Gayatri Projects is primarily into roads and irrigation construction activity and has an order book of over Rs 10,000 crore.

The Company executes civil works, including roads, canals, airport runways, ports and harbors, dams and reservoirs, and railways across India.

The Company has presence in engineering, procurement and construction (EPC), and construction of road, irrigation and industrial projects across India. The Company holds interests in infrastructure, power, hospitality and real estate industry. The Company has executed projects, comprising approximately 5,094 kilometers of roads; approximately 1,200 kilometers of irrigation canals, and various industrial projects. The Company’s subsidiaries include Gayatri Infra Ventures Limited, Sai Maatarini Tollways Limited and Gayatri Energy Ventures Private Limited.

Rs 675 crore order from the NHAI for 6-laning of Eastern Peripheral Express Way in Haryana and Uttar Pradesh.

4-laning of National Highway(NH)-233 on Ghaghra Bridge-Varanasi section in 4 stretches amounting to : (Aug 26, 2015)

Rs 741 crore

Rs 785 crore

Rs 986 crore and

Rs 806 crore

Rs 4744 crore freight corridor contract (2 March 2016)

Rs 175 crore from Hyderabad Growth Corridor Limited (26 March 2016)

Rs. 340 crore road project in Nagaland (11 April 2016)

Rs 700 crore from CIDCO as part of navi Mumbai International Airport (20 Jun 2016 )

Triggers:

Trading at PE of 29 which is still reasonable

May get irrigation canals project

Cons:

Stock is trading at 2.95 times its book value

Company has low interest coverage ratio.

Promoter’s stake has decreased

The company has delivered a poor growth of 5.03% over past five years.

Company has a low return on equity of 7.12% for last 3 years.

Contingent liabilities of Rs.9616.58 Cr.

Promoters have pledged 90.37% of their holding

Disclosure: Invested as I was bullish on Modi govt for infra, it has already had a 10 bagger runup in last two years not sure if it makes sense to hold it further. Views welcome.

anyone still tracking this stock?

as per the new guidance for NHAI (highway construction funds).

i thought this could be a good best.

hence anyone tracking this stock can through light on he same.

Hi Radhika, sorry just saw this question. NHAI orders have increased sharply. Gayatri should also benefit from this being a pure EPC play with 70% orders in roads

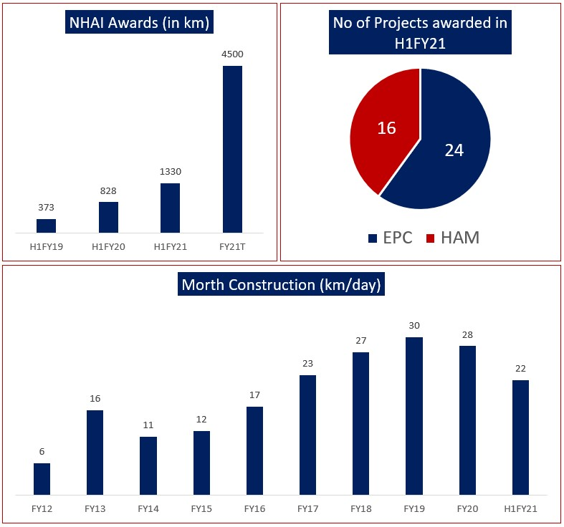

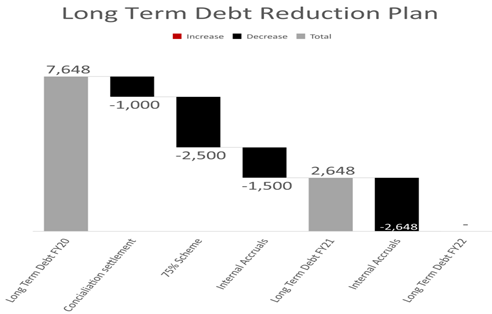

Gayatri Projects posted strong results with revenue up 14% and EBITDA up 7%. The company has returned to Profitability with this performance. It’s order book remains strong with book to bill ratio of 3.7x. While the company is guiding for Rs3500cr revenue but a closer look at the status of it’s orders suggest that probably it can do closer to Rs5000cr topline. Company is also guiding towards becoming long term debt free in next 12 months, Appears to be a strong turnaround in company’s performance. The stock has corrected from peak of 225 to now 24. The full presentation is here https://www.goindiastocks.com/GIA/downloadReports/70

Conference call is also there today at 11AM, dial in 7550004474,

Gayatri Projects have repaid Rs208cr of debt amounting to 27% of long term debt through monetisation of it’s arbitration awards. This is first among the plan to repay the long term debt fully in next 12 months. Mkt cap is Rs600cr and if they repay total Rs750cr long term debt, could be a good trigger for stock.

Source: Down but Delivering...

