Of course the individual businesses above have some issues - that Mr Market is still coming to terms with - about whether to bracket the issues in Ignorable category, or not. But there are no two interpretations of the story the numbers seem to be telling!

@rohitbalakrish_

You are putting me on the spot. I thought subtle hints would suffice

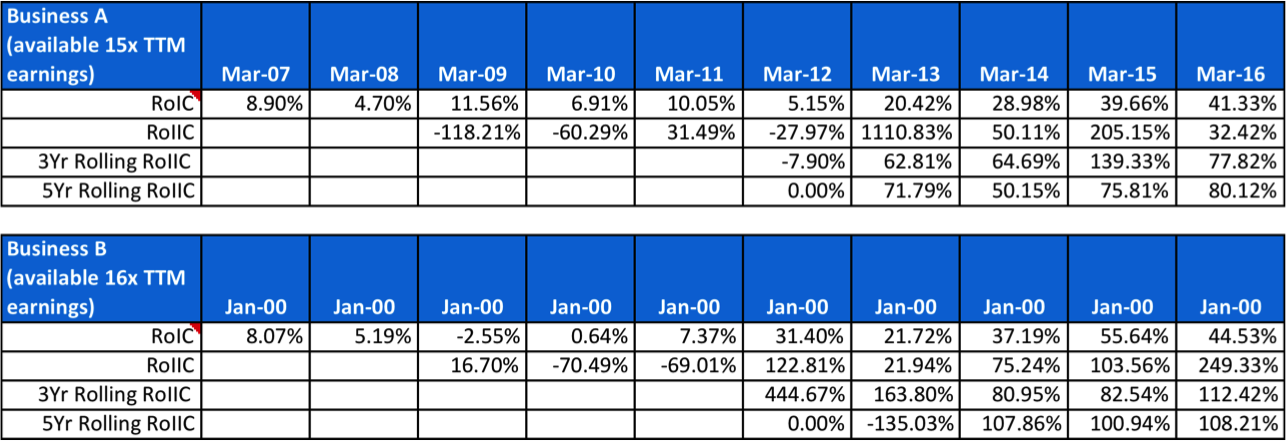

1.Generic comment specific to Business A & B.

Everyone will agree Business A and B numbers look good. Now the fact that they quote at 15x and 16x TTM basis - despite indisputable numbers - implies that Mr Market hasn’t made up its mind on BQ/MQ and sustainability.

Potentially, there lies lot of opportunity - GAP between Perception (15x) and indisputable business performance

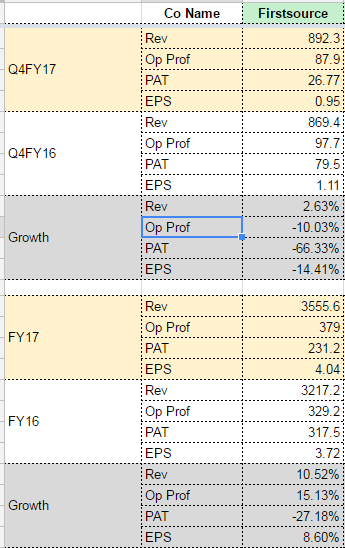

2.Re: FSL

To me FSL numbers are telling an average revival/sustainable story. The GAP between Perception (11x) and actual Business Performance is not that apparent (to me) - and hence, subdued potential opportunity.

Concentrated guys like me, need to choose very very selectively.

Given the (past) data points, I wanted to see what are the reasonable baseline assumptions we could make for a business like this - trying to come to the same page as everyone else on this business

Sales growth for next 2-3 years: Baseline between 8-10%? more than 10% growth assumption would be optimistic?

Business value-migration (assuming they start playing at the level that a WNS does today) may add again a couple of percentage points to Operating Margins

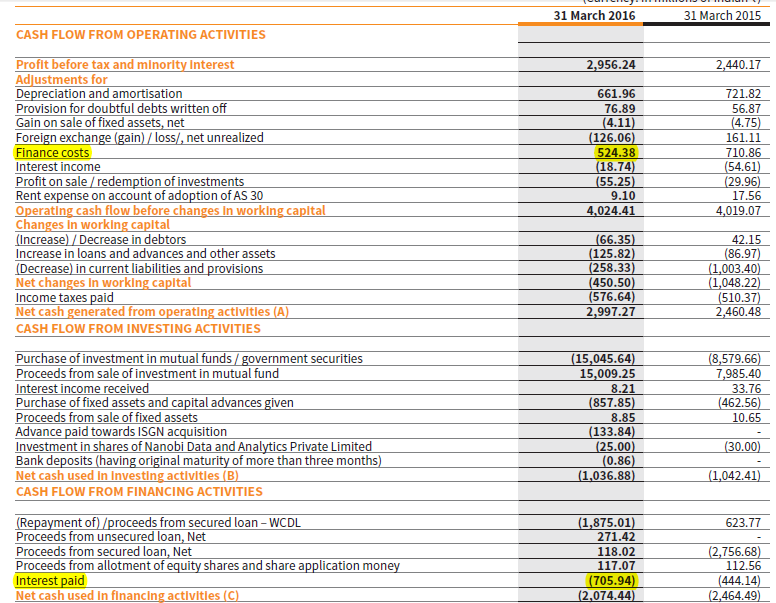

Debt Reduction in next 2-3 years: 905 Cr debt gets completely paid down

Consequently Interest Expenses (historically between 2-4% of Sales) may aid Net Margins to expand by 2-3%

