With this company, it appears “A new announcement a day to keep bears away !”.

Only a curious bystander. No investment.

With this company, it appears “A new announcement a day to keep bears away !”.

Only a curious bystander. No investment.

Due to Rating downgrade, it is in lower circuit. Rating downgrade is mainly due to not paying properly overdues by Gensol. Source: Disclosure on Exchanges

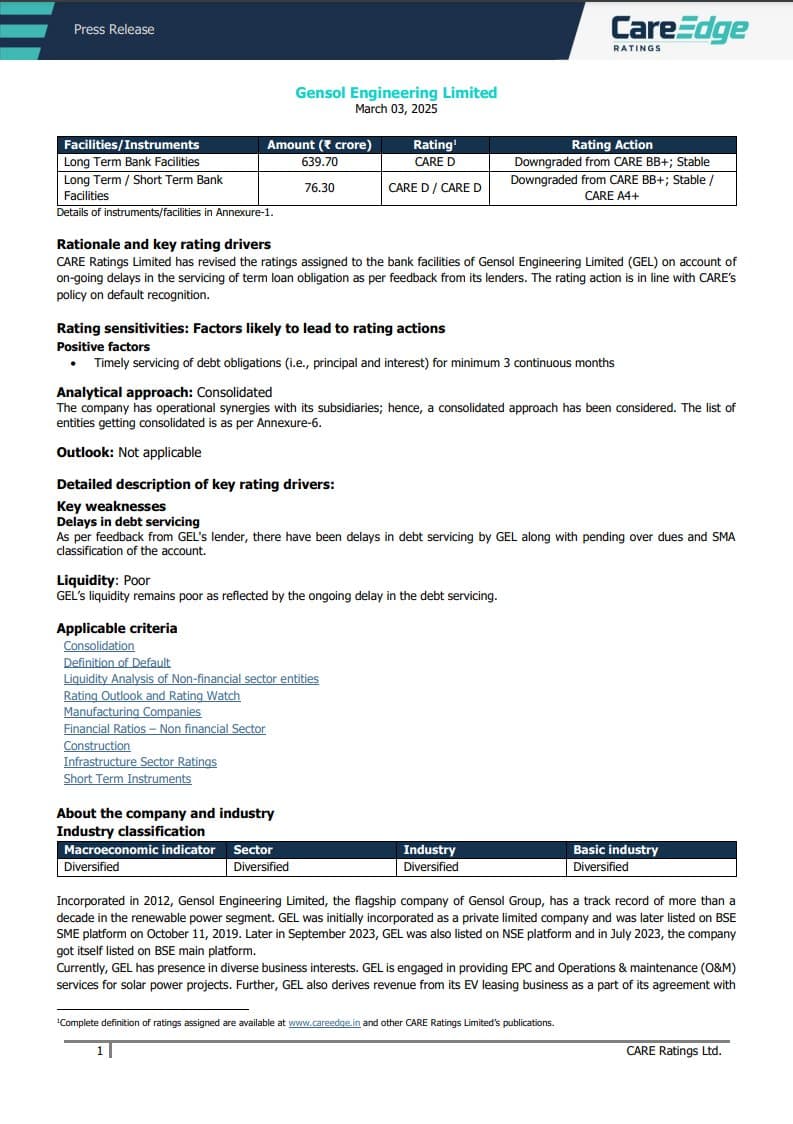

CARE Ratings downgraded Gensol Engineering Limited’s (GEL) credit rating to CARE D, meaning “default”, because the company has not been able to make payments on time for its loans.

What I understand is:

a. * Loan Payment Delays: The company failed to pay its term loan obligations as reported by its lenders.

b. * Liquidity Issues: Gensol is facing cash flow problems, making it difficult to meet debt commitments.

c. * SMA Classification: The company’s bank account has been categorized under “Special Mention Accounts” (SMA), which means it has missed payments and is at risk of becoming a non-performing asset (NPA).

d. * A CARE D rating indicates that lenders and investors may see Gensol as a risky borrower. * The company may face difficulties in raising new loans or investments at favorable terms.

