Overview:

Freshara Agro Exports Limited presents a classic inflexion-point setup. The company has recently commissioned a second processing unit, enabling a near 2x capacity expansion, operates as the 3rd largest exporter of gherkins from India, and has expanded beyond India through a strategic acquisition of the largest olive processor in Spain.

Supply Side:

Global production of cucumbers and gherkins is highly concentrated. The top 10 producing countries account for ~92% of global output, with China alone contributing ~83–84% (~80 MMT) of total global cucumber production (largely for fresh consumption cucumbers and gherkins of all varities). As a result, global supply dynamics are disproportionately sensitive to changes in Chinese acreage, yields, and policy.

Outside China, production growth across countries such as Turkey, Russia, Mexico, the U.S., and Egypt remains modest and fragmented, typically in the 0.6–1.6% range, with periodic weather disruptions adding volatility. This creates a global supply structure that appears large in aggregate but remains operationally fragile.

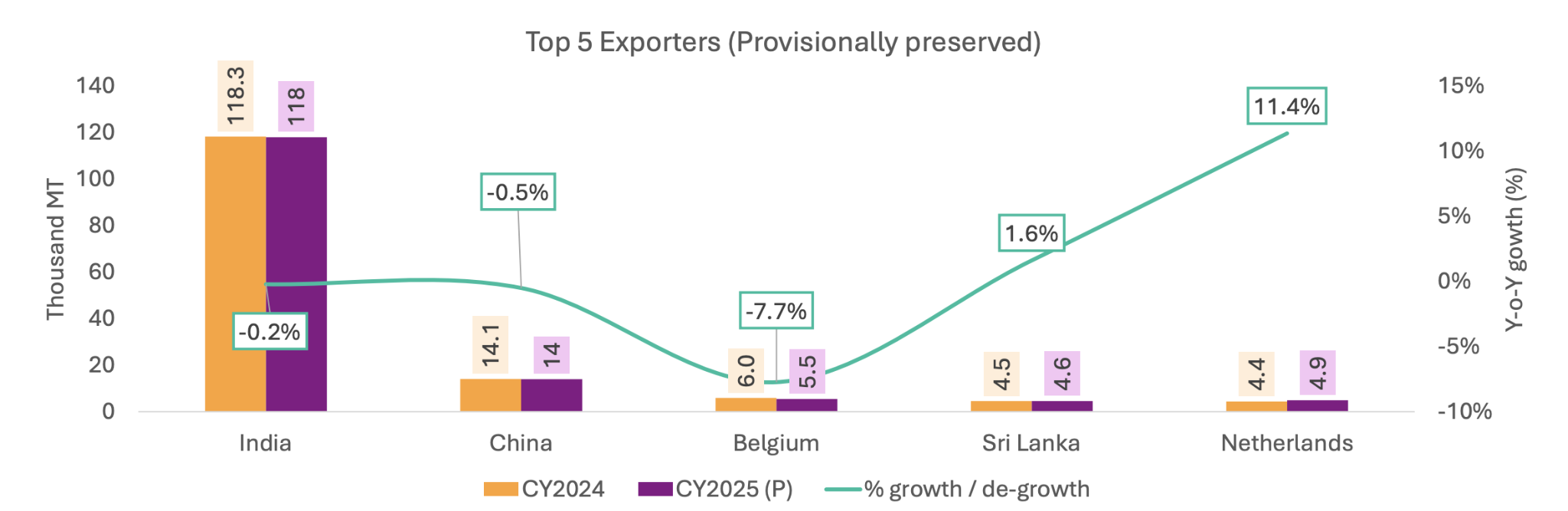

Despite its production dominance, China is not a meaningful exporter of processed gherkins. Export leadership instead resides with countries that have built export-first processing ecosystems, of which India is the most prominent. India produces < 1 million MT—only ~15% of global processing-grade gherkin requirement—, yet it dominates global exports of processed gherkins due to its contract farming model, processing infrastructure, and compliance capabilities.

In provisionally preserved (brined) gherkins, India accounts for ~72% of global exports, supplying standardised industrial inputs to European and global processors. In prepared or vinegar-preserved gherkins, India holds a ~30% global export share, competing with Germany and the U.S. While parts of Indian exports face U.S. tariff exposure, CY2025 volumes have remained resilient due to diversification toward Europe and Russia, with EU demand partially offsetting U.S. softness.

