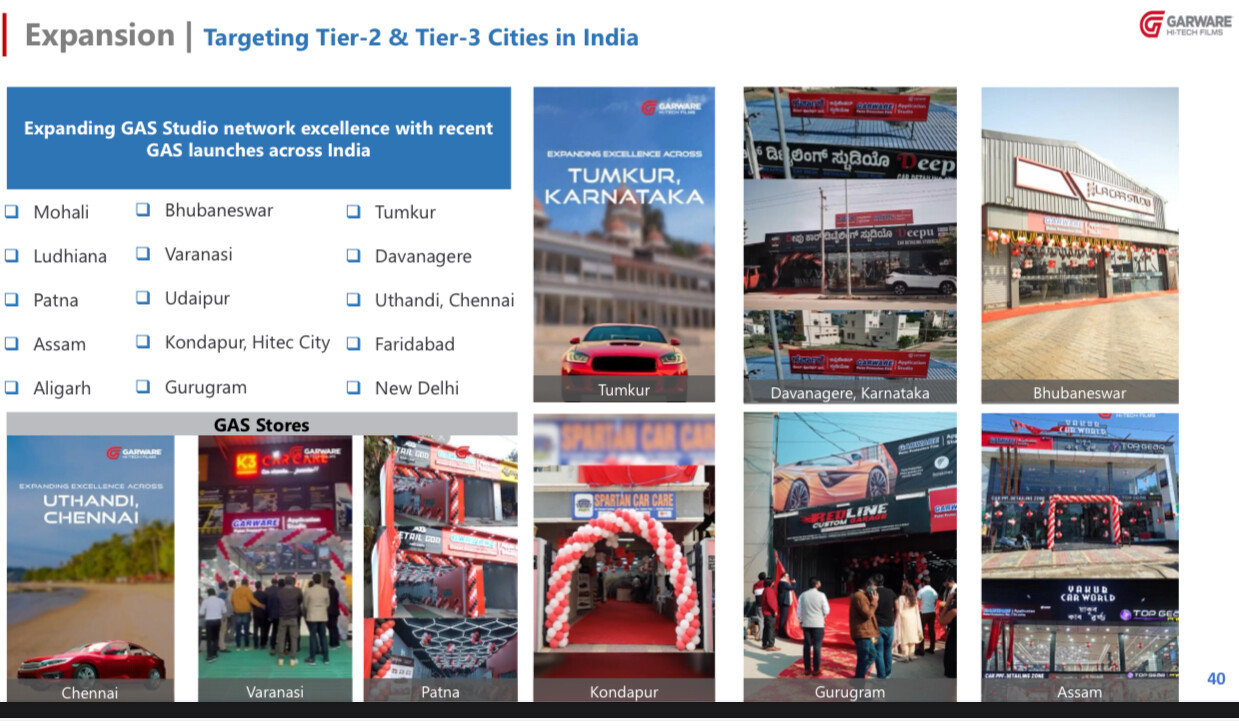

The company has said they will continue to add more than 200 application studios( initially they were supposed to go from 160 to 200 but seeing nice demand they will expand further)

cash reserves stand at 544 cr and 0 net debt

The new plant of ppf will be operational from Q2 FY26, this quarter ppf was running at 135% utilization, and scf us running at 100%.

added 5 new regions/international countries (that is why volume growth is seen in this quarter)

with colored ppf coming and titanium ppf , the ppf segment of the company might take market from 2% to 10% level( 5 times of current).

Despite Q2 and Q3 traditionally being a lean season for SCF, this quarter PPF segment drives volume growth(SCF grew by 64% year-on-year, while PPF grew by 67%, while IPD grew by 30%), Q3 might see a seasonal dip but Q4 will show nice numbers

architectural film is experiencing growth, running at a 100% yoy growth rate. This include spectrally selective films and the DecoVista series.

