Hi guys

would really appreciate those who are following FSL to compare it with HGS. I feel HGS is hugely undervalued compared to its peers, and hence has better chance of delivering shareholder returns from current levels.

Is this different from the previous deal with SkyTV?

Edit: It’s the same deal and they have signed an official contract now.

Firstsource Solutions Ltd has informed BSE that

Firstsource Solutions UK Limited (“FS UK”), a Wholly Owned Subsidiary of

the Company and Sky Subscriber Services Limited, UK (“Sky UK”) has

signed the contract for the previously announced 10-year strategic

partnership. The Letter of Intent for the same was signed on July 18,

2016 last year and was sent to the Exchanges on the same day.

I have recently invested in Firstsource Solutions. Wanted to share my thought process on how I am thinking about this investment opportunity. My thesis is predicated on the following points-

Inherently sticky business with strong cash flows - The BPM business is inherently very sticky, most of the revenues are from your existing customers. Entering a new customer is a long-drawn lengthy process. And if you are an important vendor to your client, your exit is also not that easy. This leads to predictable revenues and cash flow. The table below shows the Cash flow from operations for FSL over the years

Improvement in Business quality over the last 4 years - Over the last four years, the company has been consistently improving its business quality by exiting low/non profitable ventures and getting bigger & more outcome/fixed priced contracts. For e.g. -

.` FSL’s domestic business which is a low margin business has been consistently downsized/reduced. As a result of this its contribution to overall revenue has declined from 13% in FY13 to ~ 6-7% in H1 17. Also # of employees in India has reduced from ~ 21 K to ~ 15K

Also it has reduced its share of voice revenues, which is largely a commodity service. Share of voice revenues has reduced from 70% 5-6 years back to ~ 30-35% at the moment

Focus of the company has been to win bigger deals, for larger tenures and where it can sell some productized solutions. It has won two such deals recently - a) SKY Deal - 10 year deal b) Lloyds banking deal.

All these efforts towards improving its business quality have resulted in improving its return metrics

Consistent de-leveraging- FSL’s probelm has been its acquisition that it had done 8-10 years back. The acquisition was done at a high price and the economics, this was financed through a FCCB the company came close to defaulting, this is where the company changed promoters and a new promoter in the form of Sanjiv Goenka came in. The FCCB was re-financed and since 2012, the company has been consistently repaying its debt This has been facilitated by strong cash flow generation in the business. Over FY12- FY16 the business has generated INR 1146 Crores in operating cash flows and ~ 900 Crores in free cash flow

Given the current run rate of repaying USD 45 MN every year, the business should become debt free in the next couple of years. This will add to the bottom line in terms of savings in interest cost. While, interest costs have already come down drastically, there is some more room to go