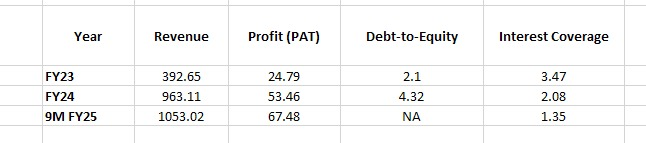

Debt-to-equity has doubled (2.1x to 4.32x), meaning the company has taken on more debt.

Interest coverage ratio has dropped (3.47 to 1.35), indicating lower ability to pay interest.

Now the margin calls wll begin; the fall going forward can be very severe as brokers will offload without looking at the price. Don’t catch a falling knife…

Looking at today’s sell orders.

Seems brokers / lenders are triggering the sell orders.

It’s a painful journey for the ones who have had already invested.

Looking at the downgrade by CARE to ‘default’ rating, questions will arise of the firm continuing to be a ‘going concern’. Company is not paying its interests on time, has huge cash flow/liquidly issues, debt to equity is very high and the promoter has pledged shares. Looks like a single-digit penny stock soon.

Hope you are not holding the bag on this. One should not be very exuberant on such firms

Todays volume on both exchanges is just 10 lacs; shares pledged by promoters are upwards of 1.7cr I believe. Long way to go…

Not all lenders would rush to offload.

If jaggi has provided some additional collateral with some lenders, they will back off from selling.

Holding heavy losses, there was always a concern of pledging and high debt.

But somehow got sucked in projecting future earning for couple of years and the valuations.

But lesson: there is no value at any valuation for the some scripts.

Disclosure : holding and looking to get out when exit is there, No recommendation

Yes, I think this is on its way to be a penny stock. If invested, get out when you find a buyer at some price. This is likely to hit a series of lower circuits to a penny stock

Feel sad for those who are holding the bag on this.