Market has started discounting expected tariffs on Indian exporters by Trump administration to boost thier own local manufacturing industry. The primary reason for US to behave like this is possible de dollarisation as many Eastern countries like China, Russia and India have reduced thier US dollar buying rate and are diversifying thier forex reserves into other currencies and gold. So, basically the unlimited capability of US to keep printing dollars (due to reserve currency status) is being challenged now. And these are US reactions to handle the situation. If, de dollarisation happens at all, that would not be good for exporters in long run as well. This is just one of the possible outcome from here.

Garware Hitech films’s 77% revenue comes from exports and out of that 2/3 rd comes from US. Cant remember any other Indian listed manufacturing company which has such high exposure to US. There are many IT companies like that but hardly any manufacturing company.

It is close to impossible to predict macro economic outcomes because of more variables than we can ever cater for. So, these predictions hold no value more than a coin toss. It is possible that American government increase more taxes on countries like China, Mexico and Canada because US has maximum trade deficit from these countries. There are many countries like Vietnam and few others, who enjoys nill tariff environment in US. So, it’s possible that Indian exporters may end up benefiting. However, this is just one more of the many possible outcomes. Currently market definately thinks otherwise.

Disclosure: Invested. No opinions on future outcomes. Just the update on what’s happening in the world right now.

Anybody can flag a post by selecting a certain reason or providing one manually ,there are no rules for it . So it’s not necessary that the post was flagged by a moderator.Anyone could have done so.Till the moderators review it and decide one way or the other ,the post stays hidden .

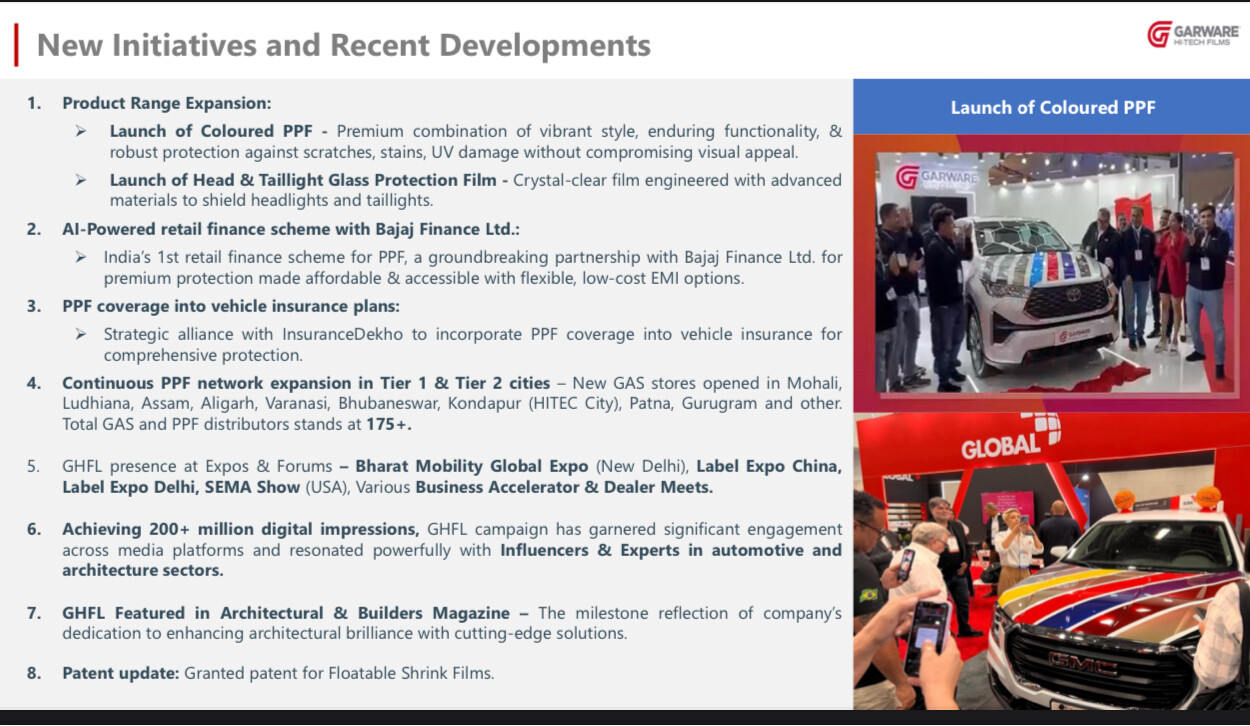

Garware launches 2 new products + EMIs + Insurance:

Coloured PPF: A game‐changer for Indian auto enthusiasts, introducing vibrant colour options to

personalize and protect vehicles like never before. Headlight & Taillight Glass Protection: Pioneering advanced solutions to safeguard the brilliance of

your car’s lighting systems EMI Solutions with Bajaj Finance: Making premium protection accessible for every Indian car owner

with low‐cost flexible financing options PPF Insurance in Partnership with Insurance Dekho: The first‐of‐its‐kind comprehensive insurance

coverage for PPF in India, redefining car care security ensuring long‐term stress‐free utilization

With Trump imposing Tariffs left and right, what could be the impact on Garware’s USA revenues (Global Films) if there are import tariffs for Polyester films, esp. PPF and Window films in the USA.

While XPEL sources from China and India, other players like 3M and Eastman have plants in USA. They are likely to gain market share from other players.

Just a hypothetical scenario and trying to understand how bad it could be.

The company is closely monitoring the tariff situation, especially in the US market.

Current tariffs favor the company—duties on Chinese imports are around 35%, while Garware’s duty is only 6.6%.

Even in a worst-case scenario, the impact of reciprocal tariffs is expected to be minimal (2-3%).

The company sees this as an opportunity and is positioning itself to capitalize on it.

2. Business Growth

9M FY25 revenue grew 27% YoY to ₹1,561 Cr, driven by sustained demand across key segments.

Q3 FY25 revenue stood at ₹466.4 Cr, a modest 2.8% YoY growth.

Exports contribute 74% of total revenue, with value-added products accounting for 85% of the mix.

The IPD segment grew 24%, while the CPD segment saw a 7% decline.

Strong growth in the domestic market—architectural films grew nearly 100%, while the sun control film business expanded by 20%.

The company expects significant growth in PPF (Paint Protection Films) with new financing and insurance options becoming available.

Management is targeting 20-25% top-line growth in the coming years.

3. Margins & Profitability

9M FY25 EBITDA grew 61.7% YoY to ₹374 Cr, with an EBITDA margin of 24%.

Q3 FY25 EBITDA was ₹93.7 Cr, an increase of 10.7% YoY. PAT for the quarter rose 11% to ₹60.8 Cr.

Q3 margins were softer due to seasonal weakness in higher-margin IR products.

The company aims to maintain margins at 25% ± 3% and continues to focus on improving operating margins, which have grown from 9% in 2018 to 24% currently.

4. Capex & Expansion

The company approved a ₹118 Cr capex for India’s first TPU extrusion line at the Waluj plant.

The line is expected to be operational by October 2026, with a capacity of 360 lakh square feet per line.

The TPU line will support cost savings, R&D innovation, and an expanded product portfolio for PPF.

The payback period for the TPU investment is estimated at 33 months.

A fourth PPF line is on track for completion by September 2025.

All expansions are funded through internal accruals, reflecting the company’s strong cash position.

5. Future Guidance

Management remains confident of achieving ₹2,500 Cr in revenue by FY26.

The TPU extrusion line and the new PPF line will help improve profitability and utilization.

The company expects Q4 performance to be in line with Q1 and Q2 results.

Strong growth is anticipated in the domestic market for both architectural films and PPF.

6. Financial Strength & Strategic Moves

The company holds a cash surplus of ₹572 Cr and is net debt zero, ensuring financial flexibility.

It is expanding its team globally, participating in industry events, and strengthening its digital presence.