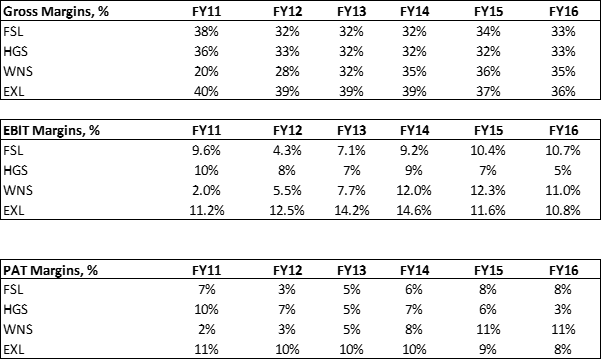

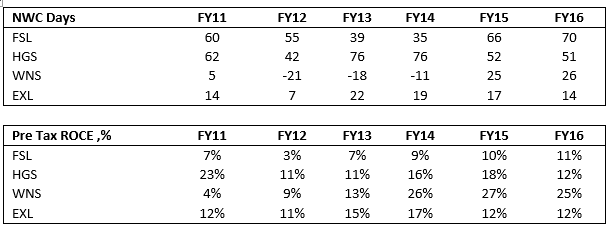

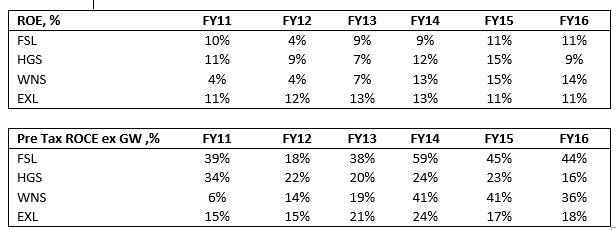

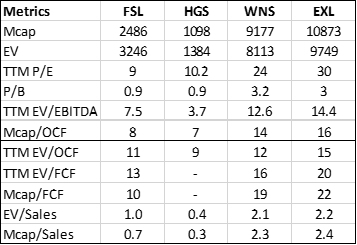

Cheap valuations - FSL looks undervalued both at an absolute level and also on a relative basis. Below is a peer comparison for FSL & some of its peers

Most of the metrics, barring debt/equity and working capital , are similar for FSL , EXL & WNS. However the valuation difference is stark as shown below

As the company becomes debt free, i feel the company can see multiple re-rating, helped by some momentum in the business & earnings

Key Risks

Slowdown in healthcare vertical spending owing to unfavorable US government regulations

Increasing protectionism across western countries -

US Yields rising - ISGN is in the refinancing business, rising US treasury yields will impact the demand for re-financing

INR currency appreciation -

Technology risk owing to automation -

Discl : Invested in the company. I am not a SEBI registered Investment advisor, This is not a buy/sell recommendation. Please do your own research before buying/selling a stock.

Thanks Rohit for your detailed inputs.

Some observations based on Screener Excel: (as is usual, I know nothing about this business). Please correct if below data points are wrong.

a) Huge Invested Capital in the business (2600 CR NB and 600 Cr WC)

b) 10-11% EBIT Margins, 1x Capital Turn => 8-9% RoIC (In a low EBIT margin business, you definitely need high Capital Turns to compensate)

c) What about low tax rates between 5-10%

How is this business creating any value over its cost of capital? at normalised tax structures, why is this business not destroying value?

Incremental Capital returns cannot be looked at in isolation? Unless the Capital structure of the business changes, how would this start generating Value?

What is likely to change in next 2-3 years, that above picture (if correct) would start looking much better?

Sorry that I have not taken the trouble to read through the thread. Please ignore this post completely, if the above has already been discussed in this thread before

The large portion of invested capital is owing to Goodwill of ~ 2500 Crores. This is owing to a large acquisition that they did a decade or so back. The debt was also for the same reason. What has been happening is that while the GW remains, the company has been re-paying the debt.

I don’t think the Goodwill can be immediately written off from the books, and hence the optical ROCE/ROE will be much lower.

However, if you take a look at the incremental returns, that sure are great. If you think about it, the business doesn’t need much capital to run. It isn’t capital intensive (fixed or working capital).

Tax rates are at about 15-18% and not at 5-10%. Largely because of overseas subsidiaries.

Not sure if we can/should take out Goodwill (Thats a sunk cost, and needs some amortization write-off eventually). If we take out Goodwill, BS quality? Impact on D/E? By the same token if that entire Goodwill is taken out, D/E is much higher (worse), looks optically low now.

Subject matter Experts can comment on that.

I remember Opto Circuits had lot of goodwill in BS in 2011 (due to high-profile acquisitions in later years). And we were advised to take that into active consideration, while looking closely at the quality of the BS.

HI Donald, I am in agreement with you about taking in account the goodwill. However, I think in the case of FSL, the business has been punished for that error, and now they are re-paying that debt against which the goodwill is there. A large portion has been repaid as mentioned in the post. The remaining the company is repaying regularly.

They don’t need any incremental cash to fund their business, thus the incremental returns are strong.

On a diff note, as per Ind-AS don’t think the goodwill needs to be compulsorily written off. I could be wrong here.

