Also Just to highlight

Have checked promoters background from various Unlisted small players in Precision engineering background who runs 1-2 furnaces in Gujarat saurahstra

As per them the promoters are as clean as they can be

Disclaimer - Invested position size above

3 Likes

Just to make sure, you are talking about promoters of Galaxy or SKP?

Both SKP and Galaxy bearings

1 Like

Sir, your views on Q3 results Fy24?

- Interesting insights from galaxy bearing founder stating that expansions plan, key customer , revenue bifurcation

- Link :https://youtu.be/ygyf4W54XCU?si=HqRRh6ihyK-ztMuq

2 Likes

Quaterly results not upto the mark. Quaterly result of other listed peers were too under pressure for Q4, due to low demand in exports. Any updates are welcome.

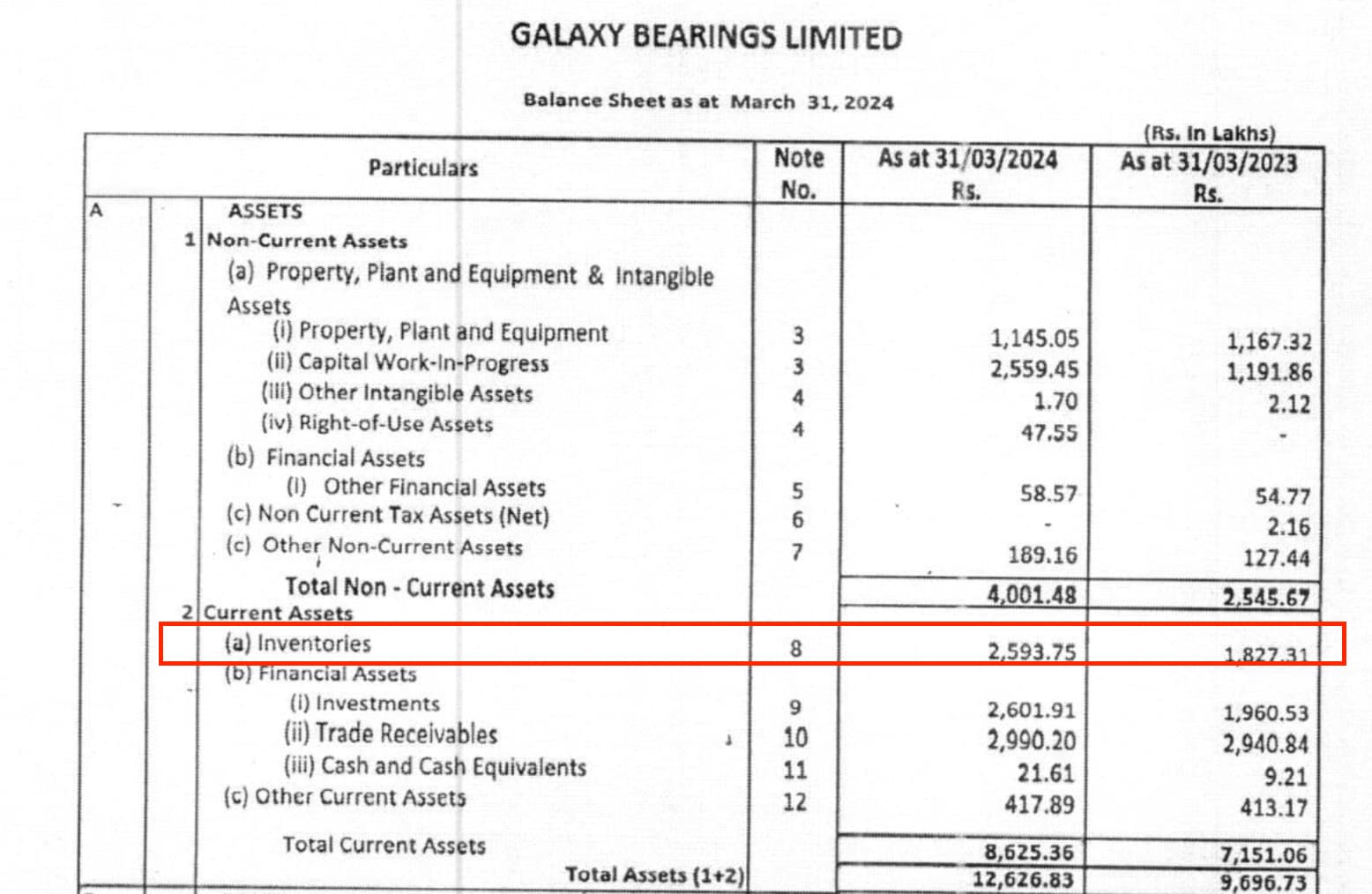

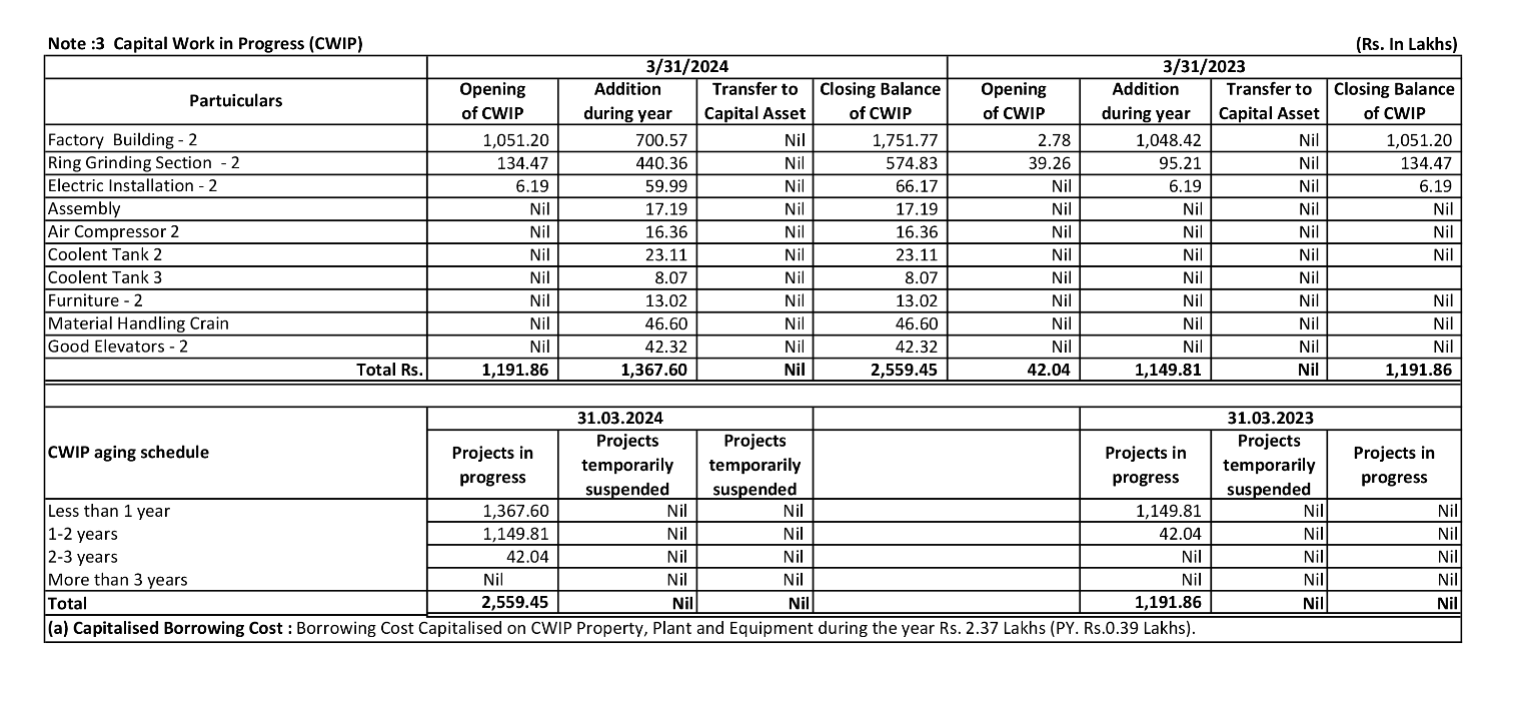

Galaxy announced a fair set of numbers today and seems to be making significant progress on the CAPEX front (CWIP up to 26 Cr for March ending, out of their assumed CAPEX of Rs. 35 Cr).