One would make the case that

a) if Pt2 - margin expansion - is not happening for this business, then there isn’t much case for investing in this business at this stage

b) again if Pt 3 - Debt Reduction - is not happening in this business there is not much case for investing in this business at this stage

c) If both are happening, then that might be the best case for this business

d) It would look like Pt3- Debt Reduction - is a certainty (from past repayment patterns)?

If these are reasonable assumptions to make for the medium term of the business, those invested, Please comment if these are valid

One can then make the base-case with debt reduction, sales growth at 8-10% for next 2-3 years

The Optimistic case - would build in another 2% operating margin expansions in getting a feel for where this business can reach in 2-3 years

Please point out if there should be other significant considerations while thinking about this business. I am assuming that other than these, there are no big-ticket expectations from a reasonably well-understood business like FirstSource.

That there aren’t much “Variant” Perceptions about making an investment thesis on this business (a la Howard Marks asking the question - And, who doesn’t know that ??) is what I am trying to understand

I would say 10%+ growth in dollar terms is something that would be achievable. In INR terms hence this would be higher than 10-12%.

Other things I’d broadly agree with you. However, if that were to happen then I think the chances of the multiples getting re-rated are pretty high.

For a business generating strong & growing cash flows, buying it at ~ 7-8 times cash flow (currently @ 10) offers significant margin of safety for me. Incremental improvements in the business (not major) will help the business getting re-rated, in my view.

Their Base case scenario for Revenue growth is 15% in INR. India Business (reduced from 700 Cr to 300 Cr Apprx) will go back to 700 Cr over 3 years. That is a 3% CAGR. Bank of Baroda deal $ 45 m. Moving the mix from Telco/Voice to BFSI + Telco ( Voice + Data)

Sky will add 8% CAGR over 3 years. Deal size 10,000 Cr over ten years. Ramp up years 2-3

I am assuming other business will contribute to 6% ( If Refinance Picks up >IGSN another $12 m, their pipeline is $ 350 m. 25% conversion.)

They are not like WNS. However, all BPO Cos are similar in a way. I doubt they will go beyond 14% EBIDTA.

Their Net Debt is $ 73 m. and they have been committing to be debt free by end next financial year…

They have been religiously paying m 11.5 $ every Quarter… Last two years paid m 92 $ (11.5 *4 * 2.)

The kind of business they are getting into will need them to invest upfront. Like Sky.

Volume :

A lot depends on how Payers business takes shape ( Obama care >> Trump >> Change of Business model) Although they are strong both in Payer and Provider.

Interest Rate in US > Refinance Volume > ISGN.

Ebita will depend on automation not as much on Debt Reduction. Most of their delivery is on sight and any automation will mean significant cost take out. One FTE reduction on site is equal to 15 FTE reduction offshore.

They have done well so far in platform. Reasonably deep IP in robotics and analytics. If they use Digital to customer servicing (SKY etc. ) they can increase Operating margins and cross sell Analytics.

That is not the only parameter for investing. Sometimes, the time horizon is equally important. Not everyone has the wherewithal (for various reasons) to buy and hold on when they are aware that the story may take a few years to play out.

Avg. Salary of Indians in US = ~ $80k = INR 53L

Avg. Salary of Indians in India (IT companies) = ~5L-6L

One FTE reduction in US => 53L /(5L or 6L) = ~9 to 10 reduction in Offshore (not considering one FTE increase in India when one reduced from US)

The company continues with loan repayment - Announcement on BSE, "Firstsource Group USA, Inc, a wholly owned subsidiary of the Company has successfully made its Eighth quarterly repayment of USD 11.25 million on its outstanding debt on March 31, 2017. "

Co is clearly on a well laid out path to decrease its debt and strengthen its balance sheet. It is well entrenched in the business it operates and seems that the co is getting its act together.

I had talked to Mr. Iyer today who handles the investor relations. He said there will be no equity dilution and FSL will operate independently. The only change will be the inter se transfer from “Spen Liq Private Limited” to “CESC Ventures”

I had also asked him if there is any fundamental issues or corporate action within the company as the stock price has corrected a lot. He assured me that everything is going fine with the company.