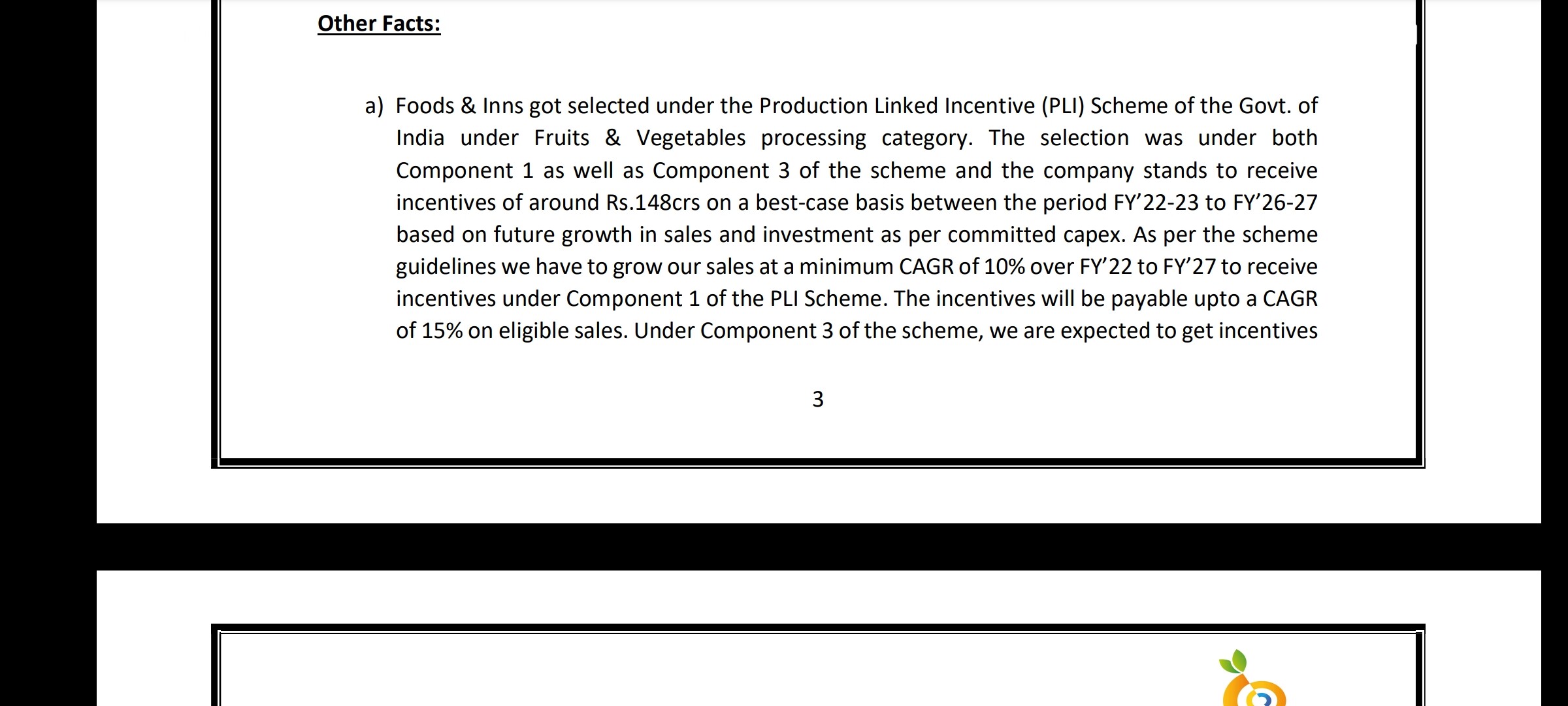

Foods and Innsis a multi-locational manufacturer and exporter of a range of processed Tropical fruits pulps, purees and vegetables with state of the art factories in Mumbai, Chittor, Valsad, Sinnar and Gonde (Nasik).

Our principal divisions are Aseptic, Canning, Spray Drying and Frozen fruits, IQF vegetables and snacks.