Demand Side:

Global demand for processed cucumbers and gherkins is expanding on the back of steady growth in pickling and ready-to-eat food segments, with Crisil estimating ~8–9% CAGR over CY2021–26.

Consumption growth is broad-based across Europe, North America, and other developed markets and is driven by downstream food habits rather than agricultural cycles, making demand relatively sticky and less price-elastic.

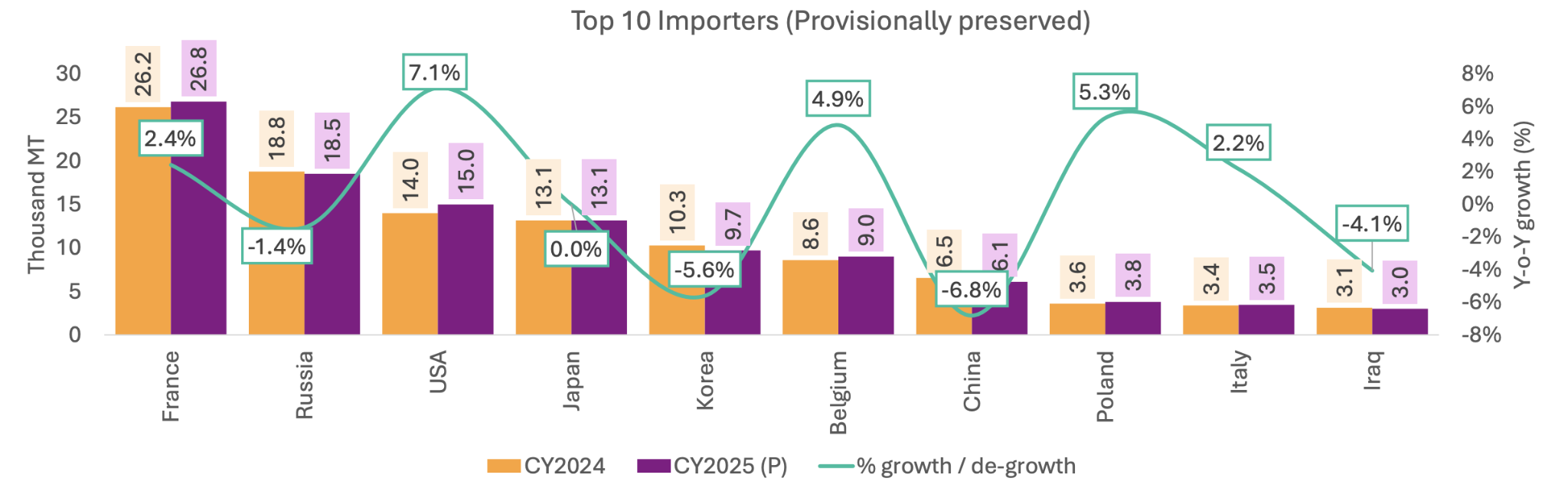

Europe remains the anchor demand market, accounting for over 60% of global import value, with EU import volumes already up sharply in H1 CY2025 and expected to grow ~5–10% YoY

While U.S. tariffs have introduced trade-level volatility, underlying consumption remains intact, with demand reallocating toward cost-competitive suppliers such as India. Importantly, incremental demand is skewed toward processed and bulk categories, reinforcing volume visibility for large export-oriented processors.

Freshara’s Strategic Positioning:

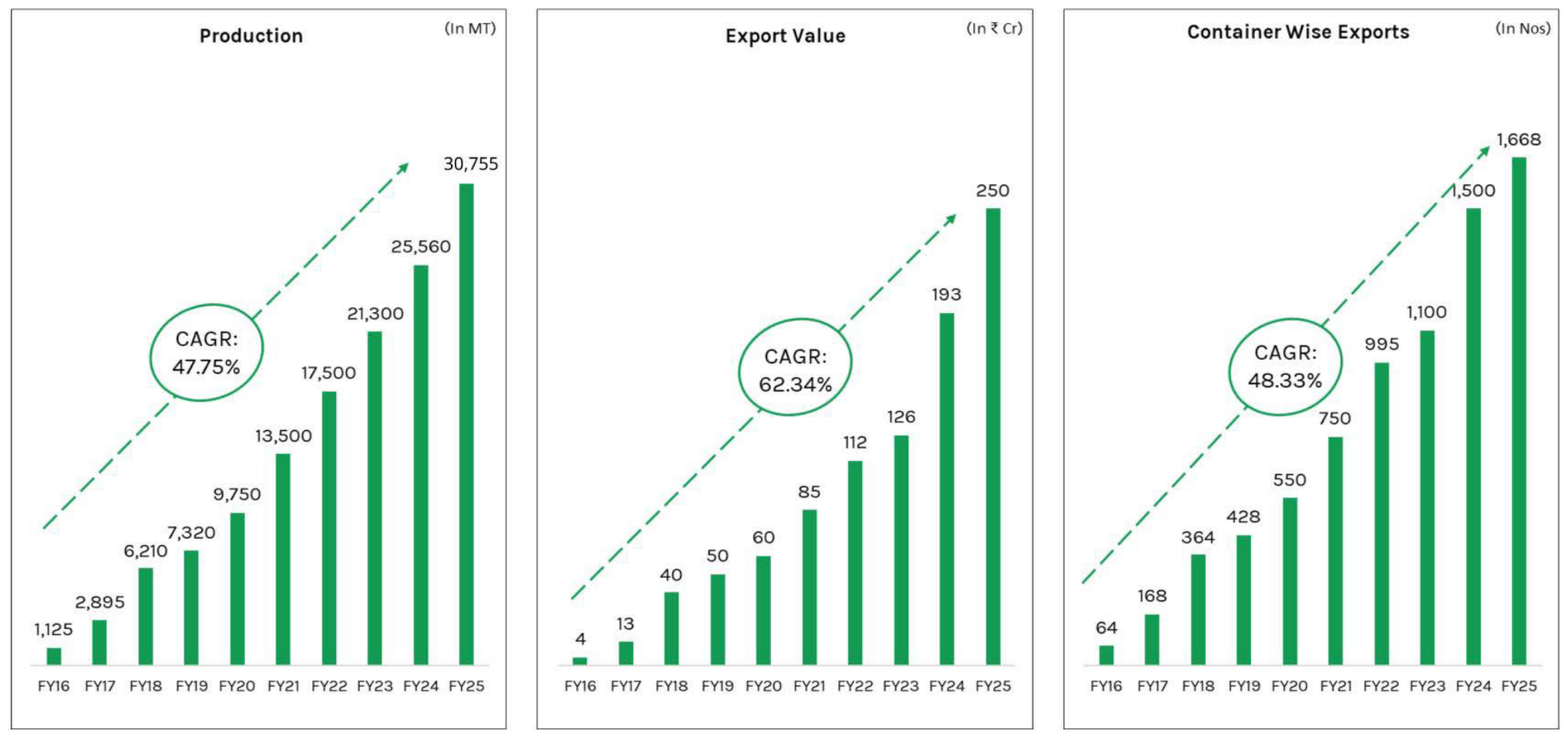

In this global context, Freshara is a scaled, relevant Indian exporter. The company is the third-largest exporter of gherkins from India, exporting 30,755 MT in FY25 and accounting for an estimated 26% of India’s gherkin exports.

Freshara operates as a 100% Export Oriented Unit (EOU) and exports to 40+ countries, primarily serving B2B customers across Europe, Russia, the U.S., and West Asia. The business is volume-driven rather than brand-led, with bulk and food-service packaging forming the core of exports.

Raw material sourcing is anchored in a contract farming model involving 4,000+ farmers across 22 districts in Tamil Nadu, Karnataka, and Andhra Pradesh. This eliminates exposure to open-market price volatility, ensures predictable procurement, and mitigates regional crop risk through geographic diversification.

Processing operations are concentrated in two facilities in Tirupattur, Tamil Nadu, with the second unit now fully operational. The new unit lifts processing capacity to 75–100 MT per day, expanding retail packing capacity from 6,000 to 18,000 jars per hour with peak capacity of about 36,000-40,000 MT.

