Q4 Earnings con-call highlights -

• Competed 4 decades. Profit compounded by 28% CAGR in 4 decades

• Operating cash flow in excess of 300 cr. ROCE = 23.5%

• Decline in Revenue in FY 20 is primarily due to decline in Fatty Alcohol Prices. Prices are likely to remain soft in the coming months.

• Update on Tarapur plant- Shutdown of pant will impact Q1 FY 21 (plant was closed for 1 quarter). 8 to 10% volume contribution through this plant.

• Capacity utilization – was around 61% for last year - enough headroom to accommodate additional demand.

• Capex - Last year capex was 230 cr for Jhagadia plant. Capex for current FY deferred by 6 months.

• Demand for performance surfactants remains stable. Demand for Speciality products likely to be impacted by down trading due to decline in consumer incomes.

• Product innovations launched in FY 19 receiving good response from clients.

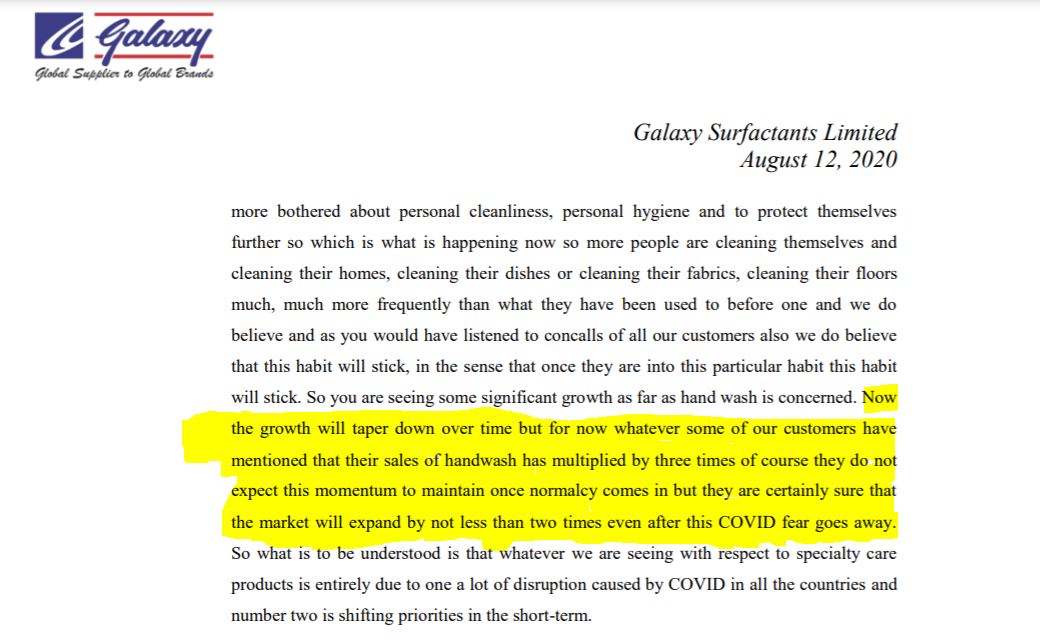

• High emphasis on cleanliness & hygiene

o Personal cleanliness and hygiene very high among end consumers.

o Washing hands frequently + high on home cleanliness. Whether it’s a sustainable trend or not remains to be seen.

o Company is supplying to almost everyone who makes hand wash. Well positioned to meet demand growth owing to increased focus on hygiene.

• International business constitutes 65% of revenue

• AMET Market outperformed on the back of strong growth registered by the local Egypt Market

• Local Egypt market – demand is almost back to its original level.

Client concentration - 55% revenue comes from MNC clients. Has reduced its concentration in last 1-2 years

. Company does not have any direct competition in listed space in India. International market - BASF is one of the major competitors

Hello Dinesh, I have gone through the link and the comments from the Chitoorgarh page, but It is not clear to me whether Galaxy promoters are involved in price hike or Operators blackmailed them but it didn’t work and Galaxy withdrawn the issue instead. because it is important to know if promoters were involved in this or not. any info on this?

Sorry. I have not been tracking this. That initial post by me was something interesting I found back then. I did not follow up on it. If you find more bread crumbs, please post here.

Thank you.

Did You find any info about whether fire broke out or not? all news claimed there was fire but management denied it. the photo in the news link is representational.

any update on why the accident happened? I hope it is not due to any rush to start the plant.

@r13rk

One of my friend working in Galaxy tarapur plant. So he told me, Accident happened due to mis-operation causing runway exothermic reaction.

so this mis-operation a management fault like wrong decision, started with less man power to handle the plant etc or the workers caused it accidently? plus any info if the fire broke out or not?

