Company has emerged as one of the leading PET- recycled RPSF manufacturers in India. We pioneered the manufacture of Recycled Polyester Staple Fibre (RPSF) and Recycled Polyester Spun Yarn (RPSY) from pre and post consumer PET Bottle scrap.

Having its manufacturing units at Kanpur (Uttar Pradesh), Rudrapur (Uttarakhand), and Bilaspur (Uttar Pradesh) Ganesha has a cumulative capacity of 97800 Tonnes per annum(87,600 TPA of RPSF and 7200 TPA of RPSY and 3000 TPA of Dyed and Texturised/ Twisted Filament Yarn) of RPSF and yarn.

Our products find application in the manufacture of textiles (T-Shirts, body warmers etc.), functional textiles (non-woven air filter fabric, geo textiles, carpets, car upholstery) and fillings (for pillows, duvets, toys).

Company Annual report and Research Report highlights

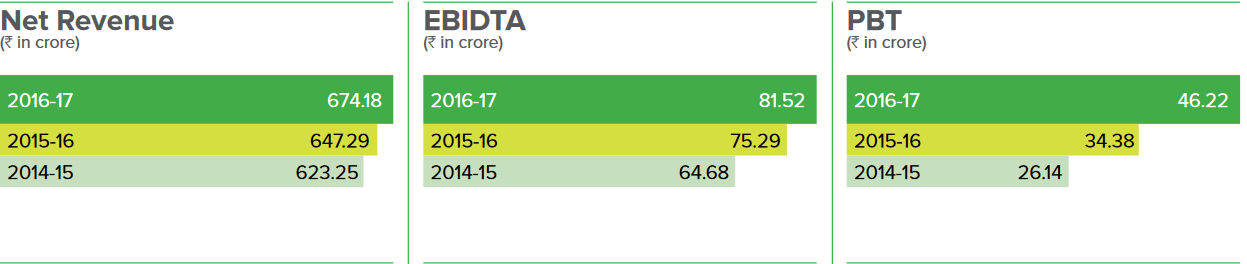

The growth of our topline and bottomline by 4.15% and 20.43% . EBITDA rose by 8.27% on account of improved capacity utilisation, PAT margin improved by 60 bps. Long-term debt-equity ratio of 0.32 and recorded a ROCE of 16.05%.

27% CAGR growth in revenue in last 10 years.Revenues, EBITDA, PAT grew at an average 17%, 16% 6%, respectively, in 2011-16

Recycling will get more importance in days to come from Government and is need of time. So company will not have issues with Raw material.

The products created by company Textile and Non Textile are evergreen segments. The increasing use of Synthetic materials is on rise.So no issues on end product market

It has major presence in North India and have scope of growth in other parts of country

Only listed player in this Niche (as per my finding but I may be wrong). The input raw material collection needs channel so new entrant will face problems competing with this company

SBI Mutual Fund has stake in it. It is still a small cap company so have room to grow.

Key Risks

Promoters have pledged 26.20% of their holding. The Promoter stake has decreased also with time. These two points have hold me to go forward with this company.

The end product of company is used in Textile Industry mainly. So the fortune of company is tied with growth in Textile Industry . Also there are many providers of Synthetic fabrics (yarn) to textile industry.

The Synthetic yarn has market share of around 50% but is very competitive as well (refer the research report for market share). This may hamper or make growth of company difficult in future.

Inviting VP friends to have a look and find loop holes in this one so that we can weigh in pros and cons of this company.

Disclosure - Tracking it and not invested. Planning to buy stakes in small size

The story seems too good to be true…tacking it since 2014 and in this time price has moved from 150 to 350+ levels given the Bull Run in market. I feel promoters credibility needs to be validated and physical inspection of plants could give more insight as to why no one else has tried doing the same…(considering this is 10+ years old company…

Disclaimer: I have a tracking position in the company

Recently govt cut down the import duty on PTA (Purified Terepathlic Acid) , which is used to make PET resins in turn PET bottles.Since Virgin PSF is made from PTA and MEG and RPSF prices are highly dependent on Virgin PSA , I believe Virgin PSA will be sold in much less price and companies will concentrating on the volumes. This in turn might affect realizations of RPSF.

In regards with the pledge shares, I believe its important to understand from management about the root cause of it.

Muted quarter, south facility to propel the earnings growth trajectory

Ganesha Ecosphere (Ganesha) reported EBITDA loss of INR32mn in 1QFY21 was on expected lines led by revenue dip of 71% YoY.

Key highlights are:

(1)volume declined 61% YoY with inferior product mix

(2) Plants were completely

shut in April, C.U in May/June/1Q stood at 30%/50%/37%

(3) July operated

at 80% and expecting recovery to 100% C.U by Sep’20

(4) BS continues to be

net cash positive.