Freshara remains a gherkin-led business, with ~83% of FY25 revenue derived from gherkins, and the balance from baby corn, banderillas, chillies, jalapeños, and mixed products. The major geographies of export are Russia and Spain, where they export almost 35% and 16% of their produce, respectively.

Freshra has grown its volumes at 47% CAGR for 10 years, achieving scale and dominance in gherkin export from 1,125MT in 2016 to 30,755MT in FY25

Spain Acquisition:

Freshara has acquired Sarasa, one of the largest olive processors in Spain, through an asset purchase (75 Crores), giving it immediate access to ~₹200+ crore of revenue at ~50% utilization and a normalised revenue potential of ₹400–500 crore. The facility operates at ~55–60 MT per day (20,000+ MT per annum) with integrated processing, packing, and logistics infrastructure, and requires minimal incremental capex, effectively adding scalable capacity below replacement cost.

The acquired business was historically constrained by mix rather than demand, with ~97% of sales in domestic Spanish retail, where margins are structurally low. Freshara’s intervention is to pivot the business toward exports, where margins are estimated at ~15–20%, and to improve cost efficiency by localising ~40–50% of production and packaging to India . Management estimates a ~4–5% margin uplift purely from cost arbitrage and mix improvement, independent of volume growth.

Strategically, the acquisition expands Freshara into olives, a globally consumed category with demand across 100+ countries, while remaining within its core export-processing competence. Importantly, gherkin production for the Spanish brands will be shifted to India, where Freshara has cost leadership and surplus capacity, improving utilisation across its Indian plants. Management expects limited contribution in FY26 due to partial consolidation, with ~₹200+ crore revenue contribution in FY27, and medium-term scalability toward asset-level capacity.

Freshara’s Spain acquisition entails a total outlay of ~₹75 crore, funded through a combination of internal accruals from IPO proceeds, short-term working capital borrowings, and a ₹45 crore preferential issue of warrants at prevailing market price, with over 45% of the warrants allotted to the promoter group, thereby aligning promoter capital with the acquisition while limiting immediate equity dilution to 1.7%.

