Dear Reader,

As we mark the close of Q4FY26 and the financial year 2026, we are excited to present our inaugural quarterly memo. While FY26 may have appeared subdued on the surface, it has been a year rich in underlying shifts-quietly shaping the contours of the next investment cycle.

For us, this quarter is not just a milestone, but a beginning. A beginning of disciplined research, sharper conviction, and a long-term partnership with our clients. As markets navigated phases of uncertainty and consolidation, we focused on identifying businesses where fundamentals remain intact and the runway for growth continues to strengthen.

FY26, in many ways, was a year of patience-where noise overshadowed narrative, and inactivity tested conviction. Yet, it is often in such phases that the foundations for outsized returns are laid.

With this memo, we aim to share our perspectives, key observations, and the thought process behind our ideas as we step into FY27 with optimism and clarity.

Recap…

Before diving into the current quarter’s focus areas, let us take a step back and revisit the key takeaways from the past three quarters. FY26, by and large, turned out to be a relatively subdued-one might even say a “lazy” or uneventful; year from a returns perspective.

From the onset of the Russia-Ukraine conflict to the ongoing Iran–Israel tensions, further compounded by the involvement of the United States, the global landscape has remained fraught with uncertainty. These developments have led to persistent volatility, intermittent disruptions, and evolving economic challenges-many of which continue to play out.

However, our study of past geopolitical events and their impact on D-Street offers a constructive perspective. Historically, markets have demonstrated remarkable resilience, often recovering sharply within an average span of 10-14 months post such disruptions. For a deeper analysis, we recommend reading our note titled “Geopolitics vs D-Street: Lessons from History and Market Outlook.”

Crude, Crude, and Crude…

From the very onset of such conflicts, even before broader economic implications unfold, one variable that consistently takes center stage is crude oil.

Historically, during periods of geopolitical tensions, crude prices have spiked sharply-often breaching their threshold levels-only to moderate once the situation stabilizes. This pattern has been evident across previous conflicts, as illustrated in the chart below.

We have consistently observed that irrespective of the nature of global disruptions—be it import duties, wars, or trade tensions—crude oil is often the first and most immediate variable to react. It acts as a key transmission channel, impacting economies well before the secondary effects begin to unfold.

Historically, crude prices have witnessed sharp spikes during such periods, often breaching the $100/barrel mark. At extreme points, prices have even touched ~$140/barrel during crisis phases, only to gradually settle closer to ~$70/barrel as conditions normalize.

From an Indian context, our analysis suggests that the economy is relatively comfortable with crude prices in the range of ~$65–68/barrel. Any sustained movement beyond this range tends to exert pressure on the trade deficit, given India’s high dependence on energy imports.

A prolonged elevation in crude prices not only widens the current account deficit but also puts pressure on inflation, currency stability, and fiscal balances. This, in turn, can influence policy decisions, consumer spending patterns, and overall economic momentum. Hence, tracking crude oil is not just about energy markets—it serves as a critical indicator for broader macroeconomic stability.