Providing a summary for everyone on this thread (and myself to refer back to):

Background: company was founded by Mr. Vinod Kangsara (passed away in 2019) - current main promoters are his wife (Indiraben Kangsara) and daughters (Shetal Devang Gor and Tuhina Bera) - who now seem to be NRIs and aren’t actively involved in the business operations. CEO is Mr. Nitin Santoki - who seems to be Rajkot based with a strong presence in the industry (no information on his shareholding). It seems that Mr. Nitin’s family has other companies in associated fields of the industry (common in auto ancillary businesses, wouldn’t consider it to be a corporate governance issue - refer to the link for Adico group below).

Catalyst/Trigger: Change in management post 2019, might have triggered a new approach to the business(speculatio). Dr. Devang Gor who is a Chair at the Department of Radiology in a leading healthcare network in Pennsylvania, USA was appointed on the board in August 2019 after completing an Exec MBA from Temple University (potentially to groom him for this role?).

Key business trigger seems to be a new product development as mentioned by Mr. Nitin in his interview (https://www.youtube.com/watch?v=ygyf4W54XCU&t=1s) - where they are manufacturing roller bearings with a hub casting attached. This saves their customer the time, effort and the cost of otherwise attaching the hub casting separately to the product.

It seems another competitor offering a similar product is Orbit Bearings (also Rajkot based), who has grown significantly by being the first taper roller bearing company to manufacture these bearings with a hub casting (Cylindrical Roller Bearings | Truck Axle Bearings | Taper Roller Bearings | Truck Hub Bearings | Orbit Bearings India Pvt. Ltd.). Orbit Bearings has scaled significantly and did a revenue of Rs. 624 Cr in 2022 with a PBT of Rs. 151 Cr. Orbit has a capacity of 10 Million pcs per annum, and it’s interesting to note that Galaxy has decided to set up a plant which takes their total production capacity to 9.5 Million per annum (in Phase 1)! Other smaller competitors also seem to be equally profitable (Turbo Bearings does a Sale of 99 Cr with a PBT of 27 Cr).

Has anyone studied the bearing industry in greater detail to check how they compare with SKF, Timken, Schaeffler?

https://www.adicogroup.com/international/group-of-companies.html

7 Likes

Few info based on CEO’s 2024 YT video during Delhi Expo and 33rd AGM video:

- Exports share ~75%

- Clientele includes Tier 1 / 2 suppliers to OEM as well as distribution players - for their private labels; OEM / Tier 1&2 (~25%) and After market private labels (~75%) are focus segments

- CV esp. heavy vehicles come up as prominent segments

- Auto is 60%, Agri 15% and Industrial 15% (based on AGM inputs)

- Focus geographies - Germany, Italy, USA, Turkey and UAE

Additional info from Timken concall - exports had one of the worst quarters with 15% share vs ~30% share during good times. Heavy vehicle segments really struggling with exceptions being rail road and South American market. Even India / domestic market had railways and industrial segment driving growth.

While MNCs like SKF, Timken along with Rolex had very healthy Q4FY24 with topline and margin expansion leading to serious re-rating - Galaxy’s flattish Q4FY24 results (YoY basis) DO NOT seem that bad in light of exports and heavy vehicle headwinds. Sharp QoQ uptick, high inventory levels (might be attributable to Red Sea in case they have exposure to related geographies) and upcoming capex (phase 1 potential commissioning in Jun / Jul) suggests that upcoming quarters may be worth watching out for.