Our manufacturing facilities are managed by an expert team of food technologists who measure all the critical parameters at each stage of the production process to ensure meeting quality requirenment of customers. Our premium varieties of fruits and vegetables are sourced from the Ratnagiri, Valsad, Nasik, Mysore and Chittor regions, where we have our qualified agronomists who check on the quality of raw materials received by us and assists farmers in their horticulture program.

Total Capacity

:

100,000 MT +

Manufacturing Facility

:

7 (Mumbai 1, Nasik 2, Valsad 1, Chittoor 3)

Warehousing Facility

:

8 ( Domestic and International)

Ownership

:

Public Limited.

Principal Division

:

Aseptic, Canning, Frozen and Spray dried.

Certifications

:

IS0 22000, CSR, SGF, USFDA, Halal, SGP, Kosher

1940s

:

Started with canning facilities to supply canned foods to the Allied Armed forces during world war II.

1971

:

The Company went public and created facility for spray dried Egg powder to supply Indian armed forces which was the 1st in South East Asia .

1983

:

Company diversified into manufacturing tropical fruit pulps with the first fully automated canning lines.

1995

:

Setup frozen fruit and vegetable lines in Nasik to take advantage of the growing demand for ethnic snacks and vegetables in international markets.

1999

:

1st in India to install skid mounted, PLC operated Aseptic processing and packaging line.

2001-2007

:

Added 5 more Aseptic processing lines with Concentration facilities during next 6 years.

2008

:

Setup a new Aseptic Processing facility exclusive for Alphonso and high Aroma single strength Purees. The plant layout and design was done with the technical assistance of a leading Japanese Group.

Same year we initiated the NPOP(Organic Mango) program for Alphonso Mango.

2010

:

Certified By Control Union (NL) for Organic Alphonso Mango tree

2011

:

With the commissioning of new concentration line in Southern division we have doubled the capacity.

44+ issues were listed in 2012 and not sure on the count now or about the activities of other promoters. Curious and the brave can dig more for more colours on their recent activities. Sample was enough to turn me off.

Disclaimer: Not to be construed as advice. Not holding any positions. Please do you due diligence.

I am tracking this share. Industry potential is huge. Main customers are pepsi and also others. But promoters were involved in some scam in past before 2000. But looks like they have come back strongly, but have to check this more before investment. Any recent info on promoter quality is welcomed. Few links …

I am a fresher here, but even to my eyes there is not enough information. You have presented a story with no numbers or critical analysis, PE is not the sole criteria.

Mr Damani bought on April 12, 2019 @ 184 per share approx.

The share has been ex bonus from April 30, 2019.

Which means, post receiving bonus shares (2 shares for each 1 held i.e. 2:1), the acquisition price of Mr Damani comes down to 61 (almost 1/3rd, right?).

The share is available right now (as on 30th Aug) at ~ 45. That means it is available 25% cheaper (with compared to Mr Damani’s acquisition price).

Forum members following this company pls comment your views regarding the long term prospects of the company.

Any receny update on this company?

