CMP â 292 - Market Capitalization - 3636 cr

Part of the Finolex Group. Manufacturer of PVC Resin, PVC pipes and fittings. Till 2008, this was primarily a PVC resin manufacturer. Management however realized that the real money was in the end product and has gradually shifted to becoming Indiaâs largest manufacturer of PVC Pipes.

Change in management guard from father to son â also led to a fresh wave of thinking and the debt that was weighing down the balance sheet has significantly gone down in the last few years and if the management is to be believed â it will be a debt free company in 2 to 3 years.

Revenue Growth: India still has a long way to go in irrigation and there is significant potential opportunity for this company to expand it revenue. Though it is not expected to post scorching growth rates â but it still expects to compound revenues at 15-20% for the next 5 years. They have set up a new warehouse in Orissa and are aggressively targeting the North East region for growth.

Moat: Their distribution of network of 15000+dealers and a strong brand which allows them to command premium pricing for their products.

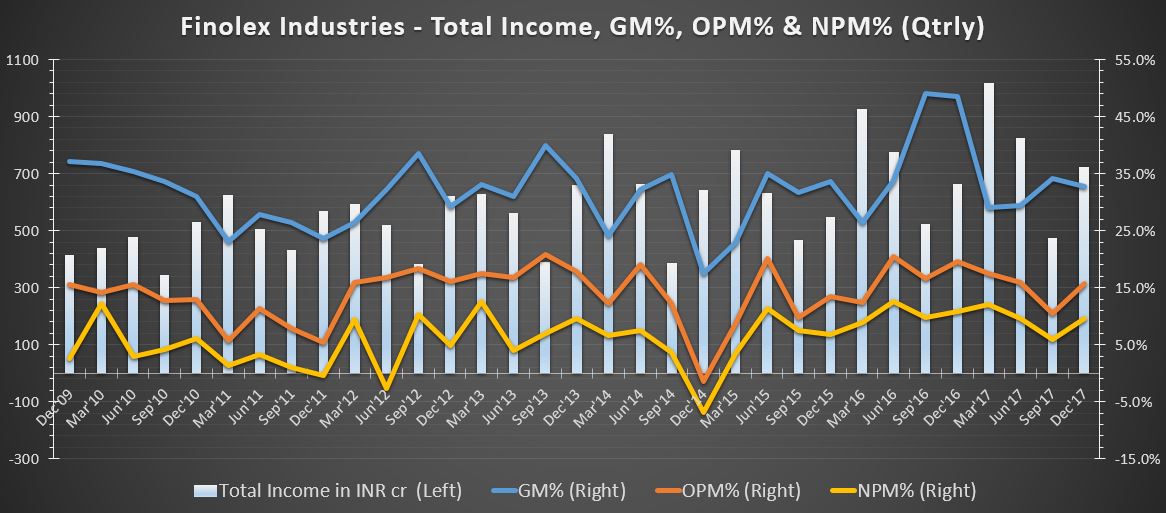

Improving Margins: As they have steadily moved from resins to PVC pipes and now PVC pipe fittings â the margins earned by the company are continuously improving. EDC â one of its key RM will be seeing significant capacity addition particularly in North America due to the Shale oil boom. This is expected to reduce the EDC prices and thereby improve the margins for the company. Fittings are also a very high margin product and their introduction to the mix is expected to add to the margin expansion in the upcoming years.

New Products: The company announced a few months back that they will be entering the water business - particularly water supply equipment and water filters. This is currently under planning stage and they expect to launch this perhaps in Q4 â FY16 or Q1 FY 17. According to a report issued by Barclays in July last year current market size of water supply and sanitation is $6 million and is expected to grow by $10-12 billion by 2016-2017 according to Planning commission estimates.

This is a market with significant competition and thus their forays in this venture will need to be closely followed.

Free Cash Flow Generation: They work on advances from the dealers (similar to Atul auto ??) and thus their cash flow generation seems pretty good. Cash flow from operations for last 2 years is averaging 250 crores a year.

Debt Repayment: They have also paid down debt of roughly 600 crores in last couple of years. Debt on FY14 balance sheet is 636 crores.

Black Swans â what can go wrong: Since RM is imported â exposure to foreign currency fluctuations is a significant risk. They have however began hedging their exposure recently.

Cheaper Imports ? Not at present â but cannot rule out completely. It though has the advantage of manufacturing its own resin.

Water Supply Foray â This could go wrong and damage future FCF generation.

Valuations

At current CMP of 293 â it is available at a TTM PE of 19.

Couple of important observations: The company owns 14% in Finolex Cables which is worth 550crs at CMP. The company also owns industrial land at Chinchwad, Pune. Though various values have been quoted in different articles âon an average â this land is worth 500-600 crores. They have been actively trying to sell this for last 4-5 years â but havent managed to do so yet.

If we take these two aspects into consideration â we are getting the operating business at approximately 2500 crores.

Not to forget a dividend yield of 2% at CMP.

Other PVC pipe manufacturers like Supreme, Astral enjoy much better PE multiples. If the debt hangover goes away and margins further improve, there is also a chance for PE rerating. However even without such rerating â it appears to be good candidate for compounding in my view.

Though its not a bargain price â is it a good business at a fair price?

It appears imho to be a stock which can be a steady long term compounder with reasonable downside protection.

Views invited to poke the bubble and feel free to raise as many doubts or questions.

Disc â Invested and you may assume that I am biased in its favour. :)

Financial Snapshot for last 3 years (figures in crores)

| Mar-12 |

Mar 13 |

Mar-14 | TTM |

|

|---|---|---|---|---|

| Sales | 2099.78 | 2144.82 | 2453.03 | 2548.21 |

| Op Margins |

10.32% | 12.25% |

16.17% | 15.10% |

| Net Profit |

75.15 | 136.14 | 170.15 | 183.99 |

| Div Payout |

41.50% | 42% | 42.37% |