Moreover, one negative which I see is shockingly low CFO to Operating Profit - Really concerning!

2 Likes

Ashish Kacholia added another 10 Lac shares on 03 August

An interesting take on textile sector - given that Fineotex is specialty chemical supplying to the textile sector (60% of sales) The Mega Textile Push Explained

Also there are some red flags that I see in their numbers and statements a) Most of its ratios such as cash conversion cycle, working capital days are in upward trajectory since 2017; which is not a good sign. If the demand is high and they are niche supplier they must be able to negotiate better terms and improve on these ratios. b) Any idea on why promoter equity dropped in Dec 2020? c) Also diversification into Health & hygiene is a crowded market, and we don’t have enough information on what chemicals are they supplying in Drilling business, there is not much info in public domain.

What proportion of revenue comes from Textile chemicals, Cleaning & drilling business?

Fineotex Chemical Q3FY23 earnings call highlights. https://www.bseindia.com/xml-data/corpfiling/AttachHis/7bdb8968-f23d-419d-8225-57c435022996.pdf

-

In quarter Q3 FY23, our operational revenue improved to Rs.1,092 million from Rs. 1,051 million. The operational EBITDA has grown by 14% from Rs. 251 million to Rs. 286 million with a margin of 26.1%; PAT grew by 17.8% from Rs. 191 million to Rs. 225 million and with a margin of 20.6%. The volume has doubled and the increase is 100.12% Y-o-Y basis, demonstrated a strong performance.

-

Our bestselling antimicrobial treatment HealthGuard AMIC has received the US EPA approval.

-

we have proceeded towards more FMCG cleaning and hygiene businesses, which has a better cash flow and a better working capital requirement compared to the traditional textile chemicals. Right now 40% of our sales value of the Q3 is from the cleaning and hygiene segment.

-

Large order from an FMCG major for around Rs. 150 crores in the last quarter, started supplying in Q3. We just had a small requirement in the month of December and a little bit in November. That was just the beginning of the consignments. Less than around Rs. 10 crores business was there on the new product line and this has been picked up now from 15 January also and I think you should be seeing that impact happening from Q4 for sure. And more importantly from the next year onwards, we are also looking at some more the upgrade in the volumes also going forward.

-

For textiles, I would like to mention the top 10 customers contribute only 27% of our business and the top 10 products contribute only 18% of our business. With the 470 product lines which we have and in that we are doing almost all sorts of chemistries, phosphonation, sulfonation, polymerization, esterification etc.

-

We are not those kinds of companies where you will find our EBITDA sometimes 5%, sometimes 35%, this will never happen with Fineotex. And this is not our business model. When we sell our products, we sell as a solution. The cost is not material to the customers, because like I always say, the full processes of textile together require 25 different functional chemicals and all put together contribute only 3% cost to the users. So every chemical is costing 0.15%, which is insignificant. At the same time, the risk of changing the chemical is very high. So there is a big risk entry and exit barrier for the businesses. Going forward also, you can expect similar range of EBITDA margins what you have seen in last few quarters.

-

Generally, the price per kilo, the realization in the cleaning and hygiene per kilo is quite lower compared to textiles. However, the volumes will always be good enough. So it will lead to the overall turnover would be almost again contributing to 40%, 50% going forward. Average realization per kilo in textiles, generally it’s like Rs. 130, Rs. 140, that’s the normal levels. But in the detergents, it’s almost like Rs. 60 to Rs. 65 broadly, per kilo. So it’s almost, you can say, little like almost 40% of it.

-

FMCG brands like Patanjali, and other ones have started using our products in their FMCG products.

-

In textiles, what also happens is there is a lot of promotional expenses, technical services, which we are providing and things like that. So there is a good gross margins in textiles as such. However, looking at the blended EBITDA, if you talk about the EBITDA margins, more or less, it is similar because in detergents, then your overheads are not too high from the point of view of giving technical services comparatively to the textile businesses.

-

Textile Sector: I see that already from 14, 15 January, things are getting much-much better than it was.

-

in the last five quarters, our business of cleaning, hygiene, FMCG has gone almost we can say almost 20x from where it was.

-

Right now, where we are today is like 1,04,000 tons. I think another 35%, 40% easily we can expand in the same line. And that would not take a lot of investments also nor will it take a lot of time comparatively. we have increased our capacity from 43,000 tons to 1,04,000 tons in the last 14 months.

-

Fineotex in a way as a very high end specialty chemical company which is translated by three things, I believe, is the EBITDA margins, which is consistently growing, consistently there. Asset turnover ratios are quite good enough, which also demonstrates our products specialty and the performance, the focus which we have. And the third thing which we are quite happy about is our cash flows, which is almost 87% to the EBITDA value so operating thing obviously.

-

Rs. 150 cr new order: Per kilo realization, this is around Rs. 49, Rs. 50 per kilo broadly. we have supplied I think around 2,000 tons only yes only 2,000 tons approx… So that would be around Rs. 10 crores only we have supplied in the last December month. And a lot of things has been postponed for the January month and things like that. That Rs. 150 crores will also be increased actually. So on a conservative level it is Rs. 150 crores.

-

Q4FY23 total volumes we are reaching around 18,000 tons to 20,000 tons, which I feel is not difficult.

-

Volume 21,000 tons for the nine months for the cleaning & hygiene. Full nine months volume is around 38,000 tons.

7 Likes

If you go by the commentary of textile players then things are improving sequentially. Have crossed checked with someone working HT co. the demand has come to normal levels.

Day by day orders are picking up as inventory with large retailers is getting cleared up.

Form H2Fy24 things should be alot better due to Lower base and festive demand.

3 Likes

Effect will be more on the absolute textile players. Fineotex’s good portion of revenue was/is contributed by the FMCG (domestic, as I write this) division too and this contribution is increasing in a progressive manner, and based on the management commentary in the last concall, contribution of 150cr order from FCMG will be major in the Q4. I don’t think numbers will be affected here like other pure textile players.

Disc: Invested

5 Likes

![]() FCL (Fineotex Chemical Ltd) - Q4 FY23 - conference call -

FCL (Fineotex Chemical Ltd) - Q4 FY23 - conference call -

Key Highlights -

https://twitter.com/AnirbanManna10/status/1661567695635255296

4 Likes

FCL Q1 FY24 Concal happened yesterday. I joined.