Actually fault of plant level management that poor production planning, started batch in rush with less manpower than regular requirements.

Fire was get catch in plant but local MIDC firefighters team done very well job to control it before it taking serious outbreak.

My professional working sector is Pharma API and speciality chemicals. I have been working from 5 years.

Really speaking that incident was bad fate, I know Galaxy is very good organization and care about employees. Because I had taken personally review from many employees who working there.

Why the promoter selling small quantities from last month, that too when their result is about to come out?

Unnathan again sold 578 shares today and the Q1Fy21 result is due tomorrow. What is this?

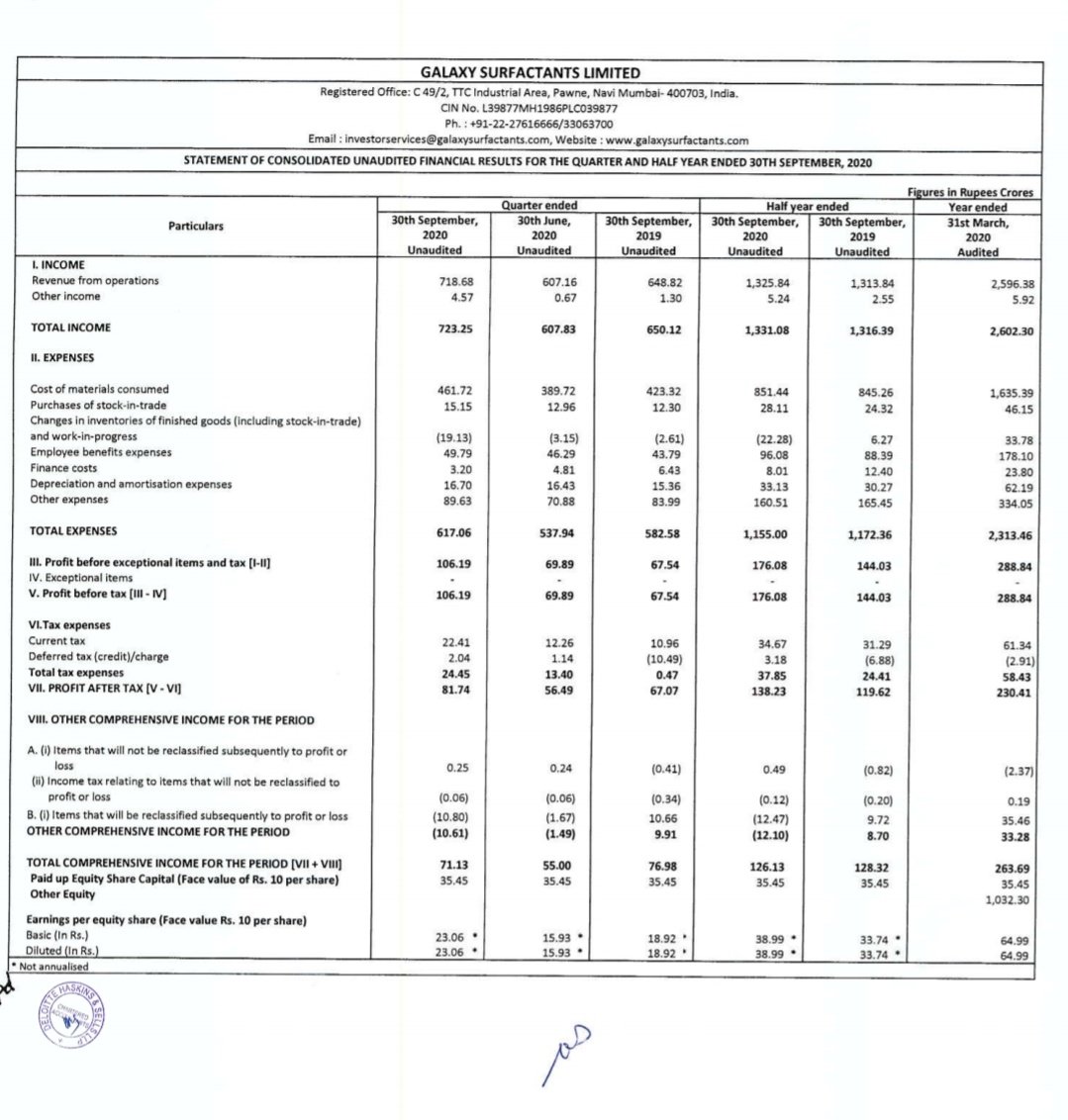

Fatty Alcohol accounts for over 50% of raw material prices. While going through past concalls, I noticed management mentioning a decline in fatty alcohol prices impacts their topline. Does it mean,

- company follows a cost plus model wherein changes in RM prices are passed on to customers ?

