I had a brief look at this company, please be very careful while valuing this company, the margins have doubled in the last year due to imports are restricted and some domestic capacity has not come up and price and margins are strong. This cannot sustain for long for sure. The market will revert to mean.

Stock is still a commodity stock and for the last six years EBITDA is only 8% and ROCE is 15%. This year can be an exceptional year like we see in many commodity stocks. Note the tax last year, the pat% is high because of tax rebate.

This stock can do better considering reduction in debt and other reasons mentioned in their ppt. But need to be careful of the entry point.

Yes this is in a commodity space as you mentioned and one needs to be careful about their entry price

for any security.

I just want to highlight that there are a lot of potential tailwinds and positives to consider for rerating

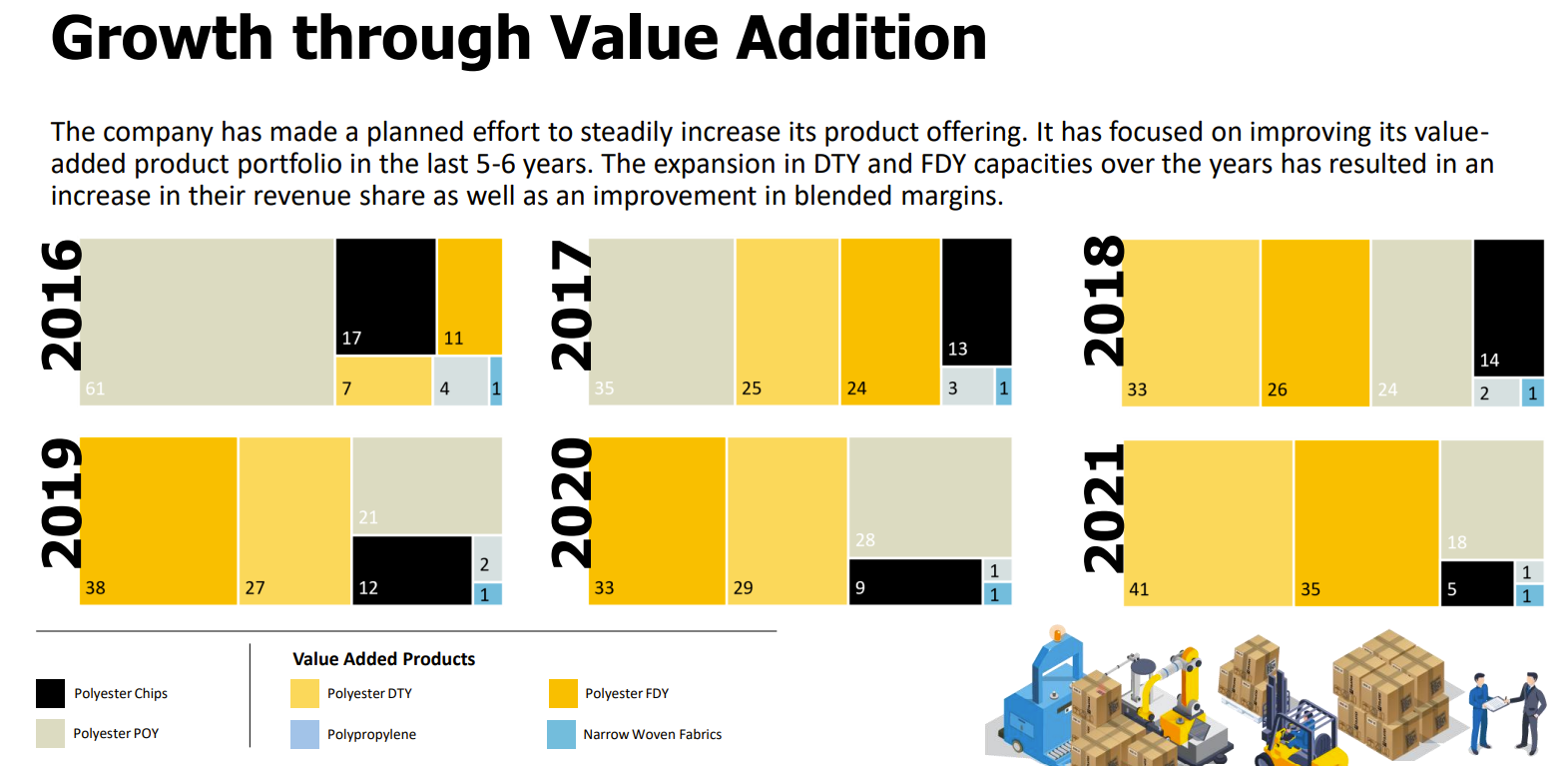

(1) If you check their history, they have been shifting to value added products more and more to improve margins. Their FDY & DTY are fetching higher margins with Bright FDY > Semi dull FDY > DTY > 10%. These filament lines are running at near full capacity utilization (90%-95%) and their combined share is about 70%. The company is going to move away from POY (8% margin) & chips (2-3% margin) and continue the shift to Value added profile.

