Basic Details

• Market Cap: ₹29,300 crores

• Current Price: ₹2558

• Revenue (Latest FY): ₹7002 crores

• Net Profit: ₹748 crores

• Revenue Growth (3-year CAGR): 40%

Industry overview

The maxim “whoever controls the sea controls the world” is the foundational principle of geopolitics, emphasizing that mastery of maritime trade, naval power and shipbuilding capabilities directly translates to global influence. And hence the need to have a robust shipbuilding industry.

China’s dominance in shipbuilding

China, South Korea and Japan together control 93% of global market share in shipbuilding; with China commanding 53% market share.

China is home to more shipping ports than any other country, including 7 of the 10 busiest ports in the world. China also owns over 100 ports in approximately 63 countries.

In addition to its dominance in shipping ports, China is the leading manufacturer of shipping equipment, producing 96% of the world’s shipping containers, 80% of the world’s ship-to-shore cranes, and was receiving 48% of the world’s shipbuilding orders in 2020. It boasts the world’s second largest fleet of commercial shipping vessels.

Sector tailwinds

Maritime vision

India’s share in global shipbuilding is less than 1%. Shipbuilding industry in India was at 1.2 billion dollars and is expected to jump to 8 billion dollars in 2033.

Enter Maritime India Vision 2030– a comprehensive framework for the holistic development of India’s maritime sector, encompassing ports, shipping, and waterways.

Objective of Maritime Vision: Aiming to be among top 10 countries by 2030 and among the top 5 by 2047.

India plans to be among top 5 shipbuilders

Policy Guidelines for Shipbuilding Assistance

Govt has earmarked ₹24,700 cr for Shipbuilding Financial Assistance Scheme; wherein the government will provide financial assistance ranging from 15% to 25% per vessel, depending on the vessel category

As part of another initiative - Shipbuilding Development Scheme; Govt has set aside ₹20,000 cr for promoting development of Greenfield projects and modernization of Brownfield projects. These schemes would be valid till 2036. Clearly they have the potential to propel the shipbuilding sector similar to what PLI scheme did for EMS sector

Export Opportunities in Commercial Shipbuilding

India actively being looked at as a commercial shipbuilding hub by leading European nations, opening up opportunities for commercial shipbuilding.

Shipbuilding and freight dependence gap in India

Nearly 95% of India’s overseas trade by volume moves by sea, and about 92% is carried on foreign-flagged vessels. As of Dec’ 2024, while we had 1,545 vessels with 13 million gross tonnage, however only 32% were engaged in overseas trade.

This is owing to multiple constraints, including higher steel costs, elevated interest rates and low labour productivity, resulting in a 20–25% cost disadvantage versus global competitors. Also many Indian shipyard companies have a dependence on defence orders, and lesser focus on commercial shipbuilding orders.

Lessons to learn from Korea (powerhouse in shipbuilding) – In South Korea, a shipyard is supported by a 50 km radius of specialised vendors (valves, specialised steel, sensors). In India, we often have to import these components, leading to higher costs and ‘dead time’ during construction.

Recent India – South Korea partnership

A comprehensive framework for partnership in shipbuilding, shipping and maritime logistics was signed last month. A strategic move to aid India’s ambitions under Maritime India Vision 2030. Korea brings advanced shipbuilding technology; India offers policy support, land, and a growing order base - a complementary partnership.

The framework targets technology and supplier ecosystem development – something which is lacking currently

South Korean firms will support design, production engineering and advanced manufacturing. For instance, Korean yards use massive ‘block fabrication’ techniques. They build the ship in giant sections with 90% of the internal piping and electricals already installed before the blocks are even joined. With implementation of these best practices and development of an ecosystem, the Indian maritime sector will get a further boost, paving the way for more export opportunities in commercial shipbuilding too

Naval Defence / Warships

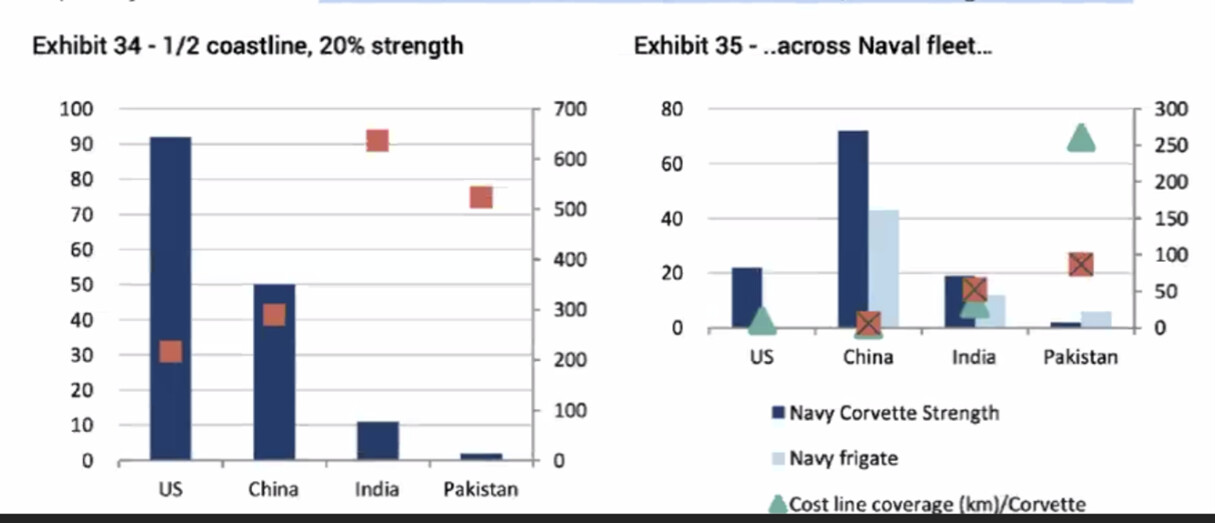

Now coming to naval defence, there is a significant disparity in the naval fleet, between India and China. Couple of stats highlighting the disparity between India and China when it comes to maritime superiority; and therefore the need for bolstering our naval might.