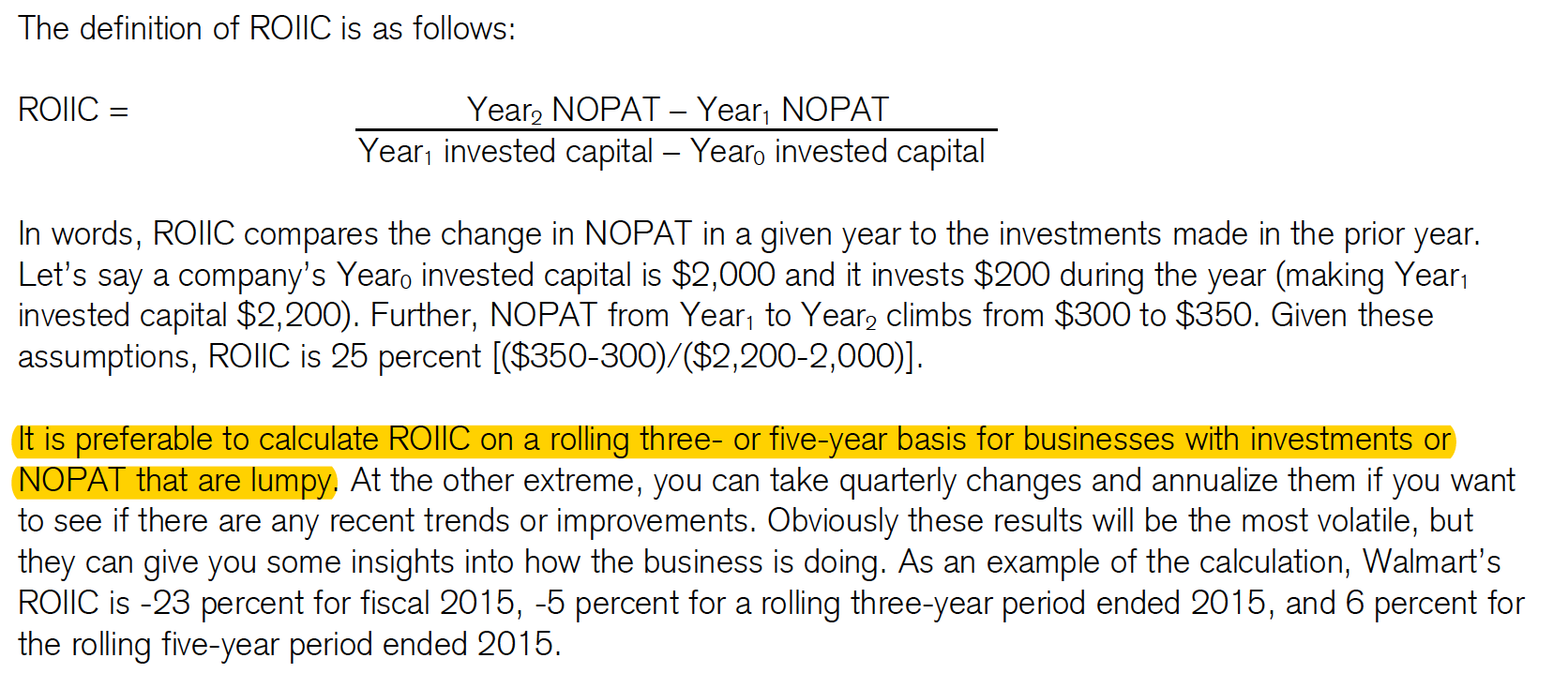

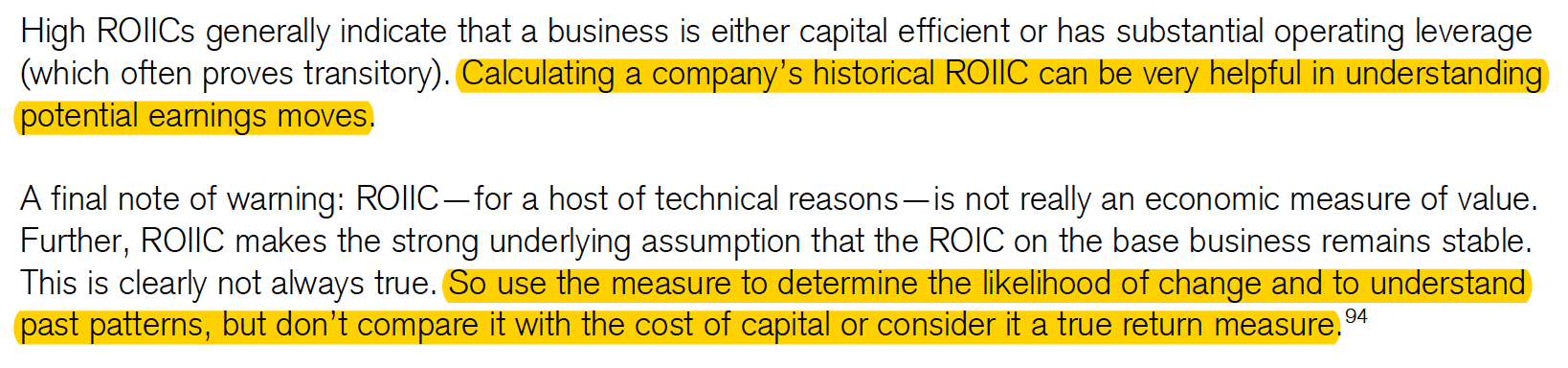

I have always wondered about the correct way to look at Incremental Return on Invested Capital. So Rohit’s poser on RoIIC took me on another back-to-basics trip

So here’s a question for you Rohit/other CFAs/subject matter experts.

I do not see FirstSource EBIT and/or Invested Capital as lumpy - its rather progressive year on year. Firstsour.Solu.xlsm (88.2 KB) {Rohit/Others - will be good if you can check/correct the rolling RoIIC calculations; you guys are the experts}

Why isn’t the year on year RoIIC data a more relevant picture? (since last 5 years EBIT data is linearly progressing while Invested Capital is more or less same)

If we look at the Net Block and Working Cap data more closely over 3 or 5 year periods, is it the case that 5 year rolling looks optically better?

Back to the basics question for me: Is the Business really that much stronger?

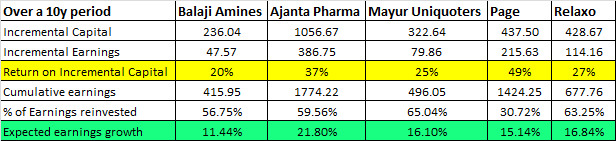

While incremental returns on incremental capital invested is a useful measure, a slightly more useful measure in my opinion would be incremental returns on incremental equity deployed. This would allow us to create an estimated earnings growth rate for the business as well ( based on the earnings retained )

While nothing can replace the subjective & qualitative analysis of the more seasoned investors on this thread, a look at the incremental returns on incremental equity can be revealing.

After looking at some of the blockbuster stocks of the forum I can say for certain that they have been able to deploy additional equity capital at really high rates over a very long period(10 yrs)

