Q4- 2025 concall+ investor presentation summary

1…Crossed Rs. 200 crore in EBITDA and Rs. 100 crore in PAT for the first time.

2…Raw material

=Raw bottle scrap prices soared all time high during the quarter though prices have started to cool-off during May, 2025.

3…rPET fibre(rPSF)(textile)

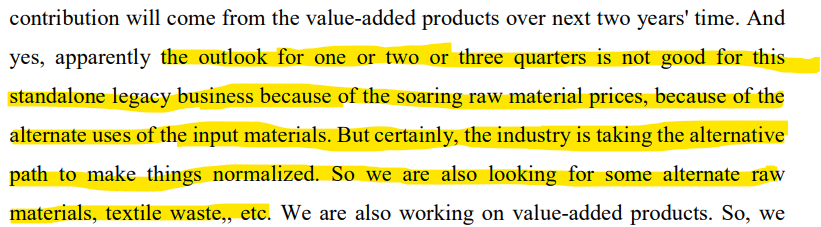

=Legacy business ( rPSF fibre and granules) under pressure due to:

A…High input (scrap bottle) prices,

-High volatility in scrap bottle pricing, driven by increased exports of washed PET flakes (intermediate).

B…Crude price down , widening gap between vpsf and rpsf

4…rPET granules(bottle)

=Sales Volume of rPET granules moderated due to rising gap between virgin and rPET granules

=Gap widened to 30–35% due to falling crude (lowering virgin PET) and high bottle scrap prices

=Food-grade rPET granules “set a new benchmark in the industry.”

80% capacity utilization for rPET

=High entry barrier in rPET: “Very highly technical product…not everyone will be able to manufacture very high quality rPET production.”

5…Value added portfolio

=Value-added products currently ~40% of mix; targeted to rise to 55–60% in two years.

=Value-added product portfolio growing (antimicrobial fiber, hollow conjugated fiber, dyed fibers, etc.).

=End-user industries for value-added products: geotextiles, automotive, carpets, technical textiles, apparel, and home textiles.

=Focus on increasing market share in technical textiles and

household textiles sector.

6…rPET granules

=Strategically realigning product portfolio towards high-margin, value-added products(rPET granules)

=rPET fibres v/s rPET granules capacity

2023@ fibre@90% granules@0%

2024@ fibre@80% granules@10%

2025@ fibre@50% granules@20%

2027@ fibre@ 40% granules@50%

So company has kept fibre capcity constant while hugely expanded granulea capacity from 2024/2027

7…Future growth guidance

=FY26 Revenue Guidance:

Rs. 1,700–1,750 crore (revised down from earlier Rs. 1,800–1,900 crore due to muted base business and stable rPET volumes).

=FY27 Revenue Guidance:

Dependent on new capacity ramp-up.

=FY28 Revenue Potential: Rs. 2,600–2,700 crore post-expansion.

=EBITDA Margins:

Consolidated margins expected to remain at improved levels (14–15%)

8…CAPEX:

Rs. 725 crore over 2 years; Rs. 90–100 crore already spent.

Fully funded; no immediate funding concerns.

A=600cr@orissa@greenfield

@67,500 MTPA@rPET granules @by H1FY27

B…125cr@warangal@brownfield

@22,500 MTPA @rPET granules @ Q4FY26

10…Capacity utilization

=Capacity utilisation in standalone business was of 99% and for Warangal business, it was 63%.

11…EPR Mandate & Plastic Waste Management Rules

=EPR (Extended Producer Responsibility) mandates 30% recycled content from April 1, 2025.

Management: “Plastic waste management rules…have also been implemented as per the schedule.”

Initial compliance slow; many brands still ramping up rPET usage.

12… Conclusion:

=Management Stance

Management remains optimistic for the medium-to-long term, citing:

A…Stabilization and ramp-up of Warangal and new capacities.

B…Regulatory tailwinds (EPR, FTA with UK).

C…Shift towards value-added products and

D…exports.

=However, they acknowledge

A…short-term challenges in legacy business

B…input price volatility

C… Slow initial response to the EPR mandate.

Disc…invested