Dear VP’s,

Thank you for this wonderful community, where newbies like me can seek genuine advice which is not distorted by any incentives.

Below is my risk profile & financial situation: as I think without knowing risk profile, the advice might not be relevant.

Profile: 31 years old Engineer, Father of a 2years old son, working as a consultant with telecom vendors, saving a decent amount on contractual basis which is usually for 6 months extendable contracts, I never worked as full-time employee as I came to know early on that contractor make more money than full-time employee with some risks, which I was happy to take.

Risk: I may lose job any time, currently have visibility of next 6 months only, also the telecom market is in a structural downturn, so I really don’t expect to find any contracts after 2-3 years, though I intend to work more 4years.

Financial setup: Already made a new home, bought some land worth 1cr at the peak 2014, which is now worth much less(Was my biggest financial Mistake), I intend to sell it.

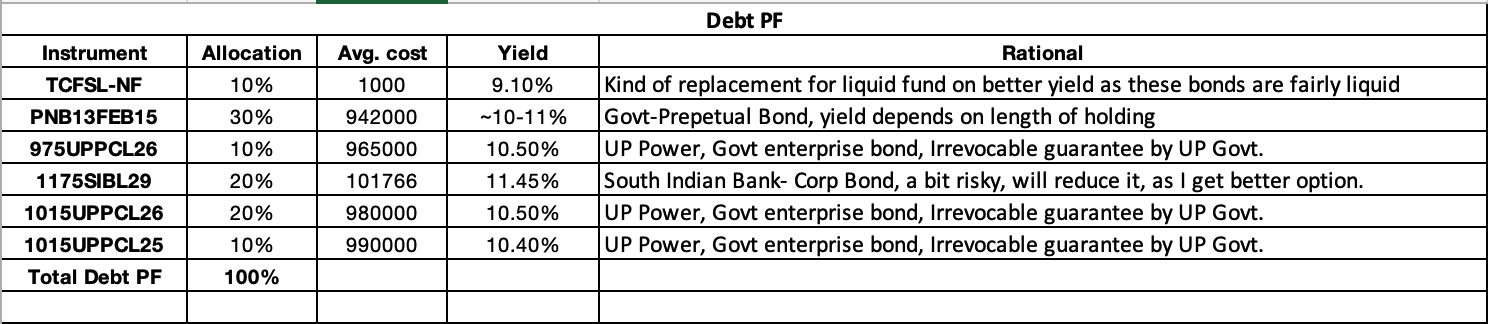

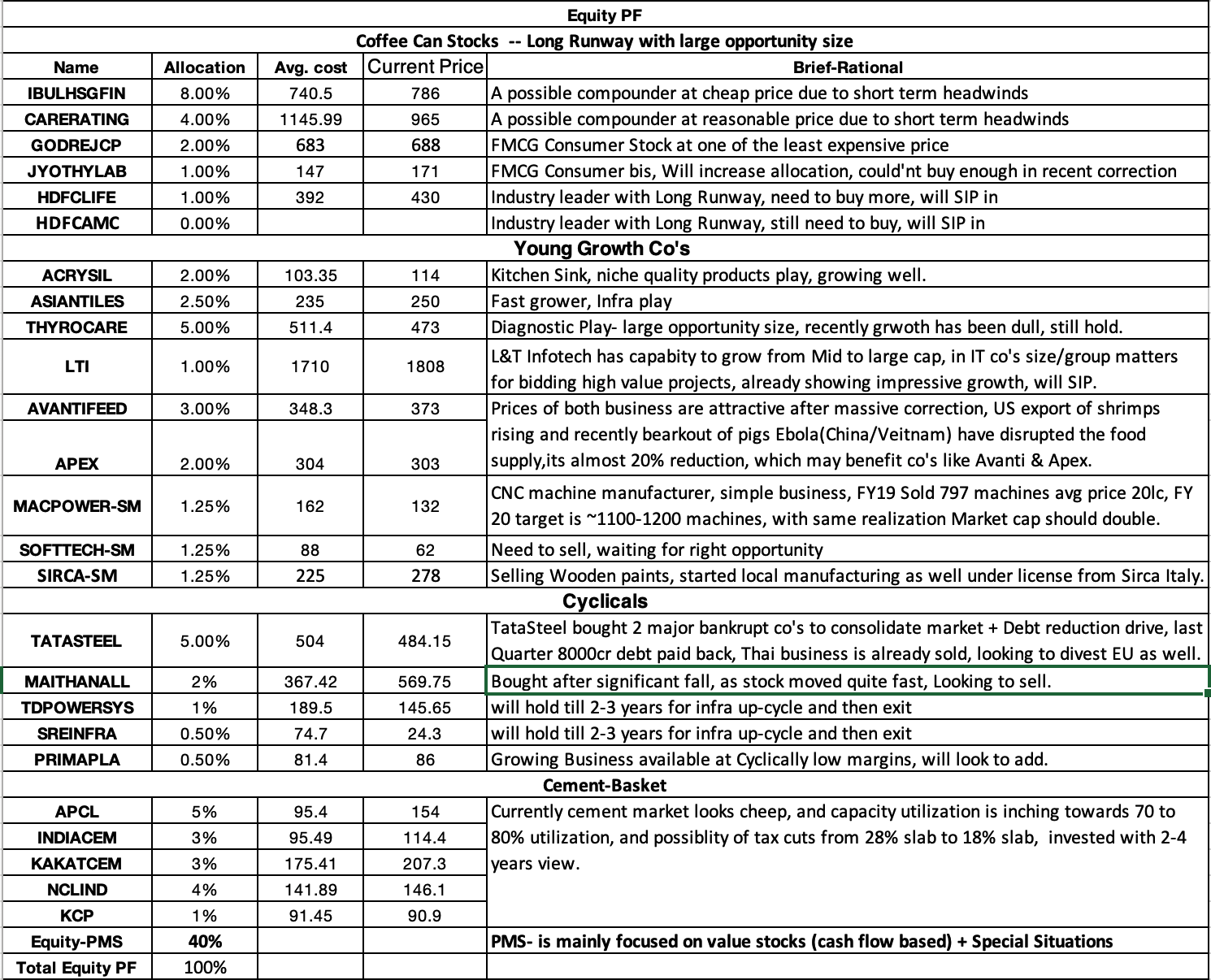

have a total of 2.2cr of financial saving, out of which 1cr is invested in equities, rest is in FD+ Liquid funds.

Objectives and Target: after 4 years, I expect to have a total of 1.7 to 2lc spending each month, I know it seems quite high with respect to my capital base.

I started investing in equities since 2016, CAGR is decent(24%) not great, it’s lower due to a lot of churning I was doing, I sold my full PF(30 stocks) in Jan 2018 due to valuations concerns and bought single stock Shemaroo and in March 2018 I bought few other stocks as per below details.

Current Fresh Equity PF:

Stock Name: Allocation %age, Avg Price, Type, Brief thesis.

-

Shemaroo: 35%, 440, Core-Long term, Digital India growth play, Business protected by Ownership Rights of movies, increasing cheap 4G penetration is a huge plus, a high leverage business with tailwinds(demography + cheap data)

-

Reliance Capital: 30%, 425, Non-Core, Contrairian value buy for short to medium term, Anil Ambani group’s crown jewel reserved for next genration(Anmol Ambani), all other co’s in Anil’s kitty did poorly, But all the business in reliance cap(RNAM, R Genral Insurance, Life Insurance, R Money) are doing well and in tailwinds as well, Value buy at 0.6x of book value, + non core investment worth more than 10K cr’s which is almost equal to market cap, they intend to monetize all non core investments.