The incremental production is being absorbed into the market due to high demand for their products since the imports of fabric from china and bangladesh has gone down substantially creating a fillip for local fibre. Globally, the increase in demand each year is 3-3.5 million tons and my understanding is such volumes cannot be supported by China and also there is no major capacity being added in the near term (2-3 years) in india due to raw material constraints. It was indicated that Reliance/Indian Oil will probably only be able to add raw material capacity end of FY24. You are correct that the Bhilosa capacity lost due to fire is being brought back by end of the year. However, that will take care of only 4-5% of the demand and the actual demand is expanding in double digits leaving room still for margin improvements. So we are talking tight supply for next 2-3 years atleast as demand for synthetic yarn is very high.

(2) Also current export situation is not conducive due to shortage of containers and freight rates continue to be high. Once these constraints elapse, their export volumes will pick up growth wise and they would definitely do better than FY21.

(3) It will be a bonanza for the textile sector if and when the government will consider one GST rate for the complete textile value chain and the management has indicated that the concerned govt. officials are supportive in principle and interested in providing stimulus to this labor intensive sector. If it happens, it will be a huge boost for domestic production and growth. There is also an expectation of announcement for PLI scheme for garments made from man made fibre which could be forthcoming this quarter as per what management shared in the recent con call.

(4) They are also focussed on innovation and have a product development team to develop specialty yarn like hollow POY, multiple profile yarn and other such products which are currently imported.

(5) They are planning capex for recycled fibres using chemical process which will sell at a very good premium above virgin fibre in the future cos there is a commitment from big international brands & insistence from fashion industry and they are not able to avail the quantity (currently they can only get upto 20% of what they require). This indicates a multi year strong demand for this production line. They are projecting a ROCE of 40% when this comes online sometime in FY23. They are indicating EBITDA of 120 crores for this with revenue generation of 300 crores

(6) Commisioning of the captive power plant with annualized savings of 45cr to the bottomline

(7) Capacity expansion this year for putting up more DTY with 100cr outlay

(8) Management has indicated efforts to be undertaken for removal of pledge this year and there has been consistent improvement in net debt equity ratio (from 2.28 in FY16 to 0.72 in FY21).

Decent results considering the environment. Margins should move up from here as volumes and share of value add products go up but the real kicker will come from 100 TPD plant for chemical recycling which should be ready by end of FY23. Even Their only competitor in India- polygenta doesn’t have the capability of converting polyester yarn(only PET bottles) to virgin polyester. Hopefully by FY23 this commodity company will no longer get commodity valuations