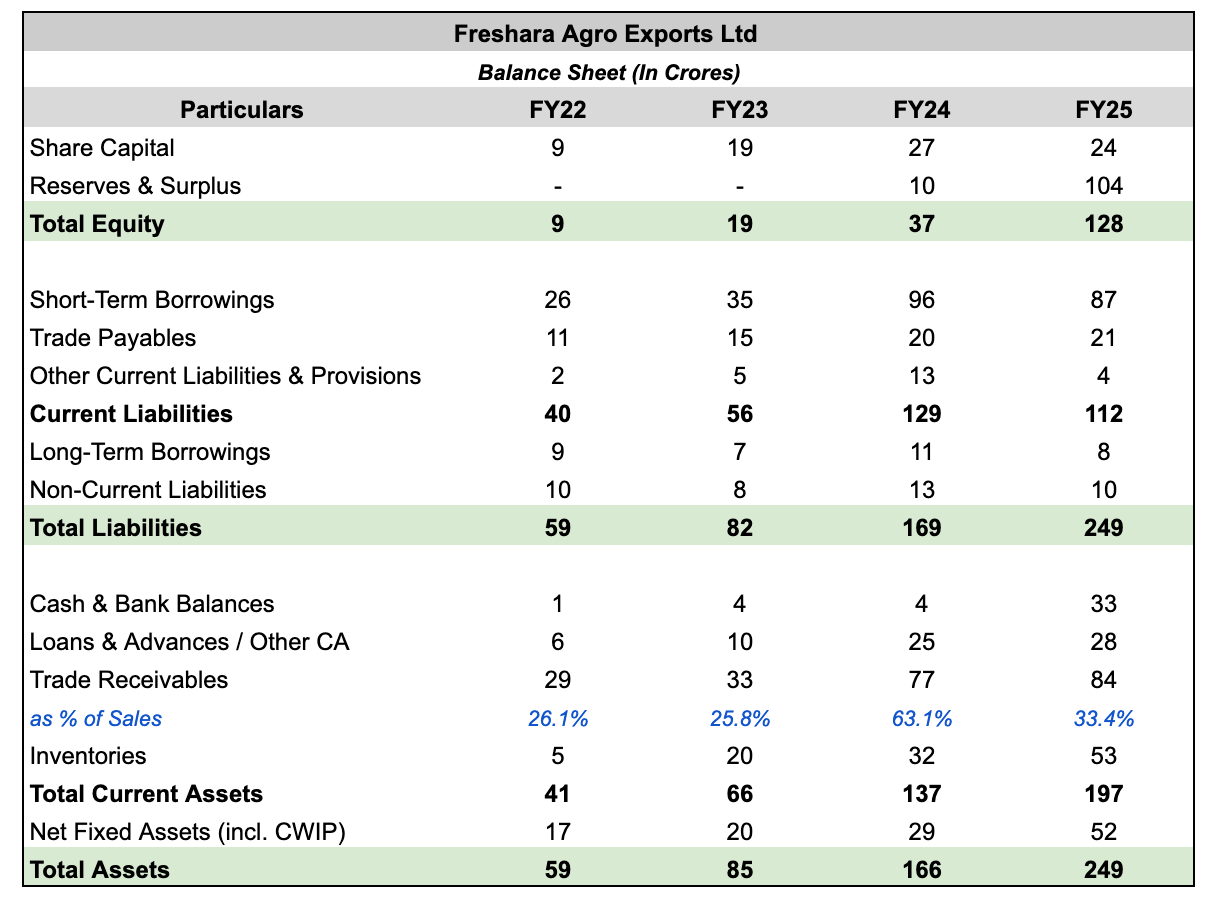

Financials:

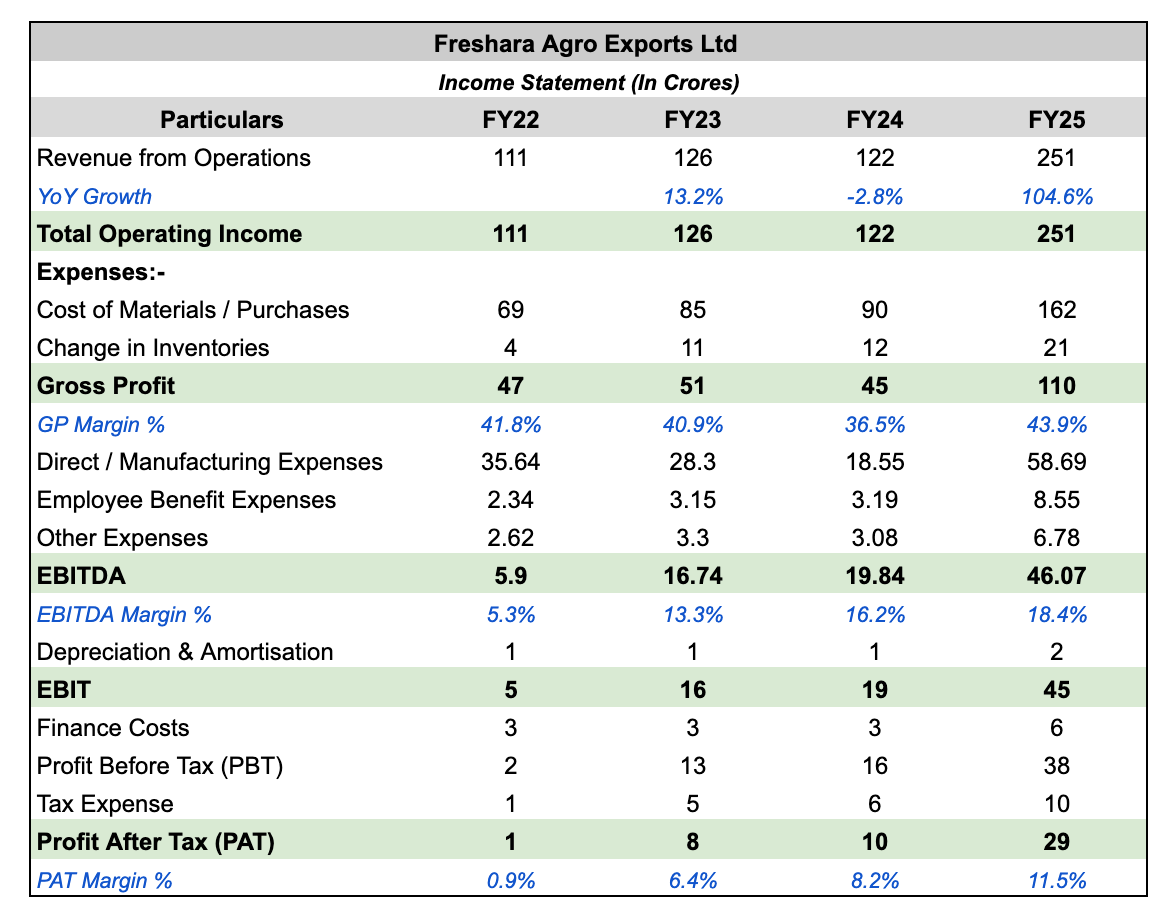

- Revenue scaled 2.3x in three years, from ₹111 crore (FY22) to ₹251 crore (FY25), driven by capacity commissioning compared to price-led growth.

- PAT expanded sharply from ₹1 crore in FY22 to ₹29 crore in FY25, growing at 65% CAGR, confirming that incremental revenue is flowing disproportionately to the bottom line.

- EBITDA grew ~8x over FY22–FY25, from ₹5.9 crore to ₹46.1 crore, with EBITDA margins expanding from 5.3% to 18.4%, indicating strong operating leverage.

- Gross margins remained structurally stable at ~40–44% despite a step-up in volumes, suggesting pricing power and cost discipline even at higher scale.

- Freshara raised ₹75 crore via a 100% fresh SME IPO in Oct’24, strengthening liquidity for a working-capital-heavy model (~35% of revenue) and enabling scale-up without stretching leverage.

- Incremental capex has been focused, with ~3x expansion in retail packaging capacity at the new plant, driving fixed assets growth.

- Elevated inventory levels reflect operational necessity, driven by 24–48 hour perishability of gherkins unless processed, quarterly export order cycles, and an 8–9 month harvesting window.

- The company has high receivable days of 122 days, which stresses the balance sheet with 1/3rd of the revenue in the form of trade receivables.