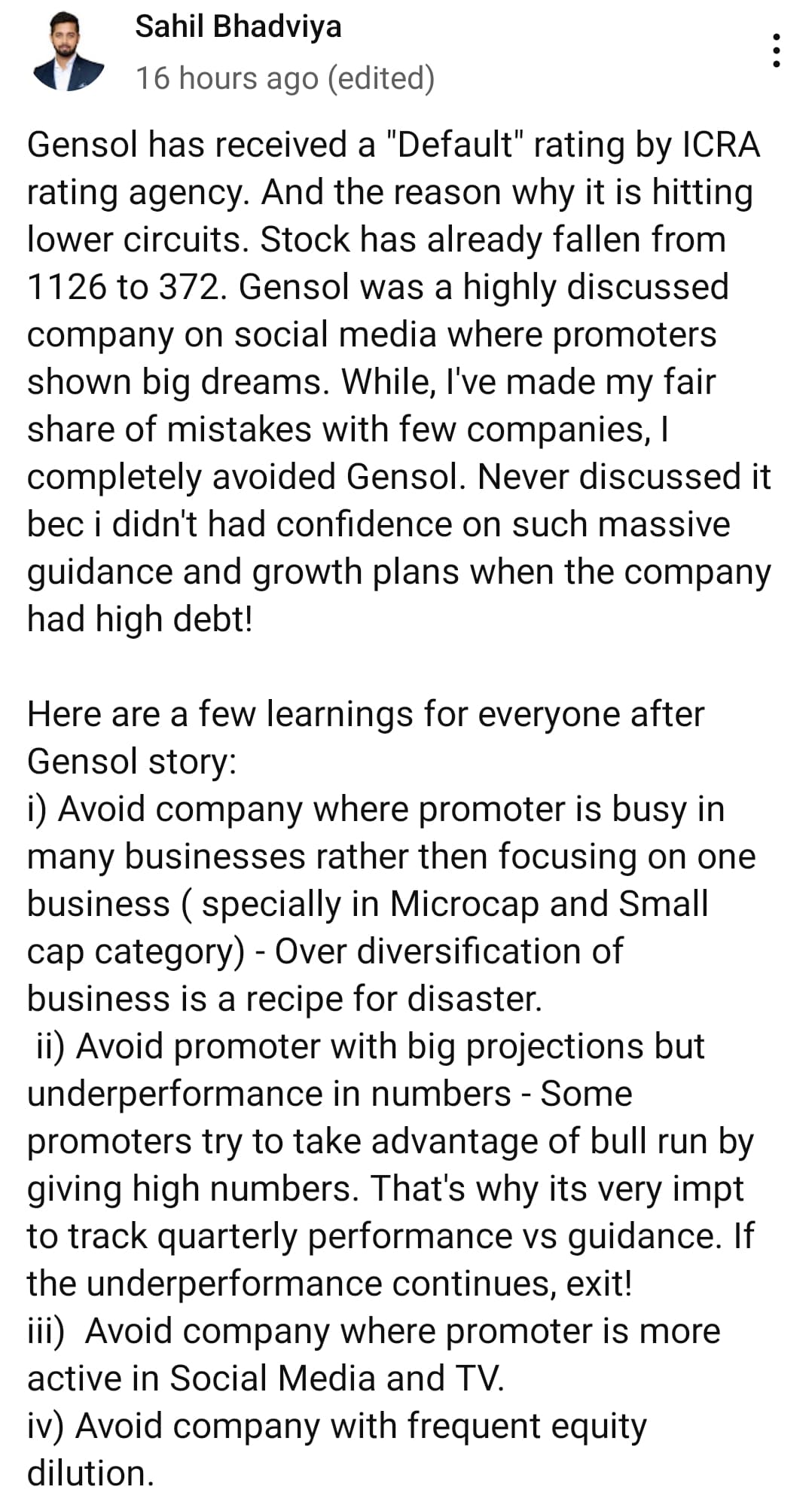

This is what I wrote about this stock last year when hype around it was at an all time high. This should be another lesson to retail investors to be suspicious of all good stories that small caps companies tell their investors whether their big order book, capex expansion or rosy prospects.

There were enough hint in the Q3 concall which lead me to believe that there was no cash left.

Booking loss in this time was relatively easy ![]()

Thought of mentioning it here but not wanted to spread anything negative without knowing the fact ![]()

Very similar thought process. The writing was on the wall. Booking small losses is key to long term investing success.

https://x.com/vineetjain1101/status/1896883278092616048?t=r3kjIT1jOBw6xrlRjXIIGw&s=19