Ganesha has acquired a under construction PET washing line of 12KMT for consideration of INR100mn in Nepal. South plant -phase1

and phase 2 (30K MT each) are likely to operational in FY22 and end FY23,

respectively.

We believe that south facility (phase 1&2) is expected to double FY20 EPS at optimal utilization with superior return ratios which will drive the re-rating in the stock. We broadly maintain our FY21/22 EPS. Retain BUY

with TP of INR360 (earlier INR340) based on 12x FY22E EPS (unchanged).

Current valuations of 7x FY22E EPS are discount of 30% to its historic average.37% utilization levels in 1Q impacts the revenue and profitability

Ganesha’s revenue declined 71% YoY at INR0.7bn on account of a) volume decline due to

lower utilization, b) realization dip due to pass on lower RM prices and inferior mix. The

installed capacity is running at 80% utilization for Jul and should improve to 100% by Sep.

EBITDA margin stood at -4.9% in 1Q (vs. 13.3% YoY). Lower staff costs were on account of

lower remuneration to KMPs and senior employees which should come to normal levels from 2HFY21. Gross debt as of Jun’20 is INR950mn and cash equivalents are at INR920mn.

We have factored EBITDA of 0.8bn/1.2bn for FY21/22E which is growth of -31%/+57% and

EBITDA margin of 10.9%/13.4% South facility can potentially double FY20 EPS at optimum utilization

Ganesha’s new manufacturing facility in Warangal, Telangana with 60,000MT RPSF capacity is on track to commercialize in FY22. This plant will help the company to seize the southern warket and reduce transportation costs. The set up and commissioning of the new plant will be in two phases: a) Phase 1 - 30,000MT at INR1.5bn by FY22 b) Phase 2 - 30,000MT at Rs1bn by FY23. The capex of INR2.5bn for south plant will be funded through mix of equity and internal accrual. The company has already raised INR1bn through QIP in FY19 at price of INR377/Share. The South facility is expected to garner profitability 500-600bps higher than the existing plant due to superior products, reduced transport cost, and advance

technology. We believe that South plant has potential to double FY20 EPS at optimal utilization.

Acquisition of a facility in Nepal to mitigate the shortfall created from commissioning of South

facility

Ganesha has acquired an under construction PET washing unit in Nepal for consideration of

INR100mn. The facility will be completed by FY21 end with capacity of 12000TPA. This

facility is located ~500km from Ganesha’s North India facility. Currently 18KMT feedstock is

being sourced from South India to the North facility. This will be shifted to new capacity in

South once operational from FY22. To mitigate the shortfall, company has acquired the unit in

Nepal which also provides access to a different geography.

Hope you all are doing good. Anybody tracking the company now? I love the business and see a lot of positives:

Capacity uitlization of 100% in 2019-2020

Constantly growing PAT and Sales

New capacity coming up in 2022 which will increase the capacity by 40%

Focus on premium products to increase margins.

Constant promoter buying from Market

But I am concerned about the below points:

One thing that I hate about textile business is low margins. Ganesha ecosphere though being in niche business is also suffering from the same. 12% OPM and just 6-7% of PAT margins which according to me is quite low and hence the company is only dependent on revenue increase.

Promoters have been talking about increasing the revenue share of premium products from 25% to 50% to increase margins. But as per the last 5 year data there has been no increase in revenue share which makes me quite skeptical about the ambitions,

Competitors are using crude oil as to manufacture virgin yarn. Can low crude price are at low and can affect the margins for Ganesha?

Would be great if somebody can throw light on the above concerns.

Only one input here, the end product prices are affected by the price of virgin yarn, the price of which is affected by the Crude price. But their raw material’s price does not move with crude, it is mostly demand & supply, as it is a waste product sold in Kgs.

So, your costs are not linked to end product, while the end product prices are volatile. So from a longer term perspective, i think it would be a volatile business.

