After listening honest acknowledgement of their mistakes by management, I have invested today in Gensol. I had missed 2-3 years ago due to sudden rise in its price. Fortunately, I didn’t chase it that time.

Best part of their business, it is scalable and promoter are willing to scale up.

Promoter Share Sale to Reduce Pledged Shares and Boost Stability

Ahmedabad, February 18, 2025:

Gensol Engineering Limited (BSE: 542851 | NSE: GENSOL), a leading player in the renewable energy and electric mobility sectors, wishes to assure investors of its financial fundamentals and continued commitment to long-term growth following a strategic share sale by its promoter. This transaction represents less than 1% of the total promoter shareholding.

The recent sale of 2,15,000 shares by Anmol Singh Jaggi is a strategic step aimed solely at reducing the quantum of pledged shares, thereby reinforcing the company’s financial stability. This transaction will significantly reduce the promoter’s pledge and move the company toward its goal of becoming pledge-free. The shares have been sold to reputed long-term investors.

Commenting on the development, Mr. Anmol Singh Jaggi, Chairman and Managing

Director of Gensol Engineering Limited, stated:

“The decision to sell a portion of my shareholding is driven by our commitment to make Gensol a pledge-free company. The pledged shares primarily served as collateral for long-term debt for our EV leasing business and Loan Against Shares. This transaction will partially repay our LAS

lenders and reduce our pledge levels. All proceeds from this share sale are being directed toward the reduction of pledged shares. We remain steadfast in our growth plans and confident in our long-term value creation for all stakeholders.”

As of December 2024, the total promoter holding stands at 62.66%, with 81.7% of this stake pledged. This implies that approximately 51.19% of the total equity is pledged.

To put this into perspective, a 51.2% pledge corresponds to ₹1,000 crore of the company’s valuation. A recent reduction of ₹33 crore in pledged shares translates to just 0.033% of the total equity, which is relatively insignificant in the larger picture unless there’s an alternate way to interpret the calculations.