Disc: Have exposure with recent purchases within last 30 days

2 Likes

Further deep dive into Orbit Bearing’s numbers: Managerial Remuneration is 22 Cr which means we’re talking about an opportunity in a 27% PBT Industry.

They did a gross margin of 42% (FY23) and a pre tax RoCE of 20.30% (FY23) and 26.20% (FY22) - post managerial remuneration.

Cash Conversion Cycle seems to be 298 days for FY23 - which is what’s dragging RoCEs down despite such high margins.

Property Plant and Equipment was only 89 Cr in FY23 which means they have fixed asset turns of over 7x.

This is similar to Galaxy’s numbers where on a gross block of 20 Cr they do a revenue of 127 Cr.

Not to get ahead of ourselves but assuming a Fixed Asset Turn of even 5x (assuming land is more expensive now) - they should be able to add another 175 Cr of business with Phase 1 of this CAPEX. If we go by the capacity they’ve added, it should take them closer to Orbit Bearing’s numbers (who has a capacity of 10 Million).

Disclosure: invested in my own and other family accounts, views may be biased

3 Likes

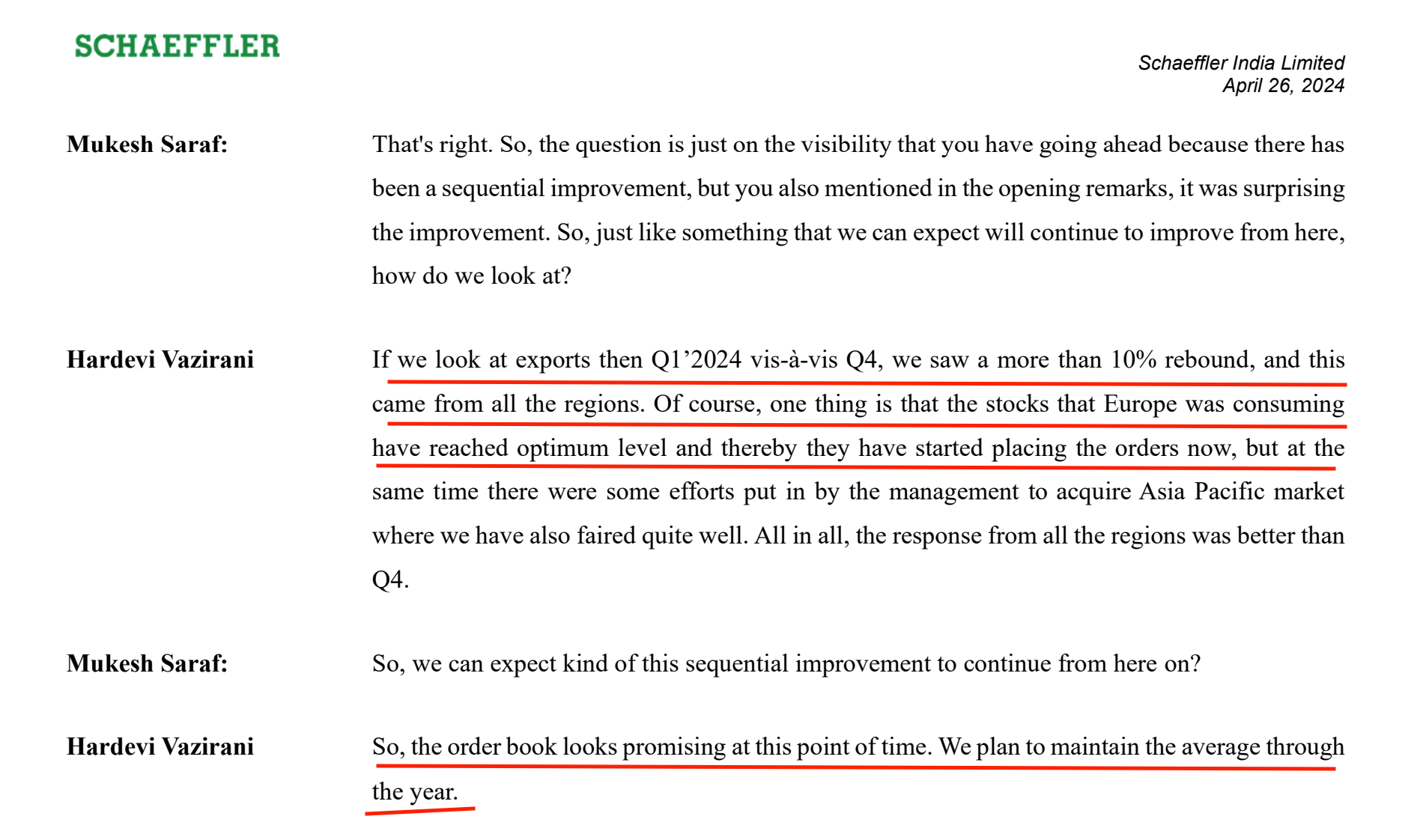

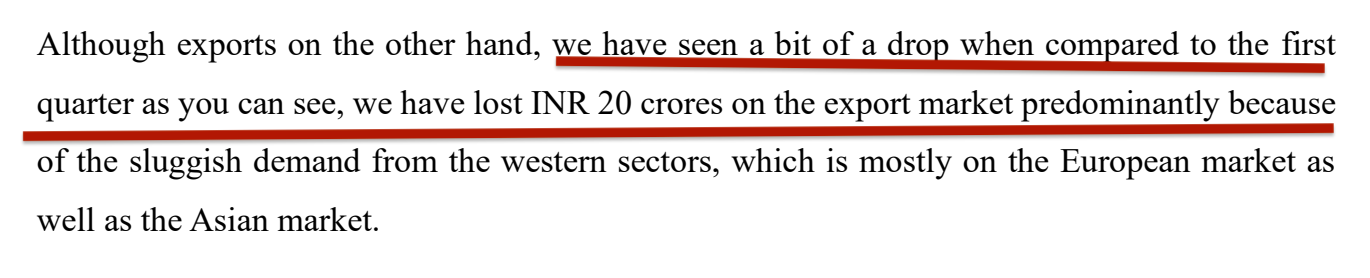

Schaeffler India Ltd saw dip in exports on YoY basis though did witness QoQ growth. Seems, uptick driven by low channel inventory and improvement in the industrial segment. Do note than Schaeffler’s FY is same as CY i.e. Jan - Mar is Q1FY24 rather than Q4FY24.

2 Likes

Does anyone know when will the capex be completed?