Ganesha Ecosphere

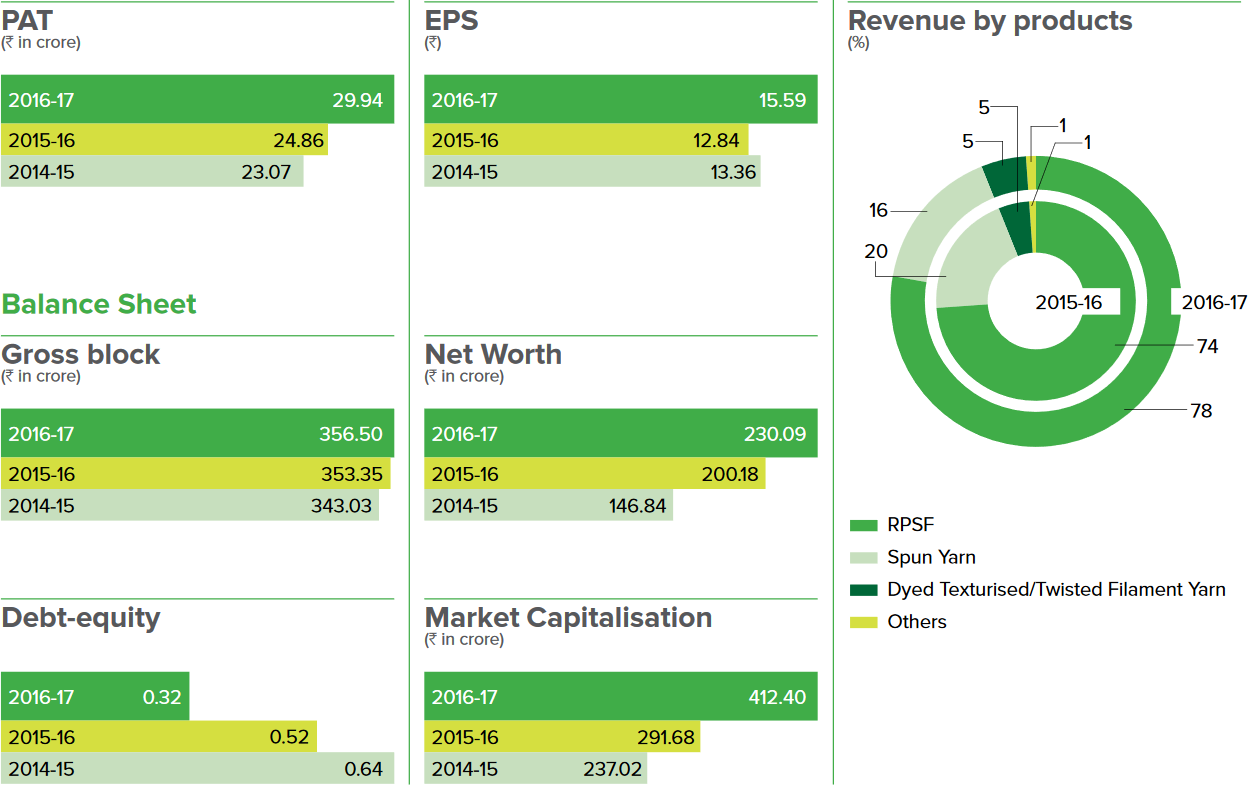

Revenue contributions

Spun yarn 18.5%

Polyester staple fibre 73.5%

Cotton, linen ratio/percentage to Viscose, rayon, terylene in sales

PET plastic share constitutes 60% towards synthetic fibre and remaining is majorly used for bottle production.

Upside for the company

Water tis not an input in the recycling process. Mainly used to clean the shredded pieces of plastic and to remove the dirt and debris

Revenue from products launched in the past three years reported strong growth 2020 A.R

High demand for 100% recycled yarn made from 100% post consumer PET waste is high

Energy used to make the RPET is less than what was needed to make the virgin polyester.

Water used recycled polyester production is only a fraction of what is required to grow cotton…

The other income is 32% of growth, largely driven by govt grants

900,000 tons of polyethylene terephthalene (pet) is produced annually in India. 65% off which is recycled at registered facilities 15% of recycling activity takes place within the countries and organised sector,while approximately 10% of PET is reused at homes.

Manufacturing units in

Kanpur (UP)

Rudrapur (UP)

Bilaspur (UP

Largest procurement of raw materials and largest production in India

200+ vendors to supply raw material across the country

Sources through rag picker.Cushions, crushed and baled by suppliers/vendors and shipped to factories.

Factors depending on these prices or is it fixed contract for a tenure?

Why should polyester be favoured to cotton

Designs ( should be the same for all)

Product advantage - good moisture barrier

Prices - relatively low prices than the others

Availability throughout the year without major fluctuations

under the age of 35 are the ones of fashionable dressing sense they could be buying textiles made of RPSF

Ban of PET scrap by India would push production in India

End products usage

Manufacture of textiles ( tshirts, body warmers etc) functional textiles ( non woven, air filter fabric, geo textiles, car upholstery, carpets) and filings ( for pillows, duvets, and toys) giving waste a useful meaning

Govt grants keep increasing with sales

Product development.

•Created a complete range of products from fiber to yarn - a one-stop for customers, among a handful of such players in the world

•

Leading recycling company to offer sewing thread: one of the key value-added products offered by the company.

