Processed Mango Product Market Expanding at CAGR of 6.1% and 7% Respectively from 2018 to 2026.

https://financialportal24.com/global-processed-mango-product-market/

Processed Mango Product Market Expanding at CAGR of 6.1% and 7% Respectively from 2018 to 2026.

https://financialportal24.com/global-processed-mango-product-market/

Does this has a market in India as of now ?

To begin with, the company has introduced its products in the Mumbai, Nashik and Pune markets in 14 flavours with plans to go in for pan-India retail expansion in a phased manner.

Can any one shed some light on Cold extracted juice shelf life. Also since the company wants to expand pan India any thoughts on how will it handle the distribution considering there is no preservative and warehousing and logistic is going to shorten the shelf life. Has any one tasted the juices being marketed.

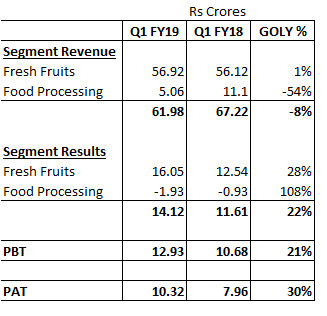

Good results by Freshtrop with some help from Rupee and Lower Tax Rate of 25% from Current Year.

I have been tracking Freshtrop for a while now and sharing some info which I collected from Scuttlebut (kindly ignore if shared already)

Company recently released a video on youtube regarding Company Info Freshtrop Fruits Ltd. - YouTube

It is a family owned and managed business run by Mr Ashok Motiani and family

Company’s main business comes from Export of fresh fruits to EU region primarily grapes (This is stated in ARs also). Last few years Company has ventured into contract manufacturing (processing) for some FMCG companies. My Ex Employer Company was one among them

Based on my experience, Processing business is a low margin, low to average ROCE business. Its difficult for a listed company to compete with a SSI Unit type of business who dont always comply with all regulations, pay taxes etc.

Freshtrop’s processing business has been loss making for some time now

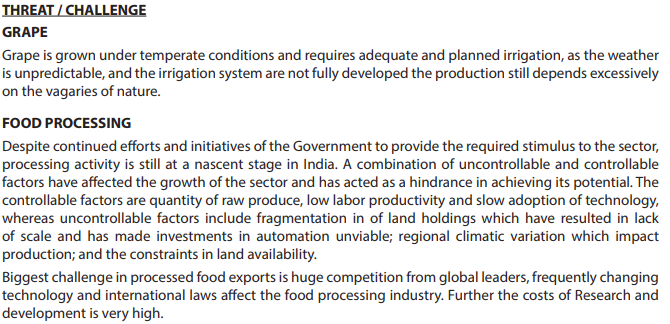

Export of processed foods is highly seasonal since there is one major product. The business is highly susceptible to bad weather and EU food regulations. Plus there is unionism attitude among farmers. I cannot see this business growing at more than 10-12% in the long run

Recent foray into Cold Extracted Juices looks interesting and this is why I am invested. The market for health conscious products is only developing in India and by many estimates would grow faster than most other FMCG products. Company has got strength in sourcing due to long standing name and favourable geog. location for procurement of fruits like Mango, Orange, Grapes, Pomegranate etc.

Marketing of Juices is the key challenge. Based on info gathered, Mr Ashoks younger daughter - Dipti is looking after the new foray in juices.There is an Instagram handle - Login • Instagram which is doing limited publicity among the urban youth and apparently a few food blogger type people.

Juices business has a low base and I feel it has to potential to grow at 20% + at the topline although whether that can be translated at the bottomline level is anybodys guess

Lots of risks ofcourse as Freshtrop will find it extremely difficult to compete with any large player like Pepsi, Dabur; Apart from the risks and problems facing the First two businesses

Invested with a small amount. Will increase allocation if \ when the story plays out

They are into a totally different premium juices segment, and competition from mass selling juices from pepsi/dabur should not matter much in my opinion. I hope they are able to market their product in a way to gain popularity amongst urban population.

Interview of Ms Dipti Motiani on Indian Retailer

Key excerpts

Since the last few months of our launch, we have grown 100 per cent m-o-m and going forward we would like to explore more categories.

While we are presently available in only 3 cities, by the end of the year we will be available in Bengaluru, Hyderabad and Delhi.

We will be focusing on increasing our footprint through five channels- modern trade, all the stores that can provide us 2-4 degree cold chain facility, ecommerce marketplace, restaurants and cafes, schools and corporate firms and finally on our own website through subscription model.

What are your immediate targets?

We want to be present in all major cities and by the start of next year we plan to be present in at least two or three cities more. Also, we would like to explore more categories in cold extracts apart from fruits and vegetables juices and we will work on that. We want to be a Rs 100 crore company in the next five years.