![]() Guidance of Growth :-

Guidance of Growth :-

https://twitter.com/AnirbanManna10/status/1689237024774270976

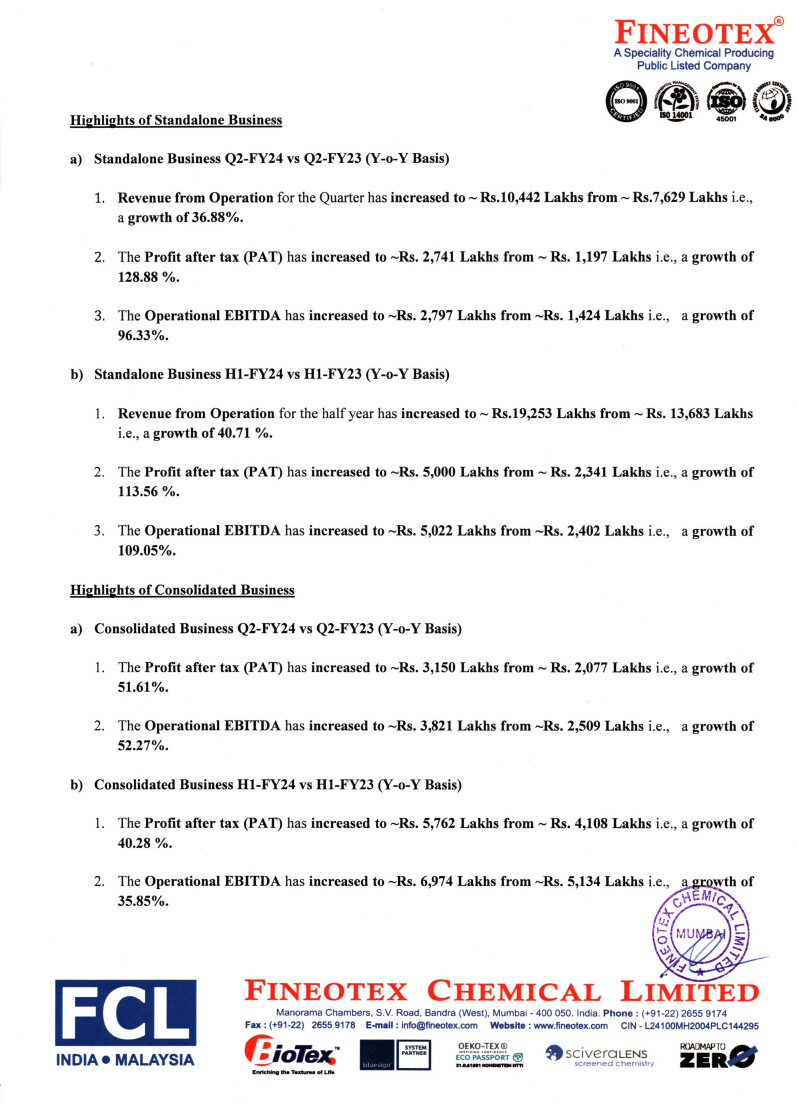

Fineotex Chemical Limited - Standalone and Consolidated Business Performance Highlights Q2-FY24

Standalone Business - Q2-FY24 vs Q2-FY23:

- Revenue Growth: Fineotex, a specialty chemical producing public-listed company, reports a substantial increase in Q2-FY24 revenue, reaching Rs. 10,442 Lakhs, reflecting a robust growth of 36.88% compared to Rs. 7,629 Lakhs in Q2-FY23.

- Profit Surge: The Profit after tax (PAT) for the quarter stands at Rs. 2,741 Lakhs, marking an impressive growth of 128.88% from Rs. 1,197 Lakhs in the same period last year.

- Operational EBITDA: The Operational EBITDA registers a noteworthy growth of 96.33%, reaching Rs. 2,797 Lakhs in Q2-FY24 compared to Rs. 1,424 Lakhs in Q2-FY23.

Standalone Business - H1-FY24 vs H1-FY23:

- Revenue Expansion: Fineotex continues its upward trajectory in H1-FY24, with revenue from operations surging to Rs. 19,253 Lakhs, exhibiting a robust growth of 40.71% from Rs. 13,683 Lakhs in H1-FY23.

- Profit Momentum: The Profit after tax (PAT) for the first half of the fiscal year reaches Rs. 5,000 Lakhs, demonstrating a remarkable growth of 113.56% from Rs. 2,341 Lakhs in H1-FY23.

- Operational EBITDA: The Operational EBITDA for H1-FY24 stands at Rs. 5,022 Lakhs, showcasing a substantial growth of 109.05% from Rs. 2,402 Lakhs in H1-FY23.

Consolidated Business - Q2-FY24 vs Q2-FY23:

- Profit Uplift: In the consolidated domain, the Profit after tax (PAT) witnesses a growth of 51.61%, reaching Rs. 3,150 Lakhs in Q2-FY24 from Rs. 2,077 Lakhs in Q2-FY23.

- Operational EBITDA Expansion: The Operational EBITDA for the consolidated business marks an increase of 52.27%, reaching Rs. 3,821 Lakhs in Q2-FY24 from Rs. 2,509 Lakhs in Q2-FY23.

Consolidated Business - H1-FY24 vs H1-FY23:

- Profit Growth: The Profit after tax (PAT) for the consolidated business in H1-FY24 registers a growth of 40.28%, reaching Rs. 5,762 Lakhs from Rs. 4,108 Lakhs in H1-FY23.