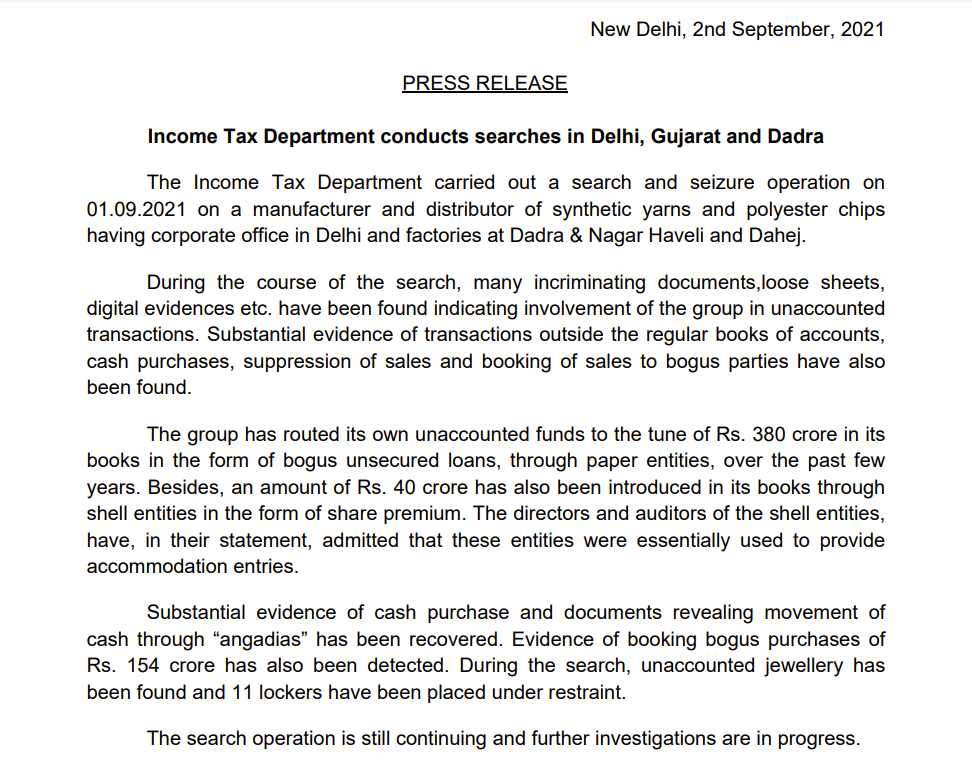

Any reason why the stock price is not performing according to the quarter results. The valuations are getting very attractive & near term earnings visibility is also good. Is Income tax raid final decision an overhang which has led to this underperformance ?

Not able to share reasons on price performance since i relate it to supply/demand pressures that can provide us with both reasons to enter/exit. Banking more on their potential, good business developments and growth indicators for long term performance.

As for the IT raid, its an ongoing assessment and a long process. Currently there is no claim or demand outstanding from the IT department.

They have guided for FY22 revenue to exceed Rs. 3,500 crores and margins to be slightly better than Q2 which implies that Q3 & Q4 would be at least as good as Q2. My conservative guess is an FY22 EPS of 12. Their capacity utilization was 93% in Q2 and demand is strong enough that they are expecting it to continue on that high mark.

Bankers have released 100% of promoters pledged shares.

Debt to Equity ratio has reduced from 0.77 (Q1) to 0.56 (Q2)

Recycled Yarn can become a big opportunity for them in future.

Inspite of good performance over the last few quarters the stock has been a laggard versus other textile names. Most likely the recent IT raid and absence of any major capex in yarn is ailing the stock. (Currently at 100% capacity utilisation. Doing some debottlenecking)

That is likely to change after successful commission of chemical recycling plant for filament (Pilot in April 22. I am guessing another 15-18 months for a full scale plant). With this Company is venturing in to unchartered territories and there will always be doubt regarding any novel idea until market sees execution.

In Q3 con-call management hinted at not being interested in being just another commodity player hence no announcements of capacity addition in yarn. focus will be to scale up recycling plant and then decide on further capex.

Successful ramp up of recycling plant could significantly re-rate this stock.

Disc: invested

Edit: on Q3 con-call management mentioned that they are planning a buyback/dividend. If done this should help improve perception of management

Sharing my notes on the opportunity and concerns in Filatex. Thought I’d flesh out all the details since the thread is very sparse.

Summary of talking points:

Company has changed its product mix from products that offered 2-7% margins to products that offer 13-14% margins. Are these margins sustainable, or the cause of an upcycle?

Company is piloting production of recycled polyester. This may potentially have an initial margin profile of 30%+ should the test be succesful.

Company had an IT raid last year. Can we trust their numbers?

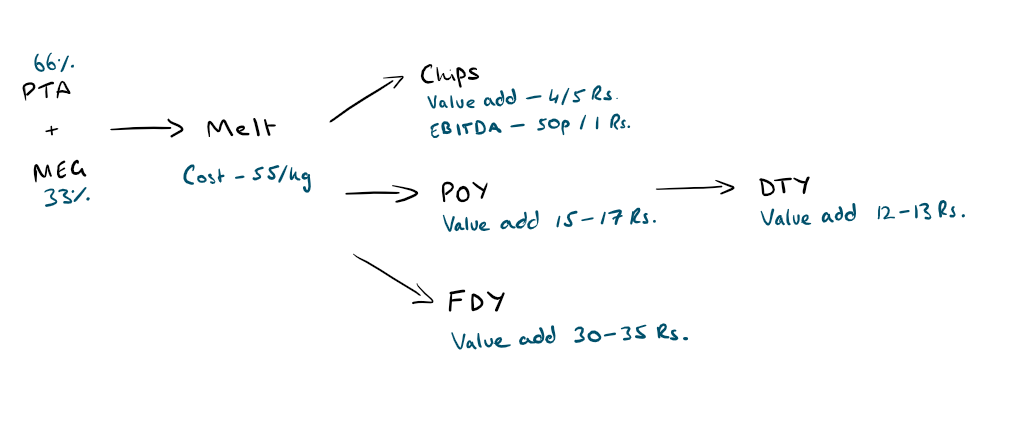

Note: these spreads were taken from a concall in 2016. Management explained the value chain with example numbers. Actual spreads will be different on today’s market prices.