Management recently received approval to increase authorized share capital from ₹10 Cr to ₹15 Cr, potentially signaling plans for capital raising to fund future capex and working capital needs.

I think the tariff effects are not clearly understood.

A higher rate of tariffs apply to China

Most of the time the competition is not USA but China, which in case it is, will make Indian products less expensive

Very much doubt US will set up manufacturing for 4 years. It takes 2-3 years just to construct a residential building. Building a plant will take atleast that much time. In that time it will be almost time for Trump to go.

Tariffs were not actioned via congress. It was a presidential act. It will take another presidents pen to write it off with a single stroke.

If at all tariffs were to stay, companies considering manufacturing will likely do a cost analysis towards beginning of next presidents term.

Over the long term, if China allows its currency to depreciate, some of the US manufacturing can be competitive again and maybe return to US. The Trump administration probably wants that more than tariffs. Previously when tariffs were introduced, China circumvented by exporting from Vietnam and other far east countries. Now the tariffs is put on all countries, so that forces China on the table in 1-2 years

For Indian companies we might have an advantage in the interim, I’m not entirely sure

Applicators of ppf and sun control films used garwares products as they earned higher margins on them due to lower costs vs 3m and eastman. The quality is at par. With increase in tarriff, the cost difference and hence the incentive of applicators may reduce to switch from player like 3M. Additionally, demand is bound to get impacted due to general inflation in US and cut in discretionary items.

Also now that we are moving towards a more protectionist world , made in America for America sentiment may overpower cost based decisions only, if at all there are cost differences. The tariff rate is higher than the discount of 5-10 pc of garware products vs it’s peers. Maintaining the same price difference as before would hit margins

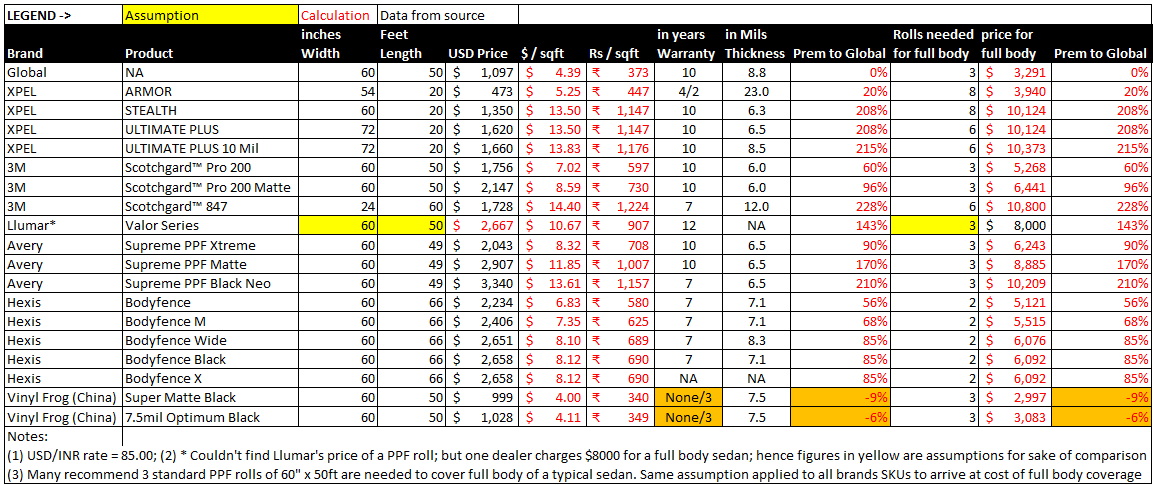

After analyzing some data from public sources, I am starting to believe that this fall in the stock price is unwarranted. I have 3 reasons to believe so.

Low-cost manufacturing gives relative pricing power advantage

In this post itself, it is already well-established that Garware has a low production-cost advantage. After all, the company is one of the most vertically integrated manufacturers of automotive films.