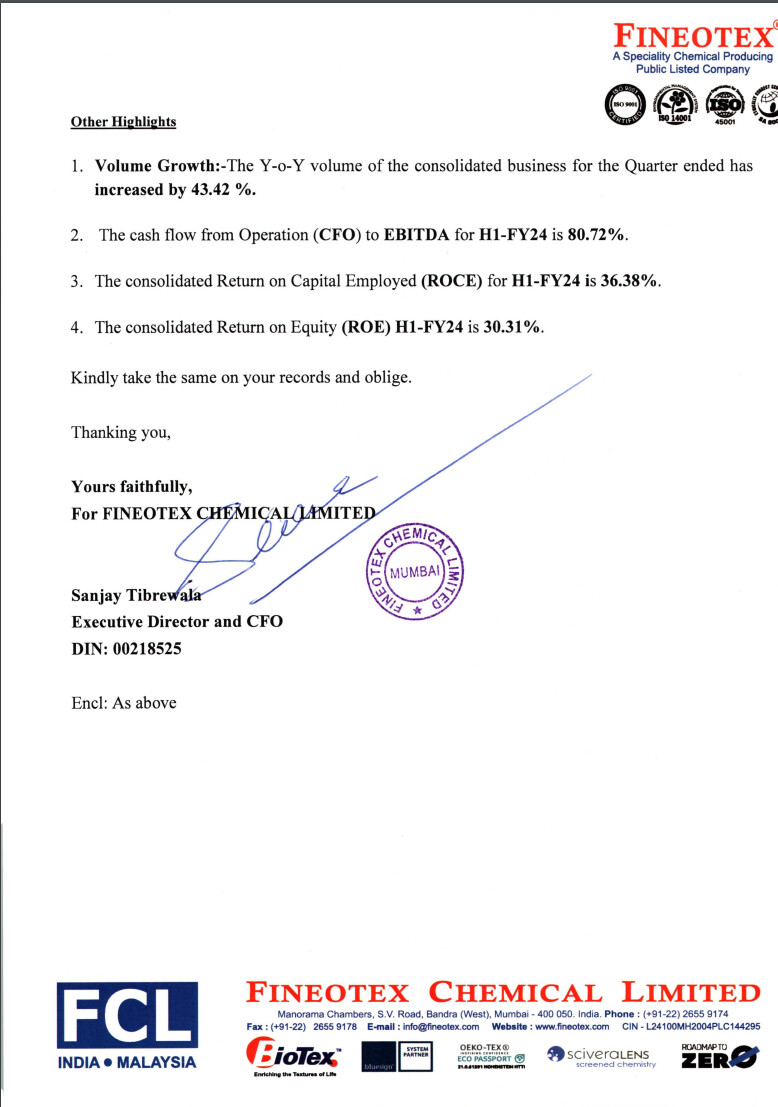

Additional Highlights:

- Volume Growth: The consolidated business witnesses a substantial year-on-year volume growth of 43.42%.

- Cash Flow Efficiency: The cash flow from operation (CFO) to EBITDA ratio for H1-FY24 stands at an impressive 80.72%.

- Return on Capital Employed (ROCE): The consolidated ROCE for H1-FY24 is reported at 36.38%.

- Return on Equity (ROE): The consolidated ROE for H1-FY24 stands at 30.31%.

6 Likes

Fineotex Chemicals

=======Sector: Chemicals

Know your Company -what speciality chemical sector and category falls into

About the company:

Once recognized primarily as a niche textile chemical producer, FCL has undertaken a successful transformation over the recent years, diversifying its portfolio to include cleaning, hygiene, oil and gas, and FMCG chemicals.

-

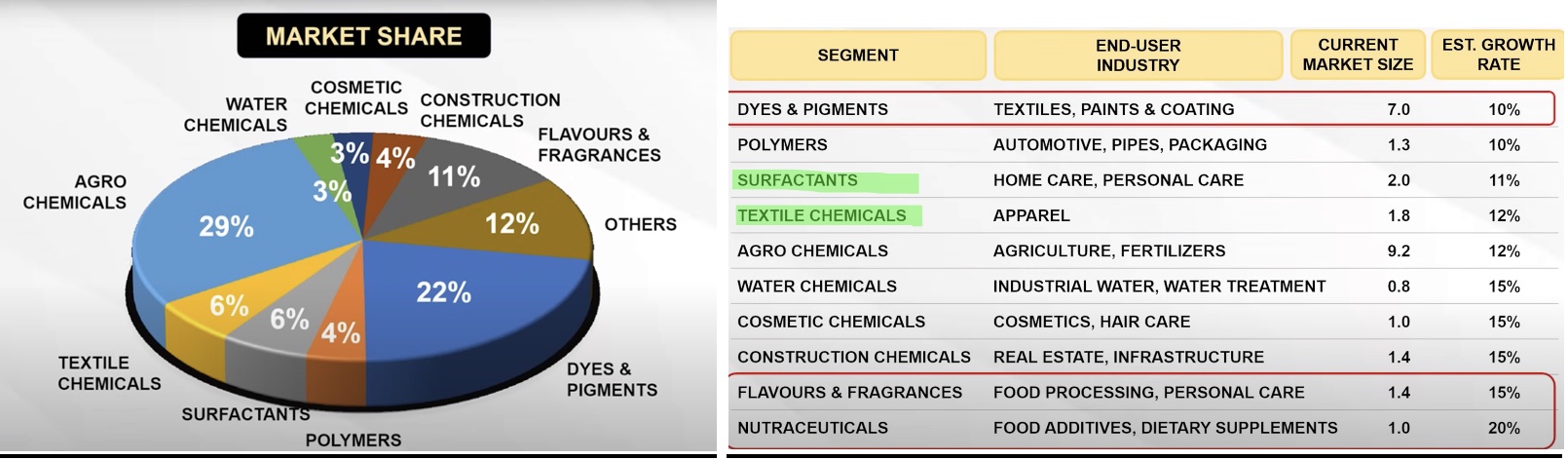

Fineotex Chemicals Limited (FCL) is a chemicals manufacturer operating in 4 segments:

o Textile Chemicals:(Pre Treatment products, Dyeing Products, Printing process products)

o Cleaning & Hygiene: 51+ products – Launched in 2020

o Oil & Gas: 13+ products

o Industrial Water Treatment: 5 products -

Company is a leading manufacturer of over 470+ specialty chemicals and enzymes.

