-

Consolidated revenue of INR 1,419 million for Q1 FY2025, up 7.3% year-over-year

-

EBITDA of INR 353 million, up 11.8% YoY, with 24.8% margin

-

PAT of INR 292 million, up 11.7% YoY, with 20.6% margin

-

Textile segment: 46% of revenue

-

Cleaning and hygiene segment: 54% of revenue

-

Successfully raised INR 3,425 million through preferential allotment to support growth

-

Appointed Dr. Amit Prabhakar Pratap as Additional Director to leverage his expertise

-

Exploring manufacturing partnerships with Eurodye in Asia to improve efficiency

-

Focus on sustainable and eco-friendly product lines

-

Expansion into international textile hubs over past 3 years

-

Ongoing development of new products to meet changing customer demands

-

Textile industry showing signs of recovery after a challenging 2023

-

Geopolitical issues and container shortages impacting shipping and raw material costs

-

Increased freight costs and container shortages presenting challenges

-

Currency fluctuations impacting costs

-

Company aims to repeat performance of last 3-4 years in coming years

-

Expects to maintain comfortable EBITDA and gross margins

-

Funds raised will be used for organic and inorganic growth opportunities

-

New facility expected to be operational by end of current financial year

-

Opportunities in sustainable solutions for textile and cleaning industries

-

Increasing demand in textile sector as inventory levels normalize

-

Growing interest in sustainable solutions from customers

In one of the call, management answered that the maximum capacity of Ambarnath - 1 plant is 150,000, however post that they bought additional land nearby and doing capex there. Can anyone help why they are not utilizing space available at plant-1 first before starting at new one?

Source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/1d24a9e6-d5f9-44af-86ad-fd92534d69c1.pdf

Just noticed few notable names who participated in fund raise:

- Arti Rajendra Gogri (from family of Chairman & MD of Aarti Industries) subscribed shares of Rs.7.8cr

- Ravi Vasudeo Goenka (Chairman of Laxmi Organics & Ex-president of the executive committee of the Indian Chemical Council) subscribed shares of Rs. 3.5cr

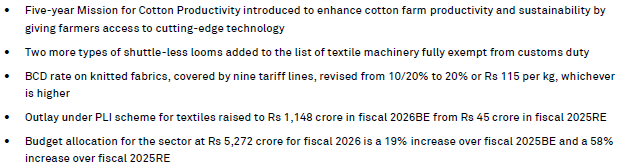

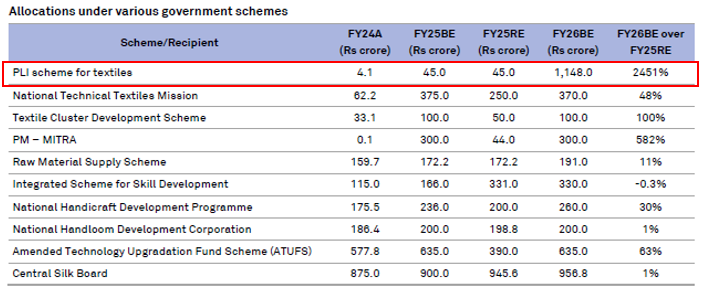

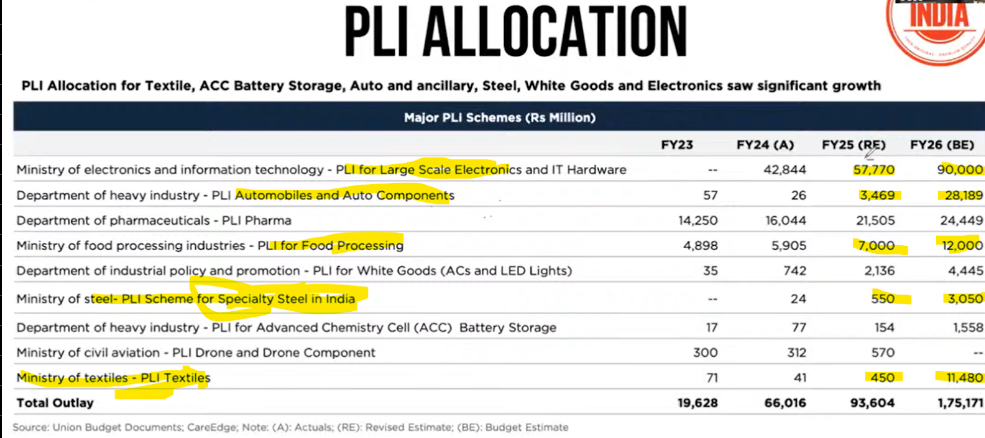

Textile got biggest push from government through PLI allocation leading to 2451% growth compared to FY25 revised estimate, should contribute positively to growth of textile sector and indirectly leading to growth of textile chemicals mfr like Fineotex.

Other announcement related to textile sector:

Source: CRISIL Intelligence report

can you please share the entire report here

The data from SOIC says its 20X increase in PLI for textile. Anyone with better knowledge can suggest what is correct figure.

As per the image, growth its 25x growth, which is equal to 2451% in percentage terms, where’s the confusion?

Ohh…my bad, missed that your image had percentage.

So a good potential for textile sector to grow.