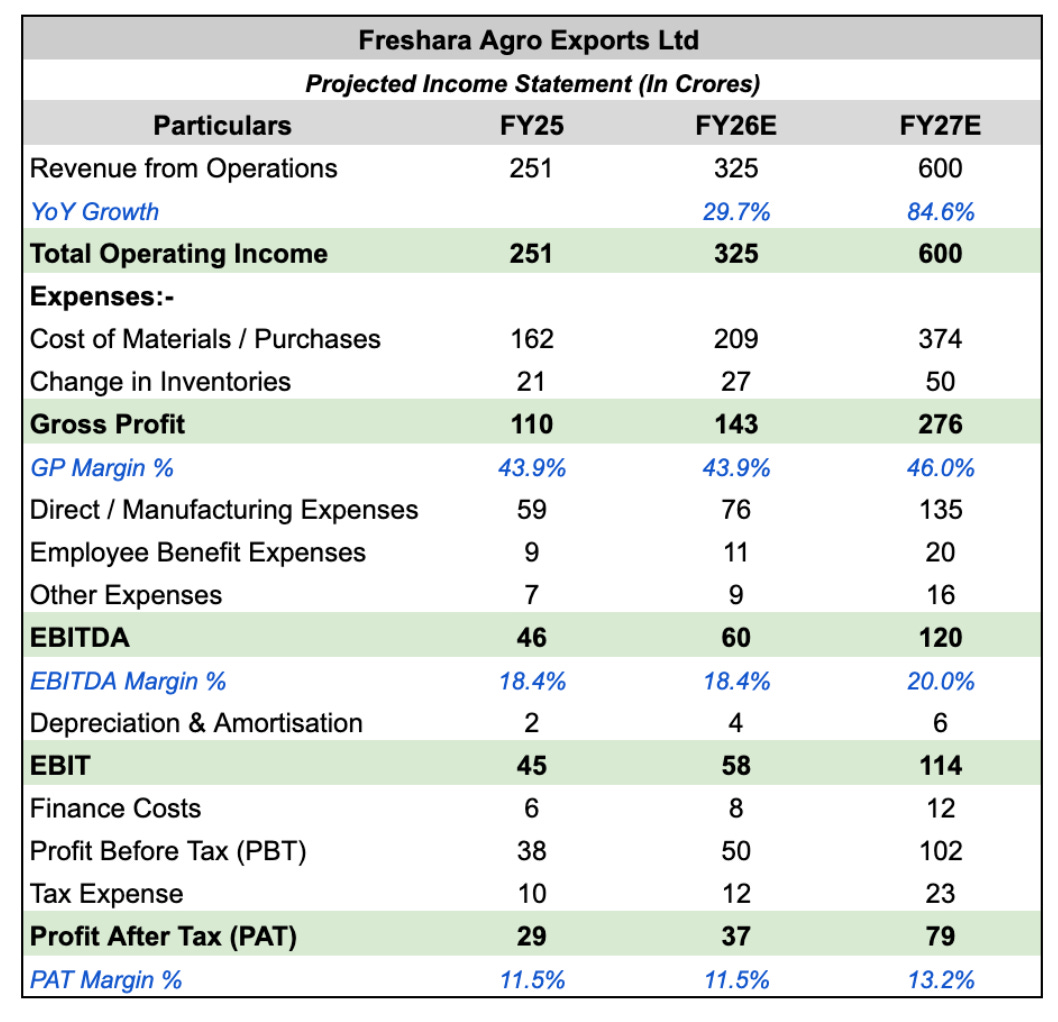

Earnings Trajectory: FY25–FY27E

- FY27 revenue of ~₹600 crore assumes ~20% growth in the India business, implying operations at ~85–90% capacity utilisation, alongside an incremental ~₹200 crore contribution from the Spain entity, modelled at a conservative 50–55% capacity utilisation in the initial ramp-up phase.

- Gross and EBITDA margins are expected to improve by ~1.5–2%, driven by a favourable product mix shift, with olives (higher margin) forming almost 30% of the portfolio by FY27.

- The projected increase in finance costs primarily reflects higher working-capital borrowings, particularly to support the Spain operations.

- Employee expenses are assumed to scale broadly in line with revenue, as the Spain entity operates with low incremental manpower requirements due to high automation and SAP-driven systems, limiting operating cost inflation despite scale-up.

- Depreciation is kept in line with the modest increase in new asset additions post FY26.

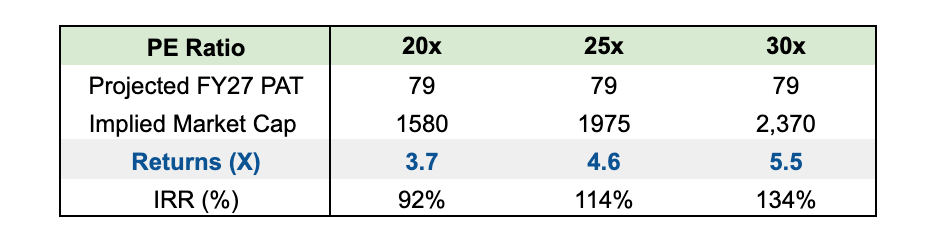

Valuation and Upside Potential:

Currently trading at ~13.5× earnings with a market capitalisation of ~₹432 crore, Freshara is scaling volumes, integrating a materially sized acquisition, and compounding profits at over 50% CAGR through FY27. Given the visibility on growth and operating leverage, the business warrants a meaningful re-rating, with a reasonable valuation band of ~25×–30× earnings.

Key Risks:

- Delay in capacity ramp-up and utilisation at the Spain facility.

- Weak operating cash flows leading to higher working-capital interest costs.

- Crop failure in key contract-farming regions is causing a 2–3 quarter earnings disruption.

- Geopolitical escalation (Russia) impacting demand and logistics costs.

Disclaimer :

I currently hold shares of the company discussed in this post and therefore my views may be biased.

This write-up is prepared solely for educational and discussion purposes on the ValuePickr forum. It does not constitute investment advice, a recommendation, or an offer to buy or sell any securities under the regulations of the Securities and Exchange Board of India (SEBI).

The information and analysis presented are based on publicly available sources and my personal interpretation, which may be incomplete, inaccurate, or subject to change. I may be completely wrong in my assessment.

I may buy or sell shares of the mentioned company without prior notice. Readers are strongly encouraged to conduct their own independent research (DYOR) and, where necessary, consult a SEBI-registered investment advisor before making any investment decisions.