a. India has 18 submarines compared with 78 in China; and 68 in US

b. China’s fleet size is 2.5 to 4x , that of India . (including corvettes, frigates, etc)

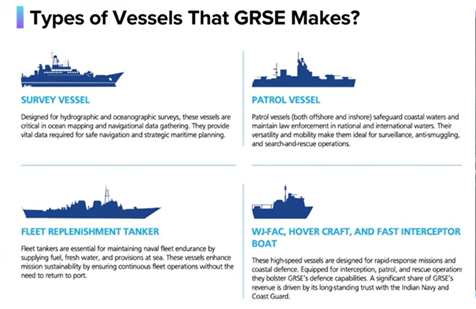

Overview of various ship types

A quick look at the major types of ships ..

Company background

Garden Reach Shipbuilders (GRSE) is one of India’s premier shipbuilding companies. The company is the first shipyard in India to build warships for the Indian Navy and the Indian Coast Guard.

GRSE has built over 800 platforms of all kinds, including 115 warships—77 of these have been delivered to the Indian Navy.

Types of Vessels GRSE makes

(Pic credit: SOIC)

Key Difference between GRSE and MDL

- While GRSE’s core strength is mid sized warships and fast patrol vessels; MDL is more into slightly larger warships like Scorpene submarines, Destoyers, etc.

- GRSE specializes in frigates, corvettes and patrol vessels

Diversified company

GRSE also builds commercial ships and undertakes engineering and engine production activities. A diversified company unlike other conventional shipyards.

1. Commercial ships- Has built survey vessels for Ministry of Earth Sciences and DRDO. They have also built multipurpose vessels for a German client Carsten Rehder. Survey Vessels are used for oceanographic surveys; and are critical in ocean mapping and navigational data gathering

2. Steel bridges - Company is engaged in the manufacture of prefabricated steel bridges. During FY 25–26, GRSE achieved a significant milestone with the launch of first-of-its-kind Modular Foot Suspension Bridge (FSB), a fully indigenous structure designed to span up to 400 feet without the requirement of piers.

3. Specialized research vessels – They are constructing Acoustic Research Shop for DRDO , two coastal research vessels for Geological Survey of India. The only Indian shipyard currently constructing specialized research vessels.

4. Weapons - They have delivered seven 30mm Naval Surface Gun systems to Indian Navy and executed multiple refit projects. They have already supplied 10 guns; Seven more are under final negotiation and contract stage.

RFP for 50 more guns is on the anvil. A single gun costs around 20 to 30 cr. This was earlier being imported, and is now being indigenized. Company is expecting lot of orders from Navy and Coast Guard for these Naval surface guns.

Focus on Indigenization

MAKE Procedure was promulgated in Defence Procurement Procedure (DPP), to foster indigenous capabilities through design and development of required defence equipments, products and systems.

a. MAKE I - Govt funded projects to promote indigenization. Min 50% indigenous content

b. MAKE II – Industry funded. Mn. 50% indigenous content

c. MAKE III - No design & development but manufacturing in the country with min IC of 60%.

