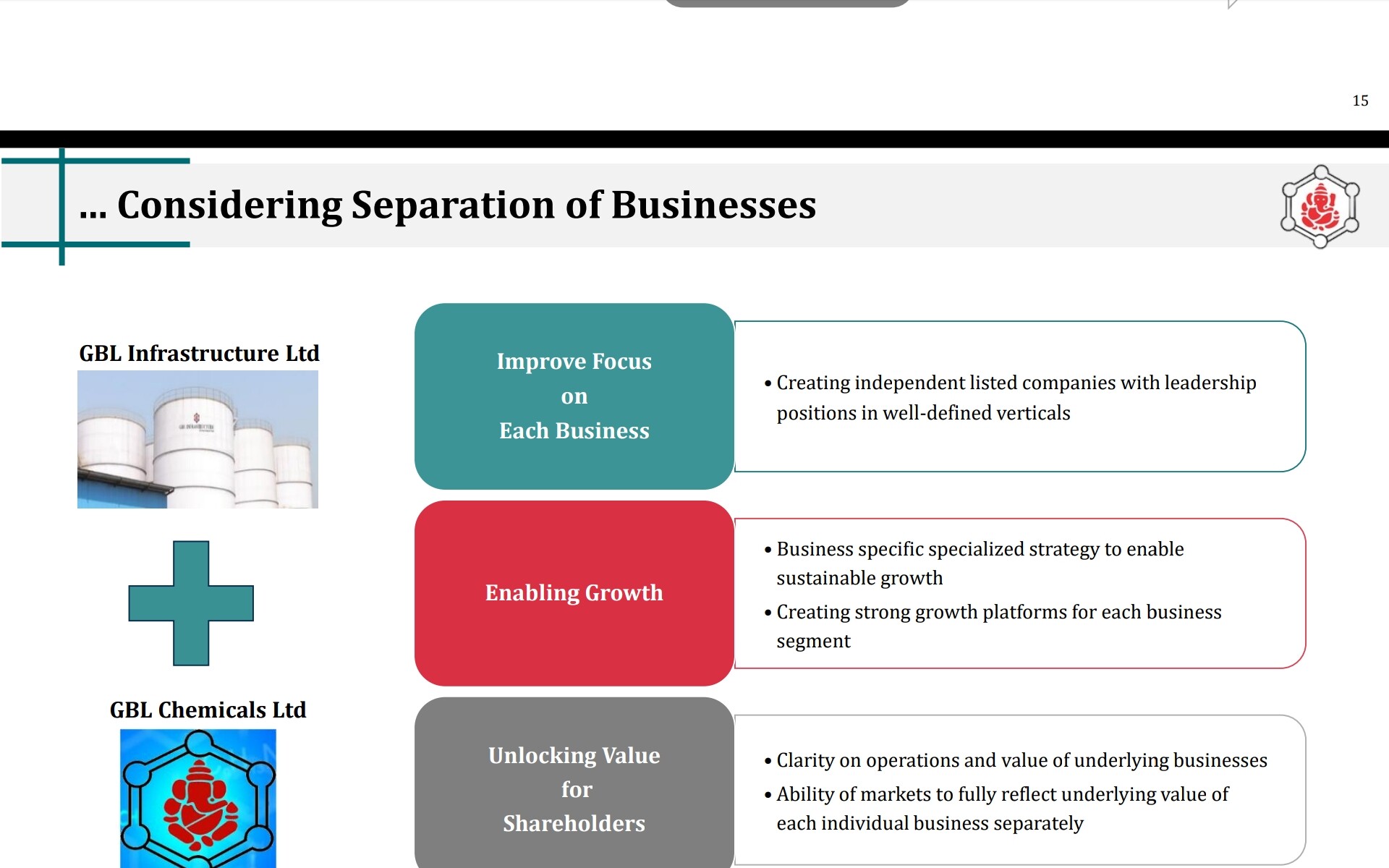

demerger intent called out by company in today’s presentation uploaded , while also acknowledged that chemical business need Capex and is capital intensive. To be seen as to how existing shareholders gets allocation. Sequence of events are encouraging and management is being transparent, One first stolt came on board recently with a board seat. As well as recent preferential issue to promoters to infuse capital.

GBL infra once demerged stands to be valued as a niche high margin business with strong entry barriers, predictability of performance which market likes, and on its own may command higher valuations than current market cap .

GBL infra current runrate annually could be 150 cr+ revenue and PBIT margins in vicinity of 45-50%, PAT of 45-50 cr type - a conservative valuations will be 700cr + with 15PE

No growth visibility in both the biz aka LST and Chemical is hampering its valuation. Without addition of new capacity or tank farm it wont get the fair value. U are right market likes growth and visibility which it lacks. Management wont be able to growth LST with same pace as it is 100% utilized so they brought in Stolt so that the topline growth can be shown but again after some quarters would it be able to add much to topline. Management did not give any idea about how they are going to grow in future…no roadmap except one sheet about demerger even no mention of demerger time. This bull market dont have interest in no growth stories what ever be the profit. What is EPC biz ROCE? would it be anywhere near to LST? and if not then why expand it…?why not giving profit as dividend?..also slow reduction in debt indicate that the biz is capital intensive and does not throw free cash flow.