-

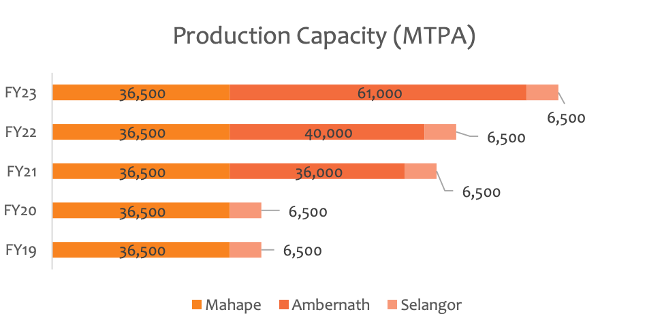

The company operates 3 facilities:

o Ambernath: 40000 MTPA + 21K MTPA added in 2022

o Mahape: 36,500 MTPA

o Malaysia: 6,500 MTPA

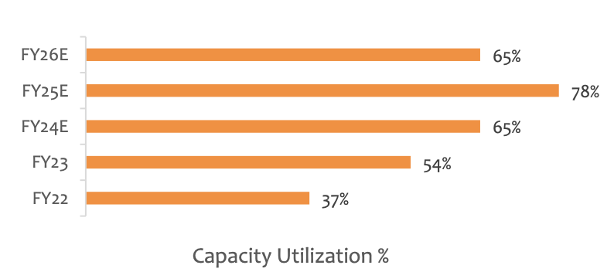

total installed capacity of 104,000 MTPA, capacity utilization @ 68% for Q2FY24 and @64% for Q3FY24 , max capacity utilization – ~80%

The primary drivers for increasing capacity utilization would be

-

Higher Export Turnover

-

Pick up in textile chemical segments

-

Expansion of Cleaning & Hygiene Product Portfolio

-

INR 35 crore spent through it’s a new wholly owned subsidiary FSPL Specialties Private Limited on 30th December 2023 for purchase of 7 acres of land, the land will be used to further expand manufacturing capacity. – Funded by internal accurals ***

-

Subsidary Biotex(Malaysia) acquired in 2011- spearheads their research and development initiatives

o specializes in high end specialty finishing textile chemicals like water & oil repellents, antimicrobials, etc. for textiles and also has a great presence in few segments for the paint sector. -

Joint venture-:

----- 2021 with HealthGuard ,Australia: enhance geographic reach and provide metal-free sustainable chemistry (no silver, no zinc, no copper) antimicrobial and anti-viral sustainable chemistry in the market.

----- 2021 Eurodye-ctc, Belgium: Through this joint venture, FCL will be bringing pre-treatment and dyeing products of Eurodye-CTC to the ever-growing market in India.

plan is to bring the entire Eurodye’s business to India and run it in Fineotex’s operations.

----- 2021 Sasmira,India: Setting up a state of art Research & Development centre with one of India’s premier textile institutes -

While the company captures the entire value chain for textile chemicals, focus is on the finishing process.

----Finishing chemicals have the higher margins and customer stickiness -

Have 102 distributors in India, global footprint in 69 countries.-:

o FCL works with key clients like Vardhman, Chenab Textile Mills, Welspun India, Only Vimal, Raymond, among others. -

Company is under process of releasing products for replacement of LABSA/Soda Ash for use in detergents, FCL has already received trial orders

-

Opportunities in Make in India initiative to drive further growth

Strength and Investment Rationale

Brownfield expansion in 1 year

- Acquisition about 7 acres of land next to the existing Ambernath Plant, the land has buildings already constructed as it was an existing plant for packaging and labelling products.

- company expects ~1-1.3 years for development and operationalization of the plant.

- Capex for new plant in range of 40-60 crore, and management expects it to complete it within 1-1.3 year

The plant is expected to be fungible like the Ambernath plant and will contribute to manufacture of both Textile and Cleaning Hygiene products.

Cleaning & Hygiene Segment to drive growth

Cleaning & Hygiene segment started by the company 4 years ago.

- Cleaning & Hygiene segment contributes to 56% of volumes and 41% of revenues for Q2FY24, this segment is poised for future growth with growing products like mosquito repellents, toilet cleaners,detergents, floor cleaners.

- Cleaning & Hygiene segment is mainly driven by B2B business

Established position in the specialty chemicals market and reputed clientele:

The company has a good standing not only in the domestic market but has also increased its global footprint, with a presence in around 70 countries.

FCL operates in an industry with high barriers to entry and high customer switching costs.

- The complete range of textile chemicals constitutes only 3% of the overall production costs for textile manufacturers.

- Customers prioritize timely delivery and performance over the cost of these chemicals. Moreover, there is a substantial risk associated with changing these chemicals, as they can potentially damage the fabric, thus ensuring customer stickiness.

This situation results in significant switching costs for manufacturers, acting as a deterrent for new entrants into the market.

Thus, FCL has strong multi-year relationships with major clients like Chenab, JCT, Aurodyne, Aurotextile, Mavi Spinning, Raymond, and Baswada. These premium clientele not only bring stability but also act as magnets for additional business opportunities.

Sustained growth in sales with robust margins

- FCL has had a good last 10 year track record, with 10/5/3 year CAGR in revenues of 38%/29%/49% as on FY23.

- This revenue growth has been supported by consistent margins with 5 year average EBITDA margins at 19% as on FY23, for H1FY24 the company posted EBITDA margins of 25%, highest so far.

- The PAT margins also stood tall with 5 year average at 15% as on Mar’23, and H1FY24 coming in at 21%.

Buoyant margins along with sales growth over such a long period inspire confidence in management.

Healthy operating efficiency and expanding into non-textile segment:

-

The capacities for the company are fungible across segments and products. The company is moving towards a balanced end user profile from the past textile concentrated end user.