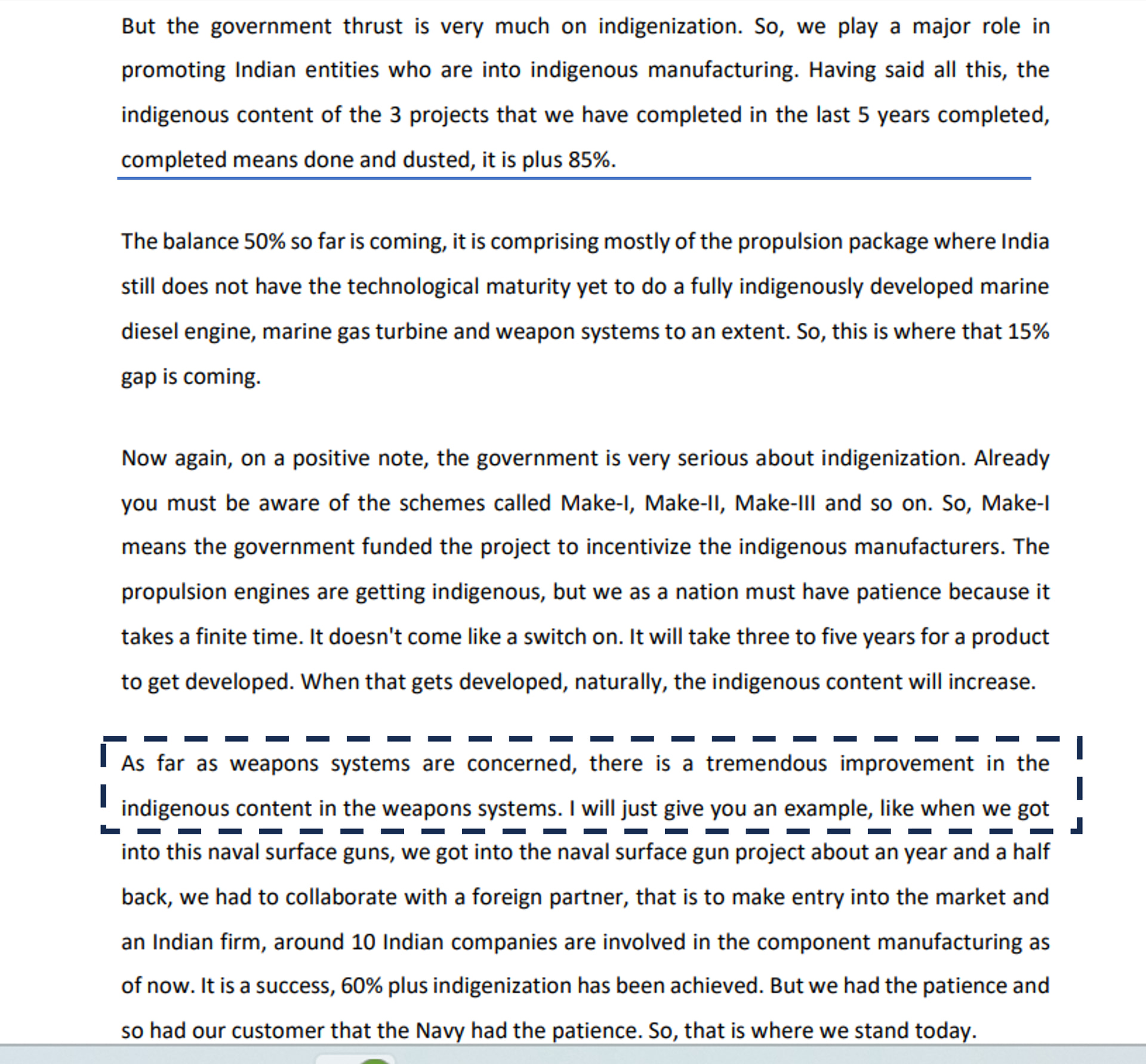

The level of indigenization for 3 major projects completed by GRSE, in recent years is approx. 85%. Within those projects, propulsion engines is an exception which is yet to be indigenized.

Within weapon systems, naval surface guns were being imported by India till 5-6 years ago. Currently, 60%+ content has been indigenized in this.

GRSE has designed and developed the 30 mm naval surface gun in collaboration with the BHSEL (Blue Horizons Strategic Engineering Pvt Ltd) and Israeli company Elbit Systems. The weapon is integrated with an indigenous Electro Optical Fire Control System (EOFCS) for precision targeting.

For P17 Alpha, indigenization content is approx. 80-85% . With more equipment getting indigenized, the indigenization content in future projects like NGC and P17 Bravo is likely to increase to 85-90%

This increasing thrust on indigenization is likely to open up new opportunities for companies like GRSE going forward.

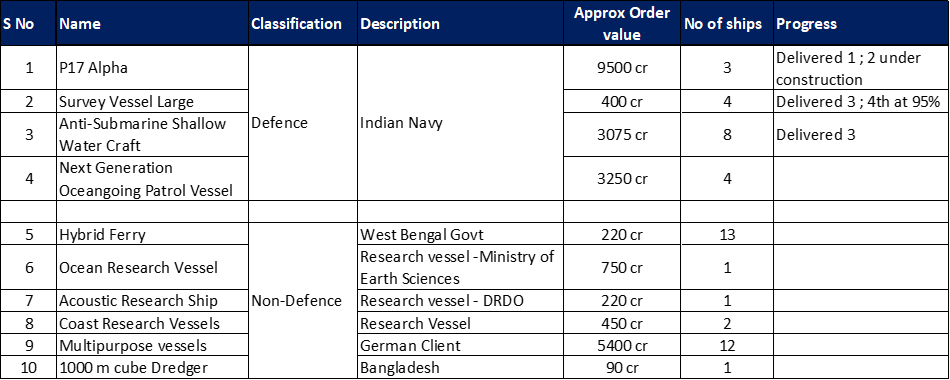

Order book

Order book position as of 31st December is ₹18,482 crores. And as of Q4 FY 26, it stands at ₹15,324 cr

Comprises of 10 projects consisting of 42 platforms. Projects and order value of each, listed below

In addition to this, there is a Nextgen Corvette project – which was an 8 -ship project (worth roughly ₹50,000 cr). GRSE has been declared as L1 and is likely to be awarded 5/8 ships amounting to approximately ₹33,000 cr. Approval process is on track and they are likely to be signing the contract very soon.

So that will take the order book to ₹50,000 cr. FY 26 revenue is ₹7002 cr.

Robust pipeline, Building multi-year revenue visibility

1. Defence segment : Seven high-value projects totalling about ₹1.5 trillion, have been accorded the Approval of Necessity by DAC. Primarily –

- P 17 Bravo, for which RFP is expected very soon. A seven-ship project, AON amount of ₹70,000 cr. 4 shipyards are in contention. But since GRSE and MDL have already delivered the P17 Alpha frigates, they are likely to be among front-runners for Project Bravo.

- Mine Countermeasure Vessels (₹320 billion)

- Landing Platform Docks (₹350 billion).