With this in mind, the change in product mix explains their improving numbers over the years.

Compare this with the value chain and realisations given above. Note how in 2016, POY and Chips were the major offerings (Value add of 15 Rs. and 4 Rs. respectively), but today the pie is formed from the higher value add products of FDY and DTY.

Secondly, their key RM of PTA and MEG had anti dumping duties revoked in 2020, as the government is trying to encourage growth in the textile industry.

One wonders if the steady state margins for these value add textile products should be in the 14-15% range, not the 10% seen before 2020.

2. The rPET Opportunity

,

As part of a new wave of sustainable products in the West, a number of global fashion brands have committed to using recycled fibres in their clothing lines, and a plan to phase out new fibres, opting to use recycled materials instead.

Looking at the value chain, the polyester melt is the focus of recycled polyester. The idea is to use plastic bottles or other sources to form this polyester melt, rather than having to produce it afresh from PTA + MEG. Once you have a recycled polyester melt, you can use your existing spinning machines to produce recycled yarn fibres at no additional cost.

There are two paths to producing this rPET melt, physical treatment and chemical treatment. Physical recycling is the process of collecting used plastics, and mechanically crushing them into a suitable form. This is a tough process that numerous countries in the West have struggled with.

Firstly, one needs to collect a large amount of plastic bottles, and without a good recycling program that starts at the level of households, this is almost impossible to do efficiently. In the domestic listed space, Ganesha Ecosphere is a company that works on mechanically recycling polyester. The second drawback has to do with the look and finish of mechanically produced rPET.

The idea behind chemically recycled polyester is to use the waste produced in manufacturing PET to produce the same polyester melt. This is tough on account of finding the right catalyst for the process, and this is a relatively new technology.

@GARP_niveshak raised the idea that Filatex shouldn’t prima facie have any expertise in chemical recycling, as not many have cracked the technology. It turns out that the landscape is different from what the management alludes to in the concall, and a lot of firms have made progress.

This is taken from a sustainable fibres summit, held by Textile Exchange. Filatex’s management has pointed out that Polygenta is the firm they’re looking to compete with in India, but there are a few more that produce rPET.

Indorama is another global leader that has invested in rPET technology and has made significant progress, but it remains to be seen what their commitment is to the listed Indian division.

The movement aims to accelerate the adoption of recycled polyester from 17% in 2025E to 45% in 2025E.

We’ll know more in the next concall what Filatex’s process looks like, and whether the test has been successful. As it currently stands, the expected margin profile of rPET based fibres is around 30%, and will taper with time, as more and more production comes online. This is the scope of opportunity, and depends on how fast Filatex can scale the technology.

IT Raids

The IT department made a fairly damning statement last year when it searched Filatex’s premises:

Management has denied all allegations, and there hasn’t been any subsequent charge as yet. The market hasn’t punished the company. From my scuttlebutt, I’m leaning towards this being politically motivated, than there being substance to the allegations, but welcoming thoughts from investors.

Ganesha Ecosphere has been given a much higher multiple by the market despite having a weaker margin profile. Should this pilot be successful, the narratives of sustainable fibres and a stronger margin profile could see Filatex seeing better ratings, but will the market ignore the raids…

There is a second opportunity in Filatex doubling their textile capacity, but details will only come in the next concall.

Revenue up 45% YoY but operating probits and Net profits are down. NP declined by 17%.

Underwelhming performance mainly due to high crude prices exacerbated by the Ukraine war and the company’s inability to absolutely pass in the inflation to the customers.

It is intriguing how the company will fair in this high inflation environment.

Does anyone know how Filatex can develop pricing power? Is it just a function of size?

And what are your views on management’s decision to buy back shares, preferentially from promoters, at 140 even though the open market prices were lower? Is there any substance behind the IT raid? @Chins

The strengthening of the USD, high freight costs along with rising raw material costs due to high crude oil prices resulted in lower margins. The company failed to pass on the inflation due to low demand.

The pilot recycling plant that was set up for testing has received quality assurance certificates from independent parties.

The management team doesn’t want to take up any big projects till the global environment becomes better.

The company is looking to add Taconic polyester chips.

In Q1Fy23 the company’s EBITDA/KG was around ₹9/KG but the management believes that the sustainable figure is between ₹13-14/KG.