The Company Introduced hollow Conjugated fiber

Introduced flame-retardant fiber

Introduced 0.9-1 denier microfibers in the recycling space

Downside risks associated

Independent director resignation in 2020

Borrowings increase along with trade payables

Tax disputes with

UP

West Bengal

Uttarakhand and Haryana

Central excise department

And

Income tax department too

Company going into an escrow agreement to keep up with the insurances and taxes every year

So that it can be paid monthly

Company has been successfully passing on any adverse movements in price to raw material suppliers as price fluctuations of finished products and of raw materials are in tandem

Indebtedness increased during the year from unsecured loans. From 2019AR

Commissions are higher than salaries, on few personal it is five times the salaries.

Balancing the salary with commissions and at par with the other directors and managers and justifying it by the normal which is above the pay and commissions.

Norm is 10% of NP.

With more than 200 products in the portfolio the company the OPM is not in Concord with it.

On being the largest manufacturer in India of RPSF and increased scale strengthened the bargain power with suppliers/ vendors and customers, the OPM does not justify for the above statement.

Does the company need to keep re investing in the existing machinery for their operations thereby suggesting a lower shelf life of the machinery in the sector.

Salary of the chairman has decreased owing to decrease in sales thereby decrease in commission but increase in salaries of all other board members.

Raw material procurement network- strength to performance

Easily disrupted if the raw material is mobilised

Assets increased during 2017-2018 period and issued QIP of 100crores to reduce debt

Unsecured loans from the directors and the company paying interests at irregular intervals.

Questions to be answered

What % of the overall market is recycled plastic and manufactured for the first time?

Is the end product recyclable again

Peer pressure

Collection networks

Input raw material quantity to output quantity

what are the value added products where the demand was lesser erratic and product enjoyed a superior returns for the company

What if the 15% of the organised recycling goes up pushing prices of raw materials for the company

OPM would be decreasing

how does the company see this as

is it a threat or is it negligible

In view of the expansions in the various geographies across the nation. Is it a move to manufacture all products in the portfolio in all units or is it to divide the products in view of convenience, advantages, cost saving,etcetra

In The global nonwoven segment company increased their market share to 25% in 2019-2020 from 24% in 2018-2019. Seems to be very tight knit market for the non woven segment.

Expansion to reduce R.M prices- to cut down transportation on R.M by vendors.

Plastic raw material cost/kg - depends on crude oil prices

Higher crude oil higher prices of Virgin polyester fibre.

In 2019AR the cost of raw material increased( higher input prices), it is due to competitiveness or crude oil ( being low )

1…ICRA has placed the ratings outstanding on the bank facilities of Ganesha Ecosphere Limited (GEL) on watch with developing

implications. This follows a fire incident at the company’s Polyester Staple Fibre unit located at Kanpur, Uttar Pradesh in June

2021, which resulted in a major damage to its building, machinery, raw material and finished goods. ICRA notes that this has

affected ~10-15% of GEL’s operational capacity, with production likely to stay disrupted in H1 FY2022, till the conclusion of the

re-development process. Together with the ongoing impact of the pandemic, this is expected to affect the company’s volumes

and revenues in FY2022 to some extent. While it has adequate insurance cover to take care of the major losses resulting from

the incident, clearances for the same are awaited. ICRA will continue to monitor the developments in this regard and evaluate

the impact of the fire accident on GEL’s credit profile once the exact implications are known

2…Increased scale of greenfield project resulting in higher-than-envisaged leverage – Post the ~Rs. 100-crore fund infusion via

qualified institutional placement (QIP) issuance in May 2018, GEL had announced a sizeable capex of ~Rs. 250 crore for a

greenfield capacity expansion. With multiple changes in the scope of the project over the past two years, the estimated project

cost was initially revised to Rs. 380 crore, and now stands revised to ~Rs. 453 crore. Correspondingly, the debt component

increased to ~Rs. 325 crore, compared to the original plan of Rs. 75 crore and the last estimate of ~Rs. 280 crore. This is

resulting in higher-than-envisaged leverage metrics. Nevertheless, given the conservative capital structure, ICRA expects the

company’s gearing to remain comfortable at less than 0.75 times. Further, Debt/ OPBDITA is likely to start improving from

FY2023 onwards with the commissioning of the project, after touching an estimated peak of ~3.5-4 times in FY2022.

Reliance Industries | The company is doubling its PET recycling capacity by setting up a recycled polyester staple fiber (PSF) manufacturing facility in Andhra Pradesh. The move is part of RIL’s commitment to lead the industry on circular economy, enhance its sustainability quotient and bolster the entire polyester and polymer value chain.

