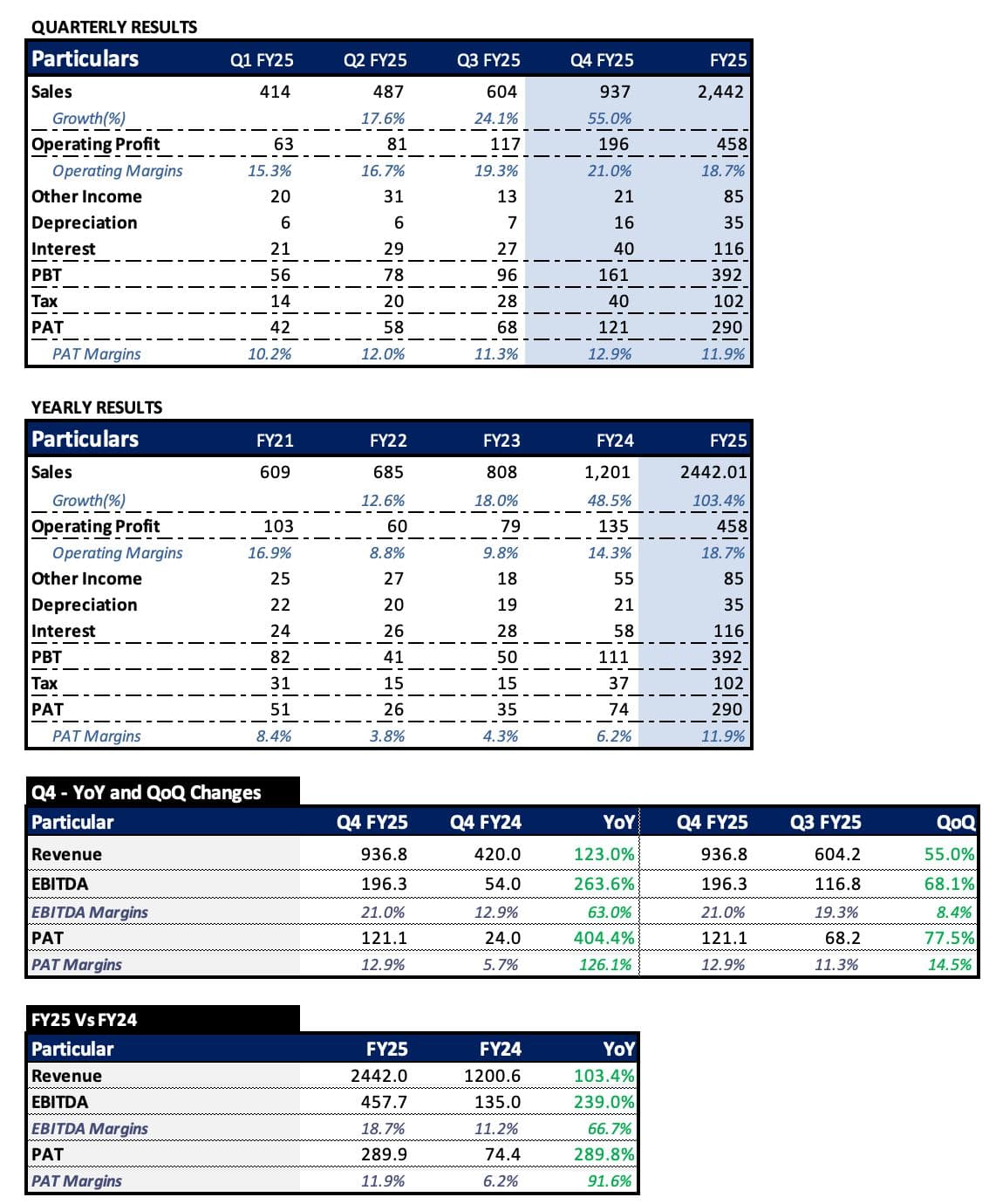

Management has given revenue guidance for FY25 at Rs. 2,500 crores. Company has done 1505 Rs in 9M FY25 & 604 Cr in last Quarter, company has to done 1000 Crores revenue in Q4 to achieve the guidance.