Capital Market…

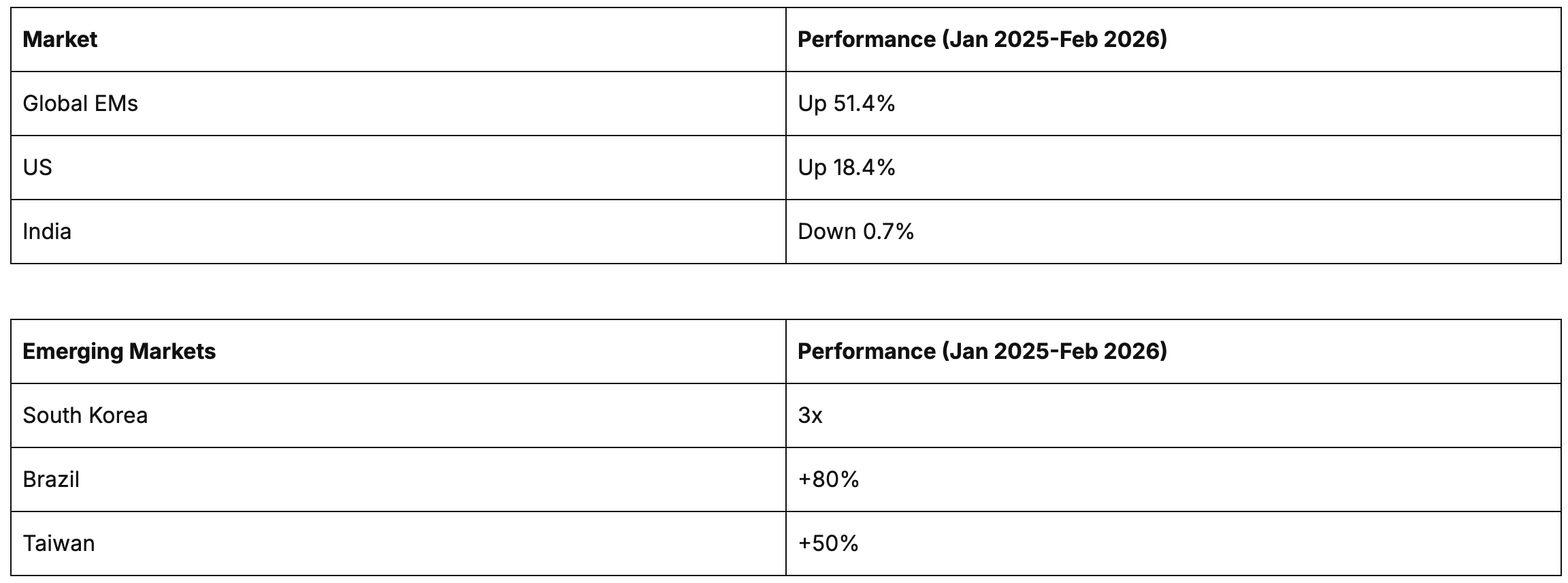

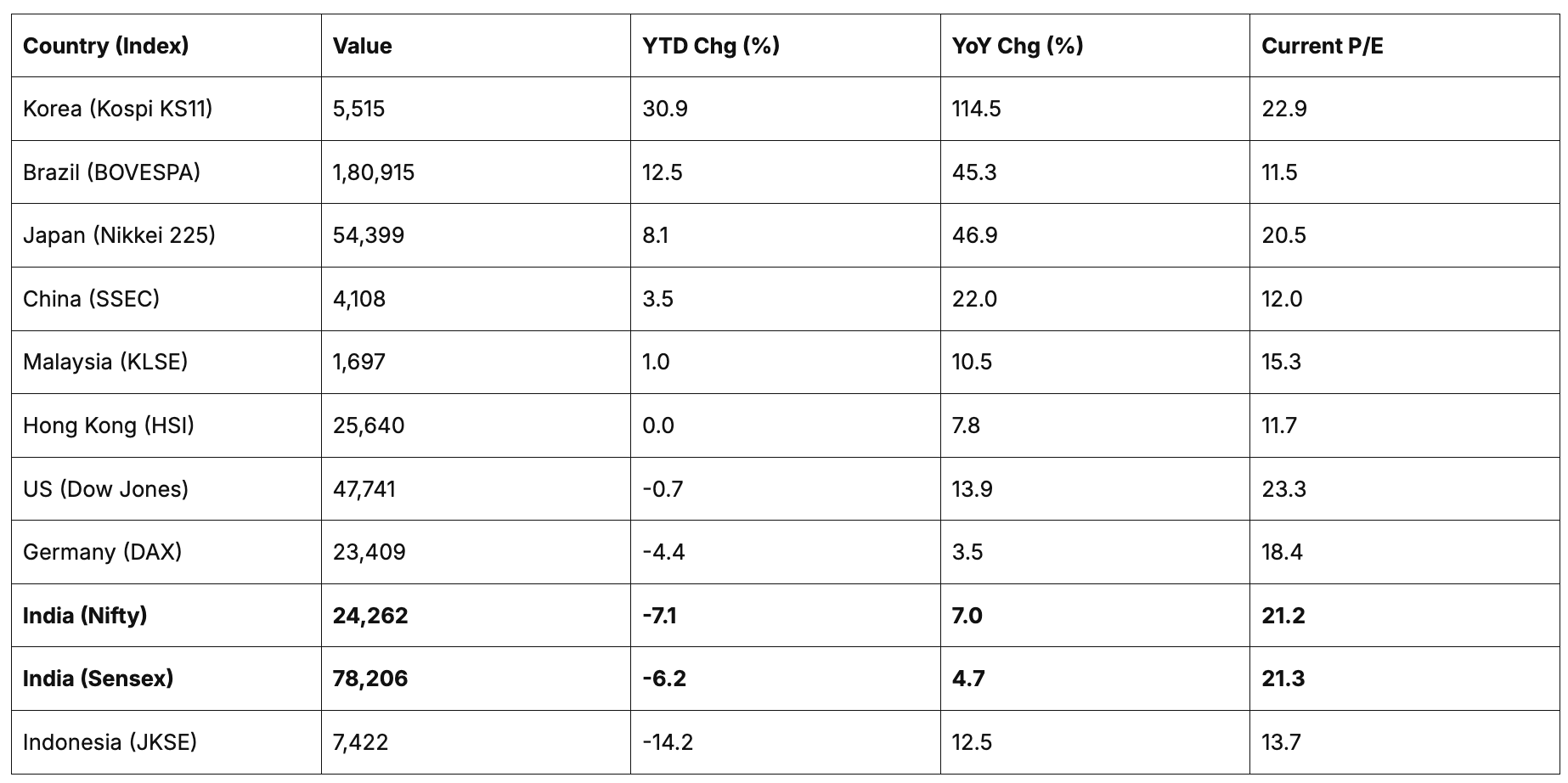

The Indian equity market has been one of the most notable underperformers relative to global peers during this period. This drawdown has largely been driven by back-to-back uncertainties—just as markets began to find relief from tariff-related concerns, the Iran–Israel conflict resurfaced, adding a fresh layer of volatility.

The ripple effects were immediate. Crude oil prices surged, recently touching ~$110/barrel, while the Indian Rupee weakened against major currencies, depreciating by ~9% against the USD and ~18% against the Euro. This combination of factors significantly dented investor sentiment, triggering bouts of panic selling—even in cases where underlying fundamentals remained intact.

As illustrated in the table below, Indian markets have materially underperformed not only emerging markets but also developed economies such as the USA. A key contributor to this trend has been sustained FII outflows, with nearly $23 billion (net) withdrawn over the past year. This was primarily driven by elevated US 10-year bond yields and relatively stretched valuations in the Indian market.

Source: CNBCTV18 Article and Veritas Research

Fundamental Outlook…

On the fundamentals front, the past year has been challenging for investors, with returns ranging from flat to negative, alongside intermittent sharp drawdowns-largely driven by the factors discussed earlier.

In 2025, government capex saw a meaningful slowdown, primarily due to the general and state elections. However, over the last six months, this trend has begun to reverse, with capex activity gradually picking up. In the Union Budget for FY2026-27, capital expenditure has been increased by ~10% to ₹12.2 lakh crore, signaling a renewed push toward infrastructure and growth.

Encouragingly, private sector participation has also strengthened over time. Over the past five years, the share of private capex by companies (with investments exceeding ₹1,000 crore) as a percentage of total capex has steadily improved-from 19% in FY21 to 35% in FY25. This indicates a broadening investment cycle, supported by both public and private spending.

India Inc Earnings: Running Ahead of the Noise

Setting aside the broader uncertainties, India Inc’s earnings continue to demonstrate resilience, with growth remaining firmly in double digits. This performance is supported by strong economic momentum, relatively benign inflation, GST and income tax rationalisation, and a steady pickup in consumption demand.