-

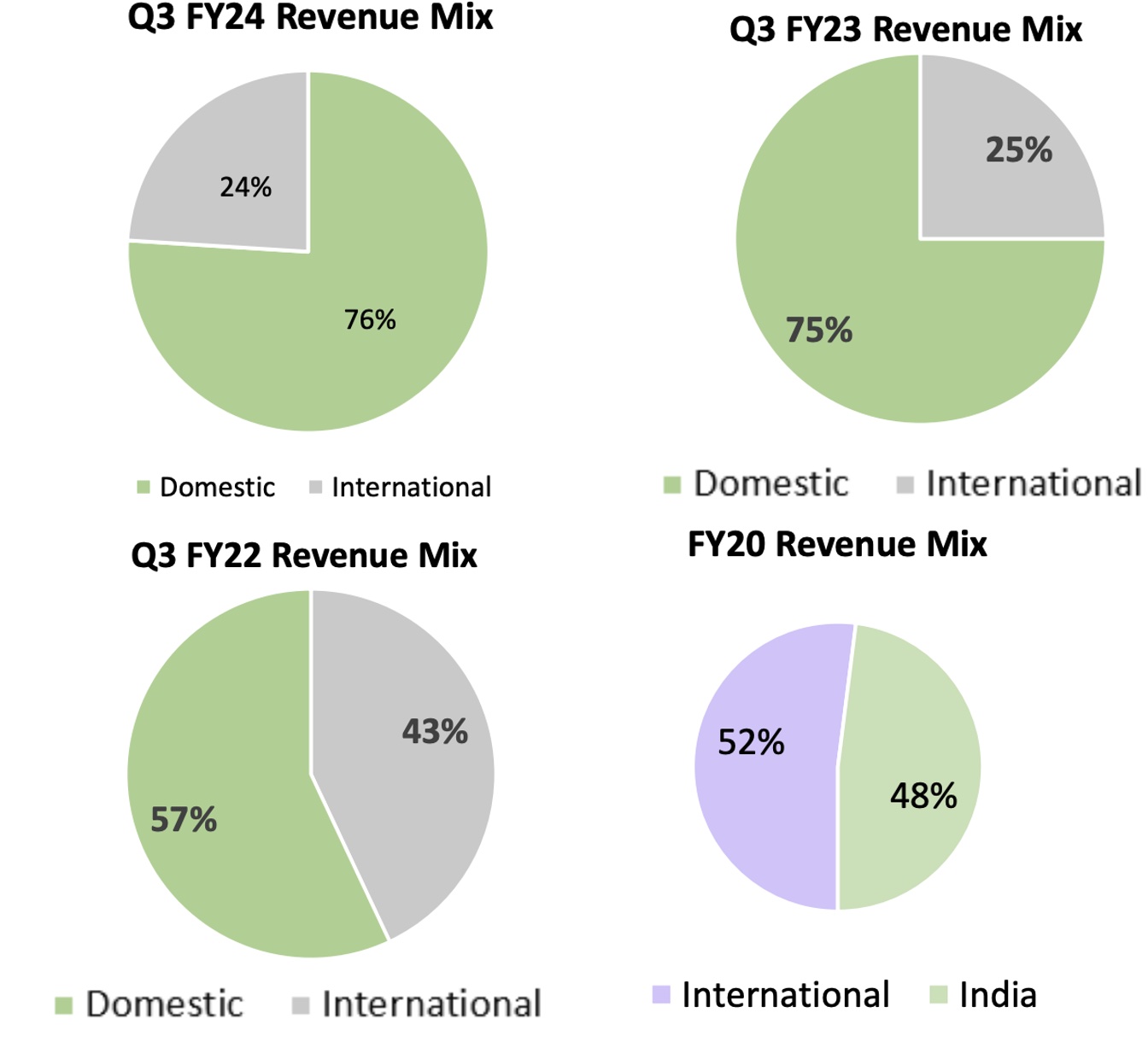

The company earlier had a revenue ratio of around 88:12 of textile vs non textile segment, in half year fiscal 2023 the ratio was at 61:39 and the company aim to sustain the ratio going forward.

-

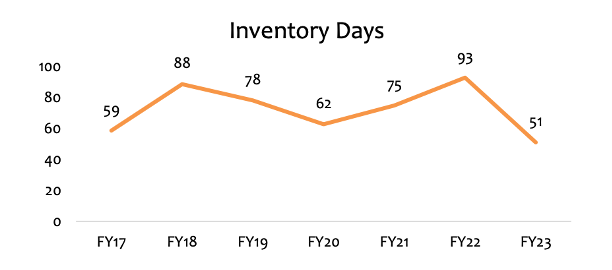

In the current fiscal, home and hygiene segment has enabled reduction in the debtors’ days from average of 110 days to 70 days, which has resulted in better accruals.

Solution based approach towards sales, with technical personnel guiding customers

- FCL follows a solution based specialty chemical approach, where it can customize and provide specialty chemicals based on the needs of the individual customer.

- FCL can thus provide better finishing/processing chemicals which adhere to local needs like hardness of water.

- The company offers customized technical solutions with the help of 34 technical experts who assist customers with their requirements, giving it more traction.

Strategic Tie-ups with Healthguard & Eurodye CTC

- FCL has partnered with HealthGuard, Australia for developing anti-microbial and anti-viral products and Eurodye-CTC,Belgium contributes specialized pre-treatment and dyeing products

Textile Chemical industry has been in a downcycle, poised for an upward trend

- Credit period for Textile Chemicals is 70-80 days and 30-45 days for Cleaning & Hygiene segment

Strong Focus on R&D

- Biotex - mosquito life cycle controller," which is used as a non-toxic and eco-friendly solution for mosquito outbreaks

- Sasmira

Main aim of research is to find sustainable chemicals that reduce water, energy, and time consumption in wet textile production

China +1

China is leading exporter for speciality chemicals. However its impacted in last 1-2 years. Reasons

- Chinese government has implemented more rigorous environmental regulations targeting chemical producers to manage air pollution within the country leading to relocation of plants and higher operation cost

- China labour costs increased

- Chinese green tax

o This action has diminished the cost benefit that Chinese producers previously enjoyed in comparison to counterparts worldwide. - Subsidies withdrawals

China’s commitment to maintaining its zero COVID strategy prompts end-user industries to seek diversification in their supply chains, potentially favoring exporters in the Indian specialty chemicals sector.

