Franklin Templeton has shut six of it’s scheme namely -

1. Franklin Templeton Credit Risk Fund

2. Franklin Templeton India Low Duration Fund

3. Franklin Templeton India Dynamic Accrual Fund

4. Franklin India Short Term Income Fund

5. Franklin India Ultra Short Term Fund

6. Franklin India Income Opportunities Fund

Total invested amount in these funds according to different sources is around 26k - 30k cr.

Shutting down fund means there will be no investment or redemption in the funds. The AMC and/with trustees will try to sell the assets of the funds and return the money to investors.

Now I have three questions in my mind, one I have a part answer to, remaining two remains unanswered.

Question 1 - What is the effect of this default on money supply in market?

Answer 1 - Assuming fund size to be 30k cr and money multiplier at 6. Amount of money out of system can be 1.8L cr.

Question 2 - What assets these funds hold?

Answer 2 -

Credit Risk Fund - Full Portfolio.

India Low Duration - Full Portfolio

India Dynamic Accrual Fund - Full Portfolio

India Short Term Income Plan - Full Portfolio

India Ultra Short Term Fund - Full Portfolio

India income opportunities fund - Full Portfolio

Question 3 - Who are the owners of these funds? Which companies will be loosing money in this? (Un-answered)

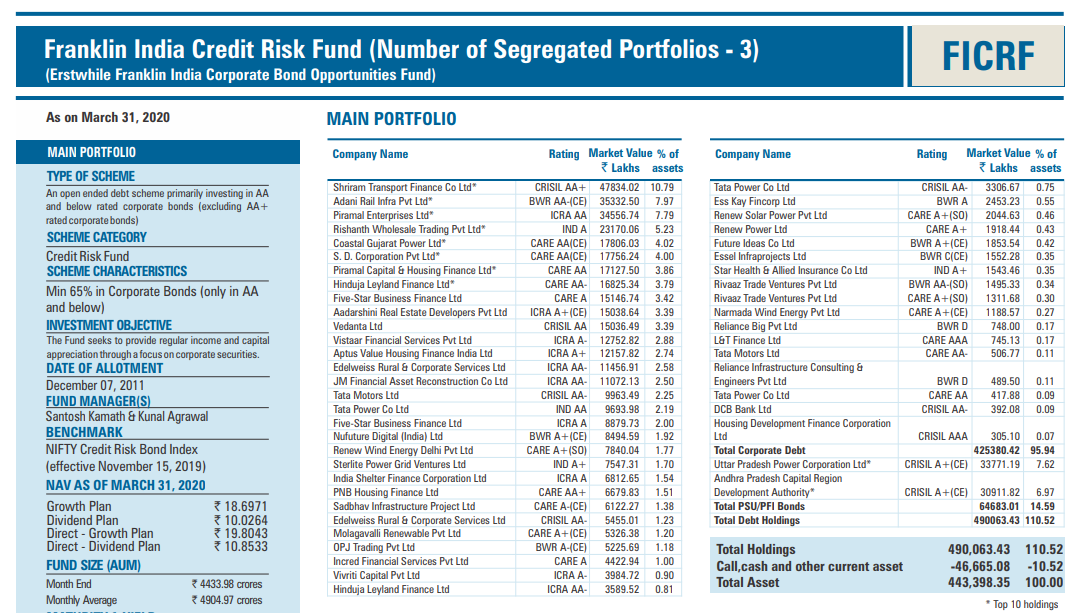

Let’s look at Credit Risk Fund in detail, it is segregated into three parts

Main Portfolio

8.25% Vodafone Idea - 10Jul20

10.9% Vodafone Idea - 02Sep23 partially convertible 03Sep21

Leaving Vodafone aside let’s analyse Main Portfolio -

Total fund size as of 31-Mar-20 is 4,900 cr

Out of the listed companies unknown/doubtful companies are -

Rishanth Wholesale Trading (RWTPL) - 2,300cr

owns VMMPL. VMMPL grants franchise rights for Vishal Mega Mart.

Coastal Gujarat Power - 1,8k

wholly owned subsidiary of Tata Power.

SD Corporation - 1,800

is Shapoorji Pallonji group company

Five-Star Business - 1,500

Finance start-up backed by TPG Capital, Matrix partners, Morgan Stanley, Sequoia Capital etc.

Aadarshini Real Estate Developers - 1,500

Wholly owned subsidiary of DLF Home Developers

Vistaar Financials Services - 1,300

Incorporated in 1991, MD - Ramakrishna Nishtala, Bangalore (Explore)

Aptus Value housing - 1,200

Raised 800cr from WestBridge, Steadview & Sequoia

Nufuture Digital - 850

No website, Incorporated-2007, Mumbai (Explore)

India Shelter Finance - 680

erthwhile Satyaprakash Housing Finance (Explore)

Molagavalli Renewable - 530

Incorporated-2017 (Explore)

OPJ Trading - 520

Jindal Steel promoter OPJ Trading raises fund from Centrum Credit

Incred Financial - 440

Invested by Rajan Pai (Manipal) etc.

Vivriti Capital - 390

Had series A & B round of funding.

Ess Kay Fincorp - 240

TPG growth, Norwest Venture & Evolvence India are investor

Furture Ideas - 190

(Explore)

Rivaaz Trade Ventures - 280

Invest in leasing retail space and renting to retail business.

Narmada Wind Energy - 120

Something to do we renew power (Explore)

Reliance Big - 748cr

ADAG group

Reliance Infra consulting - 50.6

Rating document