*incremental capital = incremental equity capital

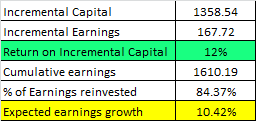

Circling back to FSL -

Over a 10y period, the incremental return on incremental equity has been a moderate 12%. Its not good or bad. 84.37% of the earnings have been reinvested which translates to a expected earnings growth rate of 10.42% ( 12% * 84.37%)

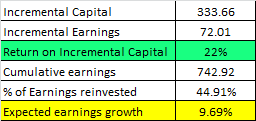

However, if you look at the rolling 3 year rates, thats where all the fireworks are.

In the last 3 years ( March 14 to March 16 )

The return on incremental equity has jumped significantly to 22% but the company is reinvesting only 44.91% of earnings leading to a lower growth expectation.

In my opinion i think the company is doing something ( i have not done enough reading on this company so please take this opinion of mine with a lot of skepticism ) that is manifesting itself in the numbers. However i don’t think the company is going to grow its earnings by more than 10%

There is market buzz of Firstsource sale by CESC. Punters indicate a potential transsaction price of Rs 65-70

Note that CESC invested in Firstsource back in 2012 which was nearly 4.5 years back.

Some of the recent M&A action in the BPM space suggests that transactions have typically happened in the 1-1.x EV/Sales multiple barring the Aegis BPO takeover by Teleperformance at 1.5x Sales multiple( This probably was on the higher side as Aegis had a higher share of domestic BPO business which is less profitable).