Had mailed the IR regarding the update on capex focused on expansion of capacity from 2.1 Mn to 9.6 Mn. As per the response “The capex plan will be completed by the end of the FY 2024-25” . Thus it seems that it is delayed as a timeline ~ Jul’24 was shared by the management in an interaction during Delhi Expo’24. May get more granular input during the AGM scheduled on 28th Sep’24.

9 Likes

Do we know whats the current factory utilization? Looking at the weaker demand in the European and USA market, the order infow may not be that great. In addition, the iron steel price is also in downward journey impacting the tompline. In my opinion, following factors to be watched out closely

-Uptrend in the European and USA maket

- Higher row material price

- Freight cost /Red see Issue normalization

1 Like

An extract from FY24 Annual report -“India Bearings Market size is projected to grow at a CAGR of 13.5% during 2024–32. (Source: 6Wresearch) due to growing demand for specialized bearing solutions and improved designs to increase product performance and efficiency. However, the outbreak of corona virus pandemic would impact the automotive and other industries affecting the bearings market over the coming years, though the effects might be short lived.”

I dont understand why they are still in “Corona virus era still”

Page 56 -“The global bearings market size is expected to reach USD 271.99 billion in 2023, registering a CAGR of 14.01% over the forecast period, according to a new report by Grand View Research”

I dont know what to make of this statement. The incharges, CFO/ Promoters seem less serious on reporting to shareholders.

