GFL - Attractive Risk-Reward opportunity:

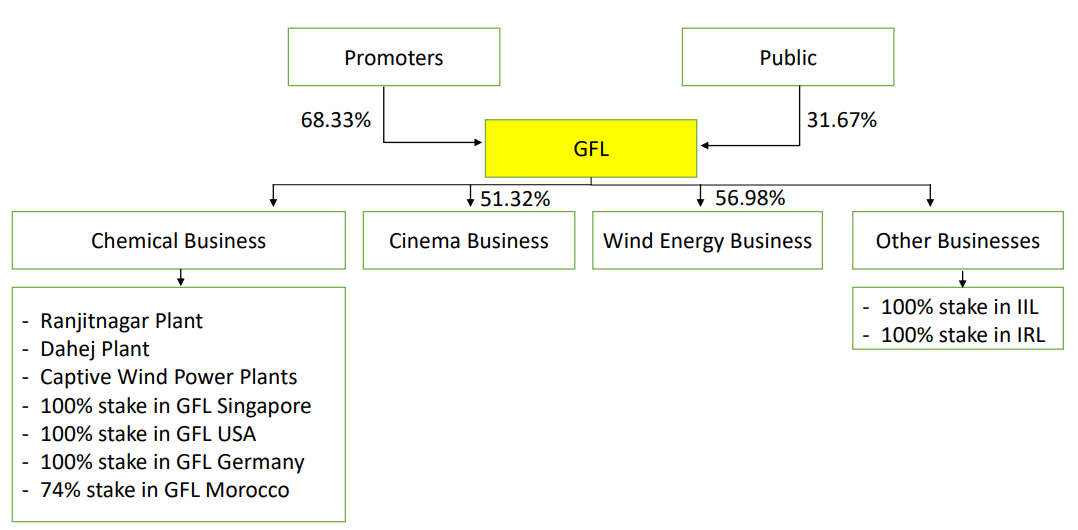

GFL is a special sit investment candidate with an extremely attractive risk-reward. As a quick brief, the corporate structure of GFL before the demerger of its chemical business was as follows:

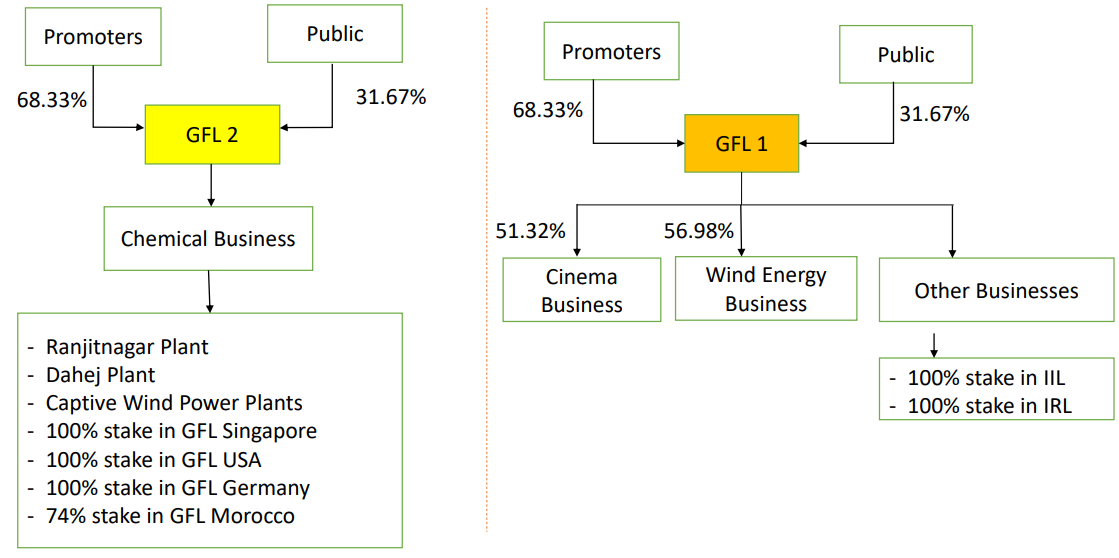

The company demerged its chemical business into a separately listed entity called ‘Gujarat Fluorochemicals Limited’ and the current demerged structure is as follows:

This write up is about GFL1. It is now primarily a holding company with investments in two listed entities of the group and doesn’t have any operating entity as such. GFL limited before the demerger of its chemical business was almost a 10,000 Cr market cap business. Now the market cap of the entity is hardly around 1000 Cr.

Hence, there has been a lot of forced selling from investors who have market cap constraints or were invested only for the chemical business. I believe this has created an extremely attractive asymmetric investment proposition.

For a company whose current market cap of the firm is approximately 1000 Cr, the company holds the following assets:

-

Inox Leisure - Listed entity (51.32% stake) - 1530 Cr

-

Inox Wind - Listed entity (56.98% stake) - 590 Cr

-

Inter Corporate Deposits with the 2 listed group firms/ their subs - 400 to 450 Cr

-

Investment in Wind Farm which they want to monetize - around 400 to 450 Cr

Hence, the total value of this entity should be somewhere around 3000 Cr (even the BV of GFL if the listed investments are MTM would be around 3050 Cr). Hence, the stock is currently trading at a holding company discount of over 66%. The firms expects ICD’s and Wind farms to get converted into cash over the next few quarters. GFL limited doesn’t have any standalone debt on its balance sheet and the current assets itself is around 50% of the current market cap.