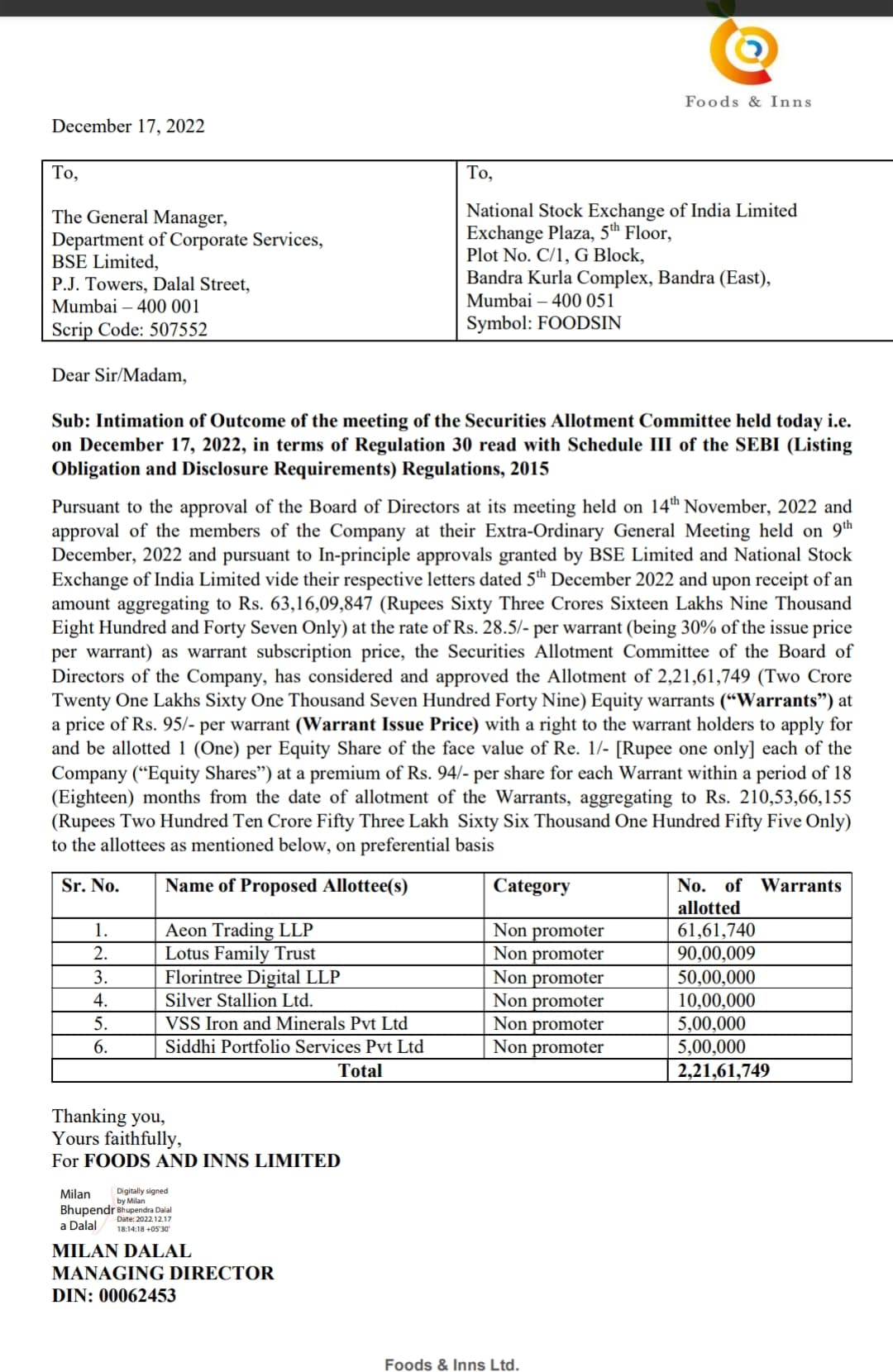

With recent good results, raised 210 cr from marquee investors ,Mathew cyriac also invested, good capex, PLI beneficiaries… l

But I have read about the negative reviews about management in this thread (2015 post).

If anyone has studies please share your views especially about the management

Thanks

Disc : tracking position

Despite all negatives, this co has performed good.

After pref, promoters’ holding will go down to 30% from 42%.

Half of promoters holding is with dhupelia family, for which I havnt found any negative yet. Utsav dhupelia was actively involved in this co as per old presentation, and now his son ameya dhupelia (who was CFO, then UK head) seems taking interest in company. Not much info available outside…,

But yes recent developments are interesting.

Company is planning to issue warrants and as per their latest credit rating report equity infusion of 221 crore may be infuse in future. EGM has held for the same.