1 Like

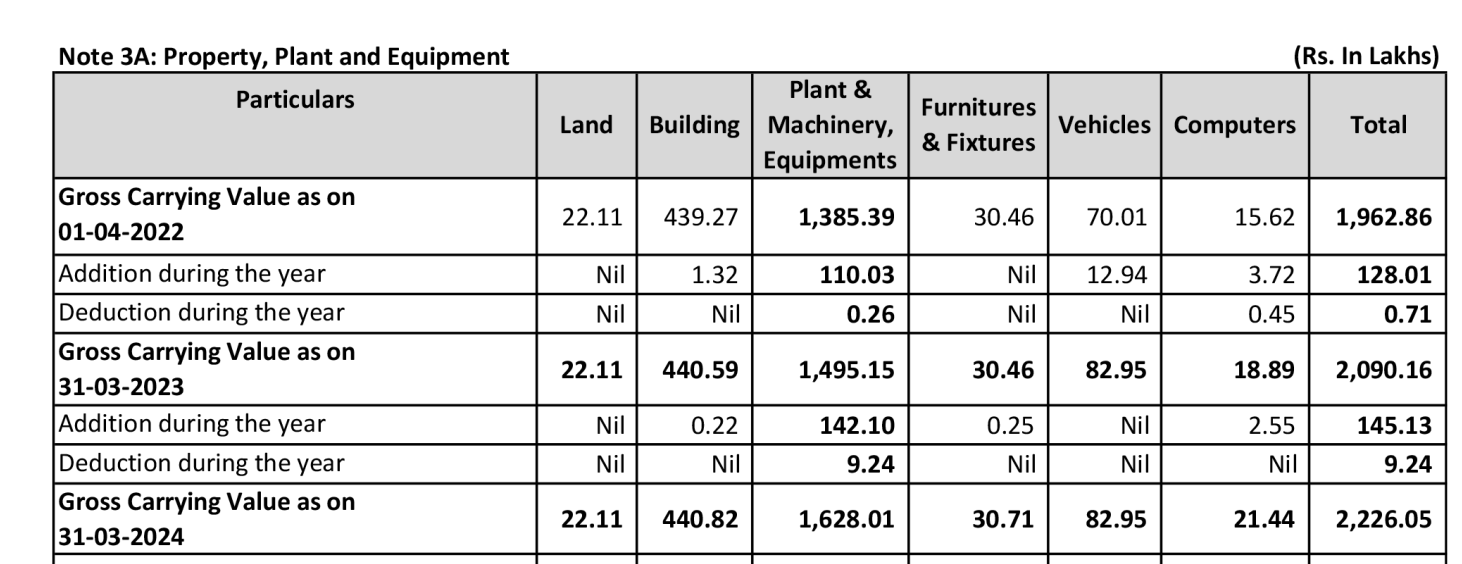

The Annual report provides detailed breakup of the CWIP, however management commentary around specifics like estimated capacity increase as well as timelines for going live, is missing.

Just to put things in perspective, the CWIP value is more than the Gross value of fixed assets i.e. Land, Building, PPE etc., hence it is substantial (even if you consider inflation). Let’s see if management provides better clarity on this development during the AGM.

2 Likes

New update and guidance:

40123e4e-4d13-4031-bb1d-4de4356cc182 (1).pdf (540.8 KB)