It is not uncommon to see large Holdco discounts in India, especially in a small cap bear market. The recent changes to corporate dividend taxation should ideally reduce the Holdco discount as the tax leakage is reduced under the new amendment. Also in general this move should lead to a lower Holdco discount rate on firms with good governance and disciplined capital allocation. My interest in GFL stems from the following facts:

A.) Unlike most Holdco’s in which there is no catalyst or intent from the promoter to reduce the discount, GFL’s team has been communicating their intent to collapse the Holdco structure going forward and the demerger of the chemicals business was just the first step in this process. The group wants to simplify the structure further and provide investors their economic interest in the two listed entities directly. They are looking for a tax efficient way to achieve this objective. In March of this year, they have announced a further onward de merger in which the wind assets of the group will be demerged from GFL and separately listed under the name “Inox Wind Energy limited”. Existing GFL holders will receive 1 share of the new firm for every 10 shares held in GFL. So hopefully in a year’s time, you will have two separate Holdco’s (one for Wind assets and the other for holding the Inox Leisure shareholding). The management has indicated in public con-calls in the past that their ultimate goal or the next step is to merge these two Holdco’s with their respective listed Opco’s with minimal tax leakage. Even if the second step doesn’t happen or is delayed for some tax/ promoter control reason, the separation of the Holdco’s should lead to lower discount going forward as the Leisure Holdco will be a clear single listed equity holding firm. There is complexity in the final structure and hence it could easily take 2 to 3 years for the complete corporate restructuring to get completed. I believe that there is a 50%+ probability of a full corporate restructuring happening within the next 2 to 3 years.

B.) Also, unlike most listed Indian holding companies, GFL only has two listed entities which drive almost all the value for the Holdco and the rest is cash equivalent current assets that can be distributed back to shareholders easily. Also, the holding firm owns over 50% of both the listed entities and hence the results of the Wind & Leisure business would get consolidated into its own numbers going forward. Hence, the value wouldn’t be too difficult to uncover for any analyst going forward. Also, unlike the typical Holdco structure which has a mix of diverse monetary and strategic assets, the two new GFL Holdco’s should have clear underlying operating assets for investors to play a particular sector or theme.

C.) I have looked at Inox Leisure and Inox Wind themselves as standalone potential investments before. They are both very well run businesses and run efficiently by young management teams. They are amongst the best run firms within their industries. Inox Leisure is an extremely well run business and is a strong No: 2 in the growing cinema exhibition business in India. It has the strongest balance sheet in the industry and continues to scale up aggressively. It’s mature sites have consistently been doing 20%+ ROCE’s and the opportunity for growth is enormous. There are only 3 healthy players who are rolling up and expanding the multiplex industry in what is a traditional single screen market. Inox Leisure can continue compounding shareholder value for a long time and is a brilliant play on the Indian discretionary consumer growth despite the next 2 year headwind because of COVID related dislocation. The second listed entity, Inox Wind is also at an interesting turnaround situation. After all the mess in the Indian wind sector from the regulatory changes, the competition is more or less bankrupt and there is a strong consolidation in market shares possible going forward. Inox Wind has a good balance sheet and has survived the crisis. When they come out of this phase, there could be significant opportunities as the market is huge and growing. The supply shortages of wind turbines will provide profitable growth opportunities. The recent launch of 3.3 MW turbine, execution of its large order book and the healing of its balance sheet are key triggers. If they are able to execute their 8000 Cr order-book over the next 24 months with a healthy margin profile, then the current market cap is extremely cheap. Inox Wind at its peak was a 7000 Cr market cap firm.

GFL’s parent group has a long history of shareholder value creation and treating minorities fairly. They have always had a huge aversion to debt and most of their businesses are debt free and asset rich. The young scions of the group have incubated new businesses in different segments with large opportunities and have scaled up well. All the group’s firms are either No:1 or No: 2 in their respective industries and have focused always on operating efficiency and profitability. Most of the issues in the group’s businesses seem to be from the industry level headwinds and very few self-inflicted damages.

Hence, I see multiple ways to win in this investment. Of-course the best case is that the corporate restructuring leads to no holding discount. Or else, just that the holding company discount narrows over time as the value emerges with the yearly results. Or else, the two underlying two businesses continue to compound in value and are much bigger entities 3 to 5 years down the line. Hence even without a change in discount, I get my 20%+ returns purely from underlying value growth. Or else I hope the cash and ICD income is being used for dividends, allowing us to wait for the restructuring.

The real risk in this investment is if the promoters allocate capital badly going forward and destroy value or if the wind energy business takes much longer to turnaround, sucking up even more resources of the holding company. Also, the risk is that the current creation of this two Holdco structure through demerger is primarily because of the split in the family and hence no final collapse of the Holdco’s with their respective Opco’s. Even accounting for these issues, I think the Risk-Reward in this investment is extremely favourable for investors and hence we have been accumulating its shares for a while now with a lower average acquisition price than the current market price. While the daily trading volumes are low, there are blocks available from forced sellers and we have been able to accumulate around 2.5% of the firm. Since all the four listed entities of the group have detailed disclosures, earnings transcripts and annual reports, diligent investors can analyze the underlying businesses or promoter background and ascertain if they themselves standalone are attractive investments.

Disclaimer - I don’t have any research analyst or investment advisor certification from SEBI. I am clearly biased on this name because of our existing investment and we could sell shares at any moment and not inform this forum members of the same. So please do your own research or consult with a SEBI registered advisor. I haven’t spoken with the management or met the team of GFL and hence all the information is from the public domain. I or my firm haven’t bought or sold GFL shares over the last 3 weeks.