While these are on competitive bidding, there are a limited number of players in the fray; company given its experience and expertise has exuded confidence in winning 20% of these projects in pipeline.

With that, the current order book of roughly ₹18,000 cr is likely to see a sharp jump up to ₹75,000 cr in the next 15 to 18 months. And as some of the current projects (last ship of P17 Alpha, Anti-submarine shallow watercraft, etc) reach completion over FY 27 and FY 28, the newer projects like NGC corvette project, P 17 Bravo will take up their bandwidth FY 28 onwards..

Shipbuilding follows a certain revenue recognition pattern (detailed out few paras later below) , so while the book to bill ratio looks very elevated and the stated order book for ₹75,000 cr is likely to be recognized over forthcoming years, but there is clear revenue visibility for the next 7-9 years, supported by sectoral tailwinds.

2. Non-defence segment

Non-defence pipeline is across 207 platforms, starting from smaller size platforms of support vessels to VLGCs and beyond. Value of these is approx. ₹1 lakh cr.

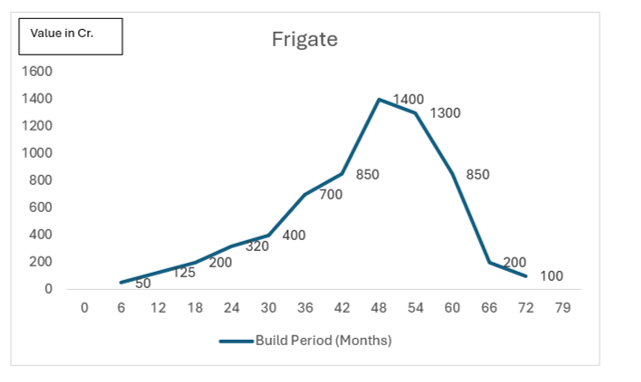

Revenue recognition pattern

Defence Shipbuilding sector typically follows S Curve for revenue recognition

- 1st phase – minimal revenue

- 2nd phase - blade cutting

- 3rd Phase – 40 to 65% recognition where equipment gets pumped on to the ship.

- 4th phase – last phase involves small part of revenue recognition. Trial phase

As the chart illustrates, after 18 months (lesser revenue) revenue starts galloping at faster pace. Incremental revenue takes lesser time; revenue can grow almost 7x in a span of 2 years. Management interview

P 17 Alpha was a landmark project commissioned by Indian Navy 6 years ago, worth ₹40,000 cr. It comprised of 6 frigates – 3 were constructed by GRSE and 3 by MDL. In case of P17 Alpha, FY 22 was the inflection point; after which revenue started growing rapidly. The exponential jump in revenue can be gauged from the fact that, the annual revenue in FY 22 (₹1700 cr) turned into the quarterly revenue in Q2 / Q3 FY 26.

Enter P 17 Bravo

Indian Navy has accorded the AON for P17 Bravo (a repeat project on similar lines as P17 Alpha) – which is likely to be a 7 ship project worth approx. ₹70,000 cr and 4 shipyards are likely to be in the fray; the RFP for the same is expected in Q1 FY 27. If GRSE is one of the companies which wins a decent share of the order value (likelihood is very strong), FY 28 and FY 29 are likely to be Build period years with flattish revenue; with 2029 likely to be point of inflection; after which revenue curve will start seeing a significant and sharp uptick .