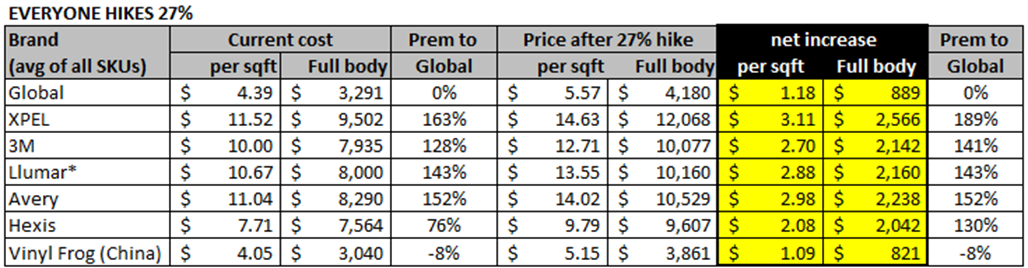

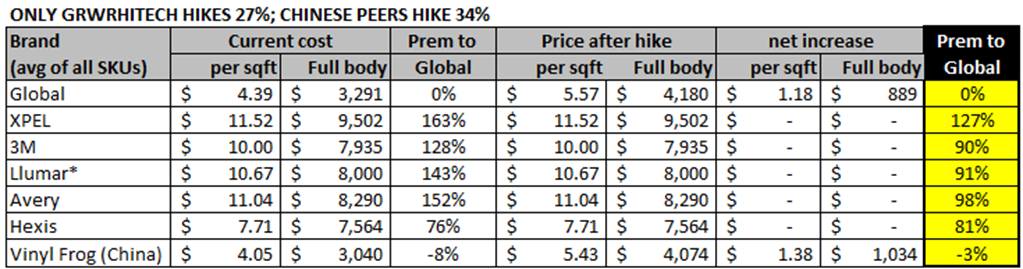

The table below lists the price of various paint protection film (PPF) brands in the USA. By analyzing the data, it is clear that Garware’s cost advantage indeed reflects in competitive pricing. And the gap is huge. Especially when we compare the cost v/s value proposition (warranty period and thickness of films).

It is interesting to note that one Chinese player comes close to Garware’s pricing. But if you do a basic online search, you will learn they have weak user reviews and do not give adequate warranty.

While the above table only presents PPF data, I am assuming that similar advantages exist on the sun control films (SCF) segment as well.

Just some handy info: In FY24, PPF grew 6x YoY and contributed 27% of sales, while SCF contributed 38% of sales (flat YoY). As of 9MFY25 USA contributed ~52% of sales as per PPT.

