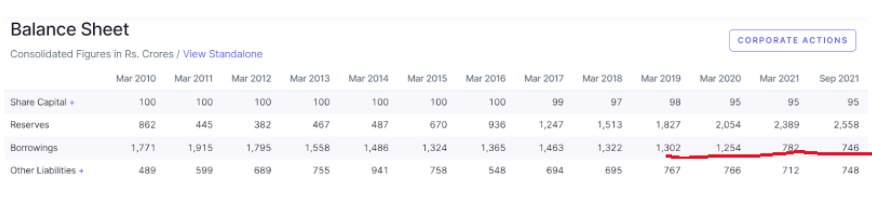

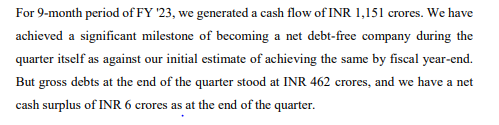

Company has done significant debt reduction:

Disc- have a position

) is why they’ve given the ratings to reduce. Selling off seems a smart capital allocation decision, so isn’t that a factor to improve the valuation multiple. Unless I’m missing out something, the stock is currently undervalued as-it-is with icing of demerger on top.

) is why they’ve given the ratings to reduce. Selling off seems a smart capital allocation decision, so isn’t that a factor to improve the valuation multiple. Unless I’m missing out something, the stock is currently undervalued as-it-is with icing of demerger on top.