For FY26, the company expects a revenue growth of 30% to 40% over FY25, indicating a potential revenue of Rs. 3,250 crores to Rs. 3,500 crores.

The company reported one of its best EBITDA margins in Q3 FY25 i.e. 19%, but management emphasizes maintaining an average EBITDA margin of 15% to 16% on a yearly basis.

The monthly smart meter installtion numbers of Jan-25 and Feb-25 are clearly more than 50% of the average monthly installations of the last quarters. So there is every possibility of Genus achieving the guidance. Below is the number of smart meters installed data of Genus power which I tracked from the website over the months:

An update on how fast the installations are happening in FY26. As seen above, on average Genus was installing close to 4.5 lakh meters in the months of Dec’24 to Feb’25. These numbers have gone substanatially higher. Let me give you the numbers from the portal of Apr’25 and May’25:

It is giving a clear signal that Q1FY26, they will do average installations of atleast 12 Lakhs which is close to 2.5x compared to the average monthly instllations of Q4FY24. As I project Q4FY25 to be a blockbuster results for Genus, Q1FY26 will unleash it as the market leader in Smart metering installtion. Really excited to grow with Genus in this journey.

(Note: The numbers on the portal, filtered with Genus name, gives not only the data of projects where genus is associated as a AMISP but also where Genus partnered with entities like Adani, Intellismart, etc. So the above numbers and previous numbers may not be solely of Genus’s installation but only shows how substantially the installtions are increasing)

These are overall numbers and not just Genus alone, right? Hard to decipher Genu’s growth given these are aggregate numbers but I guess a rising tide lifts all boats

A lot of orders are govt orders;I don’t think there is much scope for improvement in cashflows;Unless they pressure the govt;But they can’t due to the massive orders;

With Genus Power the question is they have order book of 30k cr to be executed in period of 8 to 10 years and management tells around 60% will be executed in next 3 years that is 18k. Another 12k in period of 7 years. That means after 3 years order book for smart meter is not growing means their growth can slow down. Looking at their business model where they sell meters to platform which is acting as a AMISP who wins order from DISCOMS and then give order genus. So technically when smart meters become operational that’s when Genus start to receive money. So i believe that for genus, based on their business model it becomes crucial in execution of existing orders without hiccups so money start to come in & to win more orders going ahead to justify the valuations. If order book start to decline or become flat that can impact heavily they start face immediately 2 problems one is higher receivables and second is debt. Also they need to improve their efficiency because they have avg total asset of 3000+ cr and has asset turnover of 0.65 while the competitor with 2000+cr has asset turnover of 0.86.

Is there data around which say’s that out of total meters installed in India, how many are currently smart meters (already installed as of date) and for how many smart meters the tenders have already been awarded.

I am sure that total installed smart meters and smart meters where tenders are already awarded would constitute for more than 50% of the total energy meters in India. Smarts meters would majorly be in Tier1 & Tier 2 cities only. We would have Tier3, Tier 4 & Rural area’s yet to be covered with smart meters.

Data from google as of December 2024:

Sanctioned: 222.3 million smart meters were approved for installation.

Awarded: Out of the sanctioned meters, 134 million have been awarded.

Installed: As of December 2024, around 18.5 million smart meters have been physically installed on consumer premises.

Target: The Revamped Distribution Sector Scheme (RDSS) aims to install 250 million smart meters by March 2025.

Lagging: Some reports indicate that the installation pace is slower than anticipated and that only 7.3 million smart meters were installed by November 2024.

===============

National Smart Grid Mission - Ministry of Power, Government of India

Sanctioned: 223.7 million

Installed: 32 million

Balance: 191.6 million

I could not find any data on total number of meters awarded on NSGM website.

Also, I could not find any data on total number of Electricity meters installed in India.

Also, once smartization of electricity meters happens, there may be a market getting primed for smart Gas pipeline & smart water meters, this again will give work for smart metering companies for another 3-6 years.

I worked for Landis+Gyr 10 years back which is one of the bigger players in smart meters in US & Europe and they have considerable deployment in India too. They had smart water and gas meters for US & Europe 10 years back too.

was wondering about that too; once the meters are installed, there isn’t much to do apart from 1-2% failure rate replacement. what next?