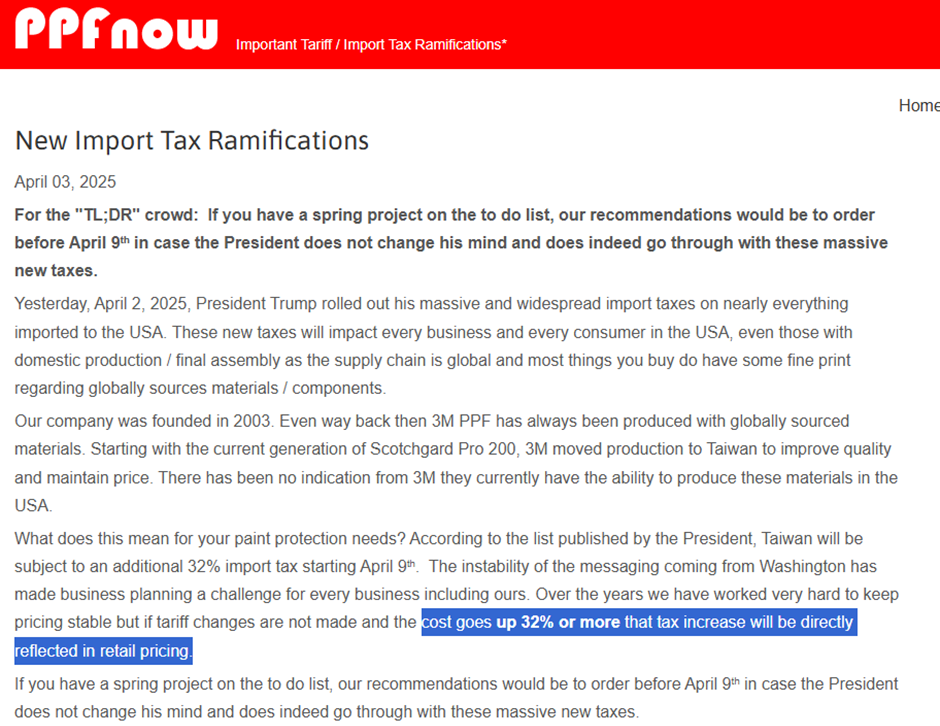

Industry is dominated by MNCs, who may pass on the tariff hike to customers

If we invert the above argument, then the main reason for this large difference in price can be explained by lack of backward integration by competition.

In this post itself there was a discussion of Xpel (major US player) facing competition from its own supplier, Entrotech, who launched their own product in the market.

So, it would be reasonable to believe that the MNCs like 3M and Eastman (Llumar), who rely on contract manufacturers, might not have the wriggle room to cut prices and will instead pass on the tariff impact to customers. In fact, one dealer has already posted this on their website. Link: New Import Tax Ramifications – PPFnow

Assume that all PPF brands take the same price hike of 27% as Garware to pass on the tariff impact to their customers.

Now this is not correct, because different competitors will have different source countries. Some competitors may have higher tariff hit, while others may have lower impact. But for sake of simplicity, let’s take 27%.

Highlighted columns below show that Garware’s product will see a much small Dollar cost increase compared to peers, making them more attractive to consumers.

My conclusions: Garware is better positioned to withstand this tariff change. Moreover, the backward integration capex for PPFs announced in 3QFY25 will only add to this factor. If the market demand slows down due to rising prices, then on the flipside, there is a chance that this development may actually hasten the pace of market share gain for the company.

Risks: Any major slowdown in the USA auto market and hence the PPF/SCF market, can impact Garware’s medium term growth trajectory. Slowdown in the market may be higher than the potential market share gain. I believe this is a meaningful risk. Hence, I personally would wait before building a large position (>5%) on this stock, until clarity emerges.

Disclosures:

This is not a recommendation. I am not a SEBI registered advisor or research analyst. These are my personal views shared purely for research purpose and benefit of the community.

I added some position in yesterday’s fall and have been invested (~2% holding). So, I may be prone to bias.

My views may change if contrary information comes to my knowledge. Will post as and when that happens.

Overall consumption in the US - including the sales of new cars and hence the sales of PPF is going to go down drastically

The chinese economy have the capacity to absorb multi year tariffs vs Indian economy has no such government support

Garware is not suffiently diversifed to sell to other regions and the brand will need multiple years to become a leading player. Untill then the only option is to become a low cost producer and let someone else market and sell

Selling to new markets implicity also imply sales teams, branding, marketing, logistics and tariffs from those countries.

Even if a 25% tariff is implemented, I referred back to Garware’s Q2 FY 2024-25 concall where the management mentioned that their products fall in the premium category, offering healthy margins not just for the company but also for dealers and distributors. Assuming the tariff impact is shared between Garware and its U.S. channel partners, with a portion passed on to end customers, I believe the company can still maintain a margin of at least 15% in USA because of their Quality and Premium positioning.

Upon deeper analysis, around 50% of the company’s total sales come from the U.S., with the remaining 50% from the rest of the world (RoW). Even if net margins in the U.S. drop to 15% due to tariffs, while margins in RoW remain stable at 25%, the blended average still works out to around 20%. This suggests that the company can continue to maintain healthy net margins going forward, despite potential headwinds in the U.S. market.

While this may be lower than current levels, it remains acceptable considering the significant potential increase in revenues.