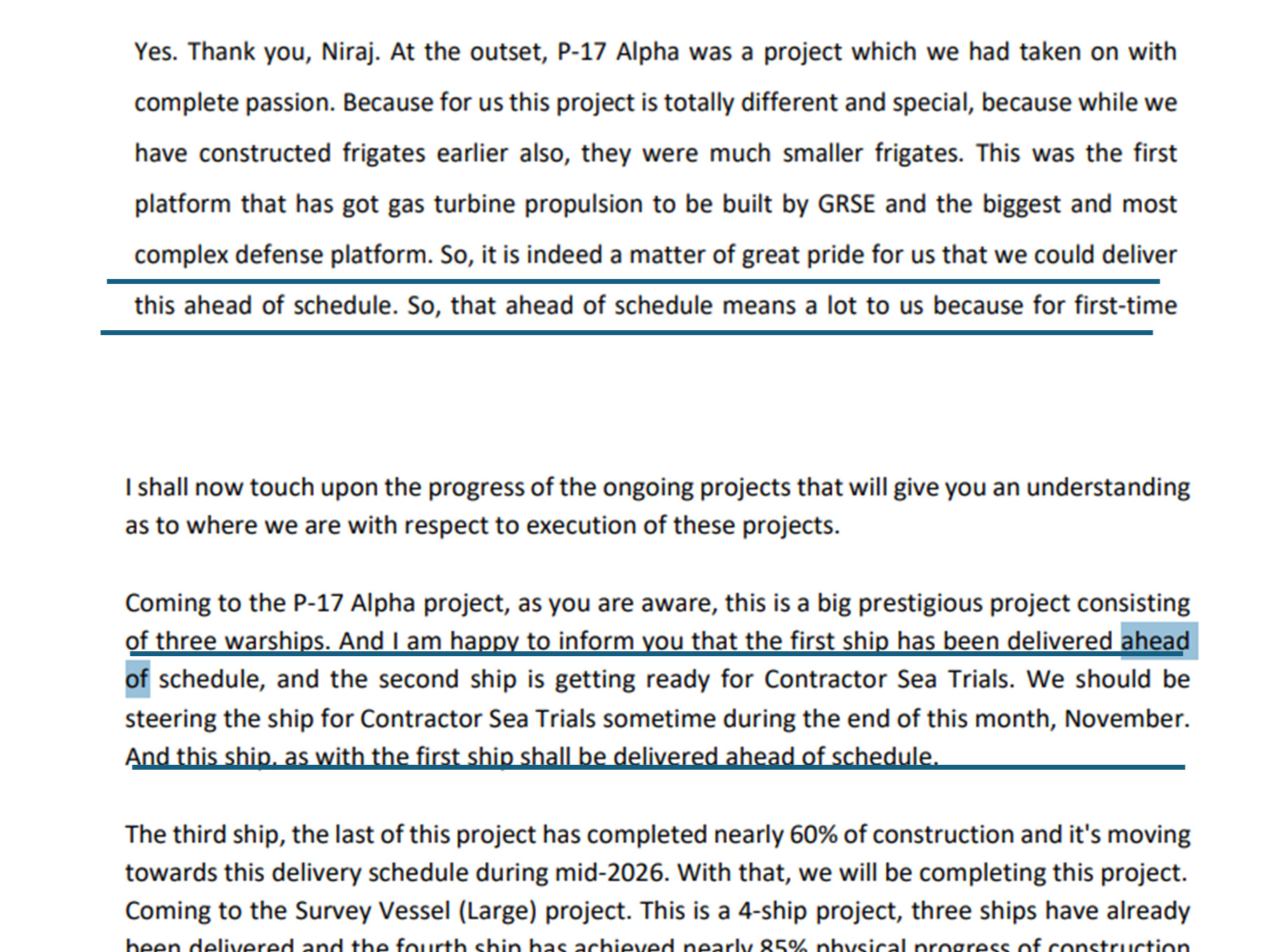

Delivering ahead of schedule

P17 Alpha was the biggest, and most complex weapon platform built by GRSE. The first and second ships have bene delivered ahead of contractual schedule, and the third one is also on track. Something that holds them in good stead to win a decent share of the next high ticket P17 Bravo project.