-

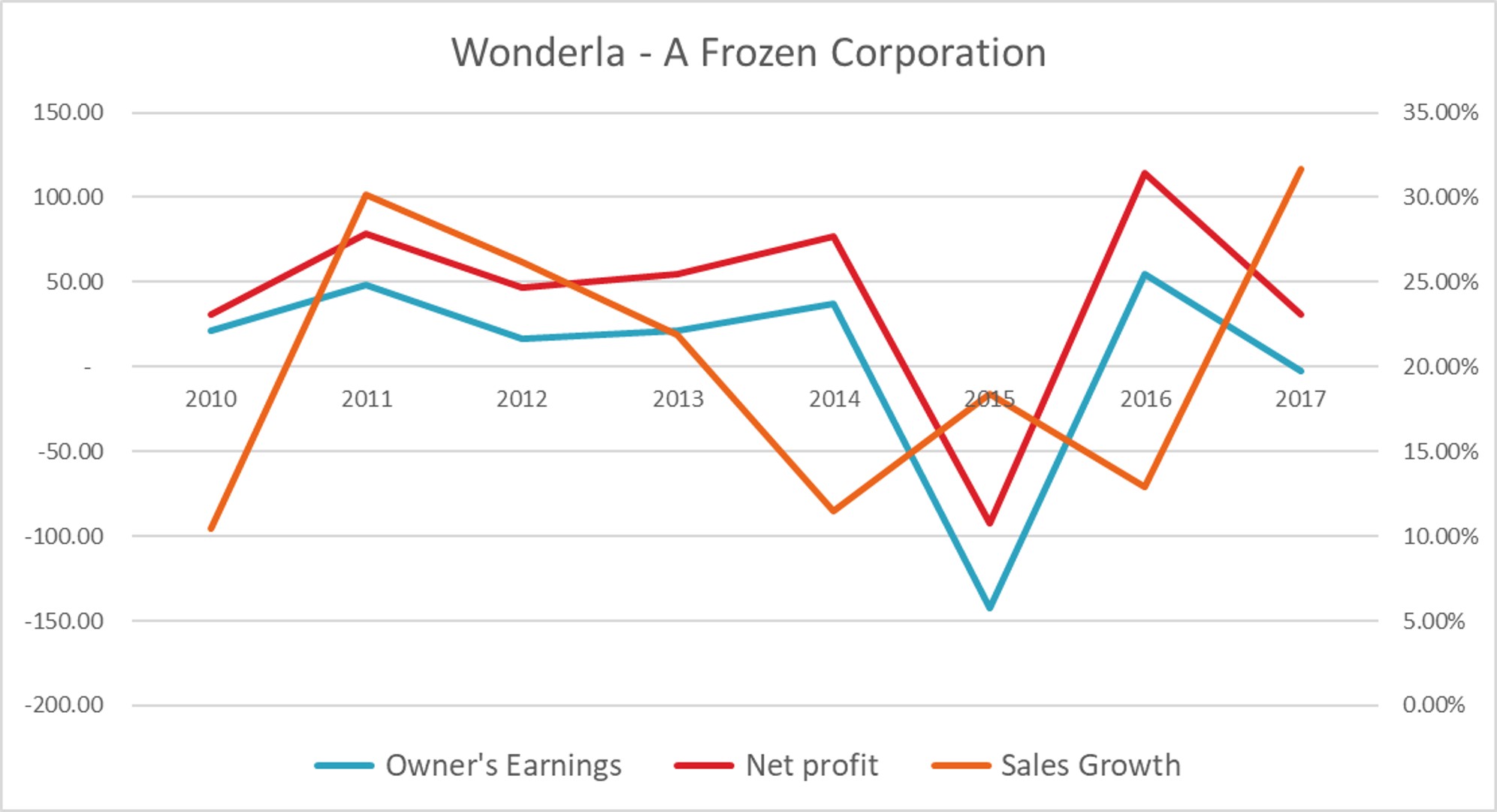

Wonderla: 7%, 360, Core-Long term, Consumption theme, New generation like me don’t like to spend money on things, but we do spend money on experiences, which is basic theme for this investment, but allocation is low, as I am not sure of the price to pay, business valuations seems high, will keep adding on dips.

-

Take Solutions: 5%, 165, Core-Long term, Niche IT Co in Life Science business, legacy business is dying.

-

Thyrocare tech: 4%, 591, Core-Long term, Wellness Industry play: lowest cost service provider with high margin, large opportunity size, and passionate promoter, looking to add further.

-

SREI Infra: 3%, 75, Non-Core, value buy just waiting for SREI Equipment IPO to come and may exit.

-

ITC: 2%, 260, Core-Long term, Stalwart, the consistent performer, evaluating to see if it’s better then FD, Liquid Funds.

-

Rest are equity mutual funds.

Concentration on first 2 names happened naturally, as I could not find relative better options, as the whole market itself looked a bit expensive, also I didn’t wanted to completely exit market, so concentration is where I think there is a margin of safety.

Now my main question is allocation related:

- Currently, I am allocated roughly 45% equity & 55% debt, considering my profile(age,risk profile) & target, shall I change the allocation more towards equity? in what balance?

Options:

A) All fresh income + debt income----> Equity, I can keep allocating additional income back to equity, whenever I find opportunity, that means stopping any further debt investments.

B) Are stalwart co’s like: ITC, Pidilite, Marico a better option than debt(FD, Liquid funds), in my case.

C) Tail risk hedging: shall I try to allocate more to equity, and try options for hedging tail risk, as some experts suggest, although I like simple things, don’t really understand how these options works, but keeping alternative open.

all of your suggestions and feedbacks are valuable for me, please point out flaws in investment thesis also please suggest for allocation.

Thank you!

Best Regards,

Gagan