- Given how raw materials prices are volatile, would their end products will also have a volatile pricing ?

the company has a pass through for raw materials with all client contracts … meaning the topline might fluctuate but the ebitda will always be in the same range due to such provision…

The stock has already reached target mentioned in research report & has started correcting after touching psychological levels of 2000. Currently we are around technical support levels of 1700 and Q2 numbers should provide it direction for further movement.

Another FMCG company came with typical comment on Sanitizer market – the way it was envisioned, it hasn’t panned out that way. Their sanitizer product was great at the start but now sales down due to crowding of the market. Sanitizer contribution - Mid single-digit earlier now half of it.

If it is true for all other producers, we may loose thrust provided by covid to this sector.

Has anyone noticed that the promotor group has been selling shares consistently in small tranches for sometime now? Any idea why?

https://trendlyne.com/equity/insider-trading-sast/all/GALAXYSURF/74800/galaxy-surfactants-ltd/

Nirmal Bang initiates coverage on Galaxy Surfactants

Established position in the home and personal care intermediates market:

The GSL group has for over four decades been engaged in the manufacture and sale of surfactants and specialty chemicals used as intermediates by the HPC industry. The group is one of the leading players globally in the HPC intermediates industry, driven by long-standing customer relationships. It caters to a large client base of over 1,750 customers across 80 countries, consisting of reputed HPC FMCG multinationals and domestic customers. The group caters to three regions namely India (35% of revenue), AMET (32%) and ROW (33%). Wide geographic and customer diversification de-risks its exposure to a single geography. Its products find applications across mass, mid-price and prestige range of customers.

Julian,

Please do not believe in 3rd party analysis. Please go to the source, in this case, the 2011 DRHP to get the actual figures. The figures in financial statements in this DRHP are in mn. and not in cr. so the actual total revenue was 594.18 cr and PAT was 40.342 cr.

Hello everyone. Thank you for the great discussion on this thread. I have some points to share:

- I have heard that Galaxy is able to obtain international customers through references. E.g. if HUL is their client in India, then HUL refers them to other international Unilever subsidiaries.

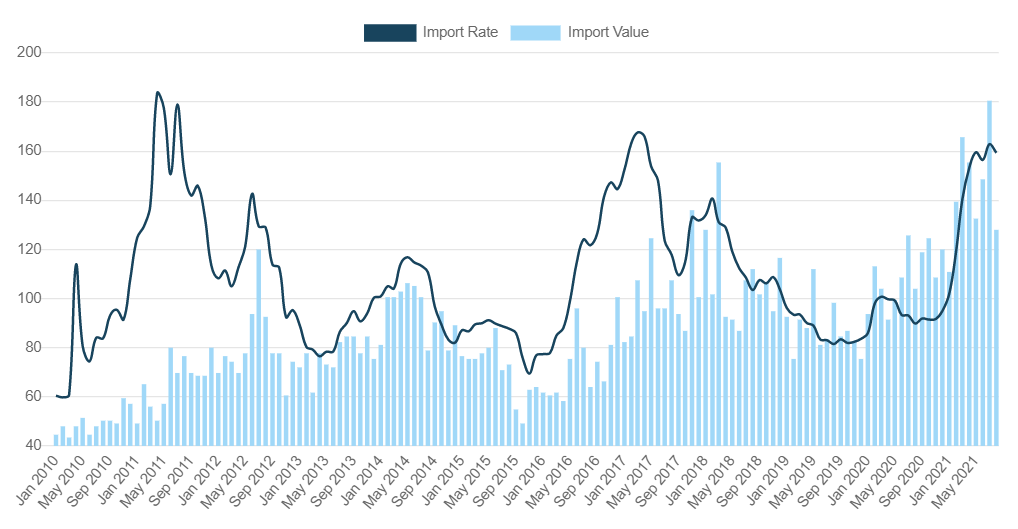

- Since lauryl alcohol is a large part of their RM, here is the price trend:

Not sure if this is correct, but if we apply a technical analysis viewpoint, historically prices have seen a ‘resistance’ around Rs 160/kg (where it is currently trading). This could possibly be a cyclical peak in lauryl alcohol prices, which may lead to lower RM cost as % of revenue (hence higher margins) in next 2-3 quarters

I also have some silly questions, if someone can please answer them:

- Are they giving the margins in performance surfactants and value added surfactants?

- Is there any possibility for backward integration for lauryl alcohol?

- Are there domestic suppliers available for lauryl alcohol instead of importing from Indonesia/Malaysia/Thailand?

Thank you.

Disc- not holding but researching and tracking closely