=(29.10.21)

Pursuant to Regulation 30 of Securities and Exchange Board of India (Listing Obligations and Disclosure

Requirements) Regulations, 2015, we wish to inform that the Board of Directors at their meeting held on

October 28, 2021, inter alia, considered and approved the reinstatement of Kanpur PSF unit by installing

an HDPE/PP Recycling Plant, subject to the approval of the shareholders and appropriate statutory

authorities.

=Recycling industry of these products are currently unstructured and down-cycling the scrap

instead of adding value. Good demand is going to be created for recycled thermoplastic with

regulatory compulsions in the form of extended producer responsibility as well as pledge for

sustainability by brands and corporates

=We are exploring this segment. Much light cannot be thrown for the margins etc, but of course

the market is much larger than the PET market. The total segment of plastic is around 100

million tonne in the country and PTE is only one million tonne out of that, so 90% is the other

plastic and what is happening is that, their recycler industry is completely unorganized and they

are down-cycling and it is eroding the value instead of adding the value, because of the

technology, because of the capital constraints and because of the unorganized sector.

In screener, data for PNL & BS show up from March 2020 onwards. Annual reports are available from 2010 onwards. Screener chart shows price vol data from 2006 onwards. Why PNL & BS data from 2010-2020 not showing in screener. Maybe I am missing some developments wrt to the company or the data. Would request senior boarders to expand if they can. @ayushmit

A…Export

=The slow-down in China has unfolded good opportunity for us to penetrate in export market and we made an export sale of Rs. 128.32 crore during FY 2022 (Rs. 35.84 crore Q4FY22) which is a growth of 112% over Rs. 60.53 crore export sale during FY2021.

= Contribution of export sale to total sale reached to 12.5% form earlier level of 7.5 -8%.

=We could grab the new set of overseas customers on the back of getting approved vendor status of some international brands like Target

and Inditex.

B…Though the EBITDA improved in absolute terms, margins were declined in comparison to last year because of increase in input costs as well as manufacturing cost

particularly power and fuel cost.

C… During Q1FY22, company had provided an exceptional loss of Rs 25.13 crore due to fire in

Kanpur Plant, which has been reversed in Q4FY22 in view of the reasonable certainty in getting the said loss compensated from insurance company.

D…Working capital days

=.Company also brought down its cash cycle from 105 days to 75 days during the year.

=We have got a lot of improvement in the current financial year, the working capital cycle has come down to 75 days because of so large project basket as well as the holding period for the raw material there is not much room available for bringing down the working capital cycle further

though 5% to 10% is always possible

2…WARANGAL PLANT

=. At Warangal, we have started the commissioning of the Recycled

Chips plant and it will start the production by July, 2022.

=Fibre and FDY plants are progressing well and expected to start by September.

=We faced a lot of hindrances in implementation of Warangal project due to COVID related frequent lock-downs and disruptions in supply chain of critical equipment specifically electrical and electronic parts. We are still facing big issues in

terms of timely availability of electrical and electronics parts not only from China and overseas suppliers but also from domestic suppliers as they are pushing their delivery schedules several times. Travel of Chinese Engineers for plant erection is also an issue and the Fibre plant is being

erected by us under guidance from Chinese engineers over online platforms which is taking

unusual time and delays. All these factors made the implementation of project somewhat

challenging and caused some delays to scheduled implementation.

3…NEPAL PLANT

=At Nepal, we have started the Wash line and commenced the production. We are hopeful in

getting this project to operate at full capacity by August-September, 2022.

=In Nepal facility , we plan to use

the Nepal capacity for captive consumption unless we have a better opportunity in the export market .

=we are getting the raw material cheaper by about 15% in Nepal

=tax is also lower in case in Nepal

4…HDPE PILOT PLANT

=We are going to start in the next one or two months for Recycling rigid plastics

=To seize the upcoming opportunity where demand would be emanating for quality products in

recycled rigid plastic (HDPE, PP etc.) segment to fulfil EPR liability of brand owners and manufacturers consuming plastic packaging for their products, we, at Kanpur unit, are working

on a pilot recycling line for rigid plastic which would be operational by July end.

= The capacity of this pilot plant is 300 tons per month. Post successful implementation, we would ramp up the capacity to 1,000 tons per month during current financial year itself.

=The estimated project cost

would be around Rs 30 crore which would be funded through proceeds from insurance claim

expected to be received by July, 2022.

A… Medium tenacity fibre

=Between our Rudrapur facility and Bilaspur facility, later is commanding superior margins in the

market because of better quality and value added products while cost of production is almost the

same between the two plants. From market point of view, RPSF manufactured in Rudrapur plant

is categorized as medium tenacity fibre and those manufactured in Bilaspur facility (and also to

be manufactured in Warangal plant) is called high tenacity fibre.