Disc: Holding

The Co. is believed to be actively pursuing the adjacent plot at JNPT. As they are already the largest operators there, they do seem to have sufficient clout. As and when the allotment comes about, it will more than double their existing capacity. That would certainly be a big game changer in terms of getting its due valuations at the bourses. Till that happens, the Company will incrementally keep increasing capacity by adding the height of the tanks. Together with annual increase in lease rentals, one would see YOY growth.

The Stolt rail logistics company will further increase the bottom line by 8-10 crs in a full year.

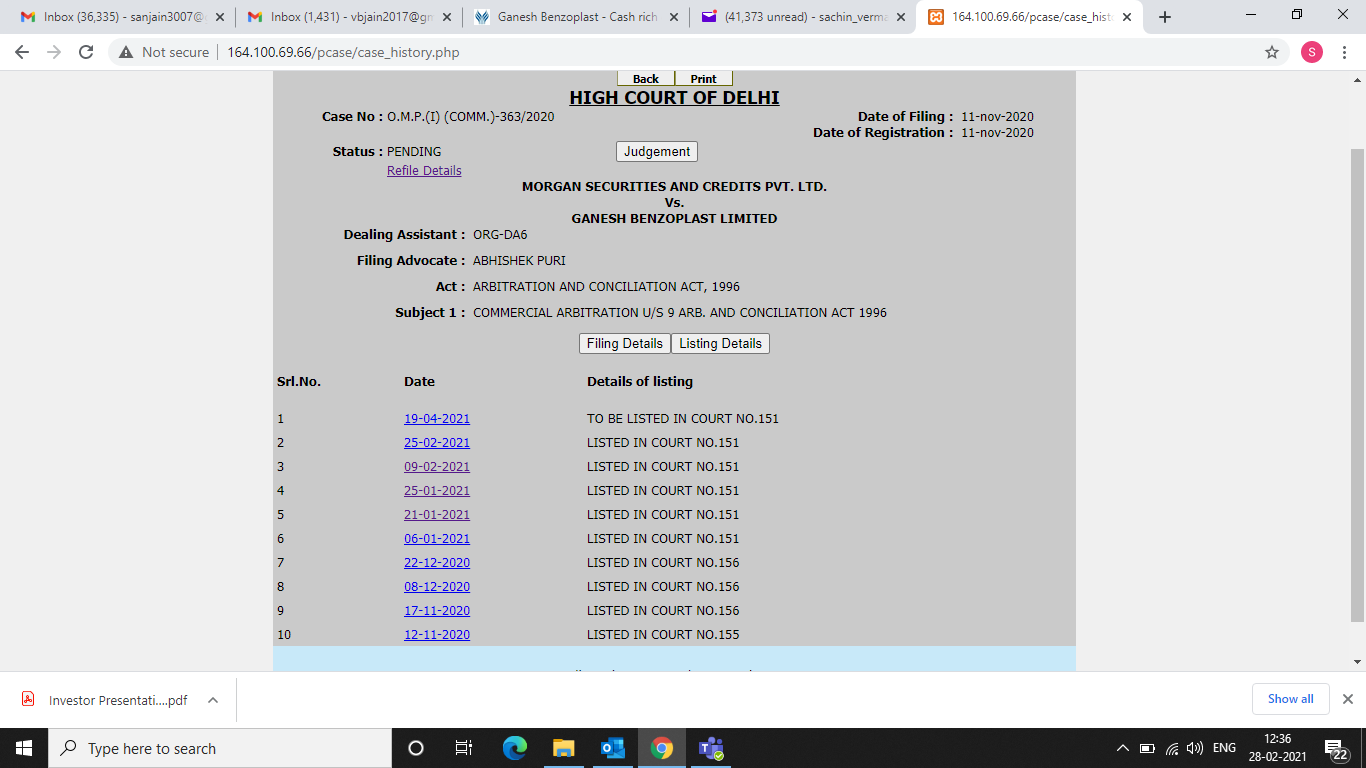

Yet another trigger would be the settlement with Morgan Securities. The matter is with the Delhi High court and the verdict is expected sooner rather than later. This is also holding up the demerger which is another potential value creating opportunity.

There is enough in this story to keep one interested!

I read the bse announcement regarding preferential allotment but couldn’t find the price at which shares have been allocated. Could you please point me where to look for the price of preferential allotment.

It appears that entire demerger and restructuring was called out in much more details in this May 19 article- appprox 2 years back

If that was the case, this doesn’t seem to be a current plan and something which was conceived few years back and for various reasons got delayed in execution.( most

Key one being formal NCLT approval for BIFR exit)

Today market reaction with good price volume action seems positive after 2+ months of consolidation, expecting some firmed up execution on demerger with some concrete action items around legal/approvals etc being called out.

Chart looks good, A breakout above 77 with good volume will open a potential upside as near 52 wk high zone

It is an year old settlement…year 2020 .