(I guess she is talking abt the juices business targeting 100 cr turnover since Freshtrop is already a 100cr + at the company level)

My take,

Recent wearing of rupee vis a vis Euro should further help margins in next year

In FY 19, Company will enjoy a tax rate of 25% since it’s turnover is less than 250 cr.

Based on info received, they seem to have reduced converter business with domestic FMCGs.( not sure abt this info) Should be positive as this business was loss making.

If Juices business even reaches half of the managements target in 5 years, it will be a superb achievement. India’s juices market is estimated to be ~ 3000 cr and growing in mid teens. Paper Boat’s revenue for FY18 was 118 cr but net losses were 44cr, signifying the kind of costs involved im setting up a juices brand. As per some news articles, paper boat is valued at 1000cr +. That is the long term opportunity available in this business.

One key concern is that management still seems to be family dominated, and perhaps lacking experience in B2C marketing, one of the most crucial part of the juices journey.

Some RED FLAGS

Remuneration of Motiani family in FY 18 was a whopping Rs 2.52 crores (FY 18 PAT was Rs 8.30 cr). Further, after almost no increase in remuneration in last 3 years, they have got a special resolution passed in latest AGM to increase MDs remuneration by more than 50%. (Logically the other family members remuneration should also increase in tandem).

Looks like the family is finding it convenient to take out money as salary instead of dividend.

Since last few months (ever since the company moved to second nature website) their old website of Freshtrop fruits is down.

There are SEBI regulations which require websites to be up to date with Annual Reports and other key info for listed companies. Again this is concerning.

Dec 18 results

Its a seasonal business…numbers only have to be compared yoy

company is not paying out dividend

Debt to equity: 0.5

one quarter is not enough to trust company

EPS (from 2008 to TTM) suggests nothing great has happened.

4.14, 0.40, 2.22, 0.05, 0.49, 2.87, 4.48, 6.04, 6.42, 7.35, 6.84, 11.32, 9.96

no holdings, no tracking, will not track as it is a microcap and no dividend, no trust factor, expecting no miracle, check what happened to vardhman holdings when one time high profits was reported

Goverment focus on agri based products and companies long standing in market with farmers and oversees buyers is valuable. Traction in second nature can be the next legup. Reasonable valuation. Cash intensive business is the only downside. Moderate management but supplying to A grade client so belive the are ethical.

Before lockdown, Grape export was lower compared to last year’s excellent figures.

Grape exports have halted post lockdown.

https://www.freshplaza.com/article/9202603/india-in-lockdown-trade-comes-to-a-halt/

Looks like it will be a subdued year for Freshtrop on the earnings front as grapes is the major item for exports. Some other fruits whose season is due to start like Mango would also be hit (although the impact would depend on how much of purchase contracts were already executed).

However share price has been battered in recent weeks and as on 27th March- the market cap was ~Rs 44 crores. Worth pointing out that company had done a buyback worth ~11 crores few months back.

Even if the current year is a complete washout in terms of profits, the risk reward remains favourable at current price.

Disc- Invested some amount in the recent downturn.

| Q1+Q4’21 | Q1+Q4’20 | Q1+Q4’19 | Q1+Q4’18 | Q1+Q4’17 | Q1+Q4’16 | Q1+Q4’15 | Q1+Q4’14 | Q1+Q4’13 | Q1+Q4’12 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 132.8 | 131.22 | 152.36 | 145.97 | 131.36 | 118.16 | 78.09 | 112.46 | 93.89 | 60.43 |

| Gross% | 37% | 29% | 37% | 36% | 33% | 28% | 33% | 31% | 30% | 35% |

Q1+Q4 are the main seasons for Freshtrop. if you ignore Covid year, gross margins are stable at 36-37% for the last 3y. In fact if you look at the margins and sales for the last 10 years co has more than doubled topline while maintaining margins. To me this looks like a pretty stable co which from '15 to '19 was steadily growing topline before covid hit.

Best

Bheeshma

Could this mean a new market opportunity? I think current exports are not in US markets - but see pomegranate arils and mangoes on the website as key products.

Discl: Tracking position

Some pointers:

Business appears to lack pricing power.

Food Processing business - a bad capital allocation decision?

Second Nature Juices - even after 3 years, the brand is nowhere near some of the largest businesses in the space that are back by large amounts of VC capital. Also, Ms Dipti Motiani, the head of SN, has incorporated another company in September 3021 - will the business be spun out or sold to her?

Consistenly Incomplete CSR Expenditure?

High remuneration taken by promoter family.

Why is a large percentage of cash being deployed in high yield securities rather than being paid out to shareholders?

Did the promoters use warrants to grow their stake at a 40% discount?

Promoter remuneration has increased even in years where company saw a fall in profits and revenues.

Anyone tracking this counter ?, Q4 results appear to be good. your insights will help