1 Like

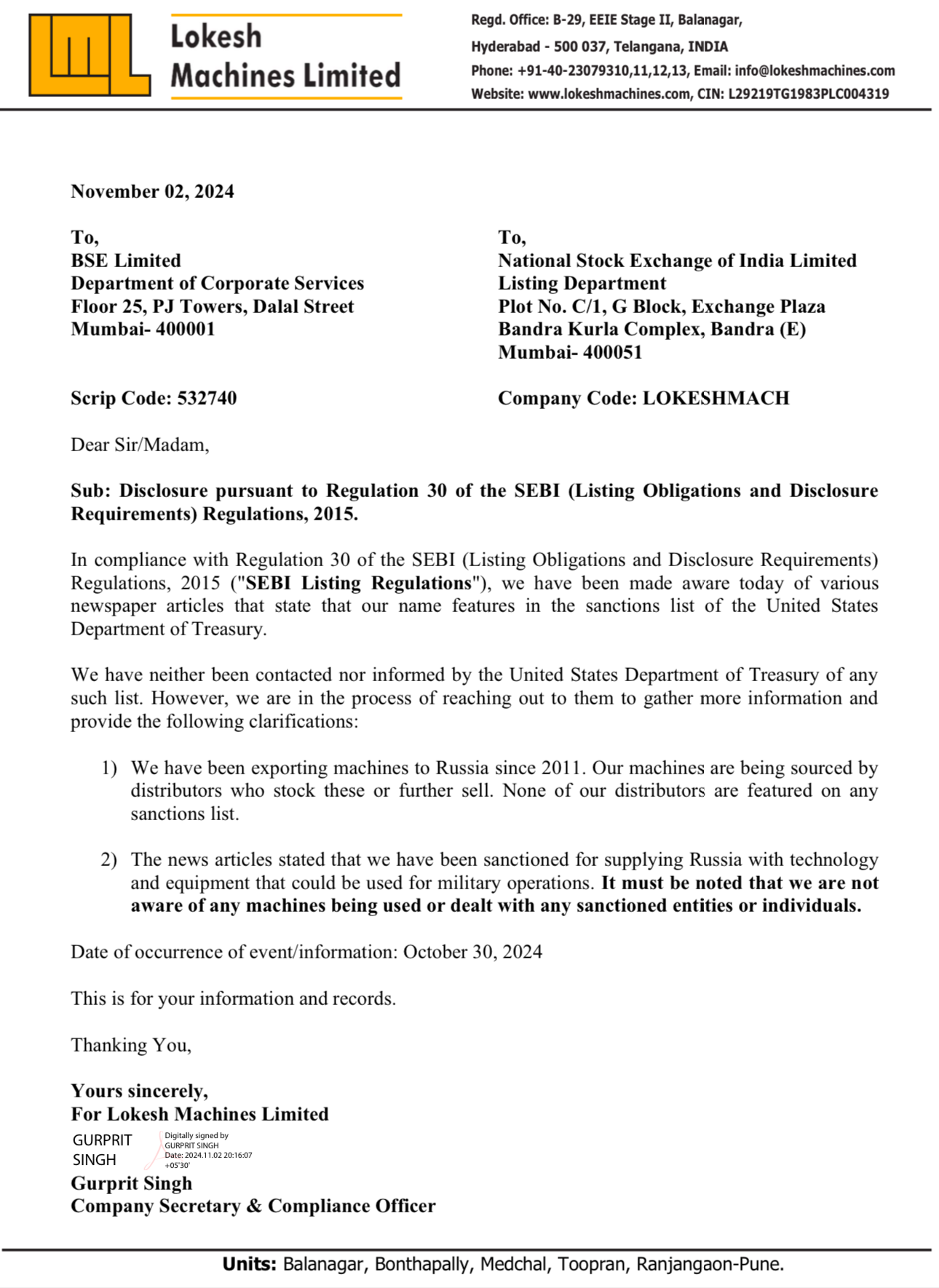

What is the implication of USA puting sanctions on some of the Indian cos including Galaxy Bearings for supporting Russia’s military industrial base?

Article:

https://www.business-standard.com/external-affairs-defence-security/news/us-sanctions-15-indian-cos-for-supporting-russia-s-military-industrial-base-124110100762_1.html

How much % revenue comes from USA since Galaxy bearings is export oriented business?

Clarification by one of the companies mentioned in the list, Lokesh Machines with Mcap of INR 650 Crs.

Company response

https://www.bseindia.com/xml-data/corpfiling/AttachHis/733a2007-9944-4545-b042-e4194fb6994d.pdf

Any Update on this co. ?

**All major headwinds appear to have been absorbed. The risk-reward from current levels looks asymmetrically favorable.

any comment on Valuation part ?**

1 Like