= Given the price and cost matrix,

medium tenacity fibres may not sustain the margins in future while selling in the market.

However, with our vast experience, we are successfully running our spinning unit consuming 100% of our medium tenacity fibre and this unit is making good margins.

B… Job work agreement ends

=Further, we were running a yarn spinning unit on job work which was contributing a production of 1500-1800 annually to us.

=The agreement for job work has come to an end during March, 2022. So we are also short in market by that much quantity running a yarn spinning unit on job work which was contributing a production of 1500-1800 annually to us. The agreement for job work has come to an end during March, 2022. So we are

also short in market by that much quantity

=So sensing the future course of industry as well as to increase our margins from medium tenacity

fibre segment, we have consciously decided to put up a spinning unit with a capacity of 34,000

spindles at Temra (Bilaspur), adjacent to our existing unit. It would be a green field project with

an estimated project cost of Rs 230 crore and it would be implemented over a period of next 18

months. At optimum capacity utilization, unit would be producing around 12,000 tons of yarn

valuing about Rs. 250 crore.

= We would be manufacturing mélange and doubled/ fancy yarn,

using our medium tenacity fibre, with an estimated EBITDA margins in the range of 25-30% with target ROE of 18%.

6…RECYCLING IS FOCUS

=We would like to clarify that due to market dynamics turning adverse on medium tenacity fibres

in future, we are moving on strategically for yarn spinning unit in sustaining the margins.

=However Recycling is and will remain our core focus area and all of our future expansions would primarily

be in that direction only. It is pertinent to mention that we are very bullish about the future of recycling industry not only in India but globally.

7…BLENDING

=New regulations are being implemented globally mandating the blending of recycled products

with virgin products and responsible organizations are pledging themselves for making their products environmental friendly. In India also, regulations have been introduced whereby all the brand owners and manufacturers are required to have 30% recycled contents in their plastic packaging from FY 2025-26 and this limit would be extended by 10% every year till it reaches to 60%, i.e., by FY 2028-29.

8…SUSTAINABILITY

=As we expand our operations, we aim to move towards sustainable efficiency. To that direction,

in our Warangal facility we have equipped ourselves to recycle 90% of water required in our

operations and only 10% fresh water would be needed.

=We are also setting up an ETP plant

which would be on Zero liquid discharge principle. All of our future projects would be working

on the same set of values as well.

= Our existing operations are already meeting 17% of their

energy requirements through roof-top solar panels and we have also set up group captive power

arrangements with Amplus RG Solar in Uttar Pradesh for 17 MW. Additionally, another deal for

14MW solar is in making as we speak which will take the organization’s renewable energy mix

to more than 50% and make our power costs escalation free for a fairly long period of time

9…GO REWISE BRAND

=For capturing the demand for premium recycled products, we are launching a brand “Go

Rewise”, which symbolizes recycling wisely. The brand is being launched with the vision to

close the sustainable loop. Go Rewise is dedicated to conserving resources and establishing

sustainability supremacy by efficiently recycling waste products into premium quality products.

=The brand has been patented and we wish to make this brand a symbol of pride among all our

customers. We are in the process of being onboarded by global brands after clearing their social

audits

10…MARGIN WILL IMPROVE

=Basically pet bottles can be

converted into three products roughly

-number one is the recycled polyester staple fiber,

number two recycled POY, FDY (recycle poly yarn)and

-number three recycled rPET which is used for making the bottle-to bottle.

So presently we are into RPSF which is the lowest margin among all the three products

A…So in Warangal facilities we are going to make all the three products, so the margins are higher in

case of recycled FDY and the bottle-to-bottle chips that is how the margins are higher there,number one.

B…Number two we are sourcing the raw material from South where the freight element is higher in case we are transporting it from south to north. So for the Warangal plant we would

be sourcing from south itself, we will be getting some benefit in terms of logistics cost over raw

materials

C…For Nepal also we are making the washed flakes and chips there, so the margins are higher because of the lower raw material prices there because there is no recycling facility in Nepal and there is no use of the recycled material itself in Nepal, so all the material is coming to

India through illegal way, so we are making this loop formal and legal, so we will be getting the

better prices here.

11…BILASPUR V/S RUDHRAPUR PLANT.

=As far as the quality is concerned you see the Bilaspur facility is having the better technology than what we are having in Rudrapur this is we called third generation recycling plant, the

Rudrapur one is the second generation recycling plant, so the quality what we are making in

=Bilaspur plant is almost equivalent to virgin fiber, so we are fetching good margins or a better pricing from market though the cost of production remains almost similar what we are having in Rudrapur, but with the improved margin from market and all the big spinners like Arvind,

Trident and Vardhman we are very well serving those big brands with our recycled products

from our Bilaspur unit.