Firstsource also trades at ãbout 1.1x EV/Sales multiple on FY17…

But as one says ‘Beauty lies in the eyes of the beholder’… so never say no to any possibility…

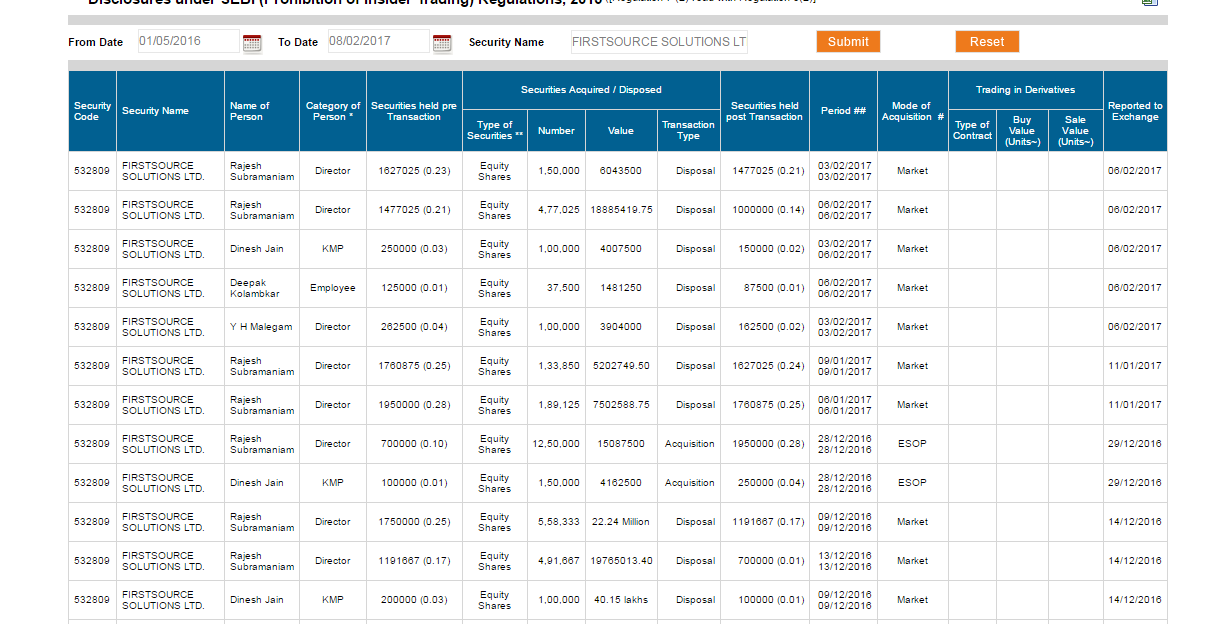

I have noticed a pattern in FSL (am holding this for a while now). As soon as the stock price crosses 40, there is disposal of shares by Rajesh Subramanyam (MD/CEO ) of the company and other directors - which does not look good.

You can take a look here http://www.bseindia.com/corporates/Insider_Trading_new.aspx?expandable=2

Hi Rohit

Nice inputs.

Question: The company has been repaying debt regularly for the last 6 or more quarters. At the current cash flow and the current quarterly debt repayment rate, when is FSL expected to become debt free?

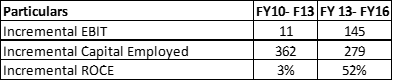

Above is the table for YoY Incremental ROCE. There seems to be some difference in your table & mine.

I don’t use YoY is because sometimes there are distortions in on the capital employed or on the EBIT level which can create noise (For e.g see FY15 data).

However, I feel it is worth looking at YoY data also in conjunction with rolling data. Both should broadly share the same insight is what I feel.

I feel incremental ROC (rolling/YoY) is the way to look at things is because of the goodwill which is there on the BS. Because of the GW the ROCE/ROE will never look good, But I feel inherently the business has gotten stronger as seen with the numbers.

As I have mentioned in the note, I feel over the next 6-8 quarters I feel they will be debt free. They can then start utilizing the cash and perhaps start paying dividend. In the current call, the management also alluded to the same.

This message has been circulated by some broker, I also received it. I would request people to just not copy paste such messages as there is limited value add. In case someone is posting, it is better to mention the source.