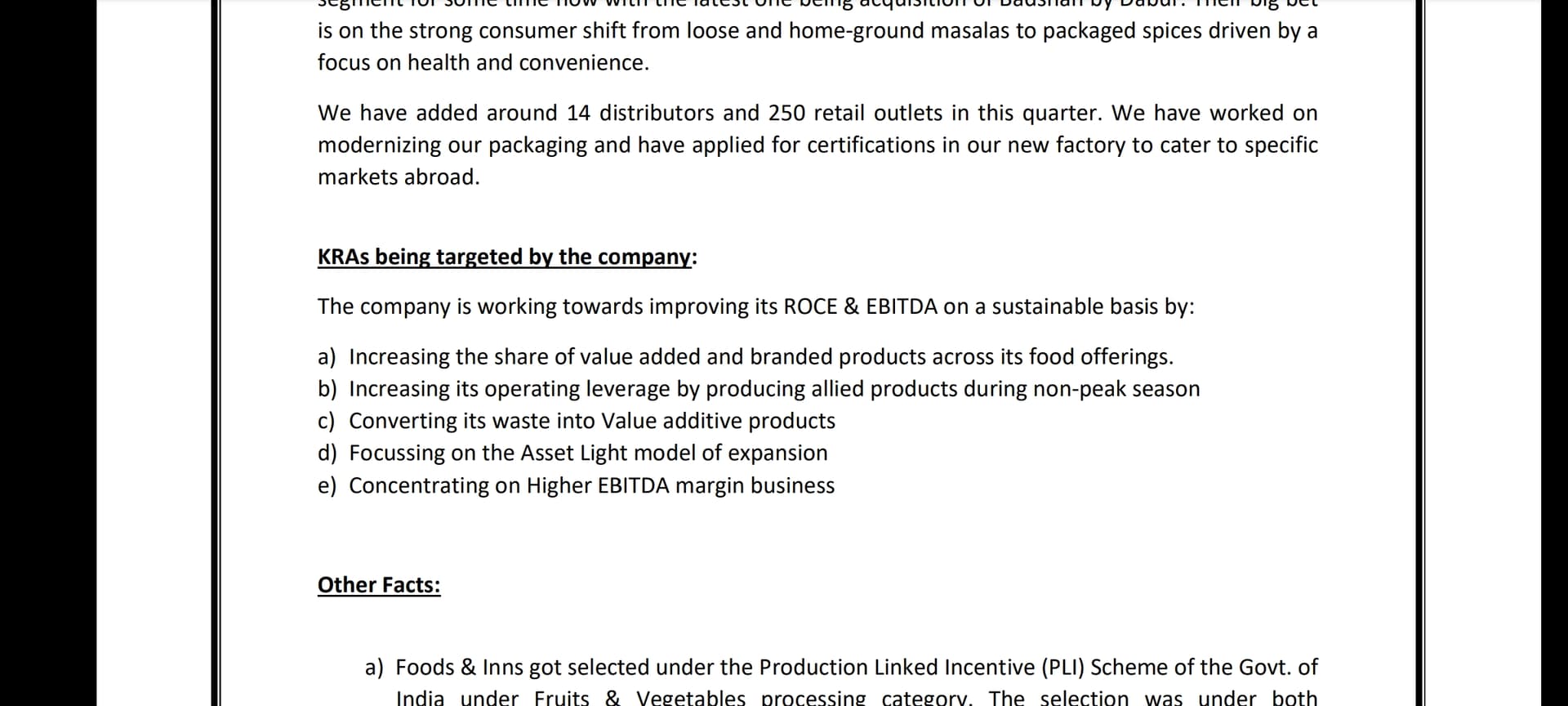

Volume growth is not coming but focusing more on VAP hence margin will shoot up. Perfect proxy to play beverages industry tailwinds, Coco-Cola and Pepsi both are focusing on juice segment to fuel their future growth pulp is main raw material for it and that’s where Food and Inns comes.

Company does not have pricing power as competition is high in this industry and that’s why margin is in 8-9% in last 2-3 years. But in their latest IP they have hinted for margin expansion due to VAP contribution, focusing on asset light model and focusing on non- peak season products.