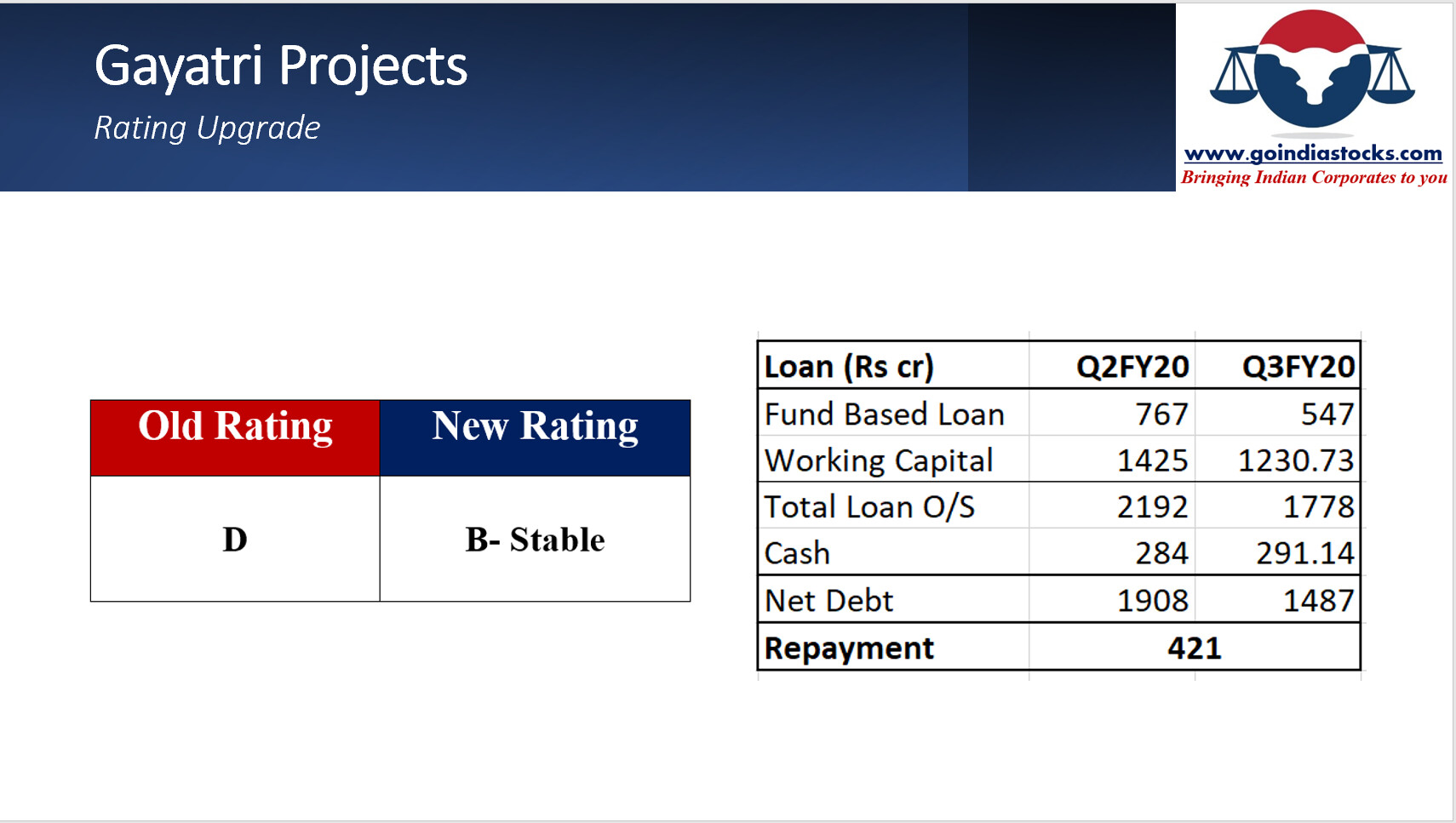

Credit rating was revised to D as on 28.2.21. As per care the revision is due to stretched liquidity position of the company. What has happened in such a short span that care has decided to revert credit rating so fast. Adding to it choice finvest pvt Ltd has invoked 200000 shares of the company pledged by Indira Reddy for personal borrowing purpose due to non payment of interest. The promoters have pledged 97.3% of their holding. One of its subsidiaries for which the company has given corporate guarantee has defaulted on payment of dues as per quarterly results.

Company has announced that it will repay long term debt in 12 months. Order book looks good. 29% of the projects are concentrated in Uttar pradesh. Usually q4 is a strong quarter for infra companies. It is to be watched whether the company is able to walk the talk in terms of retirement of long term debt. Company has done well to monetize some of the assets last FY. In addition to good execution timely realization of receivables will also be a key factor to watch out for. As per the company most of their jal jeevan projects are tied up with central funding which may help them in keeping the receivable days in check.

So the biggest concern about the company for me is servicing of debt and promoters pledge. So if the company comes up with strong credit repayment in the coming quarters, may be it can be an interesting bet

Anyone has a good view on what went wrong with this company?

We tend to discuss often why a company is doing good or but seldom discuss what are traits which will make companies poor investments. Can help to avoid landmines?

A seasoned investor had mentioned that L&T barely manages to make money in EPC and everybody else looses money in long term (not referring to stock price here).