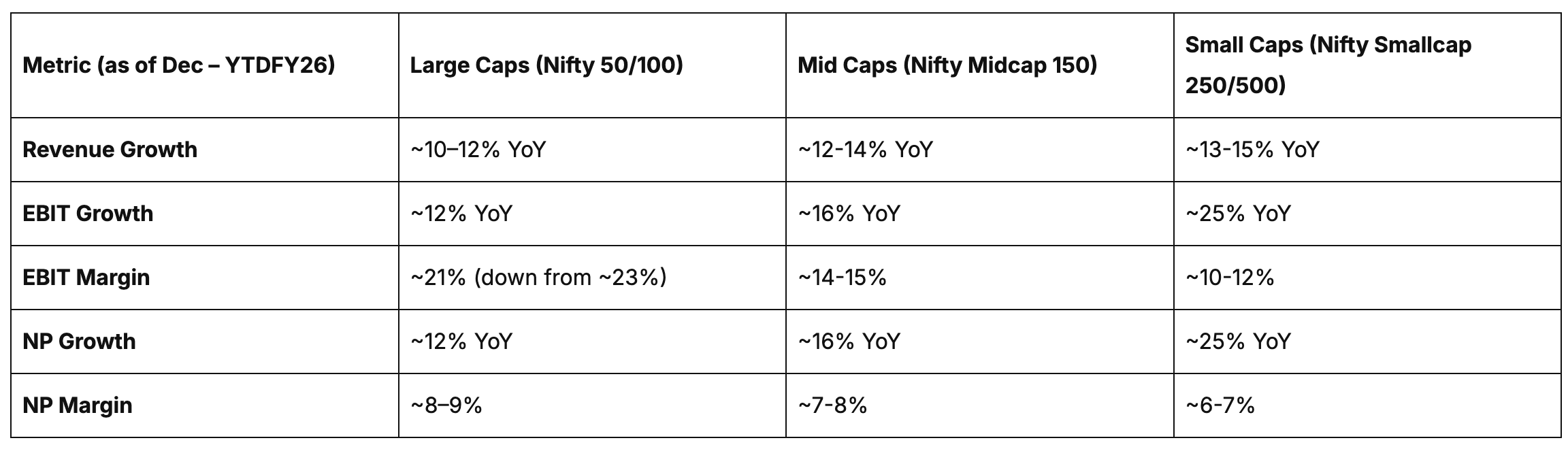

On an aggregate basis, India Inc reported ~13% revenue growth and ~11% net profit growth in FY26 YTD. Across categories, as highlighted in the table below, earnings growth has been robust across large-cap, mid-cap, and small-cap companies.

This strength is largely underpinned by healthier balance sheets, which have significantly improved over the past few years, enabling operating leverage and driving sustained profitability growth.

Source: Veritas Research

Across segments, earnings growth remained broad-based. Large caps (Nifty 50/100), contributing ~54% of market cap, delivered ~10-12% revenue growth with stable profitability despite some margin moderation. Mid caps (Nifty Midcap 150) showed stronger momentum with ~12-14% revenue growth and improving margins, while small caps (Nifty Smallcap 250/500) outperformed with ~13-15% revenue growth and sharp profit expansion, supported by operating leverage.

Perspective on Valuations and Emerging Opportunities

Valuations in Indian equities have moderated following the recent sell-off. Out of ~4,200 actively traded stocks, nearly 2,900 (~69%) have delivered zero or negative returns—highlighting a broad-based correction despite headline indices not declining proportionately.

Across segments, the pain has been more pronounced beyond large caps. Large caps (~33% of the market) are down ~8–10%, mid caps (~55%) have corrected ~15–20%, while small and micro caps (~65–80%) have seen sharper drawdowns of ~30–50% from their peaks. Importantly, this correction has largely been driven by the macro and geopolitical factors discussed earlier, even as earnings performance has remained resilient in recent as well as preceding quarters.

However, despite the meaningful correction, valuations of India Inc still appear relatively elevated and may not yet be compelling enough to attract strong foreign inflows. Indian equities continue to trade at a premium compared to other emerging markets, which remains a key consideration for global investors.

Data as of 10th Mar, 2026

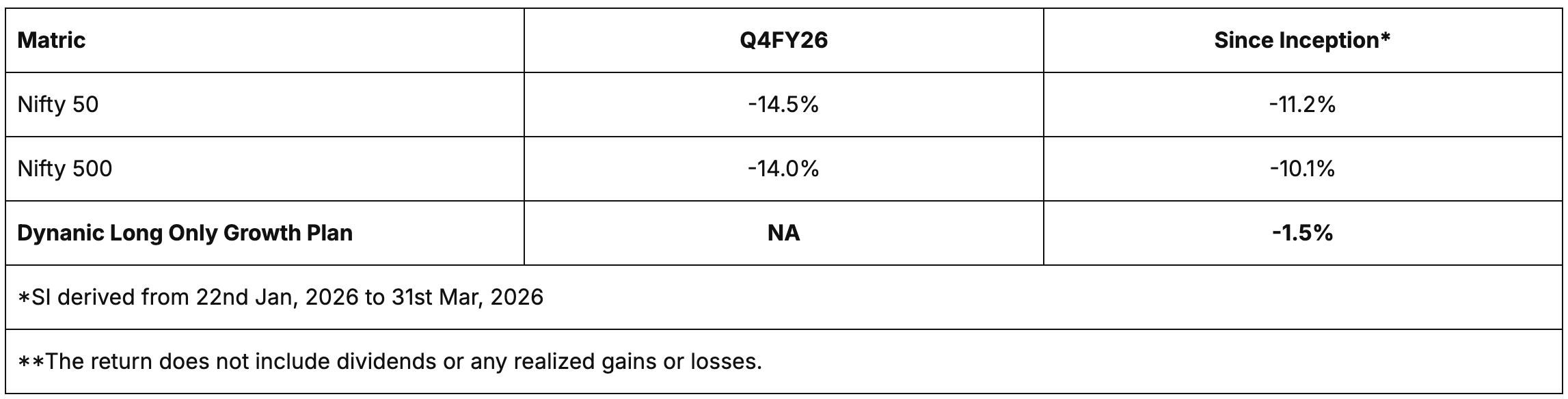

Veritas – DLOGP (Dynamic Long Only Growth Plan) Performance

Our offering went live during a challenging market phase, largely driven by geopolitical uncertainties. Adopting a flexi-cap approach provided a margin of safety, as we focused on businesses with strong earnings visibility (>20-22%) and valuations below historical averages—sub-17x P/E and <1.1x P/B (2-year forward) in small caps, and sub-40x in large and mid caps.