=we are getting Rs.3 to Rs.4 higher realizations in case of our Bilaspur facility that is about

13% to 14% of EBITDA margins in that facility as against that 10% to 11% EBITDA margins in our Rudrapur facility

12…ONLY PREMIUM YARN

=What we are doing in our spinning units we are making only premium quality of yarns we are not

working on any commodity products.

=Even in our existing facility in Bilaspur with 28000

spindles we are making only colored dyed yarns, melange yarns and fancy yarns such as slub,injection slub, etc., so these yarns are having a very good margin as compared to the commodity product of white and black yarn

=Already in existing unit we are getting a very good margin for those with specialized yarns and in the

coming facility also we will go only for these kind of premium products.

13…LOSS FROM KANPUR PLANT FIRE

=Basically the Kanpur plant was the least among all the three plants though we have lost the turnover of over 90 to 100 Crores, but on profitability front we have not lost

much.

= Now we are looking to the market dynamics and scenario we are now not going to reinstate that production lines which have lost instead we are going for putting up another

production line which is suitable for making the recycled rigid plastic chips.

=So it will be a higher realization product than the current

14…RPSF REALIZATION

=Rpsf getting Rs. 97-98/Kg which is against 110 to 115 of virgin PSF.

=The realizations have improved by about 25% in the last one year though the cotton prices have

increased multifold.

=So cotton dynamics is different and the policy dynamics is different, but one thing is that after the cotton has become so much costlier the demand of polyester has increased

15…EXPECTED REVENUE AND MARGIN AFTER COMPLETION OF CAPEX

A…Warangal we are expecting 600 Crores topline from there.

B…Nepal is about 75 Crores.

C…New spinning unit: 250 Crores from this new unit.

D…HDPE…around 90 Crores to 100 Crores.

=so close to 1000 Crores additional in topline for all these new projects and

margins you say for

=Warangal still we are maintaining this 25% margin and

=Nepal at 18% and

= yarn you have also said 15% to 18%

= HDPE@ above 20

16…MOAT

=What is stopping big companies like arvind ,vardhaman etc from doing backward integration?

A…Different products

=I would like to highlight that we are having about 500 kind of products in our basket which are available for every kind of application to the end consumer number one.

=Whenever you are coming with the different products you need to have a number of lines to be installed. So yes of course anybody is open to go for a backward integration but it would be

better to tell you that still many of the spinning units who have came up with their one or two facility for recycled fiber they are buying a lot of premium products from our company,

=So yes anybody can come with

backward integration but still they need many number of products which would not be possible in one or two lines.

B…R n D and 30yrs experience

It is a R&D over the period of last 30 years what we have done

and the products which we are making on our different lines in different plants, so it is the expertise where you are getting a good number of buyers

C…Preffered vendors

=We are on the preferred vendor list of some brands for which we are making their product, so it is also a compulsion for them to buy from us.

17…CRUDE EFFECT

=Our end product is benchmark against the virgin PSF which is a derivative of crude

and the prices of crude make some impact on the prices of virgin PSF, so indirectly we are also

impacted by the prices of crude.

18…COTTON PRICE EFFECT

=Basically there is a switch from cotton to polyester always happens, when the cotton prices are

higher and polyester prices are lower the people are looking for a better opportunity by spinning

mills especially in South of India, so now the demand is growing for polyester in most of the

cotton units where either they are shifting to polyester or they are blending polyester with cotton

to make their product sustainable, so this happens every time when the cotton prices goes high, of

course the polyester always get a benefit whenever there is an increase in cotton prices

=Fluctuation in price of crude and spinning cotton

has always been there.

19…BOTTLE TO BOTTLE

=Going forward we are sensing that our B2B chips business would be the most accelerated kind of

product in the market out of all new and old products

=In terms of these bottle-to-bottles , the regulatory approvals we need to take

=Actually there are three types of approvals are required; for the US market it is the US FDA

approval and for the European market it is the EFSA approval and for India it is a food safety and

FSSAI approval, so we are already working on the approvals from these bodies

=We have imported USFDA approved machinery for this use of recycle in plastic pet packaging so that is why we went to Europe for this particular

thing

=Bottle-to-bottle grade chips will be used by mixing this in the virgin pet chips for making again the bottles.

=It is mandated by the government also that from 2024-2025 everybody has to consume 30% of recycled material in their packaging. So yes we are in discussion with big

brands also because they want to start this from the current fiscal itself.