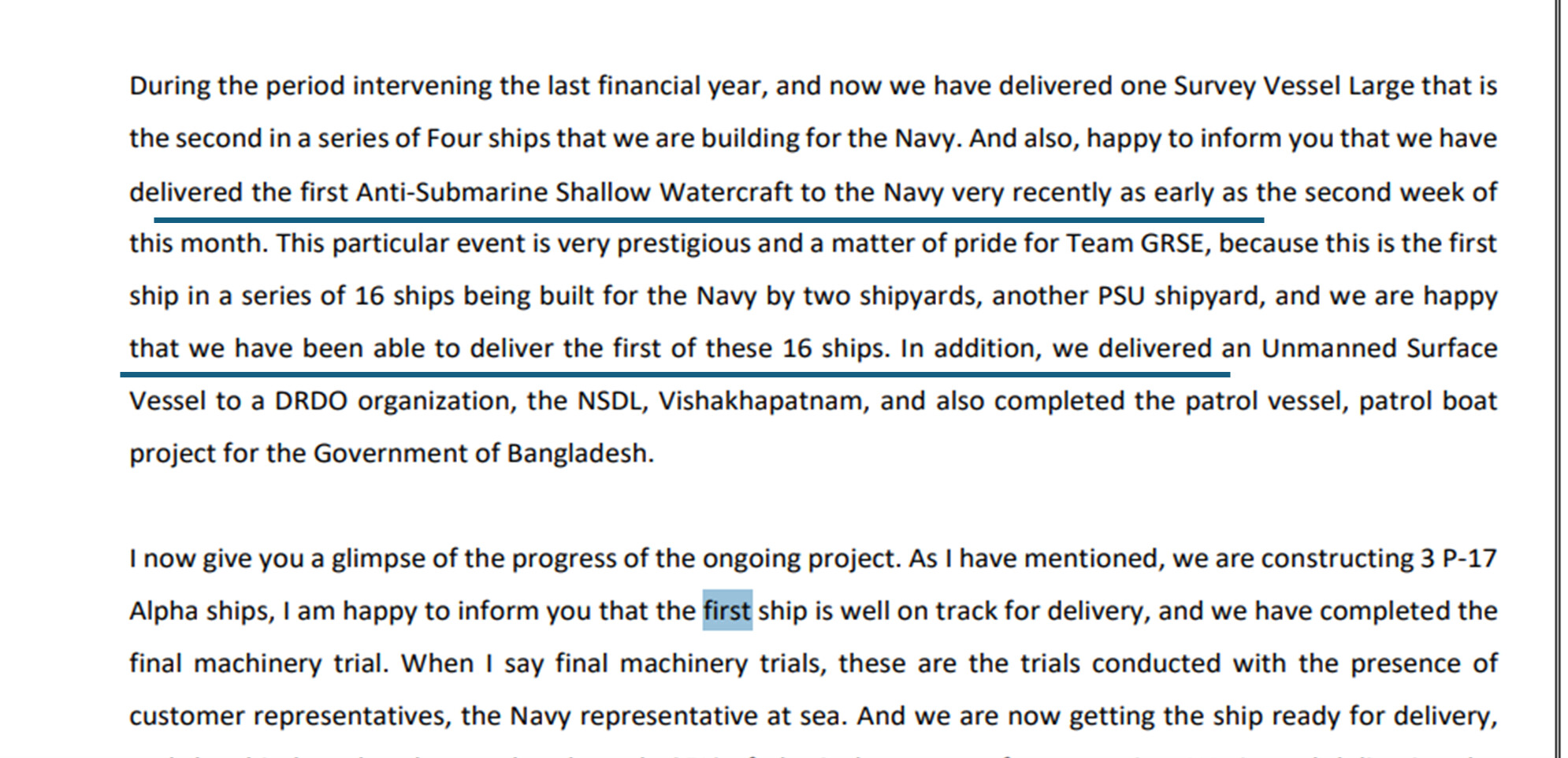

They delivered the 1st Anti-Submarine Shallow Water Craft (ASW) to Indian Navy. While 2 shipyards’ contracts were signed the same day, for 16 vessels (8 GRSE + 8 another PSU), GRSE delivered the first of 16 vessels

Commercial Shipbuilding Opportunity

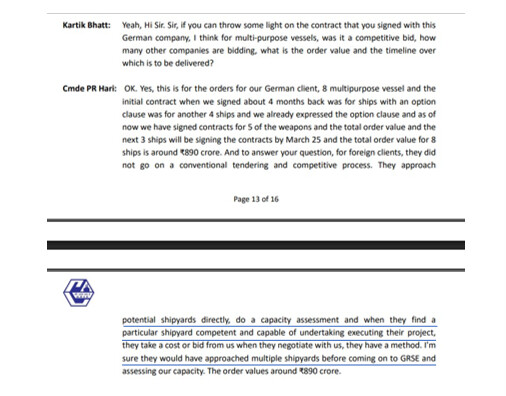

They signed a contract with Carsten Rehder Schiffsmakler and Reederei GmbH & Co to build four multi-purpose cargo boats. The contract was valued around ₹890 crore and to be fulfilled in 33 months. This was based on capability and competency assessment of various shipyards; and GRSE was finalized by the German client.

Initial agreement for 4 ships; with an option clause to extend to 8 ships – clause was already expressed in 2025. This has further increased to 12 ships as on Dec 2025; with order value of roughly ₹5400 cr.

European companies are looking at India as an alternate destination with China, Japan totally booked with commercial shipbuilding orders, something which Management highlighted during the recent call.

So be it winning commercial shipbuilding contracts with European clients or delivering complex weapon platforms ahead of schedule, it has exhibited traits of a private company, despite being a PSU..

Steadily increasing capacity

With such a strong enquiry pipeline and robust order book, building capacity for timely execution and delivery, becomes critical.

Two years back they had a capacity to construct 24 platforms concurrently. Currently, they have increased it to 28 platforms. This is likely to increase to 35 platforms, by the end of 2026.

Since this won’t be adequate to meet the demand; they are now planning both a brownfield and greenfield expansion.

Brownfield – they’ve taken over 3 sites from the Syama Prasad Mookerjee Port in Kolkata, with two facilities expected to start production by the end of 2026.

Greenfield – A state-of-the-art greenfield shipyard outside Kolkata; in Gujarat (one in Kandla and one in Bhavnagar) by 2028 to enhance in-house capacity.

The company has also signed MoUs with Swan Defence, to bid for and execute large commercial platforms. They’ve also signed a memorandum with Hindustan Shipyard Limited, to leverage its dry dock capacity for the Landing Platform Dock (LPD) defence project, AON value stated to be around ₹35,000 crores

With these capex plans, company appears to be gearing up to address the strong demand that is likely to come up in coming years, backed by policy tailwinds and indigenization push.