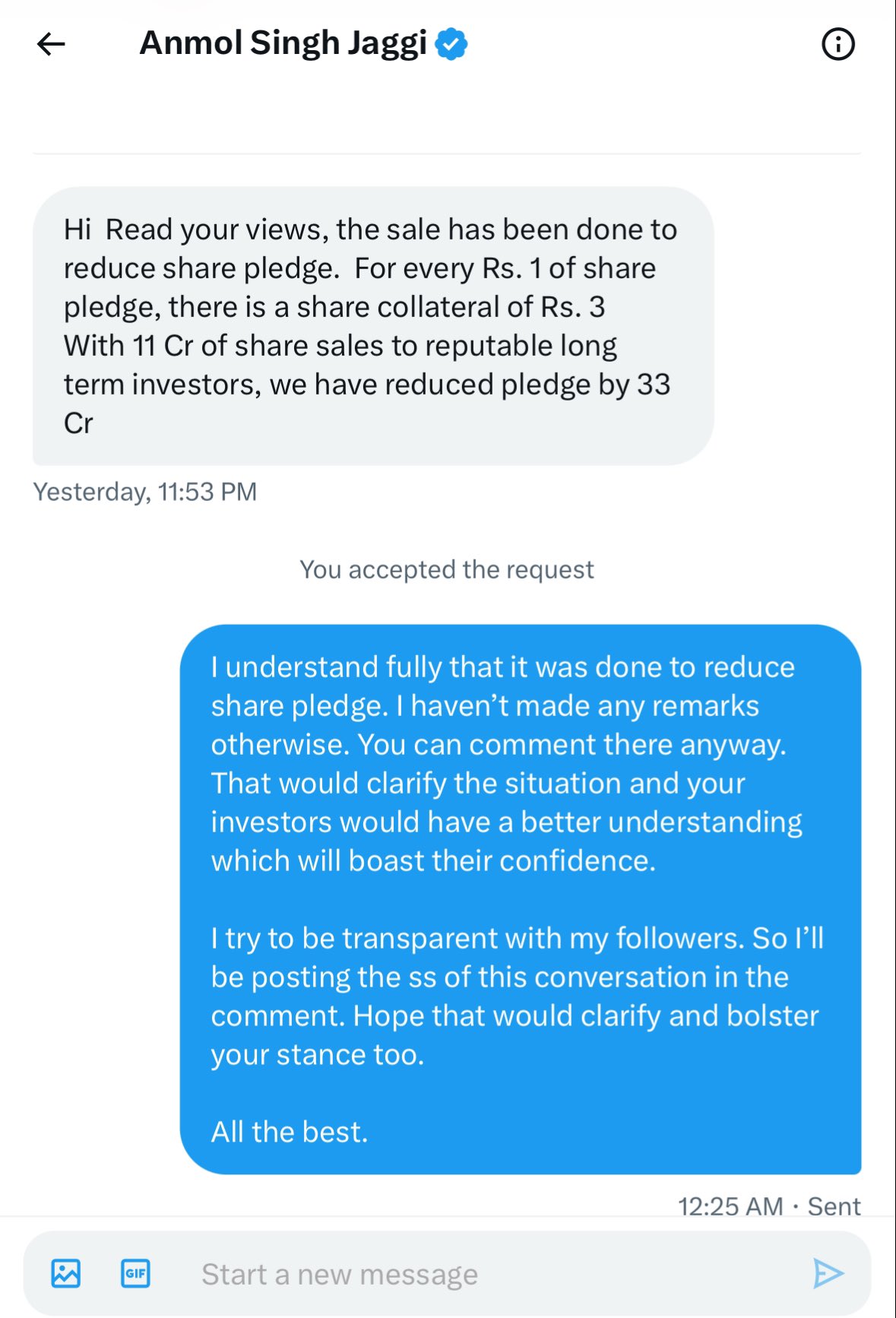

On another note, a screenshot circulating on Twitter raises some doubts. Why would the promoter of a ₹2,000 crore mcap company directly DM a user with just 12K followers over a post that received only 350 likes? This seems unusual and raises questions about the intent behind such an interaction.

From a financial perspective, the company’s Debt to Equity ratio is 2.33, indicating a heavy reliance on debt. Given this leverage, a significant portion of earnings will likely be consumed by finance costs, limiting profitability and growth. Moreover, the high pledge percentage adds another layer of risk.

Disclaimer: Not invested, just analyzing the business to determine if it’s a worthy investment.

Mr Jaggi is quite active on twitter and you will find him interacting with various handles irrespective of the followers count. If I am not wrong he had DM’d @Vineetjain111 too recently. If you read the whole twitter thread, the user was making a comment on why he sold his shares which he clarified via a DM. Personally would have preffered if he had replied directly to the tweet instead of a DM.

A promoter who is reachable on twitter and ready to response to criticism should be encouraged and not questioned. There are so many managements out there who wouldn’t even reply to your emails, let alone tweets.

The IR head of Gensol also reached out to me separately and I spoke with her briefly this morning. They are clearly making attempts to share more and improve sentiments. While she said there is no margin call scenario, I find that hard to believe with the big fall in the shape price.

If some of you want, I can request her to scheudle a call over the weekend to answer any questions.

In a interview gensol ceo mentioned that they are building a BALANCE OF PLANT but no announcement to investors by promoters about this topic.( Interview link is given already)

Gensol engineering signed a whopping 4 thousand crore inr MOU i again repeat 4 thousand crore inr MOU with Maharashtra government but no announcement to investors

My investment thesis is simple their solar EPC order book is 7000cr with one more 1000cr to be announced soon that brings us to 8000cr of order to be executed in next 15-18 months so even with 7-8% PAT that comes to 600cr + PAT

Once implemented bess should give 50cr PAT on recurring basis as now battery proces are 30% more down than their bidding price

EV manufacturing should also scale in a positive way in next 3-4 years as they have support of blusmart to get feedback and correct themselves

Any counter thesis on above calculations is appreciated

A lot of things have to go right for this to play out.

The entire order book getting imolemented in 18-24 months is very inlikely IMO. The EPC revenues in FY25 will be arounfd 1200-1400cr or so. The jump to get to 3000cr per year is large and wil need a lot of resources for working capital which they will find hard to secure tiven the high debt and low valuations for equity raise. Execution will be tested in the next two years.

Not sold yet. As of now, Gensol has just has signed a non-binding Term Sheet for an INR 350 crore strategic transaction involving the sale of its US subsidiary, Scorpius Trackers Inc.

I think once they sign the agreement they need to execute the projects with in time line like 15-18 months as per agreements unless it’s delay with client like land clearance etc

So I think they will execute this order book of 7000cr at any cost with in this next 18 months and thats the reason they are aggressively deleveraging ( selling leasing assets and scorpious ) and building their working capital

Agree they have high debt, loose talk by promoter who misses guidance and many other issues and they why stock price is beaten down

But I am betting on recent changes they did like brining Shilpa from sterling and Wilson to head their solar EPC biz and this change is already working as they are getting bigger orders compared to competition

and we just need to track if these orders are converting to nos with proper execution

I feel Mr. Anmol is changing. While many were upset of the lack of guidance, it’s good that he just didn’t say something like 2000 cr will be achieved 3 months later or something. And their intent to deleverage is showing. The US operations for Scorpius makes sense given Gensol’s India focus. I never liked their EV leasing business and that should have been reason for me to exit but here I am … but now it seems that they are getting on the right track. And the Scorpius returns are pretty good too given what it was acquired for as you said.

PE is one of the important factors in buy/sell decisions (among others). But, here there is almost 50% difference between low figure 16 and a high of 28. I understand about coming to a different number based on using TTM vs latest quarter x 4 vs last full FY.

But, if someone who is used to seeing BSE site and basing their opinion might be tempted as PE is mouth-watering 16 for a company having past performance of 52% CAGR in profit over 5 years. Whereas if I consider its PE to be 28, it might be only modestly interesting.

Thoughts?

The CMP is Rs.569 on NSE 25-Feb-2025 with slight difference in other sites.

(my first post on ValuePickr)