From recent presentation on page 6 Total tanks=83 but on page 8 its total 63+12+4=79…may be some error.

If we go by this past report https://www.nirmalbang.com/Upload/Investment%20Picks%20Diwali%202016.pdf

JNPT has seen capacity expansion of about 11-12% which is slow by any means that too in 4 years…so they better start buy some new land and stop reinvesting in capacities by increasing height of tanks which seems a costly affair. Addition in gross block is 488-436=52 crore (there would be some maintenance capex) from FY-16 to FY-20, looks high for 11% increase. Above report also mentions about expansion at adjacent land but nothing has happened till now.

My bad …Indeed 2020 settlement. Thanks for pointing out.

Market in its own wisdom seem to be rewarding and factoring future prospects, with price moving above 52 week highs with good volume, thats comforting else would have been frustrating in broad bull market rally where every other stock flying high.

Growth Trackers 1. Tank Expansion in existing Land

Management has increased the capacity by more than 27% in last 2-3 years which they were mentioning since last many annual reports they are increasing capacity by refurbishment of tanks and so on.

4.Stolt Rail Logistics - Increase in Topline and will increase margins being only service provider from port to rail in JNPT.

5. Goa Expansion - Not able to get clearance from Goa Pollution boards till October 2020.As Stolt has joined the board maybe it will resolved in coming period.Goa Expansion October 2020.pdf (3.0 MB)

6.EPC services providing end to end solution - At present, it seems that this business is adding to topline only, may be in the coming period it should start adding to the bottom line as well.

“1 of the Few contractors to design & construct tanks as per API 650 12th Edition in India”

7.Chemical Division - Raw materials - Magnesium oxide and Toluene prices needs to be tracked being major raw material .

Ganesh Benzoplast enjoys virtual monopoly in Benzoic acid and its derivatives being food preservative in India.

Lots of growth triggers keeping us busy to track .

The above judgement sets the way forward for all the NCLT cases of Ganesh Benzoplast including the Morgan Credits case (which is blocking Demerger). The court has ordered Ganesh Benzoplast to pay to the creditors as per the terms set by BIFR (25% of outstanding in five equal annual installments).

With Stolt on board the company can take big capital intensive projects in hand by making preferencial allotment to Stolt and by raising debt. Good future prospects.

Any idea about todays court order in Morgan Case?

Now this thread is rolling…

My investment thesis was simple “since 2015 chemical sector was on boom and use of oil products would only increase” but it would take this much of time to play it out was out of my thinking. I started to track it in 2017 when it was in 40s and invested in 2020 only at 50s with same conviction of export and import play. Management is bit rusty in communication with very low capacity the way forward would be to expand and lets see how it pans out from here onward.

Thank you all hardworkers here

To meet the growing demand of the liquid cargo JNPT has proposed to develop a liquid jetty of 4.5 MTPA at a cost of Rs.309 Crore. The DPR for the project is completed and the work on the new liquid terminal, of 4.5 million tonnes annual capacity. The jetty will have twin berths to handle 70,000 DWT vessels on one side and 25,000 DWT vessels simultaneously on both sides of the jetty. The work is award to M/s. ITD Cementation.

Benefits of the Project

Capacity enhancement of 4.5 Million Tons of liquid cargo in JNPT. The waiting period of vessels shall be reduced and it shall benefit the importers.

Status

Estimated Cost: Rs. 190,00,00,000 /-

Contract award Price: Rs. 181, 50,52,000/-

Name of contractor: M/s ITD Cementation India Ltd.

Date of award: 31st March 2019

Notice to proceed & Date of Signing of Agreement: 17th January 2020

Date of commencement: 16th February 2020

Contract Duration: 30 Months

Scheduled date of completion: 15th August 2022

Name of design Consultant: IITM, Chennai

Name of PMC: Tractebel Engineering Pvt. Ltd.

Top side design consultant: M/s RINA Consultanting S.p.A

Physical progress of work as on 10th February 2021: 26.16 %

Financial Progress as on 10th February 2021: NIL (Milestone based)

JNPT Liquid port is increasing the capacity which is an indication that there will be an additional tanks will be required for storage and very good chances of shortage of Land which has been clearly stated by Ganesh Benzoplast in Annual report .

So acquisition of Stolt will be adding advantage to Top line and margins as Liquid will flow from port to rail to final destination (factory), considering shortage of land in JNPT for liquid storage. (Unique service in port)

Further expansion by GBL should complete in line with the expansion with JNPT liquid port expansion if at all it is going on.

One thing which is worth tracking for expansion is capital work in progress standing in the books of Rs.11.68 cr as on 30th Sept 2020.

Vishanji Dedhia is continously increasing the stake since last many quarters.

Further Kailash Agarwal and his son Nishant Agarwal also seems to increase the stake post preferential issue. Avighna GroupLeadership

It seems that Big players are entering the stock very aggresively.

.

. …Indeed 2020 settlement. Thanks for pointing out.

…Indeed 2020 settlement. Thanks for pointing out.