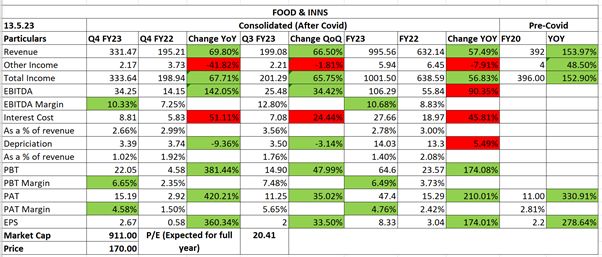

Interestingly in FY23 they have achieved sales of 454CR in 6 months of FY23, this is expected to increase further with more capacity coming up in future.

Food & Inns looks like a very interesting business, given the large downstream investments and tailwinds in the sector. Company’s diversification into Pectin (high gross margin & an import substitute) and focus on B2C is looking promising. However, not sure why they’re planning to get into Mini-QSR, plant-based meat etc.

I attended their 2022 AGM. Some notes from it:

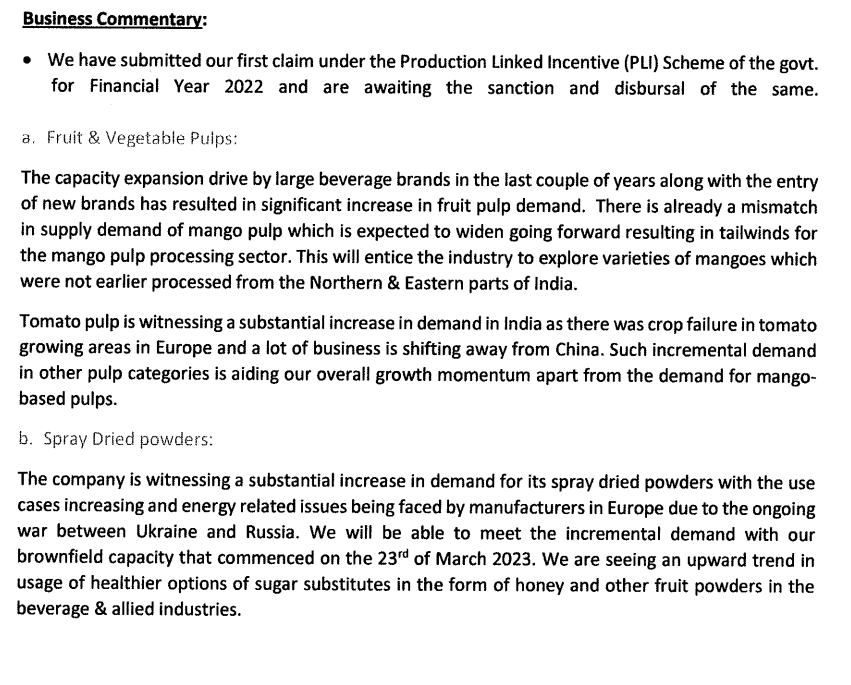

Profitability unaffected by mango prices → passed on to customers.

Demand from Europe remains very strong (unaffected by the Russia-Ukraine crisis) and is higher than the current capacity.

Tomato pulp → China has the largest market share but there is a shift towards domestic sourcing.

Guava pulp → market growing substantially. Lots of upstream capacities.

Intend to put F&I mango pulp on retail shelves in the next few years.

2 years ago, exports contributed to 70% of revenues. However due to higher container prices and fungible capacities at F&I, the domestic market had higher revenue share this year.

Pectin is a high gross margin business → only conversion cost (electricity cost). Earlier had to incur a cost to dispose of the waste.

Very briefly mentioned about plans in plant-based products (plant-based meat?)

They are testing waters with the mini-QSR (which they described as something between street food and QSR). Ticket size between Rs. 100-150. Looking at 100 sq. ft outlets serving ready-to-eat food.

One shareholder asked them to elaborate on the frequent insider trades/invocation of pledge recently and the CFO denied this. (Strange, because there have been a few filings about insider trades and invocation of pledge, recently. Wondering why would they want to deny this?)

Debt-equity → will always keep it under 2x.