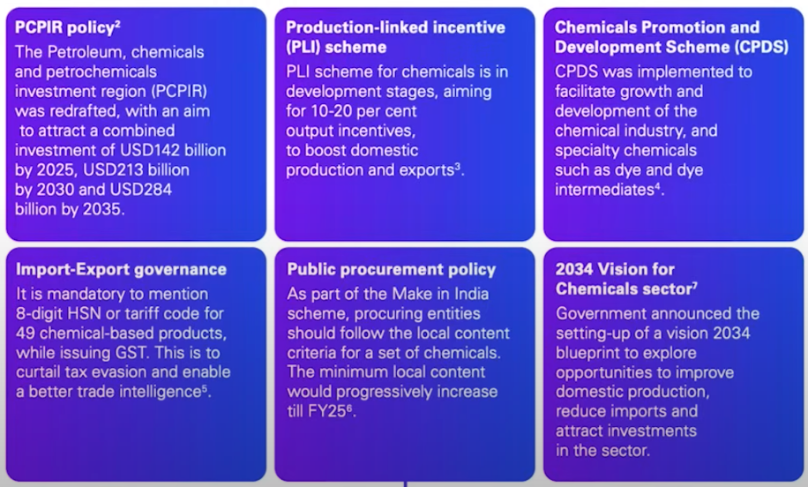

PLI’s and Policy Push by Indian Government for Speciality sectors

- The Indian government recognises chemical industry as a key growth element and forecast to increase share of the chemical sector to ~25% of the GDP in the manufacturing sector by 2025.

- Under the Union Budget 2023-24, the government allocated Rs. 173.45 crore (US$ 20.93 million) to the Department of Chemicals and Petrochemicals

- PLI schemes have been introduced to promote Bulk Drug Parks, with a budget of Rs. 1,629 crore (US$ 213.81 million)

Result Highlights for Q3FY24:

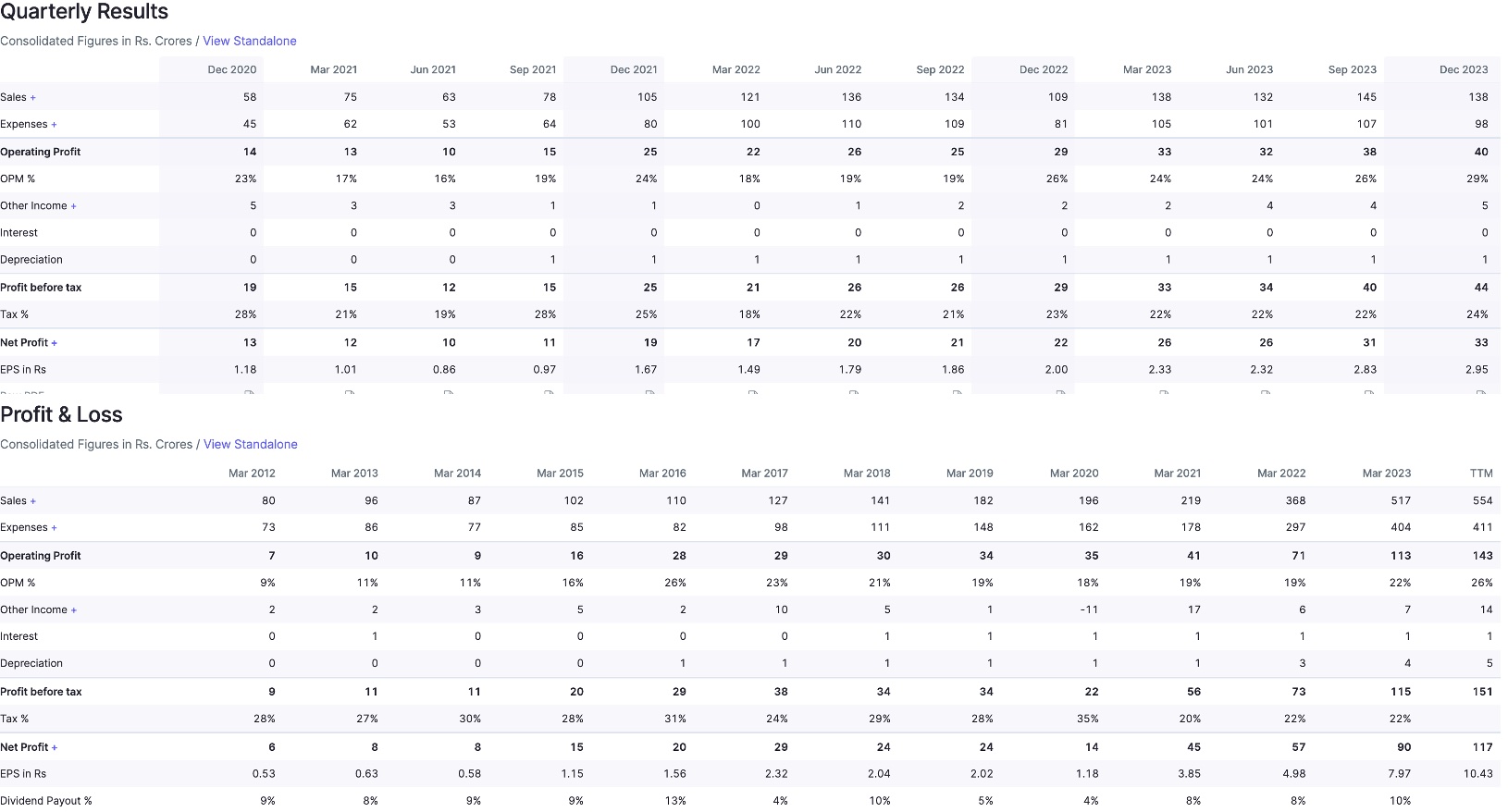

- For Q3FY24, Fineotex Chemicals’(FCL) posted a revenue of INR 1385 Mn growing by 26% YoY and -5% QoQ on a consolidated basis.

o For 9MFY24 revenue stood at INR 4160 Mn, growing by 10%. Volumes grew by 37% Y-o-Y - EBITDA stood at INR 404 Mn, on the back of 42% gross margins, with EBITDA margin coming in at 29%. with margin expansion of 301 bps. EBITDA for 9MFY24 was INR 1101 Mn growing by 38%.

- PAT for the quarter came in at INR 329 MN, with margins at 24%, expanding by 320 bps YoY, for 9MFY24 PAT was INR 905 MN growing by 42%. On a standalone basis FCL grew its PAT by ~100%.

- EPS for the quarter came in at INR 2.95/share, compared with INR 2 in the same quarter last year.