Gas meters, the CGD network already in place, MAY need to have the meter changed but network itself is not huge so far. that is, CGD penetration is quite low.

Dont see how this bull run will continue after 2-3 years for smart meters

Agreed in next 3 to 4 years if everything goes well smart metering for electricity may mature and genus will concentrate on water meter/ gas meter. But we should also consider that the model in which genus operate is BOOT model. So money coming is like a rent. So if any delay from discoms, their will be delay payment from both end for Genus from the platform and also from the discom. In such case company is exposed to more risk and valuation multiples may not justify even when growth numbers are high or return expectation become higher.

Above is from Genus’s concall. As per them less than 50% of electricity smart meters have been tendered till now.

From what is already tendered, they still have deliveries / installations to be made for about 16000-18000 cr, which will be cleared in next 3 years. So we can assume the remaining 55% (not yet tendered orders), will last them 2 years or so. So we can see them being busy (full) with electrical smart meters for atleast 5 years from now. I guess that’s a decent runway for sure shot visibility of revenues and will give them ample time to strategize on what’s next?

120 million meters yet to be tendered is pretty big. If Genus gets a third of it, or even 20% of it direct bid and another 10% whitelabelled for other vendors, it’s 30-35 million meters. decent numbers then

Evaluate in terms of peak rev, peak ebitda, peak margins. Markets will price in for that peak scenario few years ahead. Post that p/e will compress as performance gets better. Not much terminal value for this business in current form, so assigning consistently high multiples is not smart.

Also consider competition creeping in and margins compressing because of the same.

Also note that all these tenders are fixed price, so any big turbulence in rm prices can result in margins taking a hit.

Genus in concall said 27% market share, so let’s say they maintain 20-22%, so I think they will peak out at about 7000-8000cr revenue per year.. for FY 27-28-29. Which is about 3x from current revenue.

Current PE is 36, they may maintain similar or a bit more PE for next 2 years and then PE may come down to 20-25 if there are no other avenues found for next phase of growth in next 2-3 years.

Profits (PAT) at Peak may be 800-950 cr per annum. Even with PE of 20-22, it may give a valuation of 17500-20000 cr and valuations may remain at 35-40 for next 1-2 years and then have slow fall if they dont talk of visibility of additional streams of revenue to maintain atleast 20% growth post FY2017-18.

So we may see interim valuations between 23000-26000 cr.

Why I think they can maintain more than 15% revenue growth even after 2027-28:

They are coming up with Gas and Water meters too, which they are saying will start getting revenue after 2-3 years.

They are exploring (and doing trials) with Discoms abroad, order inflows may start coming from there after 2-3 years.

If we say the industry will see degrowth in 3 years from now, then very rare chances of new competition coming in.

Current numbers that we are speaking about, was the target set for smart meter installation by government 5-6 years back. I am sure total number of electricity meters installed in India are 2-5x of what will be smart meterised by 2030. So we will see bigger targets coming from government… the pace for installation of smart meters may not grow at 30-60% what Genus is targetting right now, but there will still be new tenders coming out even after 3 years from now.

Currently maintenance / support order book is about 13000 cr to be earned over 8-10 years, so about 1300-1400 crores per year. We assume out of remaining 55%, they get similar maintenance & support order book, so we can see about 2500-3000 crores per annum from these maintenance alone (not sure what will be EBITA contribution here). So, they would not have to do much heavy listing to maintain a revenue of 7500 crore per annum, which may translate to PAT of 600-800cr on conservative basis. Even if they get a PE of 15, we will still see a valuation of 10000 - 14000 cr.

My guesstimate on revenues and PAT for next 5 years (Pessimistic case):

Year Revenue PAT Average PE Multiple

FY25-26 4000 500 40

FY26-27 6000 750 35

FY27-28 7500 900 30

FY28-29 8000 900 25

FY29-30 7500 800 20

Optimistic case:

Year Revenue PAT Average PE Multiple

FY25-26 4000 500 40

FY26-27 6000 750 35

FY27-28 8000 950 35

FY28-29 9500 1100 30

FY29-30 10000 1200 25