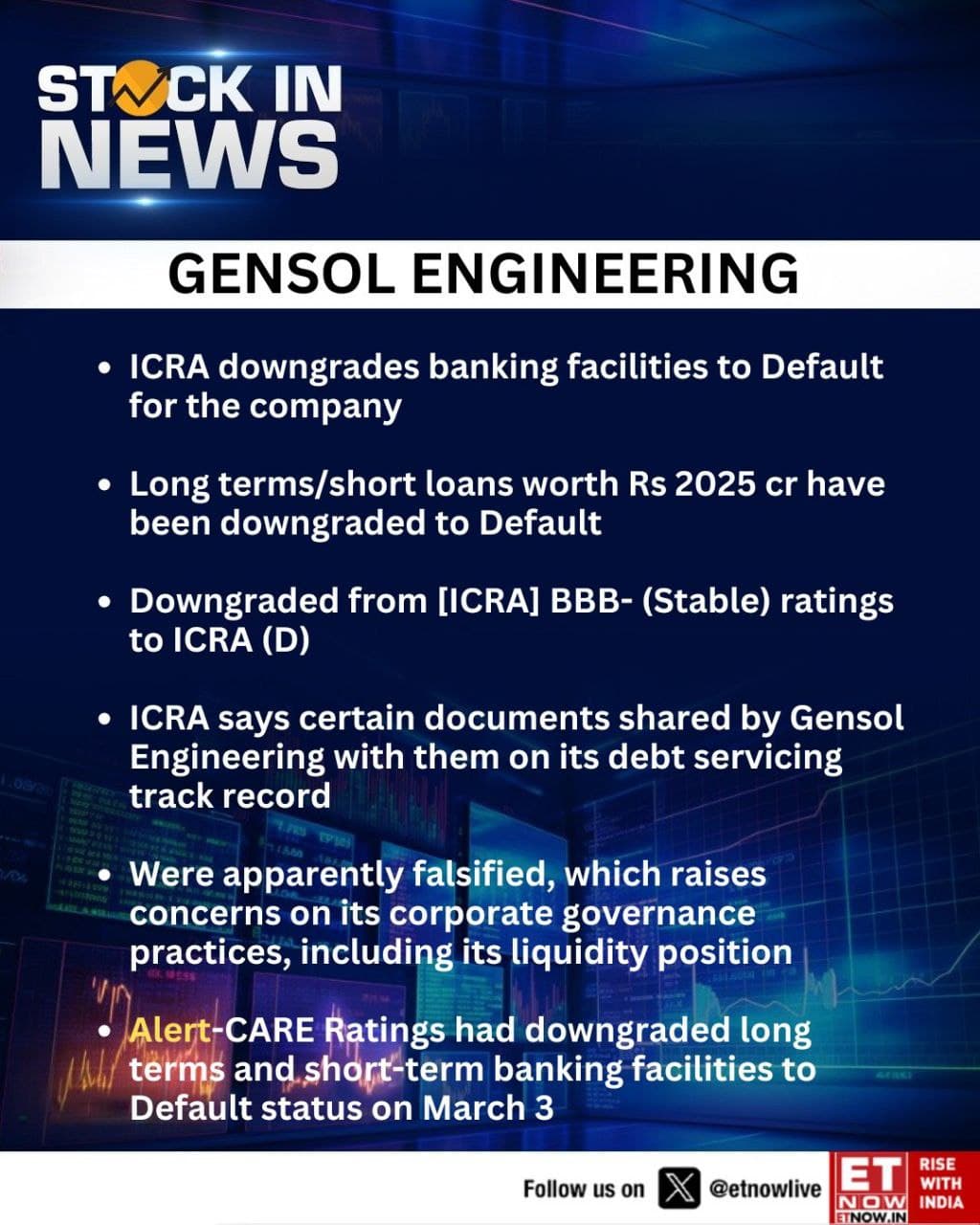

Debt Servicing Record is falsified. This means it is not a case of hubris and too much ambition. It is a clear case of fraud.

Note: Never even considered investment in this one.

I mentioned last year amid the hype surrounding the stock that biggest flag I saw in Gensol was heavy debt raising against their stocks. The deep corrections in market over last months may have also contributed to what is unfolding. When management doesn’t have money to pay off their debt bad things happen.

I think the biggest mistake gensol did was venturing into the ev vehicle manufacturing (new business ) with such high debts.

They could have sailed through easily with their epc business and market would also have rewarded them with earning multiple premiums solar companies are enjoying.

It’s quite sad to see such promising companies facing financial ruin.

9657ece5-7469-4d60-8ac2-f732e7b44713.pdf (358.7 KB)

GEL denied fake documents claim of icea

Has the asset divestment been completed or they are just planning to do it? If they haven’t then they need to find buyers. Merely saying that we have initiated the process does not bring in cash to repay debt. You need the actual sale and we know that its tough. Their statements cant be considered as reliable. In the past as well they over promised and under delivered.

They have signed an agreement with Refex on the sale of 2,997 cars for 315 Cr. They also signed a term sheet for the sale of Solar Tracker subsidiary (without Solar IP rights for India, which was good) for 350 Cr. (to be paid to Gensol in two tranches by March 2026). I am unsure if they have sufficient Working Capital to execute the huge amount of EPC orderbook in next 18 months or if they will find short term loan facilities for working capital requirements. I believe if they are able to execute the projects well this year and the divestments go as planned, they would be back on track again. Depends if they currently have / would find sufficient liquidity for the EPC executions.

Disc.:

Invested, given the growth prospects and the issue only seems short term liquidity, which I think they should get given there huge order book. No existing lender would want to unnecessarily force liquidation, if in the worst case scenario the debt can still be restructured so the some repayments are formally postponed by the lenders i.e. government owned power development financial institutions aiming to promote and support renewable energy development (majorly IREDA and PFC). Nervously hoping for the best…

To my best of knowledge where i work as client of solar epc contractors…having done small plants.

Its human to be hopeful on investments ( all kind of investments monetary as well as non monetary)

All things aside, a default is a default, doesnt matter what caused it.

In my short experience with direct equity i feel, short term, the capital deterioration shall persist untill they raise money and payback. ( if there is a chance to avoid further deterioration why not take it ?)

I am mostly good at selling when stock hits much lower levels and losses.

D- No investments.

Good points on when to be cautious about companies making huge promises without a decent medium/long term track record.

Personally was always suspicious about this company and still feel there are a lot of skeletons to tumble out from this one.

For now they have denied the falsification claims officially but personally I’m not convinced.

Disclosure: not invested