Looking to take ROCE over 20% over the next few years.

Succession planning - No such plans but looking at talent acquisition.

Tetra Recart - Advanced trials with MNCs. Packaging for consumer products.

Continuing to see strong growth in the domestic market. Coke and Pepsi are growing 22% and targeting a doubling of capacity in the next 4 years (because a shift towards packaged food/beverage is gaining momentum?). F&I are also planning capex in line with this.

Competitors aren’t faring well (which explains gain in market share this year) - Capricorn in NCLT and Jain Irrigation facing some issues too.

Kusum Masala - Plan to convert to a private limited company. Will also focus on the domestic market, but projecting more growth in exports. Plan to make this a sizable business in the next few years. (does the fact that they’re focussing on exports imply that they’ll be focussing more on higher margin blended spice mix?)

Tetra Recart - Is an advanced solution compared to Tetra Pak - cost-efficient, space-saving and eco-friendly.

Expanding cold room capacity - Increasing efficiency and cost-saving in the frozen food business.

Tetra Recart (Rs. 35-40 crores) and Pectin (Rs. 15 crores) - I am not sure if these are capex or revenue figures.

This year’s revenue growth attributed to three reasons - growth in the Indian beverage Industry, competition operating at a low-level and “tied-up” contract manufacturing.

India currently imports 95% of its pectin requirement and it is majorly from China. The landed cost of imported pectin from China is Rs. 1200-Rs. 1400/kg, while it’s Rs. 750-900 for F&I (I am not sure if this figure is based on actual production cost or an estimate of cost, but sounds quite encouraging either ways).

Pepsi, Mala and Mapro have approved lab test results for Pectin. They see a large use case.

First putting up a 150 MT pectin plant in Chittoor.

See an opportunity to expand in other mango growing countries. Also looking to manufacture Pectin using Banana peels.

Q3 concall and notes in thread is a good resource to get a glimpse in changes

Some of them that stands out are

Structural shift in demand in domestic market - juices/pulp etc gaining prominence and co has all major brands with them coke/pepsi(fruit drinks). - concall is a good listen

PLI win strengthening mgmt ambitions - mgmt had first concall post Q3

QIP done recently gives them fire power to scale biz (being WC intensive)

Communication effort - AR is a good read, press releases and concall started

Operating model transformation - a co which used be seasonal/majority mango is pulp/majority exports is now delivering more predictable/non mango share increasing/domestic share increasing/value added mix focus - to some extent visible in last few qtrs

Optionality - pectin (higher GM biz to come online by June 23), new facilities for spray powder and tetra recard went live in Mar 23 - to aid in Fy 24 performance. Co also focusing on own brand and spices performance to improve

AR also points out sustainability focus and thus thinking for long term as they work with marquee global brands like Coke, pepsi etc.

mgtm has indicated Gross profit/kg (varies by product) as key metrics - along with volume growth pattern

supply side organized player competitive intensity - though not many players here e.g. possibly jain irrigation one of listed player seem to be having bal sheet challenges(have agro segment)

Valuations and price action is supportive for some re-rating and growth

Projecting a growth of 25-30% in volume for FY2024.

Recently expanded frozen foods division to double current capacities and get into frozen and chilled foods.

Launching a pectin project joint venture with Beyond Mangoes by end of June or July 2023.

The objective is to have 40% non-mango business and 60% mango business in the next three to four years.

The company is exploring multiple options for capacity expansion in the pulp, tomato processing, and spray drying processes but has not yet determined the capex required.

The pulping business accounts for 85-87% of the company’s revenue, while the non-pulping business accounts for the remaining percentage.

Realization rates are dependent on raw material prices, and the company works on a cost-plus model with fixed realization per metric tonne.

One group of promoter selling has been an overhang, in Q4 call there were questions around disclosures on same, now seem to have filed a consolidated till date updates

almost 20% to 8% stake in last few months for exiting promoter, accelerated selling in last few weeks - supply has been absorbed well by mkt, at this rate another 3-5 weeks this should be over.