Thanks. Here are a few companies I am tracking in the segment:

- FCL

- PGIL (Pearl Global)

- NITIN SPINNERS

- VARDHAMAN TEXTILE

- GARWARE TECH

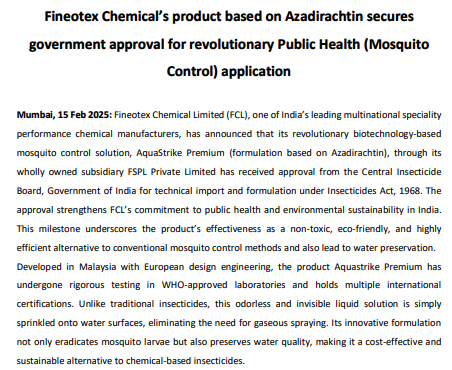

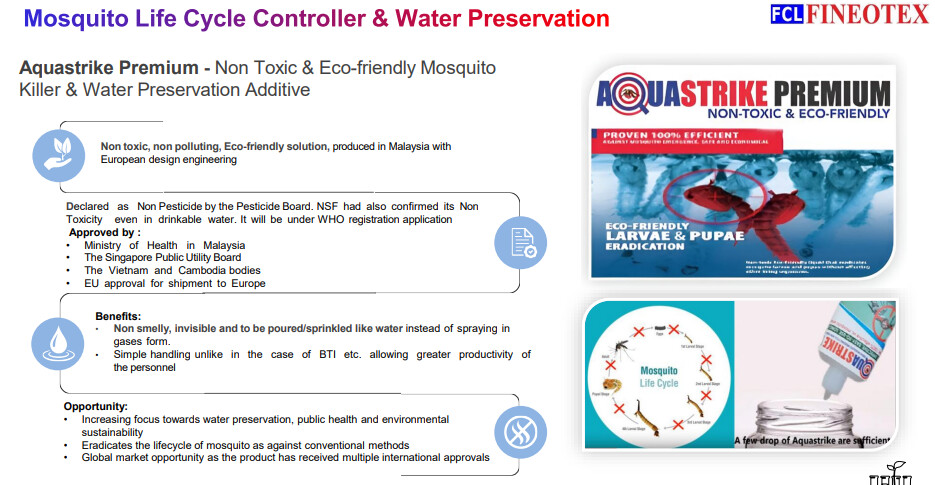

Finally after a long wait, company has recd approval from Government of India for its Aquastrike product; need to monitor the status of its approval in WHO

Good read on potential impact of tariff on textile sector:

Also, latest interview from Mr. Tibrewala

Just read that India imposed port restrictions on the import of certain goods such as Readymade garments from Bangladesh to India.

Would this affect Fineotex significantly? We’ve already seen exports impacted by Bangladesh before…

Been a year since they have raised cash

Still no sign of any acquisition

They have covered it in the Q4 call. The dip is attributed to Capex spend, Marketing expense and deferred order due to geopolitical tensions in Bangladesh.

Financial Performance (Full Year FY25):

- Total Income: “flattish as 558 crores year on year.”

- Gross Profit: “205 crores with margins being stable at 38.57 percentage.”

- EBITDA: “127 crores,” with margin softening “by 222 basis points to 23.85%” due to “capex and brand building initiatives.”

- PAT: “109 crores” (vs. 121 crores in the previous year), with a margin of “20.48%.”

- Cash Balance: “52 crores” after investment in the new facility and corporate office.

- Exports Share: “22% during the quarter.”

- ROC: “23.56%.”

- ROE: “18.32%.” (Moderately lower temporarily due to fundraise and higher capital base).

- Operating Cash Flows: “69.33 crores,” with a “healthy CFO to EBITDA ratio of 54.50 percentage.”

Deferred Orders:

“Certain deliveries were postponed during the quarter for financial year 25 due to certain geopolitical tensions in Bangladesh and other places and the trade related disruptions.” These are “expected to be fulfilled in the current financial year.”

I don’t understand how capex can affect EBITDA, also marketing expense would have been classified under other expenses in the PNL which has increased by 4 cr only if we compare it with FY24. EBITDA loss is mainly because of subdued demand and Bangladesh crisis.

Bangladesh wont improve anytime soon and with India putting more restrictions on imports from Bangladesh there are more problems to come.

The main issue however is not effectively deploying the capital they raised last year for acquisitions.

Thnaks you Sarthak & ksaravanan

Even I think the Bangladesh challenge is not going to disappear soon, any idea how much revenue comes from Bangladesh. In Q4 PPT they briefly mentioned UK trade deal, but no idea how they are going to leverage it and what the potential impact on revenue & margins could be going forward.

Does anyone know why the promoters decided to sell equity shares in a company with such a niche high margin, higher ROE business model and no debt on the B/S? They could’ve gone for debt raise too which would have been cheaper and would have been ROE accretive!

Are the promoters overly conservative?

Secondly, what and when are they going to use the money raised last FY?

That’s a good question, I am not sure either, could be that they wanted to maintain the Debt level.

- They have offered warrants at ₹387/share, the current share price is around 235/share

- Investors (and promoters) paid 25% upfront.

- They have time till November to pay the remaining 75%.

- Even if some don’t convert, the company:

- Keeps the money paid

- Loses nothing

- The same is the case with promoters as well, they have paid ₹11 crores and need to pay 33 Crores to convert.

- First Tranche (May 22, 2024):

Warrants can be converted within 18 months from May 22, 2024, upon payment of ₹259.5 per warrant, according to CNBC TV18.

- Second Tranche (July 19, 2024):

Warrants can be converted within 18 months from July 19, 2024, upon payment of ₹290.55 per warrant, says CNBC TV18.

Therefore, the conversion deadline for the first tranche is sometime in November 2025 (May 22, 2024 + 18 months), and for the second tranche is sometime in February 2026 (July 19, 2024 + 18 months).

They say that, the money will be used for Organic and inorganic growth.