20…BILASPUR YARN FACILLITY

Q# Currently in the Bilaspur the spun yarn capacity is 7200 tons with an

EBITDA margin of 16% to 18% and now we are adding another 12000 tons capacity with an

EBITDA margin of 25% to 30%, so just wanted to understand that if it is the same spun yarn that

we are expanding then how would the additional 12000 tons give a higher margin of 25% to 30%?

Ans#In the existing facility we are confined to source yarn only and in the new facility we are

coming up with a capacity to produce finer counts where we would get a better realization as

well as better margins also. So the current production capacity is in the range of average 18

counts to 19 counts while in the new facility we can produce some finer counts and the average

capacity would be around 24 counts to 25 counts so that leads to a better realization as well as a

better product portfolio for getting a good margin

21…RIGID PLASTIC OPPORTUNITY

=There are several different products one is PET and one is rigid plastic

from polyethylene, polypropylene

= In Kanpur and warangal we are coming up with other rigid plastics than PET, so all HDPE, PP polypropylene

=This is a very vast field you see the rigid plastic consumption in India is about 10 times of what we are having of PET, so you can just imagine

the opportunity there in the recycling of rigid plastic, but yes we have to work harder for different

R&Ds and making a intact supply chain of each type of plastic that is coming to the facility so you can make a better product.

=There are several sort of recycling facilities where you can mix all

the plastic and make a very poor quality of product where you would not get margin more than 3%, 4%, 5% and that too they are being done in an unorganized sector across India, already there are thousands of units who are recycling those plastics but those are all unorganized sector units

so yes you have to work harder for the supply chain so that you can get a specific type of plastic

coming to your facility where you can convert that plastic into a premium product which can be

supplied back to the big brand so we are working on that because we want to create a premium

quality product out of that plastic also.

=Of course it will fetch a good margin over the period of time but yes it will need a big asset to be done in this field.

=Bottle to Bottle market in India is a developing market. In our discussion 5 years ago, I used to

highlight that whenever food grade Bottle to Bottle will be allowed in India, there will be huge shortage of Raw Materials as same plastic is used for consumption. That situation can be

witnessed today. In future when plastic bottles will be used for making Bottle to bottle, there will be scarcity of Pet bottles for fiber and spinning.

Whatever bottles will be available, will be used for premium quality only.

= The fire loss at Kanpur plant gave us an opportunity to think and enter

in other plastics. We currently sell other plastics as waste. Going forward, we plan to use it as

raw material and converting the same in value added products

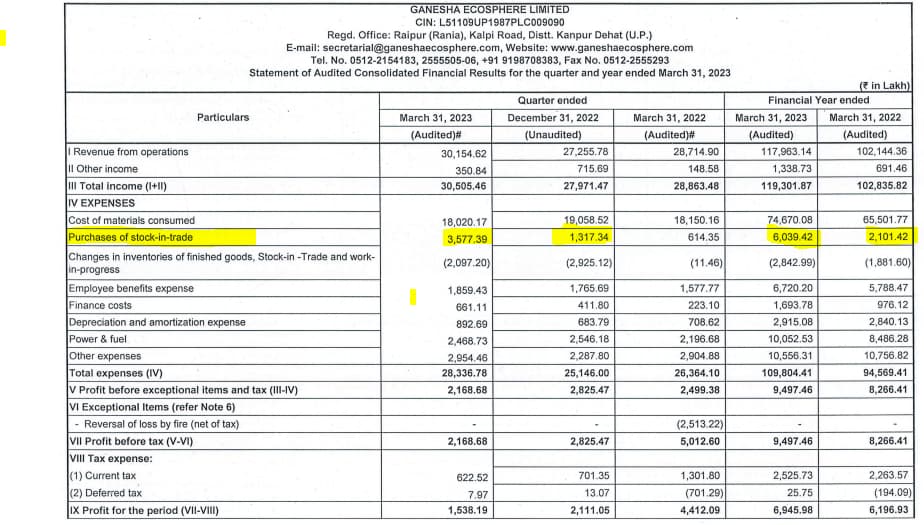

The majority of the growth that company saw, was on the accounts of higher realisation (26% higher than previous year) and management is confident that realisations would remain at about same level because of the value added products that they are producing but do you think is it really possible? If realisations go down then it could be a problem as it will counter the growth that company may achieve because of the CAPEX.

If we look at this Q4 and FY23 results, then “Purchases of stock-in-trade” has gone up significantly.

Now as per my understanding this is these are the goods which are bought and sold without any actual processing or it can be seen as purchases of finished goods that the company buys towards conducting its business.

So increase in this particular item indicates that the company is doing more of trading activities? What could be possible reason for such increase? And what happens when company is not able to sell such products in current quarter or FY? Does it become part of finished goods in inventory? In general, how one should look at this? Does such increase raise eyebrows?