- For 9MFY24, the EPS stood at INR 8.10, comparing with INR 5.64 a growth of 43%. The Board of Directors have approved a dividend of 1.20/share, a payout ratio of 15% for 9MFY24.

Key Concal Highlights:

-

The company has an extensive range of products covering polymerization, phosphates, textile finishing chemicals, detergent chemicals etc.

-

FCL had a PAT of INR 329 Mn for the quarter with ROCE @ 31% and ROE @ 34%

-

7 acres new factory premises worth 35 crores funded by internal accruals, fungible plant, next to old plant.

---- Existing demand for specialty chemicals for textile, cleaning & hygiene, drilling specialty chemicals.

---- require for the commissioning of the chemical plants from the pollution and the government authorities.

---- for interest levels and joint venture tie-ups across specialty chemicals around 2026.

---- European and American companies, they do not want to depend on China for a lot of things.- come to India from the Make in India concept also -

There will be another Rs.40 crores or Rs.50 crores organic expansion, in near future. That is also broadly, it can be funded from the internal accruals.

-

Company is diversifying into complementary products for cleaning and hygiene, drilling specialty.- Volume growth (37%) primary driver of volumes. - Co. is set to raise 280 crores via a combination of equity shares and warrants, management is looking for opportunities for inorganic growth

-

RM prices have softened, FCL has passed on some of this benefit to the customers bringing down avg realizations to INR 82/T, this has also led to expansion of margins at the same time.

-

55-60% of volumes are from FMCG ,Cleaning & Hygiene segment and balance from Textile

-

95% of the capacities are fungible

-

Management expects prices for chemicals to increase going forward due to issues in Red Sea, wars and other macro events

o Companies/clients are also stocking up raw materials currently due to anticipation of delays of Red sea

-

Increasing cotton prices can lead to higher consumption of textile chemicals- Ambernath facility has structures ready and 20% of capacity can be expanded with 2 quarters. •

-

Management expects EBITDA margins to be sustainable at Q2/Q3 FY24 levels. With realizations coming down, EBTIDA will be sustained by lower RM costs

-

Additional 20% capacity expansion at Ambernath plant is ready with structures, the plant can be expanded by addition of machineries and the company expects once started, it’ll take 2 quarters to complete the addition

.

Product/Sales Mix

- Credit period for Textile Chemicals is 70-80 days and 30-45 days for Cleaning & Hygiene segment

Textile Chemicals

- 40% of volumes are from textiles.

FMCG and Cleaning & Hygiene

- 55-60% of volumes are from FMCG/Cleaning & Hygiene segment

Oil & Gas

The company has also ventured into speciality chemicals for oil & gas drilling and is in discussions with major players in this field. FCL has also received sizable orders from a leading oil and gas company India. There is significant potential for offering effective products used for drilling in oil exploratory process. This product line is in very early stages of prototyping.

Geography

Fundamentals

- High and steadily increasing EBIDTA margins.

- Good revenue growth

- The company has maintained a strong ROE/ROCE profile of 25% average over last 5 FYs (FY19-FY23), peaking in FY23 @ 34%

- Debtor days – reduced

- Strong Working capital - The current ratio of FCL has been consistent over the years in the range of ~3 to 4

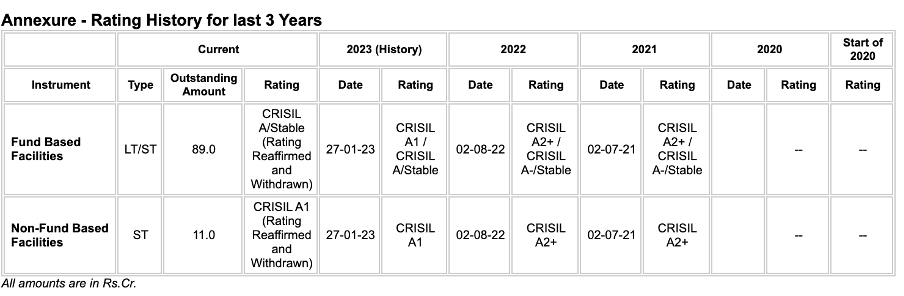

- Company has recently received upgraded ratings from ICRA, CRISIL

Lowest from the previous years at 51days showcasing a good working capital management.

- Good Promoter shareholding pattern

- DII’s reduced in 1.5 years

Industry Growth

Textile chemicals

FCL competes with global players like Archroma, Clariant, and Huntsman in this segment.

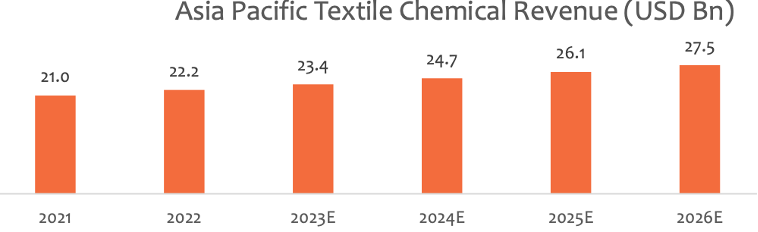

The escalating global need for finishes in technical textiles and home textiles is propelling the expansion of the textile finishing chemicals market. India’s contribution of only 9% to global cotton production, despite having the largest cultivated cotton area, suggests room for improvement.

Indian Textile chemicals market is expected to grow at 10-11% CAGR from 2023-28 whereas the $27B global textile market is expected to grow at 4-5% CAGR in the same period.

Indian textile chemical market is poised for growth due to rising global and domestic demands for high-quality textile products, an increase in textile production, favourable governmental policies, and a surge in international brands sourcing garments from India.

Cleaning and Hygiene Chemicals Sector

The Indian Home Care market is presently valued at INR 35,000 Crores and is to grow at 9-10% CAGR over the next five years. Although the per capita annual detergent consumption in India stands at 2.7-3 Kg, which remains lower compared to developed countries, this is expected to change.

Fabric care, making up 68% of the total consumption, is the most significant category, followed by dish soap as the second largest, and surface care, encompassing household cleaners and antimicrobial products, as the third largest.

Surge in demand for eco-friendly cleaners made from natural elements such as citrus solvents, corn starch, oxygen bleach, baking soda, and alcohol is amplifying this trend and driving market expansion.