Financials

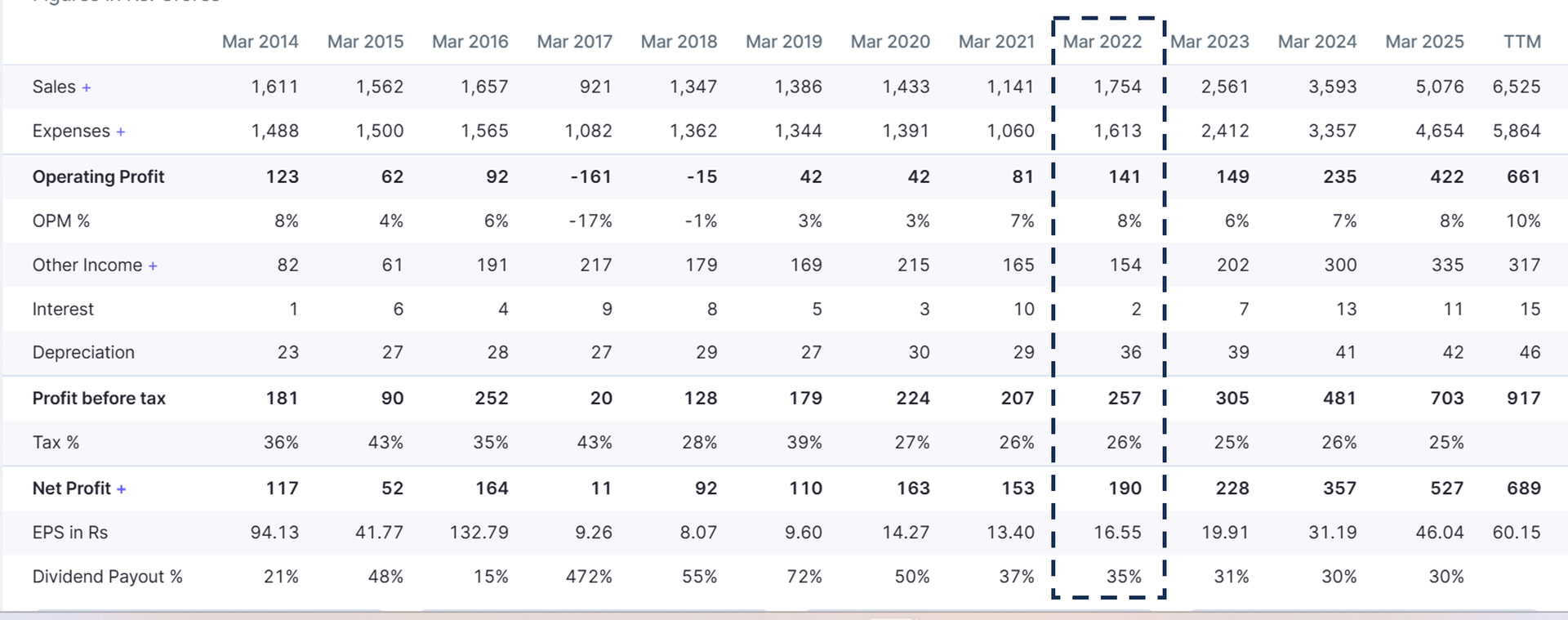

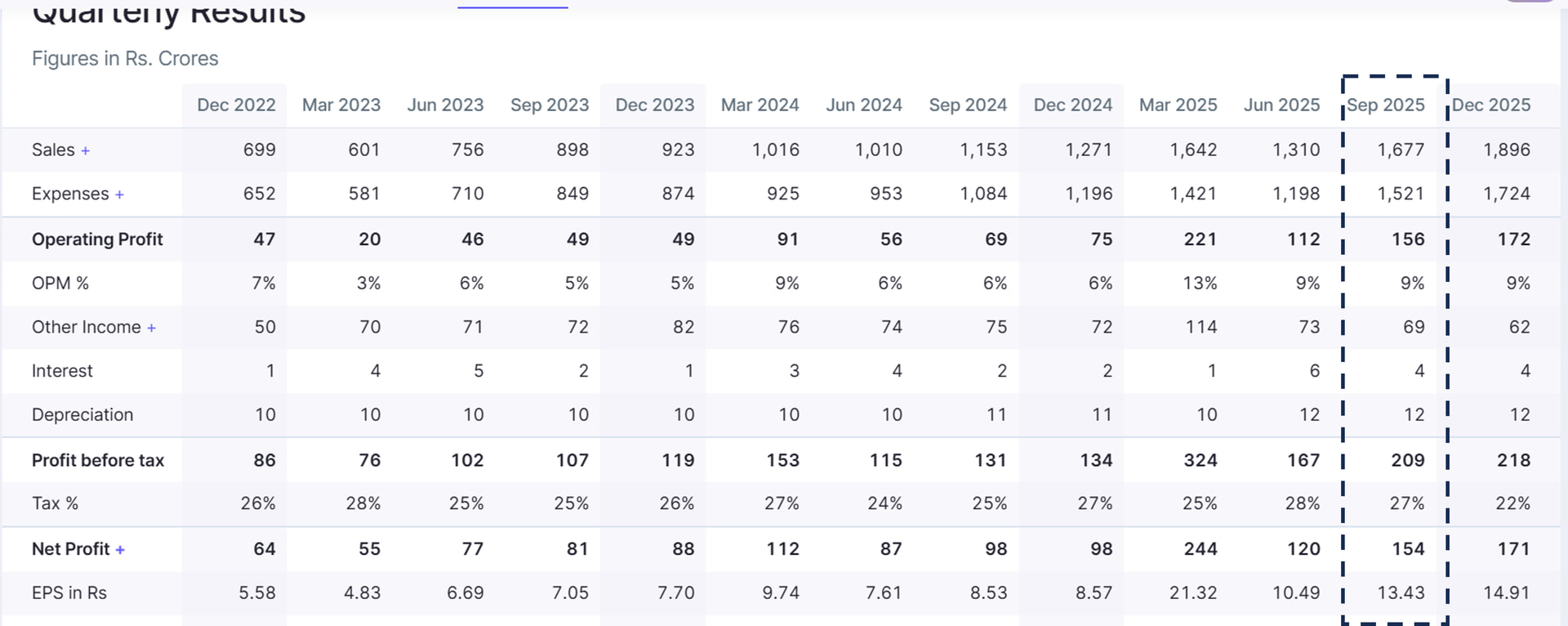

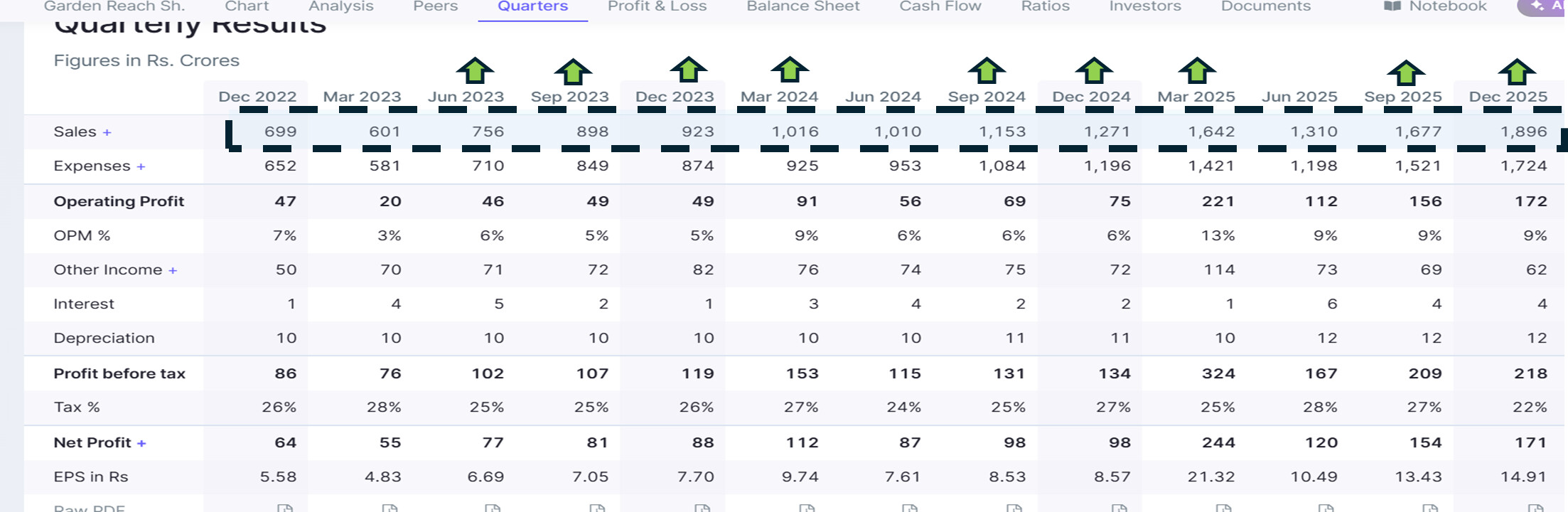

For full year FY 26: revenue is up 38% to ₹7,002 crore and net profit up 42%

One of the companies which has seen YoY revenue growth every quarter for last 13 quarters and Sequential revenue growth each quarter for the last 10 quarters (barring 2 quarters – and that’s because Q1 is lean vs Q4 which is the best qtr for them)

Management has acknowledged that FY27 is likely to be constituting peak revenue year; and a likelihood of a slight plateau in FY 28 – however they have base and depot spares from P17 A (10-15% of project cost), deliveries from research vessels as a cushion. There is intent to scale up ship repair business as well.

With high value projects like NGC and P17 Bravo lined up in coming years, this pattern of revenue growth in every quarter (stated above) is likely to get repeated in coming years, starting from FY 29

Operating margin:

Shipbuilding is a specialized sector, with margins being fixed at around 7.5 to 8% at PBT level. With costs being passed through. They have been maintaining Operating margins of 7 to 8% over last 5-6 years. This has improved slightly in recent quarters with higher revenue inflow from P17 Alpha, better operational efficiency, etc. The management has expressed confidence in maintaining 7.5% margins going forward, which are considered healthy in the sector

Cash equivalents on Balance sheet: ₹3009 cr

Debt free.

Promoter shareholding: 75%

RoCE of 36.6% and ROE of 27.6%.

To Summarize,

Strong policy tailwinds + Indigenization push + China/ Japan + 1 (commercial shipbuilding opportunity) + Capable management + Strong order book + Healthy Financial Metrics

Valuations

If one is considering a fresh entry in the company, it might be prudent to wait a while, considering the weak macros. Stock has seen some selling in recent days, even after strong Q4 results.