Our recommended ideas have delivered strong fundamentals, with 3-year CAGR of ~23%/27%/33% in revenue/EBITDA/PAT. During Q3FY26 and 9MFY26, these businesses reported growth of ~15%/22%/13% and ~14%/11%/2%, respectively. Despite near-term moderation, earnings visibility remains robust, with expected the earning growth of ~20-25% for large and mid caps and >30% for small caps over the next three years.

The table below highlights the performance of our recommended ideas relative to the benchmark as of 31st March 2026.

Our View and Outlook

A broad universe of listed companies is now trading below its historical median multiples. On FY28E earnings, large-cap, mid-cap, and small-cap businesses are currently valued at below ~37x, ~25x, and ~15x P/E multiples, respectively, while expected PAT growth over the next three years is projected in the range of ~20-35% across segments.

At Veritas, we place greater emphasis on earnings growth rather than short-term sentiment. Sustained above-average earnings growth typically leads to a natural compression in forward multiples, often resulting in PEG ratios converging toward ~0.9 to 1%; levels that have historically signaled attractive entry valuation.

Ultimately, we believe that timely sector selection remains the key differentiator-enabling investors to capture both growth and value simultaneously.

Sectoral Outlook: Where We See Opportunity

We remain optimistic on a few sectors that offer long growth runways, with some having bottomed out after 2-3 years of consolidation.

Manufacturing is entering a new growth phase, supported by indigenisation and strong export momentum, with exports rising ~65% over the past four years. The sharp scale-up in mobile phone exports highlights this structural shift.

Within financials, NBFCs appear relatively attractive as stress in microfinance eases and valuations turn reasonable post a consolidation phase. Meanwhile, consumption is showing early signs of recovery, aided by policy support and improving demand trends.

The auto sector, after years of consolidation, is also witnessing a gradual revival, with the recent GST cut acting as a key trigger for volume growth.

Sectors We Are Cautious On

We remain relatively cautious on the Indian IT and CDMO segments. In IT, the ongoing AI wave introduces significant uncertainty around long-term winners, while elevated valuations of global tech peers add to the risk. In the CDMO space, stretched valuations and increasing competition-particularly with multiple players entering the GLP-1 segment following patent expiries-could lead to pricing pressures, with supply-side dynamics still evolving and uncertain.

To conclude, we leave you with a timeless and relatable insight from Warren Buffett that perfectly captures the essence of our thinking.

“The true investor welcomes volatility… a wildly fluctuating market means that irrationally low prices will periodically be attached to solid businesses”

“Thank you for reading; See you in the next financial year!“

Note:

DLOGP – Return has been calculated on the basis of the HPR (Holding Period Return)

Disclosure:

Veritas Research and Advisors was incorporated on 06 March 2025 at Suraj Bhawan, 95 Guru Jambeshwar Nagar-B, Gandhi Path, Vaishali Nagar, Jaipur, Rajasthan, 302021.

The company is registered as a SEBI (Research Analyst) Regulations 2014, Registration No. INH000024569 and BSE No. 6904; engaged in the business of providing research analyst services, research activities engaged in preparation and/or publication of research reports or research analysis, or making buy/sell/hold recommendations on securities.

The company does not provide investment banking or merchant banking or broking services.

Disclaimer:

This note reflects the views of the author as of the date mentioned and is subject to change without prior notice. Veritas Research and Advisors does not undertake any obligation to update or revise the information contained herein.

This document is intended solely for educational and informational purposes and should not be construed for any other use. Nothing contained in this note constitutes, or should be interpreted as, an offer, solicitation, or recommendation to buy or sell any financial instruments, securities, or to avail advisory services.

Certain information included in this document may be based on or derived from publicly available data or third-party sources. While Veritas Research and Advisors believes such sources to be reliable, it does not guarantee the accuracy, completeness, or adequacy of such information and shall not be responsible for any errors or omissions.

Investors are advised to exercise their own judgment and consult their financial advisors before making any investment decisions. Past performance, whether actual or implied, is not indicative of future results, and no assurance can be given that any investment objectives will be achieved.