GreyViews reported that the market size of floor cleaning and mopping machines in India reached USD 0.50 Bn in CY22 and is projected to achieve USD 1.2 Bn by CY30E. They anticipate a CAGR of 12.0% from CY23E to CY30E.

FCL competes with global players like Dow Chemicals, BASF, and DuPont in this segment.

Leadership

Mr. Surendra Kumar Tibrewala, Chairman & Managing Director

- Mr. Surendra Kumar Tibrewala is Chairman of the Board, Managing Director of Fineotex chemicals Ltd. He is a Commerce graduate from R. A. Poddar College of Commerce and Economics from Mumbai University and a Law graduate from Government Law College by qualification. He has started his career at the age of 20 in the Specialty Chemical Industry and has more has over3 decades of experience in this business of Specialty and Auxiliary Chemicals as trader, manufacturer as well as reseller. The business of the company has been nurtured since the last 30 years. He is also involved in other aspects of the business like marketing and administration.

For FY22, Remuneration received Rs 0.95 Cr which is 0.25% of Net Sales and 1.67% of Net Profit

Risk

Exposure to volatility in raw material prices:

- Raw materials are derivatives of petrochemical products, and their prices are therefore exposed to volatility in crude oil and other raw material prices.

- Additionally, 20% of the raw material requirement is imported, which is however offset by export earnings to cover the exchange fluctuation.

Though with formula-based pricing and favorable product-mix, exposure to such volatility is mitigated.

Exchange fluctuation is also offset by export earnings

Intense competition in the high-end performance chemicals segment from large European players, who are well established with a high capital base and dominate the market, is a key concern

My outlook for Fineotex Chemicals

-

Management has set a revenue target of INR 600 cr for FY24 which is easily achievable with the aim of maintaining current EBITDA margins. Subsequently, the company anticipates an earnings growth rate of 20-25% in the medium term

-

Current P/E ratio is 40 with share price of 426 , advisable to wait for the price to normalize to P/E of 32-35 and price of 350-380 range

-

Believe the sudden rise of share price from 323 to 450 in last 2 weeks happened due to strong set of numbers by company and also since company announced the dividend payout

-

Fineotex is a company in speciality chemicals who is deploying all the right strategies , company has grown multi-folds in last few years and based on the above analysis I don’t see the growth stopping now

-

Indian Textile chemical market is having a CAGR -10-11% , Indian GDP growth is expected to be 7-8% so sector has above average growth rate

-

Cleaning and Hygiene sector also has a CARG 9-10% which establishes sectors growth as pretty high compared to GDP growth

-

Profit Margins are consistently increasing , subject to raw material costs fluctuations

-

Creating capacity takes time , the capacity utilization has been increasing and company is expanding capacity which means that company is getting/anticipating long term contracts from its customers –Good sign.

-

Not having issue of customer concentration – Have a wide number of customers.

-

Customer stickiness – with big multinational companies

-

75% of business is domestic , which is a good sign, Lesser dependency on exports issues , forex fluctuations , Geography concerns – Less Risk

-

Company has been expanding into new segments – Exploring into Oil, If unlocked then that will add into their revenue

-

company is building brands which will help in getting premium – Finocon , Ecodo, CleanJet

-

No major Red Flags-: No major debt.

Recommendation: Buy at right valuation is key, stock is predicted to consolidate and a good price should be 380-400 rs and if it consolidates further can be purchased more.

This definitely looks like a very strong fundamental company and should be in one’s portfolio for long term.

Sources : Trendlyne, Screener, company website, News Articles, Company presentations, Earning calls, Company Annual Report, KrChoksey report, Credit Reports, Speciality Chemical sector data, and ofcourse Google.

35 Likes

A short video covering both Ami Organics and Fineotex Chemical.

Just sharing.

3 Likes

I will be going for a plant visit next week. Let me know if anyone would like to know about anything specific or any questions for the management.

6 Likes

Got to know about entry barriers and customer stickiness in textile segment. Just wanted to know about how is the competitive landscape and customer stickiness in cleaning and hygiene segment?

KR Choksey has given a price target of Rs. 571 in their latest report.

1 Like

Hi Kartik, Can you please share the data points based on your plant visit if you don’t mind. Thanks !!

3 Likes

Q4 FY2024 FINEOTEX CHEMICALS CONFERENCE CALL

100 kW Solar plant commissioned.

Easing of chemical prices help expand EBIDTA margin.

ICRA upgraded rating.

ESG badge received.

Expansion Plan:

7-acre land from internal accruals of 35 cr. At ambernath plant for land and building, work already begin. Total 50 cr. Capex required for phase I.

It is fungible capacity, with better technology, increase volume and cater to all 3 streams textile/hygiene/oil drilling. It will for new/existing products.

Phase I will be 20000 T will be commissioned by FY2025, Phase II will be 20000 T, but cost and time will be lower due to infrastructure will be in place.

Looking for international acquisition with matching return ratios. It will be international and due diligence in progress.

Growth:

Confident of accelerated growth and efficient return ratio. What done in last 4/5 years had been done, can be done in next 4/5 years in percentage terms.

Business details:

Q4 volume contribution of textile and hygiene is 50%.

FY 2024 volume contribution of textile and Hygiene is 45%/50%.

Overall capacity utilization is 72% as of Q4. India is going to be specialty chemical hub of the world. Optimal capacity is 80%.

25% volume growth in total.

Company is not only for import substitute. Company also looks for export.

Other expense mostly related to exhibition and trade shows promotions.

From DOW/BASF material must come in 3 months and in drums. Fineotex supply in tanker load, which is preferable.

Previous FY was remarkably price correction; however, company manage EBIDTA. Average realisation prices must go up for chemical industries.

Textile is going to come back, which will be very helpful to company.

Raw material price increase passed to customer as Purchase Orders are for 1 to 2 months.

Sustainable solution provided by company is key and company provide those solutions. Fossil fuel-based chemicals will be stopped.

Fund raise

109 cr. by preferential issue at price of 387. 40, as per filing on Saturday as below link.

Conference audio:

D invested.

3 Likes

Hi,

Could you pls share your view post plant visit.

Thanks

1 Like