Company has been a 14 bagger over the last 5 years. (from 200 in 2021 to almost 2700 now). Therefore, if one were to look at it with a 5 years’ viewpoint starting from 2027 (especially with emphasis on the large ticket project of P17 Bravo) it might give very good returns over a longer period. For P17 Bravo, 2027 and 2028 would constitute the Initial Build period years and might provide buying opportunities. 2028-29 is likely to the point of inflection after which revenue recognition will see an exponential jump.

While FY 28 has been acknowledged as a year of moderation after the likely peak in FY 27, it will be interesting to see how the street reacts to large order wins (assuming there will be, considering the strong policy tailwinds) in FY 27 and 28.

Key risks

- B2G business – dependency on Govt orders . Though this risk seems to be mitigated to a large extent with revenue visibility over next 6-7 years

- Lumpy nature of business – revenue recognition for the frigate orders follows a certain pattern wherein the first 18 months is largely slower revenue recognition. But after 18 months incremental revenue grows at faster pace.. Though the company is pacing up its non-defence side of business too in order to have a more stable revenue recognition

- Delay in capacity expansion – capacity expansion is a monitorable, and any delay in expansion may impact on time delivery of ships and vessels

- Commodity inflation – While current contracts are fixed-price, and company claims that it has placed procurement orders early; and that there is unlikely to be cost escalation impact on ongoing projects; but this will be a monitorable

Sources

India’s shipbuilding revolution https://www.youtube.com/watch?v=-KCjbbcFM0s

https://indiasworld.in/current-affair/india-aims-for-global-top-10-in-shipbuilding-by-2030/

https://www.eurasiantimes.com/maritime-revolution-how-indias-massive-port/

https://www.youtube.com/watch?v=SNpS-zIM2no

Disc: Have been Invested since 4 years and Biased. No transactions in last 30 days